Börsipäev 10. august

Kommentaari jätmiseks loo konto või logi sisse

-

Suhkru hinnaralli seoses põuaga Indias ja uputusega Brasiilias, millest Erko täna hommikul siin kirjutab, pole turgudel jäänud tähelepanuta. Sama teemat puudutab täna Bloomberg ka siin, mille üks huvitavam lõik on järgmine:

Sugar surged 76 percent this year, reaching 20.85 cents a pound last week, the highest since April 1981. Bajaj Hindusthan Ltd., India’s biggest producer, predicts it may reach 25 cents by yearend, and Mizuho Corporate Bank Ltd. estimates 30 cents.

The number of 40-cent call options for March 2010 has quintupled to 18,800 contracts in the past four months. A call contract gives the holder the right but not the obligation to purchase a commodity at a given price by a specific date.

Global use may rise 1.3 percent to 161 million tons in the 2009-2010 marketing year, surpassing production of 156.9 million and draining inventories, according to Macquarie Bank Ltd. in London.

“Sugar is certainly going to go much, much higher during the course of the bull market,” Jim Rogers, chairman of Rogers Holdings, said in an Aug. 6 interview in Singapore. “Sugar is still 70 percent below its all-time high and not many things in life are 70 percent below what they were in 1974. Sugar has a wonderful future.”

-

Nagu reede õhtul sai kirjutatud, siis antud nädala alguses mingeid olulisi makrosündmusi enne kolmapäeva tulemas ei ole. Samuti on juba kõik olulisemad ettevõtted ära teatanud oma tulemused ning Wall Streetil algab paljude jaoks puhkuste hooaeg. Kui reedel taaskord uusi tippe tegev aktsiaturg oli paljude karude jaoks knock out vääriliseks löögiks, siis lühemas perspektiivis oleksin ikkagi ettevaatlik. Tõus on olnud ülimalt kiire, complacency suur, risk pettumusteks kõrge ning reedene ilma short squeeze'ita päevalõpp näitas, et lühikeste positsioonide 'sidrunid' on pressitud juba tilgatumaks...

-

igast "analüütikute" mullitamine ajab vaikselt oksele

majanduslangus on see kui hinnad on taskukohased ja majandustõus on aeg kui kõik on igal hetkel räigelt ülehinnatud

sooviks vabalanguse teist lainet

oleks aeg, alles hirmust värisenud ja nüüd ahnusest pakatavatel "indeksitetõstjatel", nahk maha koorida. -

kui nüüd natuke joonida (qqqq) ja esimene punkt tõmmata 2007 aasta nov. algusest, teine 2008 juuni algusest, kolmas 2008 aug. keskelt, siis jõuame tänasesse päeva, mil oleme jälle selle joone vastas.

saab siis näha kas qqqq murrab 50 poole või saabub reaalsus ja võidutseb õiglus -

rams, kas asud ka karude leeri?

-

Illustreerin ramsi mõtted ka ära:

-

Mina näen ainult 2 võimalust:

1) kuna kõik teavad, et korrektsioon alla tuleb, siis üritavad olla esimesed ja see tuleb üsna vara ehk kunagi KL prognoositud ajal so juba septembris

2) turg teeb rahvale tünga ja ütleb, et seekord on kõik teistmoodi (V-turn etc etc) -

Fuel Systemsi (FSYS) oodatust oluliselt paremad tulemused lubasid meil reede õhtul tõsta aktsiale antavat hinnasihti. FSYS on saanud positiivset vastukaja ka teistelt analüütikutelt ning tulemustejärgselt on FSYSile antavat hinnasihti tõstnud sellised väikesed analüüsimajad nagu Janney Montgomery $33 pealt $40 peale, Sidoti & Company $29 pealt $39 peale, Northland Securities $31 pealt $36 peale ning Lazard Capital on tõstnud oma soovituse 'hoia' pealt 'osta' peale ja andnud $35lise hinnasihi.

-

Euroopa autotootjad on täna analüüsimajade tule alla sattunud:

Morgan Stanley langetas Daimler reitingu "overweight" pealt "underweight" peale, kuna 2010. aasta võib kujuneda eelnevalt prognoositust kehvemaks. "Underweight" reiting määrati täna HSBC Holdings poolt ka Saksamaa autotootjale Volkswagen. Hinnasihti vähendati 205 euro pealt 95-le eurole.

-

Suvaliste joonte vedamise asemel võib ka pöörduda finantsastroloogia poole. Sama teeb välja. Bradley mudeli järgi on pööre septembri keskel. Kuu aega võib siis veel vabalt börsil mürada ja jutte graafikutele vedada.

-

HSBC analüütik kes Volkswagenit katab ärkas vist aastapikkusest koomast (:

-

Mobius usub, et ettevõtted on kiiresti tõusnud aktsiahindu lisaemissioonide korraldamiseks ja bilansilehe parandamiseks hakkamas tõenäoliselt üha agaramalt ära kasutama. Ei välista 30%list korrekstiooni. Link artiklile siin.

-

Kui nüüd rääkida Föderaalreservi poolt kehtestavatest intressimääradest ja nende ootustest, siis üks lehekülg, kus neid jälgida saab, on siin. Reedesed sulgumishinnad viitavad sellele, et tänase vahemiku 0.0% kuni 0.25% pealt võiks Föderaalreserv liikuda 0.25% peale juba kas või 2009. aasta novembris, 0.5% peale 2010. aasta veebruaris, 0.75% peale 2010. aasta mais, 1.0% peale 2010. aasta juulis, 1.5% peale 2010. aasta septembris, 1.75% peale 2010. aasta oktoobris ja 2.0% peale 2011. aasta jaanuaris. Tõusvad intressimäärade ootused saavad turgude jaoks kindlasti olema keerulised seedida.

-

Reedel oli näha, et kõrgemad intressimäärade ootused omavad dollarile ka rohkem mõju- aktsiad tõusid, kuid USD kallines (dollari safe haven staatus asendub recovery story’iga?). Selle nädala teises pooles avaldatav USA makrostatistika peaks näitama, kas tugev korrelatsioon dollari nõrgenemise ja aktsiaturgude tõusu vahel lõppeb- neljapäeval avaldatakse jaemüük, reedel IP ja tarbijausaldus.

-

Goldman Sachs on lisamas Eli Lillyt (LLY) oma Conviction Sell listi, 12 kuu hinnasihiks prognoositakse varasema $38 asemel $30.

Goldmani meelest hakkab turg peagi Eli Lilly EPSi pikaajalisi ootusi langetama, sest patentide lõppemine ning nõrk tooteportfell rõhuvad kasumeid. Lisaks on LLY sunnitud suurendama investeeringuid, et tutvustada uusi ravimeid ka pärast 2015. aastat. Samuti usutakse analüüsis, et kuigi verevedeldaja Effienti müügiootusi on viimase aasta jooksul järjepidevalt langetatud, võivad need endiselt turule pettumuse valmistada, mis oleks EPSi langetamise katalüsaatoriks.

GSi hinnasihi langetamine on küllalt suur ning kardioloogide seas läbi viidud uuring Effienti müügi kohta trumbina tagataskus, teeb analüüs LLY aktsiale täna ilmselt üksjagu liiga. Ühtlasi on tegemist analüütikute kõige madalama hinnasihiga (kui väikse jälgitavusega Atlantic Equities'i juuni lõpus antud $29 välja arvata). -

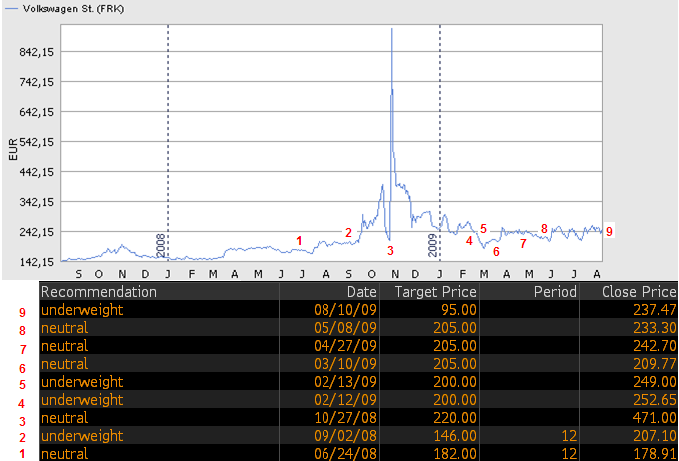

Naxitrall, graafik sellest, milliseid hinnasihte ja reitinguid HSBC analüütik Horst Schneider viimase aasta jooksul jaganud on.

Allikas: Euroland.com, Bloomberg

-

Nafta hinnatõus on siiani tugevalt korreleerunud üldise optimismiga majanduskasvu taastumise suhtes- alates märtsist on iga 50 punkti liikumisega S&P500 indeksis kaasnenud naftahinna $5 dollarit kallinemine. Energiasektor moodustab S&P500 indeksist ca 15% & kõrgem naftahind on pigem ettevõtetele kahjulik kui kasulik. Siiani on naftahind tõusnud üldise makrodata paranemise peale, kuid naftakompaniid ise olid 2Q tulemusi kommenteerides nõudluse suhtes üsna kriitilised & pärast üldise optimismiga harjumist pööratakse ilmselt naftahinda mõjutavatele fundamentaalsetele näitajatele rohkem tähelepanu. Septembri naftafutuurid on täna kukkunud 0.6% ja kauplevad 70.51 dollari juures.

-

mida rohkem pasundatakse, et kõik on rongist maha jäänud ja ahastuses, et korrektsiooni pole olnud, seda rohkem võib uskuda, et oodatav korrektsioon tuleb suurem kui arvatakse ja tahetakse

-

USA turud alustavad päeva kerges miinuses ca 0.4% reedestest tasemetest madalamalt. S&P500 futuurid püsivad veel eelturul aga pealpool 1000 punkti taset, kuigi ise usun, et suurenenud müügihuvi futuurid sellest tasemest varsti ka allapoole lükkavad.

Euroopa turud:

Saksamaa DAX -1.07%

Prantsusmaa CAC 40 -0.92%

Inglismaa FTSE 100 -0.74%

Hispaania IBEX 35 -0.46%

Rootsi OMX 30 -1.19%

Venemaa MICEX -1.87%

Poola WIG +0.89%Aasia turud:

Jaapani Nikkei 225 +1.08%

Hong Kongi Hang Seng +2.72%

Hiina Shanghai A (kodumaine) -0.34%

Hiina Shanghai B (välismaine) +0.87%

Lõuna-Korea Kosdaq +0.78%

Tai Set 50 -0.13%

India Sensex 30 -0.99% -

Arguing With a Trend Doesn't Make You Money

By Rev Shark

RealMoney.com Contributor

8/10/2009 8:53 AM EDT

Never anticipate a moment or day in your life, instead learn to embrace every moment and every day. Find greatness in everything and purpose even in the hardest times.

-- Unknown

The rally in this market that kicked off when earnings season began a month ago has been so consistent and so strong that it leaves little to write about. You can argue against whether it is warranted or not, but if you have been trying to fight it, you have been on the losing side.

I try to avoid making fundamental arguments about the market, because there simply is no way to know when they will matter. It doesn't much matter if your arguments are valid or not, the market will only worry about them when it chooses to ... and that may not be for a very long time.

If you argue against the prevailing trend in the market, you will always be proved right at some point. The trend will always eventually change, but if your timing is off you will be so far underwater that it won't be much of a victory. Folks in the media often get around this by making you sure you never really remember their entry points -- that way they can always declare victory. But for folks who are actually investing, timing is the difference between victory and defeat. If you are right but your timing is off, it isn't going to be a victory.

Since using fundamental arguments is nearly an impossible way to time the market, we have to focus on the actual price action. We have to respect that action, no matter how much we may disagree with it, until it ends. Arguing against its irrationality isn't going to make us money.

Right now this market is engaged in an extremely strong trend. There was a little hesitation last week, but the jobs report on Friday caught the bears by surprise yet again and the buying continued. Certainly the market is due for a rest after the move it has made, but there are few if any signs that a major pullback is likely to ensue. On the contrary, there is likely to be a very significant supply of underlying support to prevent the market from falling too much.

The bearish arguments for this market can be quite persuasive, especially if you are underinvested and are hoping to buy things cheaper, but until the market starts to act weaker, those negative arguments are nothing but more irrelevant talk.

The problem for most bulls at this point is there just aren't many good entry points to be found. All we can do is just keep looking, and more important, we need to guard against being too negative and trying to short the market simply because we have difficulty being aggressively long. Just because we may have a hard time finding new buys doesn't mean that we should be aggressively shorting. Until the price action turns negative, we have to continue to respect the positive trend no matter how much we may not like it.

Early indications are flat. With earnings season over, the news flow has slowed down and I see a fair number of downgrades this morning. The next couple of weeks are peak vacation season -- things are likely to slow, leading to some choppiness, but for now the bulls are still fully in charge.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: FRE +95.9%, CHDX +17.9%, PWRD +15.2% (light volume), DISH +9.2%, CFSG +8.9%, PCLN +6.6%, MCD +1.9%... Select financial names showing strength: AIG +3.7%, C +3.6%, HIG +1.9%, RF +1.4%... Other news: INO +30.4% (Inovio Biomedical and NIH Vaccine Research Center sign research collaboration agreement to develop universal influenza vaccines), ELON +20.5% (signs agreement to supply NES Smart Metering System to Duke Energy), NEP +11.5% (still checking), YRCW +10.2% (freight members ratify YRCW job security plan), FRED +2.8% (Fred's mentioned positively in Barron's), MGM +2.4% and LVS +2.4% (still checking for anything specific), BIN +1.0% (Cramer makes positive comments on MadMoney)... Analyst comments: MRK +2.3% (reinstated with a Buy and added to Conviction Buy list at Goldman- Reuters), BT +1.9% (upgraded to Overweight at JPMorgan), WIT +1.0% (upgraded to Buy at Deutsche Securities).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: GSI -12.0%, AVII -11.3%, ALD -5.7%, DYN -1.6%... Select European financials showing weakness: RBS -8.7%, LYG -8.1% (Lloyds TSB plots share sale to cut state tie - Times of London), IBN -3.5%, BCS -1.6%, AXA -1.4%... Select metals/mining names trading lower: CDE -4.2%, RTP -4.1% (Rio Tinto shares drop on China spy allegations - Reuters), BBL -3.6%, BHP -3.0%, GG -2.0%, SLV -2.0%, ABX -1.8%, AUY -1.8%, AEM -1.7%, MT -1.3%, GLD -1.0%... Select oil/gas names pulling back: SUN -2.2%, STO -2.1%, WFT -2.0%, VLO -1.7% (trading ex dividend), TOT -1.1%, SLB -1.0%... Select European large cap drug names showing weakness: SNY -2.0%, NVS -1.2%... Other news: TRW -6.3% (announces it has commenced an underwritten registered public offering of 14 mln shares of common stock), CROX -6.2% (modestly pulling back after 25%+ jump), NVAX -4.1% (still checking for anything specific), SPAN -1.9% (to lose Sam's Club mattress pad account)... Analyst comments: DAI -4.6% (downgraded to Underweight at Morgan Stanley), LLY -3.7% (added to Americas Conviction Sell list at Goldman- Reuters), VMW -3.0% (downgraded to Underperform at Jefferies), BBY -2.5% (cut to Neutral from Buy at Goldman- Reuters), KG -2.2% (cut to Neutral; removed from Americas Conviction Buy List at Goldman- Reuters), NTES -1.8% (downgraded to Neutral at Pali), RIMM -1.8% (downgraded to Neutral at UBS). -

Kuigi seni pole me Atlandi ookeanilt alguse saanud ja sealt Mehhiko lahele edasi suundunud suuri torme/orkaane näinud, on tegelikult orkaanihooaeg saamas just sisse oma tipptuurid - enamus orkaane leiab aset augusti ja oktoobri vahel. Mehhiko lahele jõudvad orkaanid mõjutavad kindlasti ka nafta ja maagaasi hinnatasemeid, mille populaarsemateks börsil kaubeldavateks instrumentideks on vastavalt sümbolid USO ja UNG. Üks hea netiaadress, kust tormide arenemist ja käekäiku illustreeritud kujul uurida saab, on National Hurricane Center, mille link on siin.

-

Sector ETF strength & weakness through the first hour of trading

Leading Sector ETFs:

Reg banks- KRE +2%, Ag futures- DBA +2%, Solar- TAN +1%, Clean energy- PBW +1.5%, Nat gas- UNG +1%, RBOB gas futures- UGA +1%, Comm banks- KBE +1%, Oil HLDRS- OIH +1%, Pharma HLDRS- PPH +.5%, Wind energy- FAN +.5%Lagging Sector ETFs:

Steel- SLX -2%, Gold miners- GDX -2%, SPDRS metals/mining- XME -2%, iShares REITS/real estate- ICF -1.5%, IYR -1%, Silver- SLV -1%, Basic mat- IYM -1.5%, XLB -1%, SPDRS retailers- XRT -1%, Gold- GLD -1%, SPDRS utilities- XLU -1% -

S&P cuts Estonia to A-; Latvia to BB.

-

The General Motors Company, the new automaker majority-owned by the United States Treasury, said Friday that it intended to make an initial public offering of stock by July 10, 2010, the one-year anniversary of its exit from bankruptcy. The target date range for an offering was disclosed Friday in a federal regulatory filing that the company said summarized its activities in the four weeks since it left court protection. G.M. said it was authorized to issue 2.5 billion shares of common stock. G.M. will begin releasing financial data after the third quarter, a spokeswoman, Renee Rashid-Merem, said.

-

Sector ETF strength & weakness @ midday

Leading Sector ETFs:

Ag futures- DBA +2%, Solar- TAN +1.5%, KWT +1%, Reg banks- KRE +1%, Clean energy- PBW +1%, Comm banks- KBE +1%, SPDRS healthcare- XLV +.5%, RBOB gas futures- UGA +.5%, Pharma HLDRS- PPH +.5%, Oil HLDRS- OIH +.5%Lagging Sector ETFs:

Steel- SLX -3%, SPDRS metals/mining- XME -2.5%, SPDRS retailers- XRT -2%, SPDRS homebuilders- XHB -2%, Base metals- DBB -2%, Basic mat- XLB -1.5%, IYM -2%, Gold miners- GDX -2%, Semis- IGW -1.5%, SMH -1.5%, Silver- SLV -1.5%, iShares REITS/real estate- ICF -1.5%, IYR -1%, SPDRS industrials- XLI -1%, SPDRS tech- XLK -1%, Gold- GLD -1% -

Seoses S&P downgradeiga Eestile ja Lätile, tulevad Balti riigid analüütikutel jutuvestlusse sisse ka muuseas. Viimane kommenaar RealMoney alt siia Howard Simmonsi poolt:

Howard Simons

Baltic States And Eastern Europe

8/10/2009 1:58 PM EDT

Marc's notes on the Baltic states and their various financial troubles underscores an important point. Back in February, it looked as if Swiss franc borrowers in Poland and Hungary were going to go bust. Both German and Austrian banks were on the line for what would have been unpayable debts.

Now the drama has moved north, and it is the Swedish and Norwegians who are at risk. These are small economies relative to Germany and neither currency is part of the euro.

The Swiss took Eastern Europe off the hook with their March quantitative easing. Will Nordic lenders have to do the same, and if so, will their actions continue to fuel a huge bubble forming in Eastern European equities? To ask these questions is to answer them.

When the Asian crisis hit in 1997 with the Thais unable to pay yen-denominated loans, the global response occurred within the context of strong economic growth. It did not involve years of over-ease within a recession. The "tough love" option for the Baltics and Eastern Europe is unlikely, but that this will create a larger problem down the road is a given. -

Ja panen siis sellele eelnenud kommentaari ka juba siia. Teiseltpoolt lompi jagatakse meile õpetussõnu : )

Marc Chandler

S&P Downgrades Latvia and Estonia; More To Come So Stay Short SEK

8/10/2009 12:56 PM EDT

S&P downgraded both Latvia and Estonia and kept the outlooks at negative. This has been expected and today's move is not the last. Estonia was cut to A- from A while Latvia was cut to BB from BB+. Somehow, Lithuania escaped this time but it should have been cut from the current BBB. The only surprise was that the downgrades weren't deeper. The ratings agencies have been overly generous with Eastern Europe, particularly the Baltics. Others that are overrated in the region include Bulgaria, Hungary, and Romania.

Expect Estonia, Lithuania, and Bulgaria to follow Latvia and Romania into IMF programs. This negative view on the Baltics still underscores bearish calls on SEK given the high levels of Swedish banking exposure to the region, and helps explain why SEK was the worst performer today vs. USD and EUR. FX market seemed surprised by the downgrades, but it shouldn't be. Just look at Latvia. It just reported Q2 GDP as contracting 19.6% y/y vs. an 18% drop in Q1. The banking regulator has reported that all overdue loans rose to 23.5% of total loans in June from 22.9% in May, well up from 15% at the end of 2008 and 6.8% at the end of 2007. Those numbers will only get worse with little relief in sight for the economy. Devaluation will, of course, be painful and it won't be a panacea for the region's ills, but we remain skeptical that these governments can stick with the austerity measures demanded (or will be demanded) by the IMF. -

balti riigid on nagu pennistokid, tegid hirmsa lennu ja nüüd võidakse põrmu kukkunud delistida pinksheeti või kuhuiganes