Börsipäev 4. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Baltic Morning News

Apranga (Acc.) December sales +54% = in line. The Lithuanian clothing retailer Apranga posted December sales of LTL 32m (incl. VAT), equal to y-o-y increase of 53.9%. The highest growth in December was recorded in Estonia where sales increased by 88.7% y-o-y (the company added 2 new stores to the existing one at the end of October). The second fastest growing market was Lithuania with an increase of 53.9% y-o-y, followed by Latvia with an increase of 40.7% y-o-y. By adding together monthly sales, the total revenues in 2006 increased 49.1% to LTL 299m (incl. VAT). For the full year, we are looking for a pre-tax profit of LTL 22.4m, corresponding to a pre-tax margin of 8.8% (in relation to net sales).

Klaipedos Nafta December results. The Lithuanian sea terminal operator Klaipedos Nafta transshipped 388K tons of petroleum products in Dec/06. Hence, the transshipment volume for Q4 is ca 1,213K tons, which is 200k more than in Q3, but approximately 400k less than in Q1 and in Q2. It is also 20% less than Q4/05.

Gas price increase agreed. Yesterday, Latvian Gas announced that they have signed an agreement with Gazprom on natural gas purchase price for 2007, which envisages growth of purchase price for approximately 50% at the current heavy fuel oil prices. Now, Latvian Gas can submit a tariff project to Public Utilities Commission (PUC), after which the tariffs will be decided. We see this as one of the most important short term factors affecting the share price.

CEO of Grindeks to step down. Valdis Jakobsons, CEO of Grindeks, decided to step down as chairman and he will be succeeded by Janis Romanovskis, who is currently working as finance and administrative director. However, Mr. Jakobsons will stay with the company and will be responsible for research and product development including setting up a new research centre.

Rokiskio Suris reorganizes. The Lithuanian dairy company Rokiskio Suris said it wanted to separate fresh milk production from cheese production by transferring LTL 26.85m in fixed assets to its controlled dairy Rokiskio Pienas. The assets comprise production facilities and equipment of dairies Utenos Pienas and Ukmerges Pienine. We do not see this to have any major effect on share price performance.

-

Eile õhtul langetas Hot Topic (HOTT) oma neljanda kvartali kasumiprognoosi (Q4 guidance to $0.20-0.22 vs $0.33-0.38 previous guidance) ning kauples järelturul üle 10% madalamal:

Co lowers Q4 guidance to $0.20-0.22 vs $0.34 consensus, down from $0.33-0.38 previous guidance. Co reports Dec comp store sales -5.1% vs -3.4% Briefing.com consensus. "We are very disappointed by our consolidated December results and their implications for the quarter. As a result of lower than expected sales at the Hot Topic division, particularly during the first half of the month, promotional activity was increased relative to our plans. Although sales in our licensed and fashion novelty tee classifications for both mens and womens established solid positive trends, many of the music and fashion categories performed worse than anticipated. As a result, we are revising our earnings expectations for the fourth quarter to begin 2007 in a clean inventory position. The revised guidance reflects a comparable store sales decline in the mid single digit range for the quarter and increased markdowns to aggressively address the resulting inventory risk. We expect inventories at the end of the fourth quarter to be roughly flat to last year on a per square foot basis."

Citigroup kommenteerib NUE ülevõtupakkumist Harris Steelile ning annab terasetööstuse osas positiivseid kommentaare. NUE ülevõttvõib tuua spekulatsioone mitte toorterase töötlemisse vaid terase vormimisega tegelevatesse firmadesse. Kuigi uudis oli juba eilne, omas tugev langus turul tähtsamat osa. Radaril võib hoida CMC, GNA (rebar turgul suur osalus), STLD, CHAP, kaudselt ka AKS, mis omab construction/manufacture turul osa.

➤ NUE annc friendly, all-cash bid for Canada’s Harris Steel, valued at $1.18 bln.Not a surprise, as cos have JV, and Harris prev confirmed that it was in talks.➤ Valuation 7.5x trailing 12-mo EBITDA ample but not excessive.➤ Harris' principal business is fabricated rebar, which adds downstreamintegration to NUE's 3 mtpy rebar capacity. Also: wire, cold finished bar,grating, and distribution/trading. Harris has no crude steelmaking capacity.➤ Steel cycle: Post-peak, or Near-trough? Prices likely bottoming, headwinds thru 1Q/07. Taking full-yr view, we favor NUE for defensible margins. No chgto EPS ests. Maint 1M (Buy, Medium Risk) rating and $68/sh target.

Citigroup tõmbab alla Motorola (MOT) EPS prognoosi ning kommenteerib negatiivselt KRZR turuletoomist ja RAZR hinda/marginaale.Kuigi handset turu kehv hinnadünaamika ei ole üllatus, on KRZR kommentaarid huvitavad. Motoga on seotud SUPX ning CAMD (käive tuleb ca 25% Motorolalt). Silmapiiril võib hoida ka MFLX.

➤ Coming into 2007, Motorola is faced with number of challenges in its handsetbusiness. The shift dynamics within both the industry backdrop and its ownhandset division changes our investment thesis and upside potential to theshares.➤ We think that KRZR launch has been disappointing and Motorola will probably cut KRZR price more aggressively, which will put pressure on ASP and margin.➤ While we don’t expect the volume of RAZR to ramp down rapidly in 2007 aswe expect Motorola to push RAZR hard into emerging market to offset thepotential weakness in the mature market due to aging of the product. However,we think that ASP and margin will probably continue to edge down for thisproduct.➤ We lower our EPS estimate and price target by $2 (to $27) on KRZR concernsand overall aged product portfolio but maintain our 1H rating on the stock.

Tean, et nii mõnedki kauplejad läksid eile HD tõusu vastu lühikeseks ning toon siinkohal välja lühikese kommentaari Citigroupilt:

OUR TAKE: Nardelli's resignation may be viewed as a near-term positive, butwe feel that HD's management now has a lot on their plate. Potential disruptionat HD could provide LOW with a unique opportunity to gain market share andwe reiterate LOW as our top pick for 2007.

-

Prudential downgrades ABB Ltd. (ABB 17.82) to Neutral from Overweight and raise their tgt to $18 from $17, based on valuation

Thomas Weisel downgrades Hilton Hotels (HLT 34.75) to Underweight from Market Weight, based on valuation and consider long-term expectations to be aggressive at this point in the lodging cycle

JMP Securities initiates Maxwell Technologies (MXWL 14.06) with a Market Outperform and $20 tgt, as they believe the market for ultracapacitors is now at an inflection point, evidenced recently by Maxwell's first major contract in the telecom space, sales growth for ultracapacitors approaching 50% for each of the three preceding quarters, and recent developmental contracts with major Tier 1 automotive OEMs

Merrill initiates Nymex (NMX 124.01) with a Sell

BofA downgrades Kraft Foods (KFT 35.61) to Neutral from Buy

Eilsele EAGL kommentaarile lisab värvi Trucking sektori upgrade: Wachovia upgrades the Trucking Sector to Market Weight from Underweight saying they believe the environment is increasingly ripe for investors to begin taking positions within the trucking sector. The firm says while truckers will likely face even more difficult conditions during Q1 2007, they believe the negative sentiment towards the group is starting to bottom. Wachovia also upgrades Arkansas Best (ABFS 37.05), Heartland Express (HTLD 15.34), Werner Enterprises (WERN 18.19) and U.S. Xpress (XPRSA 17.24) to Market Perform from Underperform.

RBC initiates Sirf Tech (SIRF 25.00) with an Outperform

Credit Suisse upgrades Wachovia (WB 56.81) to Outperform from Neutral and raises their tgt to $64 from $61 saying while they believe 2007 will be a year of slowing EPS growth, they believe investors should build positions in more value oriented names like Wachovia.

Energiaettevõtete osas on negatiivsus suurenenud viimasel ajal ka analüütikute hulgas. Peale eilset verelaskmist võivad nii mõnedki alla-gape tekitavad kommentaarid kutsuda välja kauplejaid, kes otsivad gap-down reversal mängusid. Wachovia downgrades BJ Services (BJS 28.11) Weatherford (WFT 38.67), and Ensco (ESV 48.45) to Market Perform from Outperform saying they continue to believe service shares are discounting bad news (and the OSX is down 12% from its recent peak versus the S&P500 down 1%). But the firm sees additional downside as activity metrics worsen and service companies give (below consensus) '07 guidance.

-

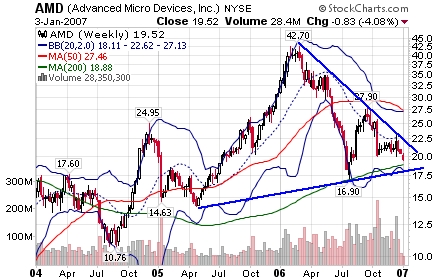

AMD on näidanud tehnilist nõrkust. Nädalaste küünalde graafikul on näha, et aktsia on tulnud oma aasta alguse tippust üle poole võrra madalamale. Moodustatud on kitsas kauplemisvahemik. Et pilt kirjum oleks, lisasin ka mõned libisevad keskmised. Näeme, et aprillis tuldi allapoole bollingeri eraldavat 20 päeva libisevat keskmist ning teistkordselt ülespoole murda ei suudetud. Selle asemel jätkus nõrkus ning selloff kuni augustini, tehes põrke 200 päeva libiseval keskmisel. 20 päeva MA on jäänud langustrendi vastupanuks. Ilmselt minnakse uuesti 200 päeva libisevat keskmist testima.

Ka päevasel graafikul on näha nõrkust. Aktsia on kaubelnud väga madala volatiilsusega ning selle kasvades on kukkunud läbi ajaloolise toetuse.

-

Stocks to watch:

- Teen-apparel retailer American Eagle Outfitters (AEOS) said that it had an "excellent" holiday sales performance and upped its fourth-quarter forecast. Warrendale, Pa.-based American Eagle said sales jumped 20% to $522.4 million in December. Sales at stores open longer than a year were up 13%, well ahead of the 8.7% average increase expected by analysts reporting to Thomson Financial. The retailer raised its fourth-quarter profit projection a penny to a per-share range of 64 cents to 65 cents.

- Applica (APN) said that Harbinger Capital Partners has increased its offer for the company to $7.75 a share from $7.50. Earlier today, Nacco Industries (NC) increased its offer to $7.75 a share. Applica, a Miramar, Fla.-based home appliance maker, said it has accepted the increased offer from Harbinger, and once again recommended the rejection of Nacco's offer.

- Atari (ATAR) said its shareholders have approved a 1-for-10 reverse stock split, in an effort to prevent the stock's delisting from the Nasdaq Global Market.

- Carrier Access (CACS) said it expects a fourth-quarter loss of 24 cents to 28 cents a share on revenue of $12.3 million to $12.5 million. On a pro forma basis, the loss is expected to be 21 cents to 25 cents a share for the quarter, the Boulder, Colo.-based manufacturer of broadband communications equipment said. Analysts polled by Thomson First Call are currently forecasting a fourth-quarter loss of 15 cents a share on revenue of $16 million.

- Cisco (CSCO) agreed to buy IronPort for $830 million in cash and stock, extending a string of acquisitions in the security field.

- Citi Trends (CTRN) said its December sales at stores open at least one year slipped 0.1%. Analysts, on average, had expected it to post a same-store sales gain of 2.8%, according to Thomson First Call. Total net sales for the five weeks ended Dec. 30 rose 17.8% to $60.4 million

- Con-way (CNW) said it now expects fourth-quarter earnings from continuing operations of 72 cents to 76 cents a share. The San Mateo, Calif.-based company had previously forecast per-share earnings from continuing operations of 81 cents to 87 cents a share for the quarter. The outlook doesn't include an expected gain from the sale of Vector SCM LLC, the company's logistics joint venture with General Motors (GM).

- Genaera (GENR) said it plans to terminate the Evizon clinical development program in wet age-related macular degeneration and cut its workforce by roughly 30%. The Plymouth Meeting, Pa.-based biopharmaceutical company said it will instead focus its resources on the development of trodusquemine for the treatment of obesity. Genaera added that it has engaged Banc of America Securities LLC as its financial advisor to assist the company in its review of strategic alternatives.

- Harrah's Entertainment (HET) Chief Operating Officer Timothy Wilmott has resigned, effective Friday, according to a filing with the Securities and Exchange Commission. Gary Loveman, the chairman, president and chief executive officer, has assumed Wilmott's responsibilities, the Las Vegas-based company said.

- Immucor (BLUD) reported second-quarter net earnings of $14.1 million, or 20 cents a share, up 75% from $8.06 million, or 11 cents a share, during the year-ago period. The Norcross, Ga.-based company posted revenue of $54.4 million vs. $44 million. Analysts polled by Thomson First Call had forecast second-quarter earnings of 18 cents a share on revenue of $52 million. The gross margin was 69.5% compared with 64.8% a year ago. Additionally, Immucor said it now expects fiscal 2007 per-share earnings of 75 cents to 78 cents, up from its previous estimate of 69 cents to 74 cents. The company also said it now sees revenue for the year of $214 million to $218 million, compared with its previous forecast of $204 million to $212 million.

- Intervoice (INTV) reported a fiscal third-quarter net loss of $88,000, or breakeven on a per-share basis. In the same quarter last year, the company posted net earnings of $3.63 million, or 9 cents a share. Excluding items, the Dallas-based software provider reported income of $2.56 million, or 7 cents a share, vs. $2.64 million, or 7 cents a share, in the year-ago period. Revenue in the period ended Nov. 30 rose to $52.8 million from $41 million. Analysts polled by Thomson First Call had forecast a per-share loss of 5 cents on revenue of $51 million. Intervoice expects fiscal fourth-quarter revenue of $48 million to $52 million.

- Men's Wearhouse (MW) said it still expects fourth-quarter earnings of 72 cents to 76 cents a share and adjusted earnings of 68 cents to 72 cents a share. Analysts polled by Thomson First Call are currently forecasting fourth-quarter earnings of 75 cents a share. For 2006, the Houston-based retailer said it expects per-share earnings of $2.48 to $2.52 and adjusted per-share earnings of $2.50 to $2.54.

- Merix (MERX) reported fiscal second-quarter net earnings of $1.76 million, or 8 cents a share. Excluding a $1.35 million charge related to the disposal of its single-sided businesses, the company reported earnings from continuing operations of 15 cents a share. In the same quarter last year, Merix posted a net loss of $2.35 million, or 12 cents a share. Revenue rose to $103.7 million from $61 million. Analysts polled by Thomson First Call had forecast earnings of 14 cents a share on revenue of $105 million. The Forest Grove, Ore.-based maker of printed circuit boards forecast fiscal third-quarter income from continuing operations of 5 cents to 15 cents a share on revenue of $100 million to $104 million.

- Royal Caribbean Cruises’s (RCL) Royal Caribbean International said it plans to begin removing trans fat from its menu items beginning March 1.

- Sigma-Aldrich (SIAL) said it has granted Pfizer (PFE) a worldwide non-exclusive research license to use DNA-directed RNAi, or ddRNAi, technology. Financial terms of the agreement weren't disclosed.

- Sonic (SONC) said first-quarter net earnings dipped to $15.3 million, or 19 cents a share, compared with $16.4 million, or 18 cents a share, for the same period a year ago. Sales rose to $174.8 million vs. $159.8 million for the first quarter of fiscal 2006. Earnings were negatively affected by 1 cent a share due to one-time gains and losses. Analysts polled by Thomson First Call expected the restaurant operator to post earnings of 20 cents a share for the quarter. Sonic said it expects to earn 16 cents to 17 cents a share in the second quarter, excluding one-time items, in line with estimates of 16 cents.

- Sprint Nextel (S) is putting its advertising account up for review, according to a media report. The telecommunications company opted for the review in an effort to explore new approaches to marketing and to reduce the number of agencies it works with, The Wall Street Journal reported in its online edition, citing a company spokeswoman. Sprint currently uses Omicom Group’s (OMC) TBWAChiatDay for consumer advertising and Publicis Groupe SA's (PUB) Publicis & Hal Riney for business-to-business advertising.

- Technical Olympic USA (TOA) named Stephen Wagman as chief financial officer. Wagman joins the Hollywood, Fla.-based homebuilder from MasTec Inc.

- United Auto Group (UAG) said it has named Roger Penske Jr. as president and Robert O'Shaughnessy as chief financial officer. The appointments are effective immediately, the Bloomfield Hills, Mich.-based automotive retailer said.

- VSE (VSEC) said it has received contracts in the fourth quarter worth up to $206.8 million, if all options are exercised.

- Witness Systems (WITS) said it expects fourth-quarter revenue of roughly $63 million and full-year 2006 revenue of $220 million. On an adjusted basis, which excludes hardware sales and the fair value adjustment to purchased service and support contracts, the company estimates fourth-quarter revenue of $62 million and 2006 revenue of $214 million. Analysts polled by Thomson First Call are forecasting fourth-quarter revenue of $58 million and 2006 revenue of $212 million. The Atlanta-based software company also forecast 2007 adjusted revenue of $250 to $255 million. Analysts are looking for 2007 revenue of $247 million.

- Specialty retailer Zumiez (ZUMZ) that sales at stores open more than a year, or same-store sales, climbed 11.5% during December, markedly higher than the 6.5% estimates from analysts polled by Thomson First Call. The seller of sports-related apparel said same-store sales rose 20.9% a year ago. Zumiez added that total net sales jumped by 40.5% to $62.5 million from $44.5 million in December 2005.

Market Summary- Asian trading closed with the Hang Seng -1.90%, Sensex -1.02% and Taiwan +0.22%, Shanghai +1.50%, Jakarta -0.58% and Nikkei closed.

-

Täna annavad oma ametivanded uued Kongressi liikmed. Ajal, mil Kongress ja Senat on läinud demokraatide kätte, jääb vabariiklasest president Bushil valitseda veel 2 aastat ning Bush avaldas lootust, et need 2 aastat võimaldavad mõlema erakonna poolse konstruktiivse lähenemise korral ellu viia tähtsaid asju USA rahva jaoks. Samuti rõhutas ta, et kuna demokraadid kontrollivad Senatit ja Kongressi ning president on vabariiklane, jagavad nad tehtud otsuste ees sarnast vastutust.

Üks tähtsamaid lubadusi tuli taas riigieelarve kohta, millest on küll ka varem juttu olnud. Kuna riiklikku defitsiiti suudeti poole võrra vähendada kolm aastat oodatust varem, loodab Bush, et aastaks 2012 saab USA oma riigieelarve tasakaalu. Pikas perspektiivis on selle saavutamine USA edu üks võtmetegureid.

It is also a fact that our tax cuts have fueled robust economic growth and record revenues. Because revenues have grown and we've done a better job of holding the line on domestic spending, we met our goal of cutting the deficit in half three years ahead of schedule. By continuing these policies, we can balance the federal budget by 2012 while funding our priorities and making the tax cuts permanent. In early February, I will submit a budget that does exactly that.

Samas hoiatas Bush, et kui Kongress võtab vastu seadusi, mis on pelgalt poliitilised avaldused vabariiklaste vastu, ootavad neid ees keerulised ajad.

If the Congress chooses to pass bills that are simply political statements, they will have chosen stalemate. If a different approach is taken, the next two years can be fruitful ones for our nation. We can show the American people that Republicans and Democrats can come together to find ways to help make America a more secure, prosperous and hopeful society. And we will show our enemies that the open debate they believe is a fatal weakness is the great strength that has allowed democracies to flourish and succeed.

-

Oleme hoidnud börsipäevas toornafta hinnaga kursis. Erakordselt soe ilm põhjustas eile tugeva kukkumise. Täna kauplevad veebruari lepingud 85,20 dollari juures.

-

AMGN kaupleb eelturul üle 1% plussis:

Amgen upgraded to Outperform from Peer Perform at Bear Stearns

Wachovia notes five reasons to own AMGN in 2007: 1) Eventual C.E.R.A. label could be limited. If this occurs, they believe the Street may perceive the threat to AMGN's EPO franchise as less meaningful than it is perceived to be now. 2) Limits on EPO use are reflected in the stock. 3) Firm believes the impact of EPO bundling will not be felt until 2011 at the earliest. 4) Although they do not anticipate a positive outcome from the Phase III PACCE trial designed to evaluate Vectibix as frontline treatment for colorectal carcinoma, potential upside could result from a surprisingly positive outcome. Phase III data from AMG 531 in ITP could provide proof-of-principle for use of this agent in chemotherapy-induced thrombocytopenia. Data is also expected from a Phase III trial evaluating denosumab for prevention of post-menopausal osteoporosis, as well as Phase II data from AMG 706 in various solid tumor indications. 5) Gross-margin improvements and impact of a newly announced $5 B stock repurchase program could contribute to increased EPS performance -

GameStop Dec same-store sales up 23.9%. Same-store sales, or sales at stores open at least a year, rose 23.9% in December, boosted by strong sales of hardware systems. The Grapevine, Tx. video game retailer said total sales rose 29% to $1.73 billion. The company said it now expects fourth-quarter same-store sales to rise 22% to 23%, and full-year same-store sales to rise 10% to 10.5%. The company also raised its fourth-quarter earnings outlook to $1.58 to $1.60 and its 2006 outlook to $2.03 to $2.05. The average estimate of analysts polled by Thomson First Call is for fourth-quarter earnings of $1.58 and 2006

GameStopi artikkel detsembri alguses: Videomängude müük tõusis novembris 34% -

SIX on eelturul plussis. Põhjus peitub selles, et ettevõtte tegevdirektor Mark Shapiro käis eile Crameri juhitud saates 'Mad Money' juttu puhumas ning lubas, et 2007. aasta tuleb pöördeline. Shapiro lubas ka varade müüki, millega vähendada probleemset võlakoormat.

When execs stick their necks out, when they make pledges, when they make it real clear that their jobs are on the line if things don't turn, I want to get behind them. Big-time. That's what John Antioco from Blockbuster (BBI - commentary - Cramer's Take - Rating) and Mark Shapiro from Six Flags (SIX - commentary - Cramer's Take - Rating) are doing.

Six Flags is tougher because it has tons of debt. But last night on "Mad Money" Mark Shapiro promised a turn in 2007 and some big asset sales. Why make that claim if you can't do it? I believe that this Six Flags is worth watching. I believe that Shapiro's going to be able to do it, and that the stock at last will get out of the $5 range.

I would buy this stock on that pledge. It's got limited downside and lots of upside, particularly if the weather simply gets better. Call it a call on global warming, which sure has been right when it comes to oil!

-

Shark räägib, et eilne FOMCi protokoll oli paljudele heaks ettekäändeks kasumivõtmiseks. Samas, asetab rõhku eelkõige emotsioonidele - s.t. et suur osa müügijõust oli ka emotsioonide taga. Pullid olid mugavaks läinud ning sedasorti kiire langus ehmatas nii mõnegi neist müüma.

The Fed Just a Selloff Scapegoat

By Rev Shark

RealMoney.com Contributor

1/4/2007 8:59 AM EST

Click here for more stories by Rev Shark

"When we blame, we give away our power."

-- Greg Anderson

The release of the Fed minutes received most of the blame for the sharp intraday reversal in the major indices yesterday afternoon. We were cruising along nicely as excitement about the new year brought in some early buying -- breadth was good, technology stocks were showing relative strength, and a sharp drop in crude oil probably was helping scare away any fears of inflation.

Around 1:15 p.m. EST the market started to roll over and when the minutes of the last FOMC meeting were released at 2 p.m. we spiked down sharply but managed to bounce back a fair amount into the closing bell. So the headlines suggestd the Fed minutes were not overly market friendly and had caused the selloff.

Maybe in part that is true but market news is much more complicated than that. The minutes of the FOMC meeting weren't really all that significant. The key was that the market was ready to sell off; it simply needed a convenient excuse and the FOMC minutes provided that excuse.

What really caused the market to reverse wasn't the minutes but the emotions. Market players were becoming too confident about the market and had used up their buying power too quickly to kick off the new year. There simply wasn't enough juice to keep things running and many were in a vulnerable position when they pressed their bets and then had to flee for safety when things failed to follow through.

Emotions in the first few days of a new year tend to be quite elevated. Fund managers want a good start, many folks are finally locking in some gains now that they have successfully deferred taxes, and many big macro investing visions are implemented. Investors are starting with a clean slate and are hypersensitive to doing anything that is going to put them behind in a major way to start the year.

If you want to assign blame for what happened don't look at the Fed, look at investors' emotions. They are the ones who determine the true meaning of news and given the current technical conditions of the indices and the high level of complacency that has been in place for a while, the path of least resistance for any news was down.

I contend that the emotional state of the market right now is such that the likelihood is that most news will be spun in a negative fashion. Market players have had a big run and want to stay optimistic and hold on to stocks, but they have big gains and if they find a reason to sell they will be more inclined to do something now than they were a few weeks ago.

We have a negative start this morning as yesterday's reversal hangs in the air. Retail same-store sales are being reported and don't appear to be particularly positive. Oil and commodities are looking weak again and overseas markets were down fairly sharply in most cases. -

Ülespoole avanevad:

IFON +17% (renews agreement with Samsung), MTRX +18% (reports NovQ, beats handily), PCOP +16% (announces deal with Wyeth), OSUR +10.4% (announces deal with SGP), WITS +9.7% (reports Q4 revs above consensus; also ThinkEquity upgrade), BOOM +7.6% (announces record Dec orders), OSCI +6.3% (announces European commericialization agreement), PANC +4.9% (Wachovia says it would be a buyer on recent weakness), NAPS +4.5% (strong rev and subscriber guidance), SIX +4.1% (Cramer interviews CEO; predicts shares have bottomed), GYMB +4.1% (reports strong Dec same store sales), GMKT +3.4% (announces two new board members), NUVO +3.2% (initiates phase 2 trial), ZVUE +3.1% (announces Dec web traffic), AZN +1.5%, SIRI +1.3% (extends yesterday's 6% move)... Under $3: ONT +9.2% (ThinkEquity names ONT as a Top Pick).

Allapoole avanevad:

Retailers trading lower on disappointing Dec same store sales: HOTT -14% (also lowers guidance), BJ -12% (also lowers guidance, announces mgmt changes and store closures), BEBE -10.4% (also guides below consensus), LTD -5.4%, CHS -5.1% (also guides below consensus), FNLY -4.3%, DDS -4%, GPS -2.7% (also guides lower)... Other news: NRMX -11% (Brean Murray initiates at Sell with $1 target price), SGTL -9% (guides lower; CEO resigns), AAI -6.7% (says it expects modest loss in Q4 vs consensus of $0.10 profit - Reuters), STZ -4.7% (reports NovQ; also Deutsche downgrade), LMC -3.7% (extends yesterday's 5% slide), BHP -2.3% (copper prices tumble)... Chinese stocks are sharply lower on profit-taking after recent surge: CHA -5.8%, LFC -4.9%, CN -4.4%, CHL -3.8%, FXI -3.4%. -

ISM Services 57.1 vs 57.0 consensus

Factory Orders +0.9% vs +1.4% consensus -

Märgin ära, et IWM on protsendi jagu miinuses kui samal ajal Nasdaq on praktiliselt nullis. Tavaliselt selline suundade erinevus head ei tähenda.

-

Distillaatide varud tõusid +2.0 mln vs oodatud 0.85 mln barrelit.

Mootorkütuse varud tõusid +5.7 mln vs oodatud 1.5 mln barrelit

Toornafta varud vähenesid -1.3 mln vs oodatud -2 mln barrelit -

UBS says that given valuation levels, healthy equity mkts & the favorable capital mkts backdrop, they continue to prefer the brokers & asset managers over trust banks, followed by the universal banks. Their favorite names are GS & LEH among the brokers, BEN and TROW among the asset managers and CS of the European universal banks.

Kuigi minu mäletamist mööda on UBS juba sektorit kiitnud, on tänane vastandlik liikumine broker/dealerite poolt negatiivne signaal edasiseks..