Börsipäev 29. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Aasia turgudel on nädalat alustatud kerges miinuses (eranditeks Hiina, Uus-Meremaa, Tai, Malaisia ja Pakistan mille indeksid kauplesid plussis). Kui oodatust parem nõudlus soosis elektroonikatööstust siis regiooni finantssektor sattus seevastu tugevama müügisurve all. Jaapani pank Mizuho ja maaklerfirma Daiwa Securities teatasid mõlemad plaanidest paisata turule uusi aktsiaid: vastavalt 6.3 miljardi ja 2.5 miljardi dollari väärtuses, lahjendades olemasolevate investorite osalust.

Makro osas täna midagi olulist oodata pole, kui suuremat huvi peaksid neljapäeval pakkuma ISM indeks, Euroopa Keskpanga intressimäära otsus ning non-farm payrolls. USA indeksid on hetkel ca -0.6% languses.

NB! USA turgudel on nädal tavapärasest lühem, sest 4. juuli iseseisvuspäeva tõttu reedel kauplemist ei toimu.

-

Hiina on korduvalt avaldanud muret oma USA võlakirja portfelli üle ning kutsunud maailma üles looma uut globaalset valuutat, mis ei sõltuks ühegi riigi majandusest. Heaks alternatiiviks USA võlakrijadele on Hiina valitsus lühiajaliselt leidnud erinevate toormaterjalide kokkuostmise. Juunis läks juba üle 10% Lähis-Idas toodetavast naftast ainuüksi Hiinasse. Riigil on 102 miljonit barrelit naftavarusid juba olemas, kuid soov on see kolmekordistada:

Crude Oil exports from the Middle East to Asia surged in June as a result of increasing demand from China. According to Data from Lloyd’s Marine Intelligence Unit’s Apex service, 5 million tones of oil had been directed from the Middle East to China this month out of a total of 40 million tones.

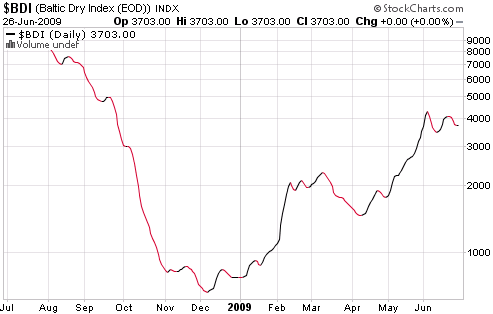

The rise in Chinese demand for crude oil is attributable to the stimulus package set by the Chinese government. That is, the government aims at piling a stock of 315 million barrels of oil, worth 90 days of import cover. The Chinese government has so far piled 102 million barrels and is still looking to receive another 213 million barrels.Baltic Dry Index, mis näitab kaubamahtude liigutamise hindu mereteid mööda, on Hiina toormaterjalide kokkuostmise tuhinas ning maailma majanduse langusfaasi stabiliseerumise järel jõudsalt ülespoole liikunud ning on viimase 9 kuu tippudes.

-

Mitmed väiksemad aktsiad tegid reedel ja ka reedele eelnenud päevadel väga suuri liikumisi. Põhjuseks oli Russell 3000 indeksi rekonstrueerimine - mõned aktsiad langesid indeksist välja, mõned lisati juurde. Nimekiri on tegelikult päris pikk, seetõttu panen lingi muudatuste tabelile.

-

Citigroup on täna tõstnud nafta barreli 2009.a prognoosi 47 dollarilt 56 dollarile ning 2010 prognoosi 55 dollarilt 65 dollarile, mis sellest hoolimata jääb tagasihoidlikumaks kui Goldmanil, kes hiljaaegu kergitas oma nägemuse 2009. aastaks 85 peale ja 2010 oma 95 dollarile. Citi prognoos tähendaks, et sektori kesumiootused paraneksid 12% ja 17% vastavatel aastatel.

-

Rahvusvaheline Energiaagentuur on seevastu kärpinud viie aasta prognoosis päevast naftanõudlust 3 miljoni barreli võrra kõikidel aastatel kuni 2013 aastani. Bloombergist võib lugeda lähemalt.

-

Sarnaselt paljudele teistele energiasektori aktsiatele on viimastel nädalatel pihta saanud ka maagaasisektori ettevõtted. Chesapeake Energy's (CHK) toimuvad liikumised on olnud üldiselt üpriski suured ning seetõttu sobib lisaks investeerimisele aktsia hästi ka kauplemiseks. Praeguseks on vajutud taas $20 piiri juurde, mida võib pidada heaks sisenemiskohaks nii lühemas kui pikemas perspektiivis. Reedel kinnitas oma ostusoovitust nii Suntrust kui ka Calyon (mõlemal on väljas $25line hinnasiht) ning neljapäeval kiitis ettevõtet ostusoovitusega ka Goldman ($24line siht).

-

Joel, kui CHK aktsia hinnaks on hetkel $20 ja sihiks on $25, siis see oleks 25% tõus. Investeerimise seisukohalt kahtlane, kuna USD ebastabiilsus (nõrkus) võib rikkuda kogu asja ära. Aga jah, kauplemiseks sobib paremini.

-

Regionaalpangad endiselt mahakirjutamistega pahuksis:

"Reuters reports Bank of NY Mellon (BK) will have further writedowns as a result of the securitized mortgages it still has on its books, the bank's chief executive was quoted as saying on Saturday. "Yes, we will book further writedowns but we will be able to handle them. The securitized mortgages on our books amount to $3 to $4 billion, which corresponds to only 2% of our balance sheet," CEO Robert Kelly told Switzerland's Finanz und Wirtschaft. Kelly said the bank, which saw first-quarter profit fall more than expected in April, would be profitable in 2009. "BNY Mellon has posted a profit in all quarters of the crisis. We will also be profitable in 2009," he said."

-

Joel

Mõned Russell 3000 aktsiad, mis reedel lendasid, võiks hoopis lühikeseks müüa? Kiirelt meenutades, siis ZN ja BWEN jt. panid taevasse. -

OunaAnts - kui dollar peaks oluliselt nõrgenema, siis tõenäoliselt tõuseksid selle võrra oluliselt ka dollaris noteeritavad toormaterjalide hinnad (gaas, nafta, kuld jms) ja nendeläbi ka aktsiad endid. GSi $24 prognoos on antud 6 kuu peale, Morgan Stanley ja JPM usuvad, et aastaseks hinnaprognoosiks võiks olla $34-$35, ise usun, et pikemas perspektiivis on võimalik kõrgemalegi tõusta.

-

stocker,

Olen põhimõtteliselt täiesti nõus. Ainult, et riskitaluvus/margin peab piisavalt suur olema ning samuti võib tekkida raskusi aktsiate leidmisel lühikeseks müümisel. Shark kommenteeris seda reede õhtul pärast turu sulgemist väga hästi:

Look at the action in extremely thin stocks like Zion Oil & Gas (ZN) , China Biotics (CHBT) , Isramco (ISRL) and many more. The ETFs are already inefficiently priced enough and this system of rebalancing turns it into a complete farce.

Unfortunately the folks who passively hold the indices aren't even aware of how these big spikes in new additions to the indices come out of their pockets. You now have the Russell 2000 holding shares of Zion at $13.30 when just yesterday you could have bought it for $7. If Zion reverses, that money comes right out of the pockets of the folks who hold the index.

Many of these moves will be reversed very quickly, so there is opportunity if you have a tolerance for a high level of risk and are able to find some shares to borrow. I just hope we won't have to hear how these big moves are legitimate and aren't a form of manipulation.

-

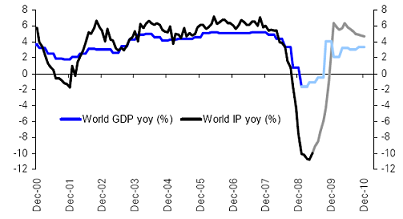

Graafikul on toodud globaalne SKP ja tööstustoodang koos konsensuse prognoosidega. Näitab hästi optimismi majanduskasvu taastumise suhtes, mis näeb välja V-kuju moodi. Kasv peaks algama juba selle aasta teises pooles, mis algab kõigest mõne päeva pärast :)

Allikas: Deutsche Bank

-

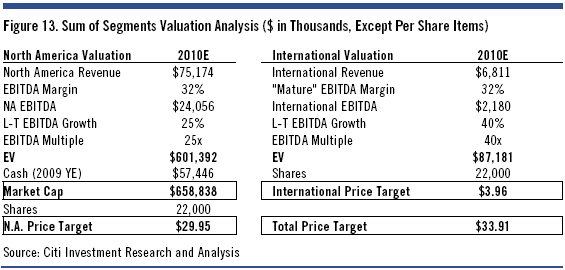

Citigroup’i internetisektori analüütik Mark Mahaney on alustanud OpenTable’i (OPEN), millest hiljuti olen kirjutanud ka portaalis, katmist „Hoia“ reitinguga ja hinnasihiga $34. Analüütikule sümpatiseerib ettevõtte liidripositsioon (üle 90% turuosa) kiirelt kasvaval restoranibroneeringute turul, võimalus kasutada sama süsteem välisturgudele ja tugev juhtkond, mille eesotsas on endine eBay juhatuse liige Jeff Jordan.

$34-lise hinnasihini jõutakse alloleva kalkulatsiooni teel:

Kuigi pikaajalist perspektiivi silmas pidades on tulevik OpenTable’i jaoks helge, siis on väga ebatõenäoline, et lühiajaliselt ühtegi tagasilööki ei kogeta. Seetõttu tunduvad ka Citi poolt rakendatud EBITDA kordajad üsna utoopilised. Samuti kui vaadata aktsia P/E kordajaid, siis Citi prognoosidele tuginedes kaupleb aktsia hetkel vastavalt 177, 109 ja 69-kordsel 2009, 2010 ja 2011. aasta kasumil.

-

Collins Stewart tõstab Microsoftile (MSFT) antavat ostusoovitust ja kinnitab, et MSFT on jätkuvalt nende top pick.

Collins Stewart is raising their tgt to $30 from $26 as they believe Street ests remain too low for FY10/FY11. In addition to 10-12% price increase for Win 7 for OEMs, there are 3 other aspects they are more positive about -- a) cost cutting efforts far better than expected, b) Android & Moblin fear overblown, and c) early good impression of Bing providing far more compelling rationale for higher opex/capex in OSB. They believed (in March) that majority of the bad news was reflected in MSFT but none of the good news such as - a) timely/successful launch of Win 7, b) incr. rev from Win 7 and c) success from cost cutting efforts. They are adjusting their ests to reflect their PC shipment views, higher S&M spend (Win 7 launch) and higher R&D on search (FY10 down/CY10 up). MSFT remains their top pick.

-

USA eelturg on võrreldes reedeste sulgumishindadega väikeses plussis. Nafta on aga +1.8% ja taas ollakse üle $70 rühkinud.

Euroopa turud:

Saksamaa DAX +1.30%

Prantsusmaa CAC 40 +1.38%

Inglismaa FTSE 100 +0.68%

Hispaania IBEX 35 +0.91%

Venemaa MICEX +0.85%

Poola WIG +1.82%Aasia turud:

Jaapani Nikkei 225 -0.95%

Hong Kongi Hang Seng -0.39%

Hiina Shanghai A (kodumaine) +1.61%

Hiina Shanghai B (välismaine) +1.84%

Lõuna-Korea Kosdaq -2.32%

Tai Set 50 +1.06%

India Sensex 30 +0.14% -

Friday Was an Anomaly

By Rev Shark

RealMoney.com Contributor

6/29/2009 9:01 AM EDT

Nothing is so difficult as not deceiving oneself.

-- Ludwig Wittgenstein

Changes to the Russell indices on Friday produced some of the wildest and most deceptive action we have seen in some times. Although the major indices didn't move all that much, volume was huge and dozens of stocks moved 20% or more as index funds scrambled to gain the exposure they needed. Some of the stocks being added to the Russell 2000 and Microcap indices are particularly thinly traded, and the action was downright absurd in many cases. Much of it will probably reverse quickly, so there should be some crazy action again over the next couple of days.

What makes this particularly difficult is that if you weren't aware of what was going on with the indexing, there were some really fantastic charts. There were big-volume breakouts that you'd normally expect to see gain momentum. When stocks move like that, there's usually some solid fundamental reason behind the move, and there may be good reasons you'd want to jump in and maybe chase it higher.

That was not the case on Friday. These stocks moved simply due to indexing; there is no reason at all to suspect that the momentum will continue now that the funds have the shares they need. The ironic thing about these index funds is that it really doesn't matter to them what they paid for a stock. They simply need to have their shares so that their funds reflect what is happening in the index.

To make things even trickier, we also had end-of-the-quarter window-dressing games to go with the indexing. Some of the big-cap momentum favorites like Apple (AAPL) , Baidu (BIDU) , Amazon (AMZN) and Shanda (SNDA) saw some very energetic action as money managers try to add performance points before the quarter ends.

Overall, while the action was favorable in the indices and extremely good in some individual stocks, it leaves us with a rather muddled market. We have been able to rally back to some key resistance levels on good volume, but we haven't quite broken through. The big problem is that there is no good reason to believe the momentum on Friday will be sustained. We really have to be skeptical of what the charts are saying at this point because the action was so artificial.

We have a positive start this morning as some of the strength from Friday carries over. There will be some pressure to at least preserve the mark-ups through tomorrow, but quite often end-of-the-quarter games come to an end a day or two early.

We will have to be patient as the market deals with Friday's action. It was something very exceptional that you don't see too often, and we can't treat it like it like a normal market. We'll have a better sense of the health of the market soon -- just be careful about reading anything into what we saw on Friday.

-----------------------------

Ülespoole avanevad:

Select oil/gas names showing strength: SNP +3.3%, STO +2.0%, RDS.A +1.6%, TOT +1.1%, PBR +1.1%... Select financial names ticking higher: SLM +4.1% (tgt raised to $16 at FBR Capital due to improving student loan spreads and increased earnings potential), DFS +4.0% (upgraded to Outperform from Market Perform at Keefe Bruyette), LYG +3.5% (upgraded to Buy at Goldman- FT.com), HIG +2.8%, RBS +2.0%, AZ +2.0%, FITB +1.7%, AXA +1.6%, STI +1.3%, WFC +1.2%, BCS +1.1% (upgraded to Hold from Sell at Societe Generale)... Other news: DCGN +55.6% (says discovers a gene linked to risk of kidney stones and osteoporosis), CYTR +22.2% (reports "favorable" progress update for its pivotal Phase 2 clinical trial with Tamibarotene as a third-line treatment for acute promyelocytic leukemia), EVTC +13.1% (announced the successful completion of the first Phase I study with its P2X7 receptor antagonist EVT 401), IOC +9.1% (Energy giants to bid for $500 mln gas project - SCMP.com), WEN +7.4% (Wendy's/Arby's mentioned positively in Barron's), SVA +6.1% (receives revised approvals for Panflu), MDRX +6.1% (still checking), CLR +5.2% (Cramer makes positive comments on MadMoney), CSIQ +3.1% (announces 120 MW in recent sales orders), SNY +2.4% (no definitive conclusions can be drawn regarding a possible causal relationship between Lantus use and the occurrence of malignancies), ELN +1.9% (Novartis in talks to buy much of Elan: Report - Reuters), NOK +1.3% (still checking), PCAR +1.1% (renews bank credit facility)... Analyst comments: TRW +11.0% ( upgraded to Overweight from Neutral at JP Morgan), JCP +4.4% (upgraded to Overweight from Equal Weight at Morgan Stanley), RGC +1.6% (upgraded to Buy at Merriman), ZBRA +1.5% (upgraded to Outperform from Neutral at RW Baird).

Allapoole avanevad:

M&A news: EPD -2.1% (light volume; Enterprise Prdcts and TEPPCO agree to merge forming largest publicly traded energy partnership)... Select European drug names showing weakness: GSK -1.4%, NVS -1.4%... Other news: UEC -16.9% (completed a private placement financing involving the sale of an aggregate of 9,099,834 units together with 200,000 common shares at a subscription price of $2.40 per Unit), BIIB -3.6% (reports 10th PML case in Tysabri MS patient - DJ; also downgraded to Hold at Deutsche), STT -2.8% (discloses "Wells" notice relating to ongoing investigation), WW -2.4% (Watson Wyatt and Towers Perrin to combine in a merger of equals to form Towers Watson; also downgraded to Hold from Buy at Citigroup), EPD -2.1% (Enterprise Prdcts and TEPPCO agree to merge forming largest publicly traded energy partnership)... Analyst comments: IPCM -2.7% (downgraded to Hold from Buy at Deutsche Bank). -

Fed's Rosengren says US GDP expected to turn positive in 2H 09

-

Bernie Madoff gets 150 years in prison for ponzi scheme, CNBC reports

-

David Rosenberg täna:

IS THAT ALL YOU GET FOR YOUR MONEY?

And it does seem like such a complete waste of time.

Let’s see. In April, total stimulus from the federal government to the personal

sector, in the form of tax reduction and increased benefits, came to $121 billion

at an annual rate. But that month, in nominal terms, consumer spending rose

the grand total of $1 billion. Then we found out on Friday that in May, the total

stimulus from the Obama economics team came to $163 billion at an annual

rate, and consumer spending increased by a measly $25 billion (again at an

annual rate). The big story is that the personal savings rate surged again to a

new 16-year high of 6.9% from 5.6% in April and 4.3% in March. This is a repeat

of the fiscal impact from the tax relief a year ago when the savings rate jumped

from 0.2% in March 2008 to 4.8% in May 2008. This is what economists refer

to as “Ricardian equivalence” — the money from Uncle Sam goes into the coffee

can instead of being used to buy more coffee.

So let’s get this straight, the future taxpayer is being asked to contribute to a policy

today that is aimed at perpetuating a consumer cycle — and yet for every dollar

that is coming out of Washington to support a 70% consumption/GDP ratio, it is

getting barely more than 8 cents worth of new spending activity. In real terms, as

was the case with the tax rebates of just over a year ago, the real impact is on the

savings rate, and it is very clear that not even the most aggressive monetary and

fiscal policy since the 1930s is going to stop consumer spending in volume terms

from rolling over in the second quarter.

Ja nagu ikka, veel palju huvitavat lugemist. -

CHK pole praegu just kõige parem investeering olnud. Täna turg +0,8%; nafta +2,7%; CHK miinuses. Võiks küsida milles asi, kui vaid keegi seda teaks :)

-

Üks intervjuu siia Faberiga Bloombergi vahendusel - link siin.

-

Balco, arvestades seda, et maagaas (CHK näol tegu ikkagi ju maagaasi aktsiaga) on täna 3% punases, siis mina küll aktsia liikumise üle ei kurda.

-

Kas Madoff läheb OZ-i sugusesse vanglasse?Kaasvangid võivad ju hakata survet avaldama, et äkki veel vanamehel kuskil mõni miljon peidetud.

{kind=link}