Börsipäev 18. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

PKN has 84.36% of Mazeikiu, takeover bid expected. According to an announcement by Mazeikiu, PKN became the holder of 596,834,352 shares of Mazeikiu Nafta on Friday (84.36%). The total price paid amounted to USD 2.343b. Also, CEO of PKN Orlen, Igor Chalupec was elected the Chairman of the Board of Mazeikiu Nafta. At the same time, Polish daily Rzeczpospolita speculates that Kazimierz Marcinkiewicz, former Polish PM, may become the new CEO of PKN Orlen. The company also said in its stock exchange release it will submit a takeover bid to acquire the residual shares of Mazeikiu Nafta.

Starman's DTT launch successful. Estonian cableTV provider Starman launched digital terrestrial television (DTT) services at the beginning of December. On Friday, the company announced that they have run short of set-top boxes (STB) necessary for the new service. In the last couple of weeks, Starman has already installed 1,500 STB's. Before Christmas, the company hopes to receive another 10,000 STB's. Longer term goal set by the company is to have ca 50,000 customers in two years. Hence, DTT will not have a significant impact on Starman's performance in short term. However, in longer term, revenue from the new service will cover the fixed costs and probably add another income source.

Apranga store opening. The Lithuanian clothing retailer opened an Apranga (whole family concept) store in Marijampole town in Lithuania, which is the 18th store opened this year. In addition to luxury stores in the Baltic capitals, the company also focuses on the economic segment in regional centres. Apranga stores are intended for entire family and offer garments manufactured by largest European companies and broad variety of Lithuanian manufacturers. Currently, the company operates a chain of 65 stores, and another three stores are expected this year.

Olympic opens new casino. The Estonian casino operator Olympic Casino opened its 22nd casino in Estonia (40 slots, 3 jackpot systems, bar). The total investment amounted to EEK 14.4m (ca EUR 1m). At the end of Q3, Olympic had 73 casinos in 5 countries; at the moment, they have 77 casinos and in the next couple of months, the number should increase to ca 83-88, according to the company (Q3 report).

Real estate prices falling in Tallinn. According to BBN, the average price per square meter in Tallinn has recently been falling between EEK 1000 and 3000. The biggest decrease in prices has been for one-room apartments, which now cost in average EEK 24,900 per square meter, while in Q2 the average price was EEK 27,700 per square meter.

Ukraine November GDP up 8.2%. According to Ukrainian Statistical Office, November real gross domestic product grew by 8.2% y-o-y. During the period of January-November, GDP went up by 6.7% y-o-y to UAH 452,939m (EUR 69,68m). The main growth drivers were retail trade (+15.6% y-o-y), transportation (9.8%), production and distribution of electricity, gas and water (+7%).

-

Merrill Lynch downgrades Foot Locker (FL 22.93) to Neutral from Buy

JP Morgan downgrades Sealy (ZZ 15.80) to Neutral from Overweight

Merrill upgrades Citigroup (C 54.07) to Buy from Neutral

Goldman upgrades Baker Hughes (BHI 78.25) to Buy from Neutral

Citigroup upgrades U.S Concrete (RMIX 6.05) to Buy from Hold

➤ We are upgrading US Concrete from Hold to Buy, as we believe that the stocksunderperformance has significantly priced in residential construction risk, whileother sectors of construction appear to be in an upward trend. We increase ourtarget price from $8 to $8.50/share.

➤ Our 2006/2007 EPS estimates decline by one penny each (now $0.47 and$0.63). Although near-term earnings risk persists, we believe that investorsshould get in to the name now: the stock is trading below 3Q06 book value of$7.59/share, while our construction equipment dealer sentiment indexregistered its 2nd monthly improvement (after 6 months of declines).

➤ We maintain our Speculative risk rating on US Concrete. We value the stockon '07 multiples of 10.5x P/E (from 65% to 60%), 5.5x EV/EBITDA (30%) andDCF (from 5% to 10%). We concluded that it is not totally fair to overemphasizevaluation based on 2007E (which is not normalized). Target $8.5.

HSBC downgrades Eli Lilly (LLY 54.52) to Neutral from Overweight and cuts their tgt to $55 from $60.75 based on lower-than-expected operational and financial leverage. As a result, the firm says the exposure to a Zyprexa induced EPS decline in 2012 is increased. The firm says good medium term sales growth not enough to drive outperformance in 2007

Friedman, Billings downgrades Exxon (XOM 77.30) to Market Perform from Outperform and $78 tgt, based on valuation

Friedman, Billings downgrades Total (TOT 72.52) to Underperform from Market Perform and $66 tgt, based on valuation

Credit Suisse initiates PeopleSupport (PSPT 21.01) with an Outperform and a $27 tgt given the strong demand trends, stable pricing, methodical capacity expansion plans for PSPT and its voice-focused peers and the continuing migration of U.S.-based call center seats offshore.

-

China's banking regulator said Monday it approved the sale of an 85.6% stake in Guangdong Development Bank to a Citigroup Inc.-led consortium for 24.27 billion yuan, or about $3.1 billion.

C osa GDBs 20%. Saab endale umbes 500 kontorit ja $6 mld halbasid laene.

-

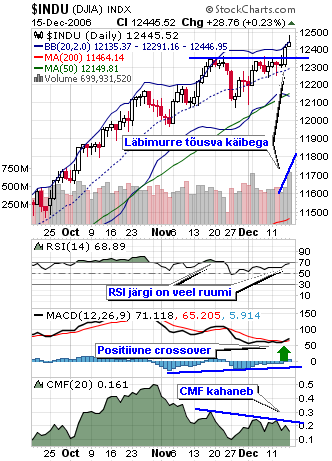

Nädal algab tehniliselt üsna positiivses pildis. Nii Nasdaq kui Dow tegid reedel tugeva käibega tõusupäeva. DJIA tegi oma kõigi aegade tipu, murdes varem paika pandud vastupanu. Nasdaq testis päeva sees novembri tipp, kuid sulges sellest allpool. Täna on juba eelturu roheliste futuuride toel avanenud mõlemad plusspoolel. Nasdaq kauplemisvahemik on jätkuvalt kitsas. Swingimise seisukohalt oleks positiivse signaalina MACD crossover. RSI on teinud mitu toetust ning see tase on korraliku põhjana toetust leidnud. Samas tõusupäevadel tahaks RSId suhteliselt tugevamana näha, et tõus jätkusuutlik oleks.

DJIA on pisut positiivsem, kuigi ka siinne CMF näitab, et käive ei toeta tõusu. Siiski on viimaste päevade kauplemine tehtud tõusva käibega, mis näitab liikumise olulisust. Indeksi volatiilsus on kohe ka suurenenud. Ka siin tahaks näha RSI samasuunalist liikumist, mis näitaks tõusu tugevust. MACD crossover näitab, et kahe libiseva keskmise vahe hakkab taas suurenema, millest on mõni aeg juba MACD histogramm teada andnud. MACD histogramm näitab MACD ja seda siluva libiseva keskmise erinevust.

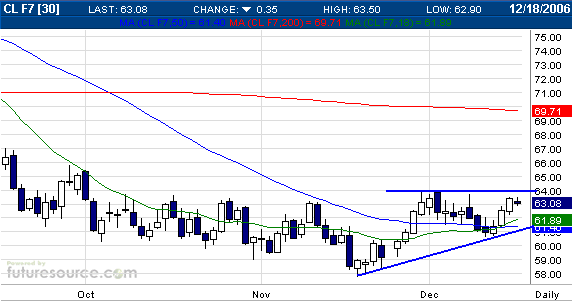

Toornafta futuurid on kergelt järgi andnud ning kauplevad 63 dollari peal. Vastupanu 64 juures.

-

Väikse hilinemisega ka Sharki kommentaar. Taaskord big-capid fookuses ning Shark juhibki tähelepanu, et suured ettevõtted on olnud viimasel ajal muljetavaldavamad kui väikesed. Näiteks GE üks viimaste aastate suurimaid rallisid reedel, mis on ka täna jätku saamas.

Singing the Big-Cap Blues

By Rev Shark

RealMoney.com Contributor

12/18/2006 8:50 AM EST

Click here for more stories by Rev Shark

"The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails."

-- William Arthur Ward

Although the major indices continue to sail ever higher, the winds driving them are gusting in unusual fashion. This isn't a market driven by astute stock pickers looking for bargains and overlooked stories; it is a market driven by a sea of cash that is looking for a place to go and doesn't much care as long as it is in the equity market.

The action Friday was a particularly good example of how recent market action is driven by macro matters, allocations and program trading. The positive CPI news happened to hit on option expiration day, which produced a big open because many were not positioned well and had to scramble to reposition.

But in addition to the option games, the huge moves in a few big-caps like GE (GE - commentary - Cramer's Take - Rating) and Citigroup (C - commentary - Cramer's Take) relative to the mediocre performance in the Russell 2000 was quite telling. There was obviously a lot of money that wanted into the market but it flowed to the path of least resistance, which is a few mega-caps. The action in GE, in particular, was quite startling. There was no news, no analyst action and nothing that would seem to attract buying but the stock made the single biggest daily point move it has seen in many years. The only explanation is a huge level of liquidity and a limited amount of options.

We are now down to the last nine trading days of the year, which tend to have positive seasonality. When you consider that, coupled with the obvious liquidity out there, this market has a lot of pressure on it to at least hold up if not rally a little further.

The problem many like me are having with this market is that individual stock-picking is pretty much irrelevant. The way to glean profit is to be in front of the places where liquidity is flowing, and that isn't the quality small-caps that I generally prefer. I may actually have to hold my nose and buy some mega-caps if this indiscriminate buying continues.

Obviously the indices are in very good shape but I have no qualms admitting that I do not like the market here and find it extremely hard to buy. I spend a lot of time working on a list of potential buys and there sure isn't much on it. That doesn't mean the market is going to roll over but it does make it hard to do anything major on the buy side. -

Oracle'il puhtalt numbrid ootuspärased, kuid järelturul aktsia languses.

ORCL reports Q2 new license revs $1.207 bln vs street expectation of ~$1.25 bln

ORCL prelim $0.22 vs $0.22 Reuters consensus; revs $4.2 bln vs $4.16 bln Reuters consensus

Reports Q2 (Nov) earnings of $0.22 per share, excluding non-recurring items, in line with the Reuters Estimates consensus of $0.22; revenues rose 26.5% year/year to $4.16 bln vs the $4.16 bln consensus. Co reports Q2 new license revs $1.207 bln vs street expectation of ~$1.25 bln. "... We continue to gain market share in applications from SAP, in middleware from BEAS, and in database from IBM. In Q2 our middleware new license growth was exceptionally strong. We expect to pass BEAS in total middleware new license sales later this year..."