Börsipäev 14. august

Kommentaari jätmiseks loo konto või logi sisse

-

Aktsiaturud jätkavad oma trotslikku tõusujoont ning eilse päevalõpu spurdiga sulgus S&P500 indeks uuel kõrgeimal tasemel alates oktoobri algusest ja Nasdaq100 indeks kõrgeimal tasemel alates septembri algusest ja seda hoolimata oodatust oluliselt nõrgemast jaemüügiraportist. Euroopast tulnud teated üllatuslikult positiivse Q2 SKP muutuse kohta leidsid investorites helgemat vastukaja. Ise jään oma arvamusele kindlaks ning leian, et riski-tulu suhe ei soosi enam lühemas perspektiivis ülespoole liikumisele panustamisele.

Tund aega enne USA turgude avanemist teatatakse juulikuu tarbijahinnaindeksi muutus - ootuseks on 0.0% ning kui Föderaalreserv tahab jätkata oma 'erakordselt pikka madalate intressimäärade poliitikat', siis CPI eriti tõusta ei tohiks. Eesti aja järgi kell 16.15 teatatakse ka juulikuu tööstustoodangu muutus, millelt oodatakse 0.4%list kasvu. -

Kuigi hetkel on USA aktsiaturud näitamas viiendat järjestikust nädalat, mil ollakse taas kõrgemale rühkimas, pole viimastel päevadel Hiinas nii hästi läinud. Hiina Shanghai A indeks kukkus täna 3% võrra ning 8 börsipäevaga on kokku langetud juba 12%. Bloomberg on langusest teinud ka ühe lühikese artikli, mille link on siin. Hiina turgude nõrkus peaks avaldama mõju ka teistele aktsiaturgudele.

-

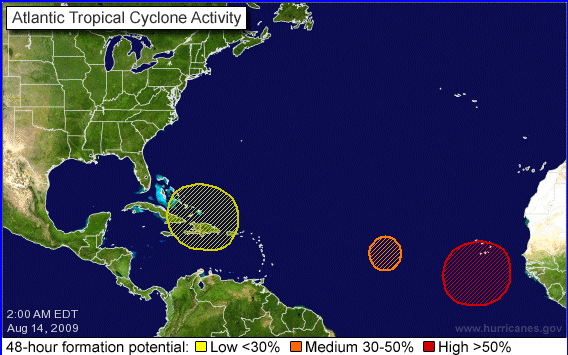

Tasapisi hakkab aktiviseeruma ka orkaanide moodustumise võimalused Atlandi ookeanil. Täna võime NHC leheküljelt leida juba kolm võimalikku orkaani:

-

TradeStation (TRAD) saab täna Ladenburgilt ostusoovituse ja $10lise hinnasihi. Tegu ettevõtega online-maaklerluse segmendist, mis on analüütikutelt viimasel ajal päris palju positiivset vastukaja saanud.

-

Juulikuu tarbijahinnaindeks tõusis mom 0.0% vs oodatud 0.0% ja yoy -2.1% vs oodatud -1.9%.

Ilma toiduaineteta ja energiata oli mom muutuseks +0.1% vs oodatud +0.1%. -

Euroopa turud:

Saksamaa DAX +0.32%

Prantsusmaa CAC 40 +0.62%

Inglismaa FTSE 100 +0.45%

Hispaania IBEX 35 -0.18%

Rootsi OMX 30 -0.65%

Venemaa MICEX -0.22%

Poola WIG +1.24%Aasia turud:

Jaapani Nikkei 225 +0.76%

Hong Kongi Hang Seng +0.15%

Hiina Shanghai A (kodumaine) -2.98%

Hiina Shanghai B (välismaine) -3.09%

Lõuna-Korea Kosdaq -0.11%

Tai Set 50 -0.46%

India Sensex 30 -0.69% -

Anticipation Can Get You Into Trouble

By Rev Shark

RealMoney.com Contributor

8/14/2009 8:45 AM EDT

Expecting is the greatest impediment to living. In anticipation of tomorrow, it loses today.

-- Seneca

Although the pace of the market ascent has slowed a bit since the first of August -- the Nasdaq closed on Thursday around the same place it was on Aug. 5 -- the technical action of the market continues to be extremely positive. In fact, the slowing momentum is providing some consolidation of recent gains and helping to build some bases.

The big question for market players is whether a slowing in the market advance is a prelude to a pullback. As I've discussed, the market is very unlikely to suddenly collapse. Market players will not be discouraged until dip-buying fails to work and there are a number of cracks appearing. As long as immediately buying weakness continues to work, market players are going to stick with the market ... no matter what. We saw a particularly good illustration of this yesterday when poor news about foreclosures and retails sales did nothing but slow down the rate of the advance.

One of my basic market rules is that indices tend to be "sticky" to the upside after a strong move. We almost always hold up longer and better than most people think we will. That doesn't mean that we won't eventually succumb to a correction, but it does mean that it is very easy to be premature in anticipating one. This recent advance has been a classic illustration: Folks have been looking for this market to pull back since the advance began back in March. It looked like we were starting to roll over at the start of July, but earnings season caused us to explode upward, and that is what really caught folks by surprise.

I believe we are going to see a fairly severe correction starting within the next month or so, but such predictions are pretty useless because it is the timing that is key. I have no idea when and at what levels we will top, and I'm not going to try to predict that. What I will do is monitor the action and look to react as I see signs that the character of the market is changing.

Right now I see little to indicate that we are the cusp of rolling over. The biggest thing the bears have going for them is that this market has surprised so many with how fast and how far it has gone up. It just seems reasonable to expect a correction, but one thing we know is that we shouldn't expect the market to be reasonable in what it does.

So the trend continues to be up and the technical action positive. The bulls are in control, and until they falter they should be given plenty of respect.

I'm going to be taking some vacation time starting today and then next week. I'll be posting on a limited basis, but I'm going to try to shut the computers down, ignore the market a bit and clear my mind.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: GRRF +31.0%, LWAY +21.9% (light volume), TBUS +9.7%, SKBI +9.1%, FNET +8.2% (light volume), VIT +5.1%, ANF +4.5%, ADSK +3.3%... Select financial stocks showing strength: AIB +8.0% (Royal Bank of Canada seeking stake in AIB, according to source - DJ), RF +4.8% (BofA/Merrill upgrades to Buy from Neutral), IRE +4.4%, C +3.4% (upgraded to Buy from Underperform at BofA/Merrill), KFN +2.4%, ZION +2.0% (coverage resumed with a Market Perform at FBR Capital), BCS +1.9%, LYG +1.7%... Select shippers ticking higher: EGLE +4.2%, SBLK +3.5% (initiated with Outperform at FBR Capital)... Other news: RJET +9.8% (announced as winning bidder in auction of Frontier Airlines), RMBS +8.2% (still checking), OREX +4.8% and FSYS +4.3% (Cramer makes positive comments on MadMoney), DMRC +3.1% (awarded contract to help secure nuclear weapons in U.S. Navy custody), RYAAY +2.5% (still checking), BSX +2.0% (CEO bought 100K shares at $11.06 on 8/11)... Analyst comments: COLM +7.7% (upgraded to Overweight at Barclays), DNN +5.4% (upgraded to Neutral from Underperform at Credit Suisse), THC +5.4% (upgraded to Outperform at Baird), SCSS +5.3% (upgraded to Buy from Not Rated at KeyBanc), EJ +3.0% (upgraded to Outperform from Perform at Oppenheimer), TRAD +2.4% (initiated with Buy at Ladenburg), SPWRA +2.4% (initiated with a Buy at Needham), RDS.A +1.5% (upgraded to Buy from Hold at Citigroup).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: BBI -20.9% (also downgraded to Neutral at Wedbush Morgan), JADE -15.2%, JST -12.4%, CRDC -10.4% (also downgraded to Hold at Brean Murray), SATC -10.1%, NEP -7.0%, DAR -4.9%, RRGB -4.3%, JCP -1.3%, JWN -1.0%... Select financial names pulling back: ING -2.4%, HBC -2.3%, GNW -2.1% (downgraded to Sell from Hold at Citigroup), AIG -1.8%... Select homebuilders ticking lower: HOV -2.4%, BZH -2.3%, KBH -1.8%... Other news: TBBK -16.0% (prices 10.0 mln common share offering at $5.75/share), MSPD -6.4% (announces pricing of 4.75 mln common stock offering at a public offering price of $2.05 per share), ARCC -6.3% (announced 8 mln common share offering), MAKO -3.5% (announces it intends to offer shares of common stock pursuant to its existing shelf), UMPQ -3.2% (prices approx 23.1 mln common shares at $9.75/share), BA -3.0% (Boeing halted work at Dreamliner plant - WSJ), CROX -2.9% (still checking), GLDD -2.6% (prices 12.5 mln shares of its common stock at $5.75 per share), KG -1.7% (confirmed FDA approved EMBEDA for management of moderate to severe chronic pain; also downgraded to Hold at Needham), GPI -1.4% (filed mixed securities shelf offering), AZN -1.4% (still checking), MON -1.4% (Last night on CNBC, Cramer said the Obama administration is stepping up its antitrust enforcement and MON could be the first target)... Analyst comments: KIM -3.1% (downgraded to Sell from Neutral at UBS), WRI -2.2% (downgraded to Sell from Neutral at UBS), SLG -2.1% (downgraded to Neutral from Buy at Goldman - DJ), BXP -1.1% (downgraded to Sell from Neutral at UBS), AVB -1.0% (downgraded to Sell from Neutral at Goldman - DJ). -

Võrdluseks- euroalas kukkusid hinnad 0.7% YoY & veel juulis oli langus 0.1% YoY (Ilma toiduaineteta ja energiata oli YoY langus juulis 1.3% vs 1.4% juunis).

-

Üks väga pikk, pisut üle 3 tunnine audiolõik, on üles laetud Bloombergi neti-keskkonda. Pealkiri on igaljuhul erutav - Austraalia keskpank kaalub ka intressimäärade kergitamist. Mäletatavasti on sellele hiljuti vihjanud ka Norra keskpank ning koos stabiliseeruva majandusega võib ka ECB tõsta intresse varem, kui paljud ootavad.

Nüüd aga küsimus - kui maailma teised keskpankurid on valmistumas intressimäärade kergitamiseks, siis kas paljude analüütikute ootused selles osas, et Föderaalreserv tõstab USAs intresse alles 2010. aasta teises pooles (kui üldse), on ikka õigustatud?! Kui väline surve suureneb, ei pruugi analüütikute poolt loodetud 0%lised intressimäärad USAs sugugi nii kaua kesta - vastasel korral saaks lihtsalt dollar peksa. Ootused võivad muutuda kiiremini, kui me seda arvame. Juba ainuüksi viimase 3-4 kuu aktsiaturgude ralli on seda näidanud, kui kiiresti võivad ootused muutuda.

-

USA juulikuu tööstustoodangu muutus oli +0.5% vs oodatud +0.4%.

-

Fuel Systems (FSYS) hetkel ühtede väheste seas, kes turu languse taustal plussis vee püsib. Põhjuseks eileõhtune Jim Crameri poolne aktsia pushimine, kes ütles, et aktsia võiks iseenesest ka $43 maksta. Link Crameri põhjendustega siin.

-

Turgude langusele andis hoogu juurde UofM tarbijate sentimendi indeks, mis kukkus augusti alguses 63.2 punkti peale, mis on oluliselt madalam, kui 66 punkti juulis ja 68.5 punkti, mida ootasid ökonomistid. Koos jaemüügiga on sentimendi langus selge märk, et USA tarbijad ei ole veel aktsiaturgudel leviva optimismiga kaasa läinud (siit saab USA tarbija rollist pikemalt lugeda).

-

Briefingus jäi silma väljavõte Carl Icahni tegevusest:

Carl Icahn discloses changes to portfolio in SEC filing -- ARII, BIIB, BBI, GBNK, LGF, YHOO, MOT, AMLN

In a 13F filing out moments ago, Icahn discloses new positions as of 6/30 from 3/31 in ARII (11.5 mln shares); decreases in BIIB (to 3.2 mln shares from 10.5), BBI (to 3.7 from 14), GBNK (to 3.8 from 14.7), LGF (to 3.4 from 13.4 mln), (YHOO to 15.1 from 60); liquidates (MOT 120 mln shares), AMLN (12.9 mln). -

S&P 500 toetatakse päris ilusti 996 pealt, kui sealt peaks läbi vajuma siis ilmselt liug ka 990 juurde.

-

Käis ka 995 all, ei juhtunud midagi.

-

See oli ainult kerge spike alla, mis kohe tagasi osteti. Hetkeks turg liikunud juba mitmendat korda antud taset testima ja püsib sellele väga lähedal, kas läheb läbi?

-

996 tase on lausa magnet, kuid läbi ei jõuta minna:)

-

Sector ETF strength & weakness @ midday

Leading Sector ETFs:

US bonds- TLT +1%

Lagging Sector ETFs:

Crude/WTI oil- USO -4.5%, OIL -4.5%, RBOB gas futures- UGA -4.5%, Reg banks- KRE -3.5%, SPDRS homebuilders- XHB -3.5%, Oil HLDRS- OIH -3.5%, Base metals- DBB -3.5%, SPDRS metals/mining- XME -3.5%, Coal- KOL -3.5%, iShares REITS/real estate- ICF -3%, IYR -3%, Coal- KOL -3.5%, Steel- SLX -3%, Basic mat- XLB -3%, IYM -3%, Commods- DBC -3%, GSG -3.5%, Semis- SMH -2.5%, IGW -2.5%, RUT 2000- IWM -3%, Silver- SLV -2.5%

-

BAC käitumas eriti tugevalt, üsna suure käibega vallutatakse uusi tippe. Kogukäive siiski väga väike võrreldes viimase aja aktiivsusega, uudiseid pole samuti silma jäänud.

Ja kogu turg tiksub jällegi ilma käibeta ülespoole. Kusjuures eile oli viimase aja väikseim kogukäive ja uued tipud:) -

Täiesti käibevaba loksumine siiani ja pool tundi veel jäänud nädala viimast kauplemispäeva. Kas kellegil tekib huvi turgu ühele või teisele poole liigutada?

-

BACi tõusu taga on kuuldavasti põhjuseks suured Merrill Lynchi aktsiaostud pangas...