Börsipäev 13. august

Kommentaari jätmiseks loo konto või logi sisse

-

Föderaalreservi kohtumine nüüdseks selja taga ning täna ja homme tulemas vahelduseks ka olulisemaid makroandmeid. Tund aega enne turgu tuleb esmaste töötu abiraha taotlejate arv möödunud nädala kohta, millelt oodatakse näitu 545 000 vs üle-eelmise nädala 550 000. Seega tööjõuturul oodatakse jätkuvat paranemist. Samuti tuleb täna ka juulikuu jaemüük, millelt oodatakse 0.7%list tõusu (ilma autodeta 0.1%). Juunis oli tõusuks 0.6%.

-

Goldman Sachs on täna varahommikul eemaldamas Nokia (NOK) oma 'veendumustega ostusoovituste' nimekirjast ning langetab antava soovituse neutraalse peale, hinnasihiks €11 ehk $15.4. Alates aktsiate Conviction Buy listi lisamisest 17. aprillil, on NOK liikunud -12.6% vs S&P500 +15.7%. Tuleb tunnistada, et see idee on GSil sedapuhku korralikult nihu läinud.

Aga ostusoovituste nimekirjast eemaldamise põhjuseks on GSi nüüdne veendumus, et Nokia on kaotamas teistele konkurentidele turgu – eelkõige keskastme nutitelefonide turul. Ära märgitakse ka N97, mis ei ole tarbijatele piisavalt hästi peale läinud. Kui mid-end turuosa peaks üldse kokku kukkuma, ei välista kõige mustema stsenaariumi järgi GS Nokia aktsiale ka €5list hinda ehk USA turul kauplevatele ADRidele $7.

Kuigi Nokial on tõepoolest täna probleeme Apple’i iPhone laadse toote loomisega, mille tarbija ’lihtsalt peab endale saama’, peaks Nokia aastane €3 miljardiline uurimus-ja-arendustegevuse jaoks mõeldud eelarve ikkagi uute ja ’seksikate’ toodete loomisega lähiajal hakkama saama.

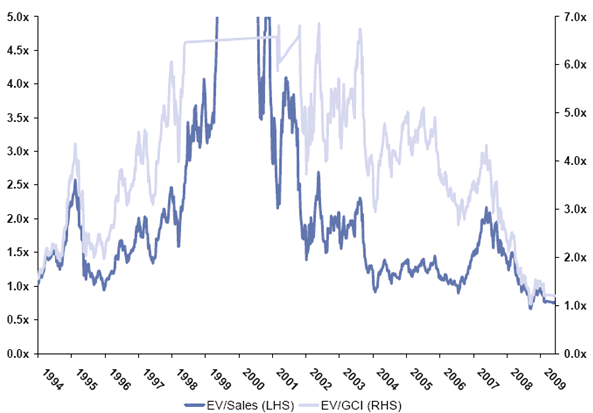

Pikaajaliste väärtusinvestorite jaoks hakkab valuatsiooni poole pealt hoolimata lühiajalistest probleemidest Nokia huvitavaks muutuma - seeega hoiame silma peal. Ettevõtte väärtuse ja müügitulude suhtarv on ajaloo põhjade lähedal:

-

Kui sessoonsusega läbi arvestatud Q1 09 vs Q4 08 langes Saksamaa majandus ca 3.5%, siis Q2 09 vs Q1 09 näidati 0.3%list kasvu. Kasv oli oodatust tugevam ning euro on nende numbrite peale täna lendu tõusnud, tugevnedes dollari vastu üle 0.5%.

-

Hedge-fondi juht J. Paulson on teises kvartalis soetanud 168 miljonit Bank of America (BAC) aktsiat. Paulson on krediidikriisi käigus teeninud miljardeid finantssektori lühikeseks müügiga ja BofA osaluse suurendamine 2%’le on märgatav suunamuutus. Ilmselt ostis Paulson aktsiad alla $10 dollariga ja eile sulges aktsia $15.93 dollari juures. FT kirjutab: He liked it at $9, but does he like it at $16, or $40? BofA tugevustest saab täpsemalt lugeda LHV Pro all.

-

Lisaks Saksamaale valmistas positiivse üllatuse ka Prantsusmaa SKP: oodatud 0.3% languse asemel kasvas Q2 SKP +0.3% võrreldes eelmise kvartaliga. Seega on kaks euroala suurimat majandust võrreldes esimese kvartaliga kasvama hakanud.

-

Oma viimase kvartali tulemused peaks täna Eesti aja järgi kell 14.00 turule teatama USA hiidjaemüüja Wal-Mart (WMT). Ettevõttelt oodatakse näha tulusid 103.1 miljardi eest (eelmise aasta sama kvartaliga võrreldes ca +0.4%) ning eelmise aasta sama perioodiga võrreldes sama suurt EPSi ehk $0.86.

-

Baltic Dry Indexit oleme foorumites koos Alariga juba korduvalt välja toonud. Kui eelmise aasta lõpus $BDi kukkumine sai otsa ja toimus stabiliseerumine, millele järgnes aasta alguses korralik spurt ülespoole, ennetades paari-kolme kuuga aktsiaturu liikumist, siis nüüd vaatab vastu peegelpilt. Indeks on kukkunud alates juuni algusest, kuid aktsiaturud on jätkanud ülespoole rühkimist. Pullidele on sellised käärid liikumiste vahel niigi harukordselt kiiresti tõusnud aktsiaturu taustal igaljuhul tõsiseks ohusignaaliks.

-

Euroopa turud on suurriikide oodatust paremate SKP numbrite tõttu korralikus tõusus ning optimismist on taaskord nakatunud ka USA futuurid, mis on hetkel ca 1% jagu eilsest sulgumistasemest kõrgemal.

-

WMT tulud alla, kasum üle ootuste:

Briefing: Wal-Mart prelim $0.88 vs $0.86 First Call consensus; revs $100.08 bln vs $102.90 bln First Call consensus. -

Weekly Initial Jobless Claims 558K vs 545K consensus; prior revised to 554K from 550K.

Continuing Claims 6202K vs 6300K consensus; prior revised to 6343K from 6310K.

July Retail Sales ex-Autos -0.6% vs +0.1% consensus; prior revised to +0.5% from +0.3%.

July Advance Retail Sales -0.1% vs +0.8% consensus; prior revised to +0.8% from +0.6%. -

Jaemüügi oodatust nõrgemad numbrid ja oodatust kõrgemad esmaste töötu abiraha taotlejate arvud andsid eelturul juba 1.3%lisse plussi tõusnud turule jääkülma duši. Praeguseks on alles veel vaid pool protsenti plussi.

-

Euroopa turud:

Saksamaa DAX +0.79%

Prantsusmaa CAC 40 +0.41%

Inglismaa FTSE 100 +0.76%

Hispaania IBEX 35 +1.06%

Rootsi OMX 30 +1.61%

Venemaa MICEX +0.89%

Poola WIG +2.18%Aasia turud:

Jaapani Nikkei 225 +0.79%

Hong Kongi Hang Seng +2.08%

Hiina Shanghai A (kodumaine) +0.90%

Hiina Shanghai B (välismaine) -0.07%

Lõuna-Korea Kosdaq +1.74%

Tai Set 50 +2.14%

India Sensex 30 +3.32% -

Same Old Story

By Rev Shark

RealMoney.com Contributor

8/13/2009 8:51 AM EDT

When you jump for joy, beware that no one moves the ground from beneath your feet.

-- Stanislaw J. Lec

The market rallied strongly Wednesday on the interest rate announcement from the Fed that contained nothing; the fierce move higher was very surprising. However, the market has had a tendency to rally on the Fed lately no matter what it does, and that inclination was good enough for the bulls, who are still riding a powerful wave of momentum.

This morning we have news of better-than-expected GDP reports in Germany and France and a disclosure that a hedge fund manager, who made a huge amount of money on the subprime debacle, was long some banks as of June 30. The market is gapping up on this news and is being led by the banks. We also have Wal-Mart (WMT) earnings that were ahead by 2 cents, and the stock gapping up $1 or so.

Market players continue to feel quite good, and as I keep writing, even though the market is technically extended and in need of a rest, we just have too much momentum and underlying support for us to pull back much. News like we have this morning just increases the intensity of the dip-buying inclination. Underinvested bulls who don't like to buy strength just aren't getting any good opportunity to jump into this market.

It will be instructive today to see if the bulls continue with the steady buying. We have not had any intraday reversals to the downside in quite some time. Once we start off strong, we just keep on going as folks scramble to find long exposure.

Economic data is out and is a bit weaker than expected, which is cooling things off as I write. We haven't had many disappointing economic reports lately, and it will probably take more than just one report to put a dent in this market.

So the game remains the same. The news flow is good, momentum is staying extremely strong and we have lots of underlying support in the form of folks who want to buy a pullback. Keep in mind that market trends always seem to last longer than you think they will.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: HRS +14.1% (also upgraded to Buy at Morgan Joseph), DPS +10.5%, UTA +8.5%, ULTR +7.8% (light volume), PUK +7.8%, ANW +6.0%, SRX +5.1%, KGC +4.3%, MON +1.9%, WMT +1.6%... Select financial names showing strength boosted by Paulson & Co filings disclosing new positions in several names: ING +6.0%, UBS +5.6%, RF +5.4% (Paulson & Co discloses new 35 mln share position in SEC filing), COF +4.9% (Paulson & Co discloses new positions in SEC filing; up to 17 mln from 2.1 mln), BAC +4.8% (Paulson & Co discloses 168 mln share new position in SEC filing), AIG +4.4%, DB +4.3%, FITB +3.8%, BCS +3.1%, C +3.0%, AIB +3.0%, GNW +2.8%, HBC +2.6%, HIG +2.6%, CS +2.5%, WFC +2.3%, XLF +2.1%, JPM +1.5%, MI +1.4% (Paulson & Co discloses new 12 mln share position in SEC filing), GS +1.4%... Select metals/mining names trading higher: AU +5.1% (Paulson & Co discloses new positions in SEC filing), HMY +4.7%, GFI +4.6%, GOLD +4.1%, RTP +3.7%, BHP +2.8%, VALE +2.4%, EGO +2.3% (identifies new gold zone in China; also Cramer makes positive comments on MadMoney), MT +1.8%... Select casino related names showing strength: LVS +4.1%, MGM +4.0%, MPEL +2.8%... Select shippers ticking higher: PRGN +5.1%, DRYS +2.5%... Other news: BPAX +58.2% (reports positive LibiGel safety data in Phase III program), TSEM +8.6% (the co and Intersil announced they will work together to develop a new high-performance power management specialty process technology platform), TPI +6.3% (receives Chinese SFDA approval for Sanqi Tablets and Yinqiao Jiedu Tablets), F +2.6% (still checking for anything specific), OCN +1.6% (prices public offering of 28 mln shares of common stock at $9/share), PAYX +1.3% (Cramer makes positive comments on MadMoney)... Analyst comments: POT +2.6% (initiated with Overweight at Thomas Weisel), SOL +2.6% (upgraded to Outperform at Credit Suisse), SHPGY +1.4% (Shire (acquisition would make strategic & financial sense- Citigroup).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: XSEL -18.5%, LDK -14.8%, UBET -9.1%, MIDD -9.1%, AEG -7.4%, NTES -5.7%, AAP -5.4%, SBLK -3.5%, CHLN -3.3%, ONTY -3.2%, URS -3.1%, KSS -2.4%... Other news: MWE -9.4% (announces 4.7 mln common share offering; entity controlled by a director of the general partner of the Partnership is selling 300k shares), YSI -7.4% (announces it commenced a 22 mln share common stock offering), SOLR -5.2% (filed for a ~105.53 mln share common stock offering by selling shareholders), GSIC -4.6% (prices 3,661,150 common share offering at $17.00/share), CRY -3.6% (modestly pulling back following yesterday's late day surge higher), CCL -2.3% (Arison family to sell up to 8.5 million shares of Carnival Corporation), AINV -2.2% (prices 18.0 mln common share offering at $8.75/share), BG -1.3% (prices 10.50 mln common share offering at $65.50/share)... Analyst comments: PALM -2.6% (downgraded to Sell at Morgan Joseph), HTX -2.1% (downgraded to Neutral at Credit Suisse and downgraded to Underweight at HSBC), DHI -1.9% (downgraded DHI to Sell from Hold at Citigroup), CBS -1.0% (downgraded to Sell at Caris & Company). -

Eelturu 1.3%line pluss on totaalselt ümber pööratud ning S&P500 indeks on langenud miinuspoolele. Päev on muidugi veel äärmiselt noor, aga vägisi tundub, et optimismist hoolimata on pullide jalgealune muutumas kuumaks.

-

June Business Inventories -1.1% vs -0.9% consensus; prior revised to -1.2% from -1.0%

-

GM CEO Fritz Henderson, on CNBC, says that demand in last week or so of July increased by 30%; August is off to a very good start

-

Maagaasivarude muutus laias plaanis vastavalt ootustele:

Natural gas inventory showed a build of 63 bcf, analysts were expecting a build of 65 bcf, ranging from a build of 58 bcf to a build of 71 bcf. -

30-year bond auction results: High Yield: 4.541%; Bid-to Cover: 2.54 (vs average of 2.22 since 2006 reinstatement of the 30-year); Indirect Bidding: 48.1% (vs average of 32.7% since 2006 reinstatement)

The previous smaller $14 bln 30-yr offering in May saw a 2.14 bid to cover and an indirect bidder take of 33%. The average has been 2.22 and 32.7% since the maturity was reinstated in 2006.

Ja turg astub julgelt ülespoole.