Börsipäev 11. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Nädalavahetusel kirjutas Barrons 2007. aasta väljavaadetest turul ning suurem osa analüütikuid olid positiivsed. Siia otsa sobib kohe järjekordne kommentaar GDP käekäigu kohta:

Friedman Billings says on Dec 4, their Chief Economist Steve East reduced his 2007 real GDP growth ests and trimmed his 10-year Treasury yield forecast to 3.90% by 2Q07-end. His revised ests imply a deeper yield curve inversion in 2007 than previously and slower economic growth but still a "soft landing" for the economy. While the yield curve's shape remains uncertain, the forecast suggests a tough operating environment for banks. Accordingly, firm contacted their companies to discuss the dynamics and implications of greater inversion in the first half of 2007 and a flat curve at year-end. They conclude that this scenario would negatively affect all cos, but those with small securities portfolios, significant fee income, mortgage banking operations, escrow deposit businesses, and/or efficiency initiatives would appear best positioned.

Deutsche Bank upgrades DirecTV (DTV 24.28) to Buy from Hold and raises their tgt to $30 from $20, as they believe DTV is best positioned to take advantage of high-definition, will likely become part of the Liberty media empire resulting in a more appropriate capital structure and more aggressive deal making posture and its valuation is attractive despite their forecast still coming in below management's long-term guidance

Prudential upgrades Time Warner (TWX 20.91) to Overweight from Neutral and raises their tgt to $27 from $21, as they believe cable marginexpansion will be much grater than they had initially forecasted and think prior estimates for Time Warner Cable are out of date and conservative

Jefferies upgrades Adobe Systems (ADBE 38.88) to Buy from Hold and raises their tgt to $45 from $35, based on higher conviction in the CS3 product cycle, see less risks than previously before the product cycle and think consensus estimates will increase for FY07

JP Morgan downgrades Wendy's (WEN 34.75) to Underperform from Neutral

UBS downgrades Steel Dynamics (STLD 35.14) to Neutral from Buy

Banc of America downgrades Federated (FD 40.38) to Neutral from Buy

-

Kui eelmises postituses oli juttu majanduskasvust, siis Merrill toob siia võrrandisse sisse ka veel naftahinna:

Merrill Lynch cut its estimate for oil prices next year, because of slower economic growth and increasing supply, but hiked its target for the commodity in 2008 on expectations demand will rebound. The investment bank now sees oil at $60 a barrel, down from its previous forecast of $65 a barrel, and crude rising to $62 a barrel in 2008, from its earlier prediction of just $50 a barrel. Merrill also boosted its forecast for natural gas in 2007 and 2008. -

Goldman kommenteerib vee-ettevõtteid, pidades sektorit pikaajaliselt atraktiivseks ja kaitsvaks:

Goldman Sachs says that water remains an attractive long term 4-6% defensive growth sector. Firm says the NYSSA water utility conference last week reinforced conclusions from their recent survey of water utilities, and they expect to see utilities continue spending on upgrading infrastructure, put through price increases, adopt advanced water treatment technologies, and engage in further industry consolidation. Firm says the number of water pure-plays has been evaporating and scarcity value has elevated valuations, and says the best-positioned takeout candidates are Badger (BMI), Hyflux, Tetra Tech (TTEK), Sinomem, Aqua America (WTR), Pentair (PNR), Calgon (CCC), Pall (PLL), and Nalco (NLC). -

Juba reedel tähelepanu all olnud Citigroup iga seoses täna jälle teateid:

The Chinese government said Sunday it will consider allowing eight foreign banks, including

Osana paketist, millega Hiina pidi nõusutma WTOga liitumisel. Veel esitasid avalduse HSBC Corp; Standard Chartered PLC; ABN Amro Holding NV; Mizuho Corporate Bank ; Singapore's DBS Bank; Hong Kong Bank of East Asia ja Hang Seng Bank.

Siiski, midagi pööraselt suurt on siit raske loota, Hiina pangad on kasvõi kontoriketi arendamisel saanud väga suure edumaa aga eks see oli ka Hiina eesmärk.

Lisaks spekuleeritakse, et just C tegi pakkumise Prudentiali Egg ostmiseks. Siiski tundub, et vaatamata kahjumi tootmisele pole PRU üksust veel maha kandnud.

-

Lisaks usub Goldman, et AMD ja TXN võivad oma tulevikuväljavaateid kärpida:

Goldman Sachs expects TXN to lower its guidance during its mid-qtr update tonight toward the low-end of current $3.46-3.75 bln range/EPS $0.40-0.46. While firm still thinks TXN is overvalued at $29, they don't think that this update will be a negative trading catalyst, as the Street is well aware of the weakness this qtr. In addition, firm believes that AMD's analyst meeting on Thursday may serve as a negative catalyst for the stock, as they think AMD is likely to lower Street Q4 rev and gross margin expectations in light of weak pricing as well as the integration of the ATYT acquisition. Firm also says there is some downside risk to LSCC's Q4 guidance for rev and gross margin due to the same supply chain inventory correction that is hitting others in the sector... Firm also says Dec NAND contract prices, released last Friday, showed significant price declines of 10-25%, depending on the configuration. -

UBS cuts their PMCS ests based on recent negative checks at the ITU Telecom World show suggesting further delays in China's 3G build out, negative mid-qtr updates from ALTR and XLNX, wireline capex delays in Japan, and near-term PON sales volatility. Firm cuts their tgt to $9 from $11.

UBS raises their KBH tgt to $60 from $52, reflecting a higher multiple off trough EPS. Firm notes that KBH announced pre tax land impairment charges, and they expect similar charges from peers moving forward. -

Shark on korduvalt välja toonud, et pikas ja äkilises tõusutrendis on näha jahtumise märke, samas, jätkuvalt on ta arvamusel, et enne tõeliselt selget ja üheselt määratud märki turu pöördumisest, ei oleks mõtekas agressiivselt langusele panustada.

Leave Prognosticating to the Pundits

By Rev Shark

RealMoney.com Contributor

12/11/2006 8:57 AM EST

Click here for more stories by Rev Shark

"In the long run the pessimist may be proved right, but the optimist has a better time on the trip."

-- Daniel Reardon

One of the pitfalls for poor performance is to focus so much on what problems may occur in the long term that you miss today's opportunities. Many traders have a tendency to form long-term investing theories but then make the mistake of thinking they have to act on them immediately. They end up missing out on the many short-term opportunities as they wait for the big-picture theories to kick in.

The long-term big-picture arguments are difficult for many investors to resist. The media, traditional Wall Street, and even our conversations with friends and family tend to make us feel like we should be thinking in that manner. It is expected that we have some theories and ideas about where things are headed because all of the pros in the media focus on that sort of thing.

When drawn into a stock market decision I surprise people all of the time when I tell them I really have absolutely no idea what the market will do next year nor do I really find it worthwhile to spend much time thinking about it. I don't need to worry about it in order to be successful; I just need to deal with the shorter term and then the longer term will take care of itself. If the market is going to roll over or explode upward it is going to take some time getting there and that journey will be all the information you need to properly yourself.

Correct long-term predictions can be good for the ego and attract media attention, but they don't equate to profits. Success in the market is dependent on good discipline and the ability to react as events unfold. Plodding along day after day, finding some good buys and making sure you don't suffer any major damage will lead you to the promised land.

The fellow who is busily preparing himself for the disaster that is sure to come at some point suffers huge economic costs as he misses out on opportunities now. Even if you believe the market is on the verge of breaking down any day, you can still find opportunities on the positive side as you wait for the damage to occur.

Today we have a mild positive start but not quite as upbeat as many of our recent Monday mornings. There were a few bright spots mainly overseas but no big blockbuster. Oil and gold are down and the dollar continues to rally.

We have the Texas Instruments (TXN - commentary - Cramer's Take - Rating) midquarter update after the close tonight, which will put some focus on chips today but more importantly we have the FOMC interest rate decision tomorrow afternoon. No one is expecting it to make a move but that doesn't mean the decision won't be closely studied and have some market impact. -

Ülespoole avanevad:

VIFL +21% (new possible e coli cases in Iowa -- AP), GSOL +20% (Cramer bullish on Mad Money), MIND +14% (reports OctQ), TSG +12% (co is on the auction block - WSJ), CPHD +10% (receives 510k FDA clearance for SmartCycler), ARDI +8.6% (to be acquired by TRMB), TARO +7.7% (fund in talks to acquire co - Reuters), CLE +6% (moves closer to a sale - WWD.com, also reporter on CNBC says co could be in takeover talks), CGA +6.5% (CSN Brazil tops Tata in bid for CGA), TGEN +6.5% (extends recent momentum, +200% in a month), CBAK +6.2% (reports SepQ), BMET +5.3% (takeover speculation), GERN +7.5% (positive clinical data), JAV +5% (NGN Capital co-founder named to the board), ISYS +3.9% (reports SepQ), ICE +3.5% (Goldman raises tgt to $130), MOS +3.3% (Cramer bullish on Mad Money), LVLT +3.1% (to be added to Nasdaq 100 index), PD +1.9% (SAC Capital discloses 5.1% stake), ALU +1.8%, TWX +1.1% (Pru upgrade), AAPL +1% (positive comments from Goldman), NOK +1%, HPQ +1% (CFO to retire), F +1%... Under $3: FORG +4.6% (extends Friday's 70% move).

Allapoole avanevad:

NUVO -81% (Phase 3 blood thinner results did not meet expectations), TSM -12%, MDCO -6% (expect weakness following failed patent legislation extension - RBC), TLK -3.3%, BCS -2.8% (profit taking after big move last week), ELN -2.1%, HLYS -1.8% (profit taking after successful IPO deput Friday), KOSP -1.5%.

Ja lõpetuseks üks arvamus endise Citi tehnilise analüüsi osakonna juhilt Louise Yamada'lt:

Louise Yamada, former head of technical research at Citigroup, is reiterating that gold is cheap and the metal is the purest play vs the dollar. Yamada sees gold surpassing $730 next year on its way to $3,000 within a decade. While we agree that gold is the place to be longer term, this morning the price of gold may be weaker due to a pullback in energy prices and a rise in the US dollar on the heels of the Bank of Japan making cautious comments on interest rates (dollar also higher vs the euro due to speculation the ECB will slow the pace of rate increases). -

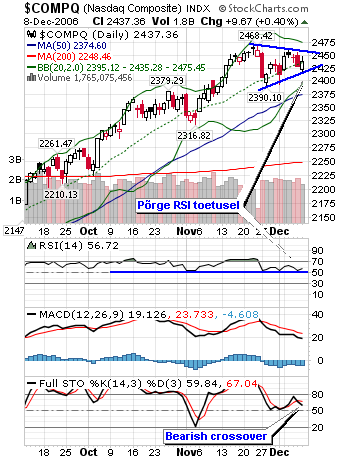

Tänased varajased futuurilepingud peegeldavad lõppenud nädala teise poole sündmusi. Töötururaportist leiti tuge ning see kajastub ka tänases eelturus. Graafikult näeme, et Nasdaq on teinud väikese põrke lühiajalisel tõusutrendil. Samad põrkekohad on kenasti ka RSI toetuskohale projekteeritud. Nimelt RSI toetusest läbi vajumist oleks võinud tõlgendada olulise negatiivse signaalina, nüüd siis näidati jällegi kauplejate poolt suhtelist tugevust. RSI ülemine kauplemisvahemik jääb aga ülehinnatud piiridesse ja olen üsna skeptiline taas üle 70 piiri ületamise suhtes. Indeksi volatiilsus on langenud ning kauplemisvahemik kitsamaks jäänud. Turu hirmuindeks VIX andis aga reedel pisut järele, kuid kauplejb jätkuvalt ülalpool 50 päeva libisevat keskmist. Selle nädala makrosündmused pakuvad kindlasti indeksite külgsuunalisele liikumisele väheke vaheldust, muuhulgas ka 12 detsembri FOMC. Täna on ka toornafta jaanuarikuu futuurilepingut pisut järele andnud, mis peaks julgust ja positiivsust päevasisesele kauplemisele juurde lisama.

-

Tänane päev on huvitav, kuna borker/dealerid (MER; LEH; GS; BSC) näitavad nõrkust hoolimata pangandussektori tugevusest. Alanud nädalal on antud sektorist ka tulemusi oodata. Lisaks on terasesektor suhteliselt nõrk (X, STLD - $STQ) hoolimata Corus Group (CGA) ümber toimuvast. Suhteliselt nõrk on peale jõulumüügiperioodi ka jaemüügisektor (RTH) samal ajal, kui turg plussis ning väiksemate ettevõtete liikumist kajastav IWM on plusspoolel vaid marginaalselt. Ei ennusta turu tippu, kuid nii mõnedki märgid hakkavad pigem seda teesi toetama.