Börsipäev 23. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

Kvartalitulemuste avaldamine on täies hoos, enne turgu teatavad oma tulemused teiste seas: AT&T (T), Bristol-Myers (BMY), Ford (F), Manpower (MAN), McDonald's (MCD), Philip Morris (PM), UPS (UPS) ja US Airways (LCC). Peale turgude sulgemist tulevad tulemustega Amazon (AMZN), American Express (AXP), Baidu (BIDU), Broadcom (BRCM), Microsoft (MSFT) ja Sunpower (SPWRA).

Makroandmetest avaldatakse kell 15.30 viimase nädala töötute abirahade taotlejate arv. Konsensus ootab numbriks 577 tuhat, eelmiste nädalate jõudsat vähenemist vaadates võib see arv ka väiksem olla. Kell 17 tehakse teatavaks olemasolevate majade juunikuu annualiseeritud müüginumbrid, konsensuse ootus 4.83 miljonit.

Turg on jätkuvalt tugev, S&P 500 käis eile läbi ka eelmisest tipust, kuid päev lõpetati sellest madalamal. Aasia on hommikul valdavalt rohelises kaubelnud, suurtest turgudest kõige enam on plussis Hong Kong (+2.5%). -

FT kirjutab, et eilsed Wells Fargo & Morgan Stanley tulemused kinnitavad kasvavaid probleeme USA ärikinnisvara turul:

The disappointing second-quarter results for two of the largest lenders and investors in office, retail and industrial property across the US confirmed investors’ fears that commercial real estate would be the next front in the financial crisis after the collapse of the housing market.

Morgan Stanley kirjutas maha $700 mln dollarit oma $17 mld dollari suurusest ärikinnisvara portfellist & ettevõtte CFO ütles: “…he did not see the light “at the end of the commercial real estate tunnel yet”

Wells Fargo hapude ärikinnisvara laenude osakaal hüppas teises kvartalis 69% & panga CFO ütles: “The commercial real estate market is soft, and most of the big banks are seeing the same kind of thing”

Ärikinnisvara hinnad on tipust kukkunud 35%. Bernanke kinnitas eile, et langevad ärikinnisvara hinnad & probleemsete laenude kasvav osakaal on USA majanduse taastumisele raske väljakutse.

-

Kusjuures mälu järgi kirjutades (hetkel ei leia allikat), oli ärikinnisvara ühekuuline hinnalangus kõige suurem juunis. Võrreldes maikuuga kukkusid hinnad ca 8%. Arvatavasti pole enamus pankasid nii kiire langusega arvestanud ning kui see peaks jätkuma, tähendaks see üsna suures mahus varade allahindlusi. Probleem on tõsine, kuigi ärikinnisvara tsükli mahajäämusest võrreldes eluasemeturuga on räägitud juba mitu aastat. Tundub, et nüüd on langus hoogustunud ning Kongressi ees aru andes Bernanke seda ka mitu korda toonitas.

-

Nagu tulemuste hooaja ülevaatest võib näha, lainetab bottom line veerus roheline meri. SP500 ettevõtetest on viiendik oma tulemuse avaldanud, kelle ärikasum on Standard & Poor's andmete järgi keskmiselt 10% ootustest kõrgemaks jäänud, samal ajal küll eelmise aastaga võrreldes 30% võrra vähenedes. Reaktsioon tulemustele on seevastu olnud valdavalt negatiivne. Nüüdseks on juba aru saadud, et ootust lööva kasumi taga on firma efektiivsem juhtimine ning sestab vajatakse kindlustunnet ka müügitulude paranemise osas, mis veenaks investoreid kasumikasvu jätkusuutlikkuses.

-

Kasumi ja tulude löömisest on ka Bespoke Investment teinud kokkuvõtte:

In the first chart below, we have updated the numbers to include today's reports. As shown, the beat rate increased a bit more today up to 72.3%. The highest beat rate we've seen since 2001 was 73% in Q3 '06, so this quarter definitely has a shot to top that.

But while the bottom line numbers are coming in much better than expected, top line numbers have been weak. In the second chart below, we highlight the revenue beat rate so far this earnings season. Of the US companies that have reported revenues, only 49.1% have come in better than expected. While almost everything about this earnings season has been positive so far (including stock market performance), the revenue numbers are one area where things still look pretty bad.

-

Microsoft'i (MSFT) tänane konverentsikõne saab ilmselt üle pika aja keskmisest huvitavam olema. Eelkõige jälgitakse juhtkonna kommentaare Bing'i (Microsoft'i uus otsingumootor) ja Windows 7 osas. Samuti võiks huvi pakkuda, mida ütleb Microsoft konkurent Google'i (GOOG) plaani kohta tuua turule enda operatsioonisüsteem.

-

Kui mais üllatasid Suurbritannia jaemüügi numbrid negatiivselt (oodatud +0.3%-lise kasvu asemel kahanes näitaja -0.9%) siis juunikuu jaemüük osutus oodatust rõõmsamaks. Prognoositud 0.3%-lise tõusu asemel kasvas jaemüük maiga võrreldes neli korda kiiremini (+1.2%). Positiivne üllatus võib olla argumendiks, et UK majanduse langus tõotab pidurduda, ent arvestama peab sellegi poolest üle kümne aasta kõrgeimale tasemele jõudnud töötusemääraga (7.6%) ning ees ootavate maksude tõstmisega, mis röövivad inimestelt ostujõudu ning võivad jätta jaemüügi pikalt vinduma. Lisaks moonutavad jaemüügi numbreid soodustused ja kampaaniad ning loomulikult ilm. Näiteks juunis mõjusid palavad ilmad eriti hästi jalanõude, tekstiili ja rõivaste müüjatele, kelle müük kasvas 4.7% - esimest korda viimase kolme kuu jooksul.

-

Sten Sonts, millal on Microsoft viimati adekvaatset infot andnud kui jutt käib enda vastandamisest konkurentidega? Ballmeri ajast seda küll ei mäleta.

-

22. juuni 2006.... tegelikult on lihtsalt Steve Ballmer'i kommentaare konkurentide kohta lõbus kuulata :)

-

Ford (F) lööb konsensuse ootusi nii käibe kui ka kasumi osas. Aktsia eelturul +5.5%.

Reports Q2 (Jun) loss of $0.21 per share, excluding non-recurring items, $0.27 better than the First Call consensus of ($0.48); revenues fell 33.8% year/year to $27.2 bln vs the $24.76 bln consensus. Based on its current planning assumptions, Ford has sufficient liquidity to fund its product-led transformation plan and provide a cushion against the uncertain global economic environment. In addition, Ford will continue to pursue actions to improve its balance sheet. -

This Market Is Still Sticky to the Upside

By Rev Shark

RealMoney.com Contributor

7/23/2009 8:21 AM EDT

What is without periods of rest will not endure.

-- Ovid

The good news is that earnings reports continue to be quite strong. Ford (F) , eBay (EBAY) , Intuitive Surgical (ISRG) , VMware (VMW) and quite a few others are putting up some solid numbers. The bad news is that the indices continues to become quite extended and in need of consolidation.

The trouble with a strong market is that it doesn't offer easy opportunities for entry. When the buyers are active, you aren't going to see nice gentle pullbacks that allow you to gracefully load up and ride the uptrend.

This market has been particularly tricky since we took off following the Goldman (GS) and Intel (INTC) earnings news. We have barely paused, and the earnings news continues to be quite upbeat.

We have another big round of earnings tonight, the most notable of which is from Microsoft (MSFT) , and given that we have had so little disappointment, anticipation of more of the same is likely to hold us steady.

Most of the major earnings reports will be over after Microsoft reports. There will be many more secondary reports to come, but the major market-movers will be out of the way, with a few exceptions such as Cisco (CSCO) . Reports have obviously been far better than anticipated, and while much of the upside has been due to cost-cutting and containment of expenses rather than revenue growth, it is certainly better than the alternative. Companies have shown that they know how to deal with tough times by adapting. They are still going to need to show that they can grow business at some point, but producing a solid bottom line is good enough for now.

I've been complaining for a few days now that the market has gone up so far so fast that there are few unextended charts. Nothing has changed this morning, and the good earning news isn't providing any convenient excuse for profit-taking.

In a market like this, you have to respect the trend and remember that they often continue far longer than we feel is reasonable. That doesn't mean you have to load up and throw caution to the wind, but you should be wary about anticipating a sudden and complete reversal. Markets that are as strong as this one have been tend to stay sticky to the upside. The folks who have been underinvested offer plenty of underlying support, as they are inclined to buy weakness rather aggressively because they are tired of missing out.

Making new buys here is not easy at all, but we'll keep on looking for situations where the charts aren't too extended. However, until the market consolidates a bit more, you are going to have to chase if you really want to add some long exposure.

--------------------------------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: ISRG +16.0% (also upgraded to Buy at Brean Murray), CCMP +15.9%, TBI +13.8% (also upgraded to Outperform at Baird), SPF +11.9%, AFFX +10.5% (also upgraded to Overweight from Neutral at Piper Jaffray), AATI +9.6% (light volume), TUP +9.3%, CELG +9.2%, EBAY +9.0% (also upgraded to Outperform at RBC Capital), VMW +8.3% (also upgraded to Buy from Hold at Needham), FITB +8.1%, TQNT +7.4%, CYMI +7.0%, NVEC +7.0%, NIHD +6.6%, F +6.6%, FFIV +6.1% (also upgraded to Neutral at BofA/Merrill), ESI +4.4%, SPAR +4.3%, EMC +4.1%, STLD +3.7%, CS +3.7% (upgraded to Buy at Deutsche), BMY +3.5%, EQIX +3.4%, PLD +3.4%, ETFC +2.9%, T +2.9%, KMB +2.5%, MMM +2.4%, RAI +2.0%, SKX +1.5%, MOS +1.5%, ZMH +1.5%... M&A news: MEDX +88.9% (Bristol-Myers Squibb to acquire Medarex for $16.00/share in cash)... Select metals/mining names showing strength: HMY +2.2%, RTP +2.1%, GOLD +1.9%, BHP +1.6%, SLV +1.6%... Other news: SAY +9.6% (still checking), ARM +6.0% (ArvinMeritor and Navistar announce long-term supply agreement), PDLI +5.8% (still checking), ALVR +4.3% (announced that it has agreed with Nokia Siemens (NOK) to expand the existing OEM agreement), HBC +3.2% (up in sympathy with CS), WU +2.7% (Cramer makes positive comments on MadMoney), OXY +1.4% (announces 'significant' California oil and gas discovery)... Analyst comments: SANM +11.1% (upgraded to Neutral at Credit Suisse), ANN +6.9% (raised to Buy from Neutral at Goldman- Reuters), WFR +4.3% (upgraded to Neutral at BofA/Merrill).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: CRA -15.5% (also downgraded to Market PErform at Leerink), PSUN -14.7%, TEX -9.4%, BPFH -9.2%, FLIR -8.9%, LOGI -8.0% (also downgraded to Neutral at UBS), CTXS -6.3% (also downgraded to Hold at Needham and downgraded to Hold at Stifel Nicolaus), SNDK -5.7% (also downgraded to Accumulate from Buy at ThinkEquity), CPTS -5.7%, OMTR -5.1%, NTGR -5.0%, VDSI -4.2%, QCOM -4.1% (also downgraded to Underperform at Charter Equity), ISIL -4.1%, CMG -4.0%, WIRE -3.5%, DHR -3.4%, STM -3.3%, UPS -3.0% (light volume), POT -3.0%, HBAN -2.6%, MCD -2.5%, MOS -2.4%, PNC -2.1%, BCR -1.9% (light volume; also downgraded to Neutral at Piper), EXPO -1.3% (light volume)... Other news: CTIC -15.3% (prices 29,332,107 common shares at $1.30/share), FREE -15.1% (prices 8,731,436 common share offering at $1.80/share), MCO -10.3% (Berkshire Hathaway discloses in Schedule 13D they have reduced stake in co to 16.98% from 20.36%), RT -4.8% (prices 10.0 mln common share offering at $6.75/share), OREX -4.5% (announces proposed 9,000,000 shares public offering of common stock), EDR -4.3% (announces pricing of common stock offering at $4.35), MHP -2.9% (down in sympathy with MCO), DRE -1.7% (announces increase in number of authorized shares of common stock to 400 mln from 250 mln)... Analyst comments: RHT -1.6% (downgraded to Hold at Jefferies), ARO -1.5% (removed from Americas Buy list at Goldman- Reuters), CMO -1.0% (downgraded to Market Perform at Keefe Bruyette). -

The number of people filing new claims for unemployment insurance in the week ending July 18 rose more than expected by

30,000 to 554,000. Economists were expecting claims to rise to 550,000 from the upwardly revised 524,000 claims in the prior week (allikas: thomsonreuters). -

Initial Jobless Claims: 554K, better than the 560K consensus.

-

Pigem nii:

Initial Claims 554K vs 557K consensus, prior revised to 524K from 522K, Continuing Claims fall to 6.22 mln from 6.31 mln -

Continuing Claims fall to 6.22 mln from 6.31 mln -- USAs tööpuudus juba langeb?

-

SideKick, enne kui hõiskama hakata: Continuing Claims “Exhaustion Rate”.

-

küsimärk lause lõpus viitab üldiselt muule, kui hõiskamisele.

-

Economic Data Reviews: Initial Claims Still Filled with Noise

Initial claims for the week ended July 18 jumped 30,000 to 554,000. The consensus estimate stood at 557,000 so the increase was expected. The latest figure left the four-week moving average at 566,000, which is down from 585,000 in the prior week.

Continuing claims for the week ended July 11 fell 88,000 to 6.225 mln. That was the second straight decline for this series and it brought the four-week moving average to 6.54 mln from 6.67 mln.

The market didn't show much reaction to the data since it recognizes it is still filled with noise as the Labor Department sorts out its seasonal adjustment factors to account for the layoffs in the auto industry that occurred earlier than normal. In turn, it hasn't been lost on the market that the initial claims total is still uncomfortably high and ensures we will see another big drop in nonfarm payrolls in the July employment report

The improving trend in continuing claims, meanwhile, isn't being taken at face value (nor should it be) as a hallmark of an improvement in hiring activity. Instead it is seen as a head fake of sorts based on the notion that a number of claimants are dropping out of the computation after having exhausted their unemployment benefits.

-

Euroopa turud:

Saksamaa DAX +0.1%

Prantsusmaa CAC 40 -0.1%

Inglismaa FTSE 100 -0.0%

Hispaania IBEX 35 +0.9%

Rootsi OMX 30 -0.0%

Venemaa MICEX +1.8%

Poola WIG +1.2%Aasia turud:

Jaapani Nikkei 225 +0.7%

Hong Kongi Hang Seng +3.0%

Hiina Shanghai A (kodumaine) +1.0%

Hiina Shanghai B (välismaine) +0.4%

Lõuna-Korea Kosdaq +0.0%

Tai Set 50 +2.7%

India Sensex 30 +2.6% -

üles ja alla avanejate listis on MOS mõlemas?

-

Philip Morris International beats by $0.06, reports revs in-line; raises FY09 EPS guidance (43.88)

Reports Q2 (Jun) earnings of $0.83 per share, $0.06 better than the First Call consensus of $0.77; revenues fell 8.6% year/year to $6.13 bln vs the $6.17 bln consensus. Co raises guidance for FY09, sees EPS of $3.10-3.20, up from prior $2.85-3.00, vs. $3.12 consensus.

Sarnaselt Altriaga tõstetakse 2009. aasta prognoose. Esmapilgul tulemused ilusad, pikem kommentaar peagi Pro alla.

-

Opex, tegelikult Briefing ei avalda neid täpselt samal ajahetkel, seetõttu võib ka selline olukord tekkida. Hetkel kaupleb MOS siiski 0.45% võrra eelturul miinuses.

-

June Exisiting Home Sales 4.89 mln vs 4.77 mln consensus, up 3.6% m/m

-

Turg on ikka äärmiselt huvitav, indeksid lineaarselt üles. Tulemused avaldanud PM hetkel üle 6% sinises.

-

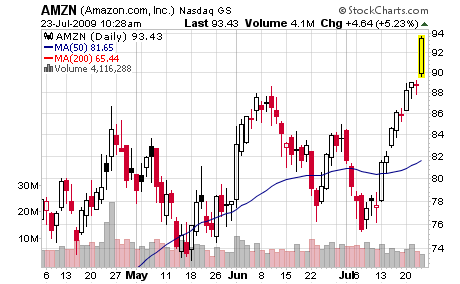

Amazon (AMZN) kaupleb eBay (EBAY) heade tulemuste ja turu üldise tugevuse toel 5% võrra kõrgemal. Aktsia on viimase kahe nädalaga lennanud rohkem kui 20%. Huvitav, milliseid numbreid peab ettevõte täna õhtul raporteerima, et siit tasemetelt oleks veel tõusuruumi...

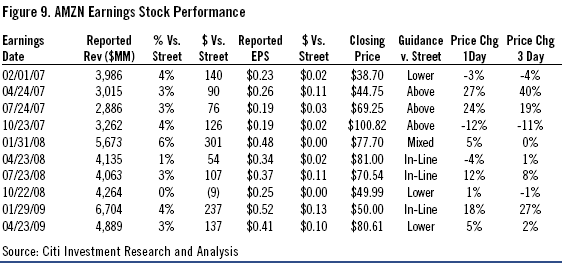

Eelmiste kvartalite tulemustele ja nendele järgnenud aktsiahinna liikumisele saab pilgu peale heita Citi poolt koostatud tabelist:

-

Üheksa päevaga on S&P 500 ligi 11% tõusnud. Kuigi sellise ralli jätkumist eriti uskuda ei tahaks, siis uutele tippudele murdmine oli võimas ja graafik bullish. Makro on oodatust parem olnud ja ehkki kvartalitulemuste puhul võib tulude osas norida, ei ole tegelikult väga halbu tulemusi olnud. Teisalt peavad ilmselt ka pullid nõustuma Bernankega, et kõige olulisem tegur on töötus, millest sõltub tarbimine ehk kolmveerand USA majandusest. Ükskõik, kui aeglaselt töötusemäär tõuseb, on tegemist ikkagi tõusuga ehk miljonitele töötutele lisandub pidevalt sadade tuhandete kaupa uusi töötuid. Samas, kui kindlus tuleviku osas paraneb (aktsiaturgude tõus aitab sellele ka ise tugevalt kaasa), hakkavad töökohta omavad inimesed siiski rohkem tarbima. Aga seda peaks siis ka makroandmetest näha olema.

-

Mis toimub UNG-ga ?

-

UNG-iga toimub see, mida varsti kogu turg teeb.

-

Panen siia Briefingust kommentaari turu optimismi kohta, üsna hea lugemine:

Floor Talk: A few observations on momentum

Our analysts have posted on a number of significant items on the page today, so we'll try to tie some of them together here.

1) Investors need to respect this momentum, even if they are skeptical of its underpinnings. What we mean by that is, even during such a headline-driven environment as earnings season, in a momentum-driven market individual news items such as earnings reports or economic data (which were generally supportive again this morning) lose some of their ability to dictate the direction of the market. In other words, regardless of the headlines, there is an assumption right now that pullbacks, however brief, will be bought. The path of least resistance has been up ever since Goldman's and Intel's earnings reports (see the July 15 & 16 TALKX comments in the archive), so for the near-term we are perfectly capable of rallying on a simple "lack of bad news" right now. To-date, this has caused a lot of pain for those shorting stocks on a bad earnings report (look at POT or CMG today) or "because we're overbought".

2) The new AAII and Investors Intelligence sentiment data released over the past 24 hours shows that there has been almost no move toward bullishness during this rally. So even while it may feel like the bulls' exuberance is getting a bit excessive (if you're watching the market on an intraday basis), this data shows that there is still a lot of skepticism out there, which implies that there is still plenty of cash on the sidelines that could flow into equities.

3) As our technical analysts have noted several times, the Financials have been badly lagging during the recent rally (not going down so much, as simply not participating). Typically, the Financials are one of the main "tells" for the market and this type of action would raise a big red flag. But there is a contrarian way of looking at the Banks now. This terribly distressed group has had huge runs off the March lows, and by many standards the banks are at least fairly valued, if not overvalued. Yet the outlooks have been positive enough that you're really not seeing the "sell the news" reaction that one might have expected now that "the good news is out". By simply moving sideways when you might expect them to be sold, this could be interpreted as at the very least supportive for the market.

4) Another factor that's adding to the upside momentum is purely technical, in that a lot of overhead supply is being eliminated. This is another way of saying that "a lot of stocks are breaking out right now." What this means in terms of supply and demand is that even those buyers who were late to the March rally and who quickly found themselves underwater in early July, are now suddenly showing a paper profit and are thus less likely to sell today than they were even just a few days ago. On a larger scale, the S&P 500 itself, which has been notably lagging the Tech-heavy Nasdaq Comp, finally broke out above the key technical resistance level marked by its June high of 956. Assuming we're able to close comfortably above 956 today, this breakout will be a significant technical event that will bolster the bullish argument.

We're certainly due for some profit-taking after rallying for nine straight days, and it wouldn't be surprising if a miss by a widely-watched company will provide that excuse. But in spite of the overbought nature of this market, the near-term operating assumption has to be that pullbacks will be bought and that the path of least resistance continues to be higher.

-

Selle peale ütleks, et hiljuti oli ka pea-õlad vanaema sündroom. Nüüd ka tehniline breakout, kas tehnikutel tõmmatakse jälle vaip alt?

-

Imax (IMAX) teatas mõni tund tagasi, et Transformerid on Imaxi ekraanidel toonud tulusid üle $40 miljoni, mis iseenesest ei ole enam suur uudis. Filmi on Imaxi ekraanidel juba neli nädalat näidatud, kohe algab viies ja viimane. Hoopis olulisem on trend, mida saab esile tõsta ka teiste filmide puhul - hoolimata sellest, et Transformerite filmi näitamisel on ainult 2% kinodest Imaxi-põhised, on seeläbi kasseeritud 8.5% kogutuludest. Publikus on huvi parema kvaliteedi vastu üha süvenenud ning selle eest ollakse ka nõus rohkem maksma. Lisaks on kinokülastatavus majanduslangusele suhteliselt hästi vastu pidanud, on ju tegemist alternatiiviga kallimale meelelahutusele.

-

arvon, UNG on languses, sest gaasifutuurid lõpetasid oodatust suurema gaasivarude raporti tõttu miinuses.

-

RHI on vastu ootusi väga tugev, hetkel kaubeldakse üle 6.5% plussis. Tundub, et tänastest tingimustes hindab turg võlavabasid ettevõtteid oluliselt kõrgemalt, kui ootasime. RHI kaupleb 66-kordsel 2010. aasta kasumil, mis on täielik müstika. Kui 2010. aasta EPSi ootusi suudetaks lüüa 200% (!), kaupleks aktsia ikkagi ajaloolisest keskmisest kõrgemal kordajal. Sellisel juhul oleks P/E-suhe 22. Samas on turuga suhteliselt mõttetu vaielda, mida näitas ka tulemustejärgne rätiku ringi viskamine Citi poolt. Müügisoovituse asemel soovitati aktsiat hoida ning anti $24 hinnasiht.

Ehkki sellisse cost-cutting EPSi jätkusuutlikkuse ei usu (eriti tõusva töötuse ja pideva tulude languse taustal), siis ilmselt ei tasuks momentumi ette jääda. Anname veel natuke aega, aga kui aktsia ikka üle keskmise käibega uutele tippudele rühib, tuleks natuke tähelepanelikum olla. -

Amazoni numbrid in-line, kuid aktsia kaupleb järelturul $5 võrra madalamal:

Amazon.com prelim $0.32 vs $0.32 First Call consensus; revs $4.65 bln vs $4.69 bln First Call consensus

Amazon.com sees Q3 revs $4.75-5.25 bln vs $4.92 bln First Call consensus -

Microsoft prelim $0.36, ex items vs $0.36 First Call consensus; revs $13.1 bln vs $14.37 bln First Call consensus

Hmm, tulud... -

Tehnoloogiale igal juhul negatiivne päev lõpp.

-

Üsna lahja sooritus kahelt suurimalt tehnoloogiasektori nimelt... kuubikud (QQQQ) järelturul 30c madalamal.

-

MSFT'il on olemas ka väike vabandus...

The financial results for the fourth quarter ended June 30, 2009, included the deferral of $276 million of revenue related to the Windows 7 Upgrade Option program that was announced on June 25, 2009. This revenue deferral reduced earnings per share by $0.02.

... mis siiski eriti kaasa ei aita. -

NFLX numbrid ei taha hästi klappida.. revenue pigem natuke nõrgapoolne, aga EPS hea.. paistab, et see on tulnud madalama customer acquisition cost arvelt. Subscribereid suudetakse lisada hästi ja madalamate kuludega, aga käive nende pealt on väiksem kui oodatud..

Ühesõnaga, virtuaalne short $47 juurest.

update: krt aktsia juba ära kukkunud. -

Ja nüüd siis võtaks virtuaalset kasumit.