Börsipäev 11. august: Reise, reise

Kommentaari jätmiseks loo konto või logi sisse

-

Tere varahommikust!

Aasia turud kenasti plussis, USA futuurid veel kergelt miinuses. Täna võib vabalt tõus jätkuda, kuigi see võib tunduda veidi uskumatuna. -

Asian Stocks Advance on Lower Commodities; Honda Motor Rises

Aug. 11 (Bloomberg) -- Asian stocks gained, led by banks and automakers, after the drop in commodity prices eased inflation concerns and boosted the outlook for profits. -

Austraalia suurim hüpoteeklaenude väljastaja Commonwealth Bank aktsia kallines 3.3%, kuna Reserve Bank of Austrialia teatas, et intressimäära langetamine võib tulla üsna pea päevakorda. Vähenev sisetarbimine on aeglustanud inflatsiooni Austraalias. Seetõttu ongi alust arvata, et Keskpank võib üsna pea stimuleerida majandust langetades intressimäära.

-

Panen siia graafiku euro-dollari kursist. Nagu näha, siis 1.50 tasemest on juba korralikult allapoole murtud ning dollar jätkab oma märkimisväärselt kiiret tugevnemist.

-

Venemaa RTS avaneb veel 4% madalamal reedesest sulgumisest

-

mis kell londoni börs lahti läheb?

-

11?

-

Menace, kell 10 ikka jah.

-

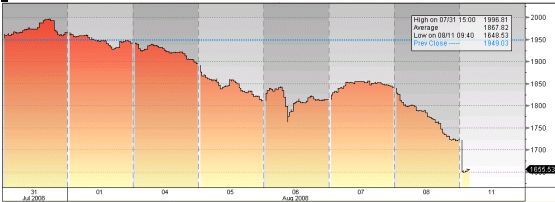

Samal ajal, kui Euroopa turud on tervikuna ca 0.5% kuni 0.8% kõrgemal, kolistatakse Venemaa aktsiaturgudel allapoole. Viimase kaheksa päeva tipust on RTS allapoole liikunud kogunisti 17%.

-

kas on mõtet panustada lühiajalisele põrkele ?

-

Londoni börsil hakkab kauplemine kell 10 (kell 8 sealse aja järgi), kuid AIM listis kell 11 (kell 9 sealse aja järgi)

ja BGEO ning Venemaa GDRid on AIM listis -

Freementar

ära sitta näpi hakkab haisema:)

Müüsin enda vene positsioonid maha. Vbla tegin valesti, aga vähemalt saan nüüd rahulikumalt magada. -

RTS kosub ... huvitav kas olulisi otsuseid sel kohtumisel?

MOSCOW, Aug 11 (Reuters) - Russia's president, prime minister, defence minister and top generals on Monday attended a meeting on the military situation in Georgia's breakaway region of South Ossetia, a Kremlin spokesman said.

He gave no details of the meeting. Russian news agencies said the meeting took place in the command centre of Russia's Armed Forces' General Staff headquarters. -

National Bank TRUST seisukoht olukorrast Venemaal (börsidel)

Public debt and stock markets have fallen. In under two months (June 18 to August 8), Russian stocks lost 28%. During the second quarter of 2008, net foreign capital inflow turned into outflow in August as a fairly attractive market lost most of its appeal to investors.

Financial crises in developed economies, serious corporate conflicts at Nornickel and TNK-BP, increased pressure from the Russian authorities on metal and coal producers and finally, an armed conflict on Russia’s border – have all contributed considerably to the current state of affairs.

By the time Georgia attempted to reestablish control over South Ossetia, the market was already on a downturn and investors were ready to sell on any negative news. The roots of this conflict go a long way back. When the USSR broke up, South Ossetia, which was then a former region of Georgia, declared independence (and has since then been independent). The Georgian authorities vigorously opposed this move. In the early 90s, an unwillingness to compromise from both sides resulted in a serious military confrontation which ostensibly ended in 1992, but the underlying issue remained very much unresolved. Since no satisfactory solution has since been found, the region has remained unstable. We believe that the current escalation of the conflict between South Ossetia and Georgia is directly linked to the unilateral independence of Kosovo.

The results of Friday’s events were serious and far-reaching:

-Russian stock market lost 6.5% in one day (RTS index);

-Demand for foreign currency increased strongly (total daily turnover reached a record high of US$14.2 bln. during United Trading Session on MICEX);

-The Bank of Russia had to provide liquidity via direct REPO (RUR127.7 bln) and sell foreign currency (based on our estimates over US$5 bln);

-The dual-currency basket jumped from the level of 29.39 (where the market opened in the morning) to 29.70 (the last deal of the official trading session).

In the event, many investors sold Russian stocks, most likely interpreting the events in South Ossetia as war. However we believe that the actions of Russian military forces will not go beyond peacemaking, which is how it looks from the perspective of South Ossetia which has considered itself independent since 1992.

The armed conflict itself is small and localized and had mostly petered out by Monday morning (August 11). Much of the activity on both sides was demonstrative in nature. While it may have serious serious consequences for all sides we would like to focus on the impact for the Russian economy:

1. In strictly monetary terms, the direct economic cost for Russia of all the events of recent weeks (including the conflict) does not look very significant (excluding public stock and debt market volatility aside). However, Russia’s reputation has been dealt a serious blow. International investors may now regard Russia as unsafe in comparison with other emerging markets. Already this year, the inflow of foreign investments (both direct and portfolio) could turn out to be lower than previously expected.

2. A decrease in foreign investments could decelerate economic growth which would be very undesirable for the Russian authorities. In response, they may increase state presence in the economy beyond its already significant level. So, more public sector investments could be on the way in the medium term.

3. An open confrontation with Georgia could close the doors of the WTO for Russia. In its current position as a major natural resource exporter, this would not have a huge impact but it could threaten plans to diversify the economy.

4. Instability in Sochi could also potentially affect the Olympic Games in 2014 as the attractiveness of the region for both local and foreign investments could decrease markedly.

We forecast that the bulk of problems both in the corporate sector and in the political arena will settle down in a matter of weeks or, at the very least switch to a more stable and predictable phase. Although it is likely that instability and provocation will linger in the region of the current armed conflict, we are fairly certain that that the Russian military presence will be limited to reestablishing peace (as borne out by the events of last weekend). Furthermore, we anticipate that the direct influence of the well-reported current conflict on real economic activity in the Russian economy will be insignificant

Unfortunately however many of the current problems may linger on. South Ossetia is not the only former region of Georgia, unhappy with its status. Abhazia has already demonstrated its readiness to engage. Things may also become bumpy in the corporate sector in the near future as the Russian authorities do more to persuade Russian companies to obey local laws (albeit accompanied by a decrease in the tax burden, VAT, resource tax, etc) and step up the anticorruption campaign.

At the same time, in terms of its general economic condition, Russia retains its strong positions - oil is expensive, federal budget is in surplus, the current account is positive and net foreign capital inflow remains, albeit lower than for last year. We do not expect the current conflict to have a serious impact on the federal budget. That means, that although in the very short term current events provide an unwelcome anniversary of the 1998 crisis, there is still plenty of room for optimism over the coming weeks and months. As soon as current corporate and political conflicts settle down (or at least stabilizes) growth may rapidly return to the market.

-

Majandusuudiseid USAst täna ei tule ning esimesteks tähtsamateks näitajates on alles kolmapäevane juulikuu jaemüügiraport (ootus +0.5%) ning neljapäevane tarbijahinnaindeksi näit (ootus+0.4% ja tuumikosalt +0.2%). Majandustulemuste poolest on väga olulised kindlasti neljapäeva eelturul avaldatavad Wal-Marti (WMT) numbrid.

-

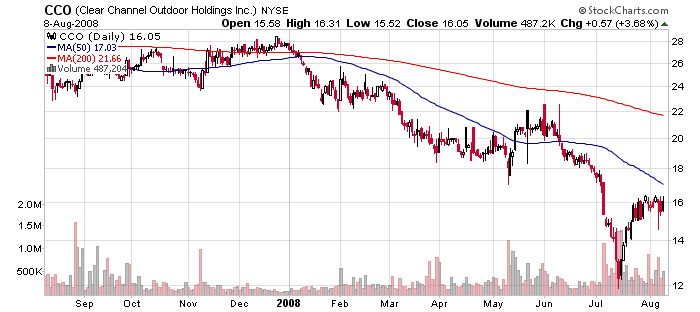

Eelmisel nädal kirjutasin börsipäeva foorumis välireklaami pakkuvast Lamar Advertising’ust (LAMR). Täna enne turu avanemist avaldas oma Q2 tulemused üks ettevõtte suurimaid konkurente Clear Channel (CCO), kes suutis konsensuse ootuseid ületada:

Reports Q2 (Jun) earnings of $0.23 per share, $0.04 better than the First Call consensus of $0.19; revenues rose 9.3% year/year to $914.8 mln vs the $864 mln consensus.

Samas tulemuste pressiteadet lugedes jääb silma, et tugevust näitas just rahvusvaheline äri ja Ameerika segment oli pigem nõrk:

Paul J. Meyer, Global President and Chief Operating Officer, commented, “In the Americas, despite growth in our national business, the decline in our local business, coupled with significant lease cost increases from major new contracts continued to pressure our cash flow.

Erinevalt Clear Channel’ist, kelle tuludest moodustab Lõuna- ja Põhja-Ameerika 42%, keskendub Lamar USA-le (lisaks tegutsetakse Kanadas ja Puerto Ricos, kuid nende mõju ei ole märkimisväärne). Sealjuures 82% tuludest teenitakse just local ad turgudelt, mis on praeguses turuolukorras näitamas suurimat nõrkust.

-

Sturdy Dollar Emboldens the Eager Bulls

By Rev Shark

RealMoney.com Contributor

8/11/2008 8:29 AM EDT

The fact that a believer is happier than a skeptic is no more to the point than the fact than a drunken man is happier than a sober one.

-- George Bernard Shaw

The dollar is continuing to strengthen this morning, and that is helping to hold the indices steady as we kick off the week. Oil has ticked up a bit, but that as being shrugged off as the bulls celebrate the idea that the dollar will continue to trend higher. The thinking is that the higher dollar will keep pressure on commodity pricing and attract foreign investment into the U.S. There is some downside to the higher dollar, such as higher prices on foreign goods, but right now that is seen as irrelevant.

Worries about a slower economy in Europe, inflationary pressures in China, the Russia military action in the Caucasus and some good old-fashioned momentum are all helping to drive the dollar. This brings up two key questions: Will the move in the dollar continue? Will it continue to drive the market higher?

To the extent a stronger dollar cools inflation it is an obvious positive, but many out there are rushing to embrace the idea that suddenly all our worries and woes are over. We are still faced with problems in banking, real estate and in the broad economy, but the market is very hungry for some relief from the negativity and is embracing the idea that the dollar will lead us straight back up.

While the bulls have some momentum going here and the technical action is better, we still can't be confident that this is anything more than another bear-market bounce. What makes it so difficult for investors is the various market pundits out there who so desperately want to convince us that this time it is different and we really ready to start a new bull market.

While the action recently has been better and the indices have made some higher highs, I remain skeptical. My biggest problem with this market continues to be the nature of leadership. The big movers on Friday were consumer stocks that tend to be defensive plays, such as McDonald's (MCD) , Procter & Gamble (PG) and Johnson & Johnson (JNJ) . Technology stocks have started to turn up, which is a good sign, but they have more work to do before they can assume leadership. Medical stocks have been the real leaders lately, but again, that is a function of investors looking for safety in a recessionary environment.

The bulls have the advantage here, and we'll see if they can keep on running. Many are underinvested, and we could easily squeeze higher, but I'm not going to be doing much chasing.

------------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: FEED +11.5%, CPN +7.9%, HOGS +5.3%, LGF +5.0%, SYY +4.6% (light volume), DBD +2.1%... M&A news: ITWO +2.4% (to be acquired by JDAS for $14.86 per share), RSG +1.8% (Waste Management confirms it improved all-cash proposal for Republic Services to $37/share, up from $34/share)... Select oil/gas names showing strength: BP +1.4%, RDS.A +1.2%... Other news: CHIP +27.3% (declares special cash dividend of $1.35 per share), CRXL +2.8% (still checking)... Analyst comments: Q +4.5% (upgraded to Buy at Citigroup), ENER +3.2% (upgraded to Buy at UBS), ANAD +3.0% (upgraded to Accumulate at ThinkPanmure), CIEN +2.8% (upgraded to Outperform at Morgan Keegan), ELX +2.6% (upgraded to Buy at Citigroup), LDK +2.3% (initiated witjh Buy at ThinkPanmure).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: URRE -23.1%, PEIX -11.4% TOD -7.7% (light volume), ISPH -3.5% (light volume), RDNT -3.3% (light volume), KNOL -1.2%... Select China names showing weakness following a sell-off in Chinese trading (Shanghai Composite closed -5.2%): CEA -10.0%, ZNH -8.7%, ACH -2.1% (led declines in China after factory-gate inflation accelerated to a nine-year high, increasing concern that higher costs will feed into consumer prices and prompt the central bank to tighten lending)... Other news: SIRF -17.1% (Broadcom announces that ITC judge finds that SiRF infringes six BRCM GPS patents), HK -6.2% (announces public offering of 25.0 mln shares of common stock), FOSL -4.6% (still checking), NCC -3.1% (discloses informal SEC investigation), BRNC -2.2% (Allis-Chalmers Energy and Bronco Drilling terminate merger agreement), ABB -1.5% (still checking)... Analyst comments: HALO -3.3% (downgraded to Hold at Brean Murray), URBN -2.3% (downgraded to Hold at Roth Capital), AXA -1.8% (downgraded to Neutral from Outperform at Credit Suisse), AAP -1.5% (downgraded to Neutral at Goldman - DJ), ED -1.4% (downgraded to Underweight at JPMorgan), SPWR -1.4% (downgraded to Neutral at UBS), QLGC -1.3% (downgraded to Hold at Citigroup), GFI -1.1% (downgraded to Neutral at JPMorgan). -

Euroopa ja Aasia indeksid:

Saksamaa DAX +0.41%

Prantsusmaa CAC 40 +0.41%

Inglismaa FTSE 100 +0.66%

Hispaania IBEX 35 +1.08%

Venemaa MICEX +2.27%

Poola WIG +0.76%

Aasia turud:

Jaapani Nikkei 225 +1.99%

Hong Kongi Hang Seng -0.12%

Hiina Shanghai A (kodumaine) -5.19%

Hiina Shanghai B (välismaine) -9.00%

Lõuna-Korea Kosdaq +2.16%

Tai Set 50 +2.16%

India Sensex +2.22%

-

Nafta jätkab allapoole liikumist, hetkel $114 barrelist, ning aktsiaindeksid liiguvad selle peale üha kõrgemale. S&P500 üritab läbi murda olulisest 1300 punkti tasemest.

-

Nafta futuurid kukkunud alla $113 barrel taseme ning turg rallib nafta toetusel. Ka finants on jalad alla saanud ning näitab üles tugevust, nõrgemalt esineb energiasektor.

-

Sector ETF Leaders @ midday:

Homebuilders- XHB +6.9%, Regional Banks- KRE +5.5%, RKH +3.8%, Retail- XRT +5.3%, RTH +4.6%, Internet- HHH +5.1%, Commercial Banks- KBE +4.4%, Cons. Disct.- XLY +4.3%, VCR +4.0%, Financial Services- IYG +3.8%, IAI +3.4%Sector ETF Laggards @ midday:

Gold Miners- GDX -5.9%, Coal- KOL -5.9%, Metals & Mining- XME -5.4%, Silver- SLV -4.5%, Gold- GLD -3.6%, Steel- SLX -3.3%, Ag/Chem- MOO -3.1%, Wind Energy- FAN -2.5%, Materials- IYM -2.4%, XLB -0.50% -

Hämmastav ikka see USA turu depressiiv-manikaalne olek.

Nafta on tippudest veidi alla tulnud ja dollar rallinud. Ja nüüd kõik siis tormavad ostma retailereid @ 15x kasumit. LOW ja HD on äkitselt 8% üleval. RTH + 5.3%!

Ja müüakse muidugi kõike commodity-related asja.

Ilmselt samad tüübid, kes commodity asjas tipus rämedalt pikad olid, püüavad nüüd siis muudesse sektoritesse siseneda. Ja saavad muidugi mõnusa trääsa jällegi.

Mõnus. -

Mulle tundub, et lähiajal saame hoopis näha mõnusat commodity short squeezi. See on siis selline väga short term arvamus.

-

Hetkel ostetakse juba pea kõike, väga laiapõhjaline ostmine.

-

`We are excited about our prospects for the 2008 second half, especially the benefits from the Democratic National Convention which will be held from August 25 to August 28. Our five Denver areas club, two of which are very close to the Colorado Convention Center, where the Democratic National Convention will take place, are ready for the anticipated increase in traffic. In addition, our Schieks Palace Royale club in Minneapolis is preparing for the Republican National Convention that will take place from September 1 to September 4. We are optimistic that both the Democratic and Republican National Conventions will contribute to our overall growth in the 2008 third quarter."

:)))

see lõik on VCGH tänatest tulemustest -

mis tasemelt sa speedy sinna vcgh-sse sisenesidki? ;)

-

Fed says banks tighten consumer, business lending standards - Bloomberg

Fed says 60% of banks raised standards for business loans and 65% of banks tighten standards on credit card loans. Fed says banks expect tighter credit through 1st-half of 2009.

Ja turud teevad tugeva jõnksu allapoole, kas suudetakse kättevõidetud tasemeid hoida?

-

Lisaks siia Briefingus avaldatud Moody's-e negatiivse hoiaku USA toiduainetööstuse suhtes:

Moody's says the outlook for the US food industry is negative, based on the view that commodity prices in 2009 are poised to further surpass historical averages, squeezing profit margins and putting cash flow at risk for most companies. "Profit margins will continue to contract as most speculative-grade food companies struggle to pass on rising commodity costs to customers. The rising food-price inflation means another challenging year for meat processors, whose profits are highly sensitive to feed costs, as well as for some weaker packaged-foods companies that lack sufficient pricing power with customers. If commodity prices rise more sharply than expected, these companies could come under significant pressure."

Moodyś-e arvamus toetab LHV Pro ideed K lühikeses positsioonis.

-

WN

ei mäleta, ammu stopiga väljas

vahepeal 2x treidinud -

Hetkel paistab, et Fed-i survey andis finantsile väikse tagasilöögi ning müük on päris intensiivseks läinud. Tehnoloogia on samuti tagasi tõmbamas ning energiasektor kosumas.