Börsipäev 27. märts

Kommentaari jätmiseks loo konto või logi sisse

-

Täna on viimane kauplemispäev USA turgudel, mil eestlaste jaoks toimub kauplemine vahemikus 15.30-22.00. Nädalavahetusel keeratakse kella ka Euroopas ning siis esmaspäevast taas harjumuspärane kauplemisaeg 16.30-23.00.

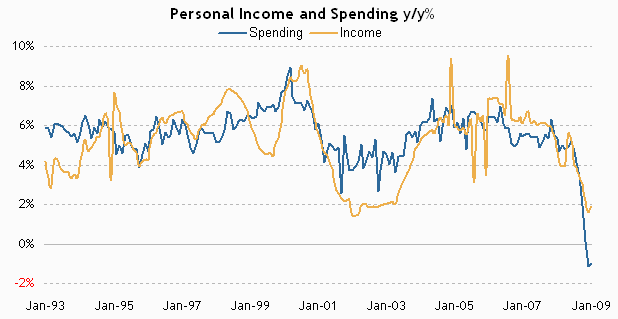

Täna tund aega enne turu avanemist avalikustatakse veebruarikuu sissetulekute ja kulutuste muutuste raportid. Sissetulekutelt oodatakse 0.1%list vähenemist, kulutustelt 0.2%list suurenemist. Seda, kuidas ameeriklaste sissetulekute ja kulutuste kasv on viimasel ajal peatunud näitab allolev graafik:

-

Lp LHV meeskond,

kui saadan orderi investeerimiskontolt Soome turule, siis kui kaua võib aega minna orderi sealsele turule jõudmisega, et mul poleks veel põhjust end ebamugavalt tunda? -

Orderid turule edastatud. Kui on probleeme, siis kiirelt saab vastuse maaklerite telefonil 6 800 420

-

Eilne solar aktsiate ralli võib täna lõpu saada, sest mitmed analüüsimajad on väljas ettevaatlike kommentaaridega. Nimelt on uudis Hiina riigi abipaketi kohta kahtlemata positiivne, kuid samas on sellest programmist avalikkusele teada väga vähe detaile. Seal hulgas on teadmata ka kõige tähtsam nüanss - kui palju täpselt Hiina on valmis kulutama päikeseenergia subsideerimiseks.

-) Notable Calls vahendab FBR tugeva sõnastusega kommentaari.

-) Oppenheimer alandab Suntech'i (STP) reitingu Overweight tasemele pärast eilset 44%-list tõusu. Eric Savitz kirjutab:

Oppenheimer’s Sam Dubinsky is cutting his rating on Suntech (STP) to Underperform from Perform after the stock soared 44% on Thursday. “We simply don’t see the earnings power to justify an $11 stock price and believe high debt levels will be an ongoing overhang,” he writes. Dubinsky adds that the subsidy program is “very favorable and could support a price cushion for the sector,” but that the run-up is premature given the lack of detail.

-) Citigroup lisab SunPower'i (SPWRA) Sell reitinguga parimate ideede nimekirja (Top Picks Live). Tõsi, Citi kommentaar oli juba eile 14:51 EDT väljas.

Adding SPWRA (Sell) to Top Picks Live! (TPL) — We are taking advantage of the ~16% move today in SPWRA to add the Sell idea to TPL, CIRA’s list ofh ighest conviction ideas. While this should absorb some excess supply, SPWRA seems low on the list of beneficiaries while we are increasingly convinced thereis near-term risk given what is likely a reset to full-year guide when it reports, likely another GAAP EPS loss in CQ2 (stock has little EPS support), more evidence of rapid ASP compression, share loss vs. leaders like FSLR when the dust settles, and potentially more news on balance sheet de-leveraging.

-

Ülevõtud ravimisektoris jätkuvad. Sanofi ostab Medley:

Sanofi-Aventis to buy Brazil's Medley for BRL1.5 bln, according to report. DJ reports the co has signed a letter of intent to acquire Brazilian generic drugs manufacturer Medley for 1.5 billion Brazilian reals ($670 million), local newspaper O Estado de S. Paulo reported. Of the total value, BRL500 million will be paid to Medley's controllers. The rest, or BRL1 billion, will be used to pay off the co's existing debts, the report said. According to the newspaper, the deal must be concluded within the next 15 days. The conclusion of the deal still depends on approval by Sanofi-Aventis' headquarters. -

February PCE Deflator y/y +1.0% vs +0.8% consensus, prior revised to +0.8% from +0.7%

February PCE Core m/m +0.2% vs +0.2% consensus, prior revised to +0.2% from +0.1%

February Personal Income -0.2% vs -0.1% consensus; prior revised to +0.2% from +0.4%

Feb Personal Spending +0.2% vs +0.2% consensus; prior revised to +1.0% from +0.6%

February PCE Core y/y +1.8% vs +1.6% consensus, prior revised to +1.7% from +1.6% -

Saksamaa DAX -1.03%

Prantsusmaa CAC 40 -1.04%

Inglismaa FTSE 100 -0.34%

Hispaania IBEX 35 -0.69%

Venemaa MICEX -2.82%

Poola WIG -1.61%

Aasia turud:

Jaapani Nikkei 225 -0.10%

Hong Kongi Hang Seng +0.07%

Hiina Shanghai A (kodumaine) +0.77%

Hiina Shanghai B (välismaine) +0.54%

Lõuna-Korea Kosdaq -1.41%

Tai Set 50 +0.37%

India Sensex 30 +0.45%

-

We Need a Test

By Rev Shark

RealMoney.com Contributor

3/27/2009 8:50 AM EDT

Commitment in the face of conflict produces character.

-- Unknown

The market has now bounced back to the levels we saw back in January and early February. The big question is whether investors have the commitment and character to keep things going. Has there really been a notable change in the market that has produced a lasting low, or is this a good-sized bear-market bounce?

Bear-market bounces always feel like they are a major change in market character, or they wouldn't produce much of a bounce in the first place. Market players will always think that a bounce is a major trend change, and that is why we see momentum like we've had this past week.

As I've said, the real test comes on the pullbacks. A real commitment to a change in market character is seen when dip-buyers consistently support the market. We haven't seen much of a test yet, as the market has run away to the upside -- probably due in large part to performance anxiety associated with the end of the quarter. Money managers are anxious to be at least close to even after poor action in January and February.

There are two major questions the market must answer at this point. First, are all the new government programs going to have an impact? To some degree the rally we have already had is in anticipation of the idea that there will be some positives from the flood of liquidity and the efforts to deal with toxic assets. It isn't just the programs themselves that are important, but the psychology they deliver. We are likely to continue to see unemployment grow and poor economic numbers, but the pace of the bad news may slow.

It is often said that the market looks ahead, and we are at that juncture now where we are going to need to see across the valley of some problems to keep this rally going. We have had a huge public relations push by the Obama administration over the past month, with daily television appearances and program announcements. We will now need to see if all these plans are really going to work like they are supposed to. I suspect there will be some uncertainty, and that will give us the pullbacks that show us if there is some real confidence.

The other question we will be dealing with in the near term is first-quarter earnings. Expectations are low, but we have to see how psychology develops. Are companies going to be cutting guidance even more, or are they going to talk about the worst being over and a turn coming in their business?

This V-shaped move off the March low has been good for a lot of excitement but we still have no clue whether it is just a good bear-market bounce or the beginning of a new, sustained uptrend. We will have some tests in the next month from economic data and earnings reports. That will tell us much more about the story.

We have a pullback at the open this morning as profit-taking kicks in and emotions cool off a bit. There is plenty of overhead resistance in the major indices at this point, and we are in need of some backing and filling.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: FREE +18.7%, WTSLA +7.1%, SNX +6.9% (also upgraded to Buy at Needham), KBH 5.9%, LULU +2.3%, XRTX +1.2% (light volume)... M&A news: CF +1.4% (Agrium Increases Offer for CF Industries to $35.00 in Cash Plus One Agrium Share Per CF Share), HTV +1.0% (light volume; Hearst-Argyle TV responds to announcement by Hearst Corporation--offer will be considered by a special committee)... Select auto related names trading higher: GM +12.6% (GM unlikely to hit goal of March 31 restructuring; auto-industry task force appear willing to extend the deadline by 30 days - WSJ), F +2.1%, DAI +1.8%, TTM +1.3%... Other news: LYG +11.0% (still checking), BCS +5.5% (Barclays stress test signals no new funds - FT), AINV +4.4% (still checking), RDC +2.4% (Rowan Cos' LeTourneau Technologies signed contracts valued at ~$185 mln), NVDA +1.1% (filed a countersuit in the Court of Chancery in the State of Delaware against Intel)... Analyst comments: ASH +3.8% (Credit Suisse raises tgt to $15.50; believes concerns over debt levels are overblown), CSX +1.3% (upgraded to Buy at BofA/Merrill), AMGN +1.3% (upgraded to Overweight from Neutral at JP Morgan), UPS +1.1% (upgraded to Buy at BofA/Merrill).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: ACN -9.5% (also downgraded to Hold at Stifel Nicolaus), CBK -9.0%, SAP -5.3% (DJ reports the co confirmed a drop in operating margin for 2009), PWE -4.9%... Select financial names pulling back: UBS -9.3%, AEG -8.7%, ING -8.6%, HIG -4.2%, C -3.9%, PUK -3.8%, FITB -3.7%, BAC -3.3%, BBT -3.2%, COF -3.2%, C -2.8%, V -2.2%, GS -1.9%, MS -1.8%... Select metals/mining names showing weakness: AAUK -5.5%, BHP -4.9% (downgraded to Neutral from Buy at BofA/Merrill), BBL -4.8%, RIO -3.6%, GG -2.4%, AUY -3.3%, GFI -2.4%, ABX -1.8%, AU -1.6%, GLD -1.4%, HMY -1.1%... Select oil/gas names trading lower: ACGY -6.4%, BJS -5.9% (added to Conviction Sell List at Goldman - Reuters), NBR -4.7%, TLM -3.4% (downgraded to Sell at Goldman - Reuters), NOV -3.2%, XTO -3.2% (downgraded to Neutral at Goldman - Reuters; also trading ex-dividend), TOT -3.0%, PBR -2.6% (downgraded to Hold at Deutsche), BP -1.7%, SLB-1.5%, E -1.4%, XOM -1.3%, RDS.A -1.2%... Select solar names pulling back from yesterday's surge higher: AKNS -7.7%, SOLF -5.7%, STP -5.6% (downgraded to Underperform at Oppenheimer), SOL -5.1%, ESLR -4.4%, FSLR -3.8% (downgraded to Hold at Collins Stewart), SPWRA -3.6%, YGE -2.7%, CSIQ -2.6%, TSL -1.6% (downgraded to Underperform at FBR)... Select casinos seeing early weakness: MGM -12.6% (Las Vegas project weighs bankruptcy - WSJ), LVS -6.4%... Other news: OSIR -41.5% (discontinues enrollment in Crohn's study due to concerns with trial design), DYAX -20.0% (receives complete response letter from FDA for DX-88 in acute attacks of hereditary angioedema), TGB -8.3% (to sell 13.8 mln shares at C$1.45 each), DHT -7.8% (to offer 6.5 mln common shares), MAS -5.8% (cuts quarterly dividend to $0.075; down from $0.235), VOD -3.7% (still checking for anything specific), SNY -2.2% (Sanofi-Aventis to buy Brazil's Medley for BRL1.5 bln, according to report - DJ), BCSI -1.7% (announces CFO transition)... Analyst comments: PCX -5.6% (initiated with Sell at Goldman - Reuters), MAC -3.0% (downgraded to Sell at Goldman - Reuters), VMW -2.6% (initiated with Sell at Auriga), AMZN -2.5% (removed from Americas Conviction Buy List at Goldman- Reuters), BBY -1.6% (removed from Conviction Buy list at Goldman- Reuters). -

Tõus on olnud väga lühikese aja jooksul võimas ning tõenäolisem stsenaarium tänasele päevalõpule oleks ikkagi kasumivõtt.

-

paistab, et ravimite mõju turul hakkab kaduma