Börsipäev 20. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Baltic Morning News

December 20, 2006

Ventspils Nafta wants to sell printing? Ventspils Nafta has started talks about media business sales but it is not ready to release any plans, BBN wrote this morning. The plot of land under the high rise building Preses Nams, owned by Ventspils, has become a goldmine. Olga Petersone, chairwoman of Ventspils opens that sales of media business is possible, at present it is not being discussed. In Q3/06, printing services made up 26% of the company's sales. However, it is not entirely clear how big share of the business they are willing to give up.

Merko wins a tender. The construction company Merko in consortium with two another Estonian construction companies, Terrat and Amaks, has been awarded for a bid to perform construction works of the pipelines and sewerage project for Matsalu Veevärk, a water utility company in western Estonia. The total value of the order is EUR 25.1m (+VAT), equal to 12% of Merko´s total revenues in 2005. However, it was not disclosed what was the Merko´s stake in the bid. Environmental projects will come into focus in the coming years as record high EU grants are expected for this area (around EUR 620m in utility sector between 2007 and 2013).

PTA acquired another 2.7% of shares in Milavitsa. Silvano Fashion Group, a fully owned subsidiary of PTA, announced it had acquired 331 shares in additional voluntary takeover bid for minority shareholders of Milavitsa. Silvano paid EEK 3.4m (EUR 0.2m) for 331 shares or for 2.7% of the share capital. The initial plan was to acquire around 5% of the company for EEK 6m. Currently, Silvano owns 62.5% of shares in Milavitsa.

Tallink's hotels get new name. The Estonian shipping company Tallink announced that they will gather their hotels under new hotel chain brand Tallink Hotels. At the moment, the chain will consist of the old Tallink City Hotel as well as the new Tallink Spa & Conference Hotel, which will be opened in the spring. The share is up ca 8% in last two days. However, the recent news is hardly behind the rise, since it is basically non event for the company.

Kalev buys another publishing company. The Estonian candy maker Kalev announced it had acquired full ownership in publishing company OÜ Olliwood, which is mainly known for publishing two magazines, Just and Basket. A few weeks earlier, the company also acquired a publishing company and a local newspaper.

High export growth from Baltics. According to Eurostat, of all EU countries, the highest increase in exports in 9 months was noted in Luxembourg - up 37% yoy. Estonia and Lithuania came in 3rd and 4th with exports up 25% yoy. Latvia's growth was the 10th highest (up 18% yoy). In import growth, Latvia was first with 31 percent, Estonia was fourth and Lithuania was fifth - i.e. no ease on current account deficit.

Lithuanians feel happier than ever. The Lithuanian newspaper Verslo Zinios writes that people in Lithuania have an increasingly better sentiment about their personal life and national economy. According to Eurobarometer survey, two-thirds of Lithuanians are satisfied with their situation. The number of people believing that their life will improve in the next 12 months has increased 6 pct points to 43% year-to-date. Also, more than a third (37%) are positive about the economic situation in Lithuania, and more than half (53%) believe that employment opportunities will improve in the coming months.

-

Deutsche Bank initiates Knight Trading Group (NITE 19.24) with a Buy and $25 tgt, saying the co is well positioned to benefit from market structure changes, secular growth in electronic trading and peer to peer execution through its integrated low- to-high touch model...

Stifel Nicolaus initiates Hansen Natural (HANS 33.34) with a Buy and $42 tgt, as the co is growing share in a category that they find established but underdeveloped and find valuation compellingSunTrust initiates Rosetta Resources (ROSE 18.30) with a Buy and $30 tgt, based on exposure to robust N. American natural gas fundamentals, multi-year drilling inventory in core areas and capital productivity that is 20% superior to coverage portfolio

Goldman removes Genentech (DNA 80.78) from their Conviction Buy list.

Goldman adds MedImmune (MEDI 32.59) to their Conviction Buy list

CIBC downgrades Juniper Networks (JNPR 19.25) to Sector Performer from Outperformer, as they believe upside in shares is limited given the more formidable edge competition of an RBAK/ERIC combination and waning possibility of an acquisition premium

Baird downgrades Kohl's (KSS 71.89) to Neutral from Outperform and $79 tgt, based on difficult comparisons that could become a near-term overhang for sentiment, the expectation of less incremental benefit in F07 from key F06 drivers and Q406 upside that may be limited by unusually warm weather

Jefferies initiates FiberTower (FTWR 5.85) with a Buy and $12 tgt, as the co's wireless backhaul network is well positioned to capitalize on the anticipated growth in backhaul services driven by massive wireless infrastructure deployment and demand for high bandwidth services and applications

J.P Morgan adds General Electric (GE 38.01) to their Recommended Portfolio and removes Northrop Grumman (NOC 67.28)

Goldman upgrades Symantec (SYMC 21.39) to Buy from Neutral

FDX FedEx reports Q2 (Nov) earnings of $1.89 per share, excluding $0.25 non-recurring charge related to new labor contract, $0.13 better than the Reuters Estimates consensus of $1.76; revenues rose 10.3% year/year to $8.93 bln vs the $8.94 bln consensus. Co issues downside guidance for Q3, sees EPS of $1.20-1.35 vs. $1.55 consensus. FDX sees Q4 EPS of $1.98-2.13 vs $1.98 consensus. Co issues in-line guidance for FY07, sees EPS of $6.60-6.90 vs. $6.82 consensus. CFO comments, "Earnings for our second quarter were better than forecast primarily due to lower than expected fuel prices, slightly stronger than anticipated growth at FedEx Ground and insurance proceeds related to Hurricane Katrina. Our earnings guidance for the third quarter recognizes a difficult year-over-year comparison, as last year's third quarter benefited from the timing lag that exists between when we purchase fuel and when our indexed fuel surcharges automatically adjust. December 2005 fuel surcharges at FedEx Express and FedEx Ground were set during the period fuel prices had spiked following Hurricane Katrina. We remain optimistic that we will continue to improve full-year margins and returns during a period of moderate economic growth."

-

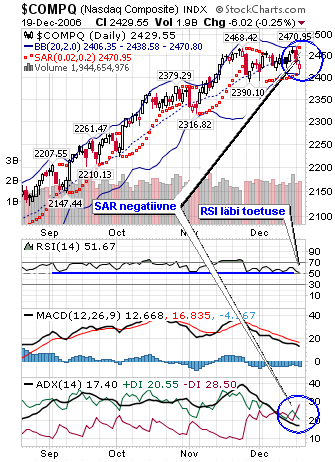

Varajased indeksite futuurid on rohelised ning peale eilset selloffi indikeerib see positiivset starti. Hoolimata sellest on lühiajaline nägemus siiski üsna karune. Täna lisan graafikule SAR indikaatori, mis on loodud stop-tasemete selgitamiseks. SAR toimib hästi trendivatel aegadel, kuid võib anda palju valesignaale. Vaadates Nasdaq graafikut näeme, et üsna mitu korda on SAR olnud ülalpool indeksit, mis sisuliselt tähendaks lühikeseks müügi võimalust, kuid tegu on valesignaalidega. SARi valesignaalide leidmiseks võib kasutada Wilderi DMI indikaatoreid. Ehk, juhul, kui DI ristumisi toimunud ei ole, ei ole ka SAR andnud õiget signaali. Näeme, et eilne kukkumine on tinginud SARi lühikese positsiooni stopi ning ka Wilderi indikaator on teinud ristumise. Aga selge on see, et see pole absoluutne tõde. TA järgi on siiski tegu selgelt bearish nägemusega.

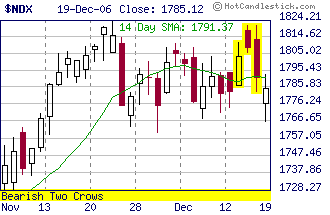

Küünalde jälgijatele on Nasdaq 100 teinud enne eilset allamüüki "Bearish Two Crows" mustri.

-

Nafta varude tänaselt raportilt oodatakse toornafta vähenemist( ca -2mln barrelit) ning seoses pisut soojemate ilmadega ootavad osad turuosalised ka kütuse suuremat kulumist(rohkem autoga sõitjaid). Veebruari nafta futuur on ka plussis - varude vähenemine toornaftas oleks 4. järjestikune.

Ülespoole avanevad:

ENCO +24% (announces contract With major pharma co for a phase 3 trial), RBAK +18% (to be acquired by ERIC +1%), MDTL +16% (successful UL test), ICOS +15% (co accepts LLY's sweetened takeover offer - WSJ), KOSN +12% (signs stomach drug pact with Pfizer), SYX +12% (reports Q3), ALTU +11% (announces collaboration with Genentech), ESCL +13% (extends yesterday's 92% move), KMX +7.7% (reports NovQ), EVST +7.6% (up on CNBC segment that it's a play on Rocky movie), FFHL +7.5% (extends yesterday's big move on IPO debut), RPRX +6.5% (positive phase 3 data), EDA +6.1% (extends yesterday's 15% move), SMOD +4.7% (reports NovQ), NBIX +4.7% (initiates clinial trial, receives milestone payment), NHWK +4.6% (Morgan Stanley upgrade), INWK +4.4% (Cramer bullish on Mad Money, says stock has a long way to run, see our recent profile), CMED +4.7% (successfully develops reagents), GMST +4% (extends yesterday's 13% move), KF +3.9% (fund announces distribution), MAMA +3.3% (extends momentum, +140% in a week or so), SYMC +2.2% (Goldman upgrade), UMC +1.5% (files Form 6-K), PAY +1.4% (Cramer bullish on Mad Money, he sees a big upgrade cycle coming; also see our recent Small Cap Focus), HNZ +1%, PALM +0.5% (reports NovQ, beats by $0.02, but guides below consensus).

Allapoole avanevad:

NFLD -48% (disappointing clinical trial data for blood substitute), PANC -36% (disappointing clinical trial data for Bevirimat), SBH -17% (loses exclusive distribution rights with L'Oreal, also downgrades from Pru and OpCo), FOXH -14% (guides lower), GBX -13% (guides NovQ below expectations), TRAC -8.4% (extends recent weakness), FSII -6.1% (reports NovQ, beats by $0.03, but light on revs, guides FebQ revs lower), GMXR -5.6% (provides operational update), DRYS -5.5%, FDX -3% (reports NovQ, beats by $0.13, but guides FebQ below consensus), EXAR -2.9% (lowers rev guidance), CBK -2.2% (reports Q3, guides Q4 below consensus), JNPR -1.5% (CIBC downgrade), TSM -1.2% (extends recent weakness)... Under $3: VXGN.PK -22% (says US cancels anthrax contract), GNVC -16% (announces stock offering). -

Miite just alati ei ole aasta viimased päevad positiivsed. Kas või eelmisel aastal oli lühiajaline tipp Nasdaqis 13. detsembril ning vaikselt aasal mõnulevat pullikarja(kusjuures veel endaga rahulolevat), on karupoisid väga valvsad üllatama.

Gauging Pullback Odds for Year-End

By Rev Shark

RealMoney.com Contributor

12/20/2006 9:03 AM EST

Click here for more stories by Rev Shark

"Trust everybody, but cut the cards."

-- Finley Peter Dunne

The vast majority of traders seem to trust in the idea that the market is going to hold up and, more likely, move steadily higher into the end of the year.

There is good support for such thinking: Upside momentum remains strong, the charts are in good shape, a constant barrage of mergers and acquisition keeps sentiment positive, and seasonality is positive. Why would anyone worry about the market now? There are no negatives. We should all be long and riding the momentum train.

Certainly we shouldn't be wasting our time anticipating great disaster, but that doesn't mean we should be so trusting that we aren't prepared for the conventional wisdom to falter. This is a market unconcerned about and unprepared for a pullback and anyone who has been in the market for a while knows that this sort of complacency is extremely dangerous. That doesn't mean we panic, sell everything and load up on shorts. However, the smart market players remain very aware of the quick damage that can be done when a large faction of the market is caught by surprise.

I spent some time yesterday looking over charts in the past year and studying the action at the end of December. Although seasonality supports a strong finish, it is by no means a certainty.

We need look back no further than last year as an example. We had a big rally off the lows of October but topped out on Dec. 13. The Nasdaq was down three of the four days following Christmas and lost 44 points. We had much the same talk then about investors holding up the market and preserving gains, and that resulted in some being caught by surprise.

I believe there is a good likelihood we could see a similar type of pullback before year-end. I'm not saying the market is going to fall apart and go straight down, but there are so many folks looking for a simple and positive finish to the year that the market beast just has to be licking his chops looking to bite some bull butt.

We have a slightly positive start this morning following a good day overseas. Oil is up and gold steady. There are a few merger deals on the wires and the tone is generally positive, but has been slipping slightly as the open approaches. -

Kas keegi oskab kommenteerida GLD käitumist. Täiesti arusaamatu.

-

Toornafta varud vähenesid -6.3 mln barrelit vs oodatud -2 mln

Distillaatide varud suurenesid +1.2 mln barrelit vs oodatud -0.6 mln

Mootorkütuste varud suurenesid +1.0 mln barrelit vs oodatud +/-0.0 mln

Renkler,

Mis kulda(GLD) puutub, siis hinnatõusule aitaks kindlasti kaasa kõrgemad kütusehinnad ning eilsed Föderaalreservi liikme Fisheri poolt öeldud sõnad, et inflatsiooni tõustes ei jää Fed-il midagi muud üle, kui intresse tõsta. -

Vabandan. Huvi pakkus QLD imelik käitumine. Peaks plussis olema, aga on 5% miinuses.

-

Kuna tegu on võimendusega kuubikute suhtes ja kuubikud rohelises, siis on ka QLD plussis. Üheks põhjuseks, miks nominaalilt hind langes, võib-olla dividendid...kuigi otsest uudist kohe hetkel ei leia

-

Yahoo näitab IYR'i plussis ??

-

Cloroxi Colgate diil, mis tegelt aktsiat lühiajaliselt diludib, mõjub kuidagi positiivsena

-

Diversifikatsioon on üheks põhjuseks arvatavasti. Mäletamist mööda oli CLX tooteliin suhteliselt tühi. Eile ei langenud ka aktsia eriti UBS kommentaaride peale.