Börsipäev 9. oktoober

Kommentaari jätmiseks loo konto või logi sisse

-

Täna olulisi majandusraporteid ega ettevõtete kvartalitulemusi tulemas ei ole. Järgmine nädal on tulemuste hooaeg aga juba suurema hoo sisse saamas.

Bloombergist leiab täna hommikul kaks pisut huvitavamat artiklit - esimene artikkel on selle kohta, et Läti on IMFi ja Rootsiga tõenäoliselt ikkagi jõudmas kokkuleppele laenurahade saamise osas (link siin) ning teine artikkel on selle kohta, et Föderaalreservi esimees Ben Bernanke lubab, et kui majanduse väljavaated on ikkagi oluliselt taastunud, et siis ollakse valmis ka intresse tõstma, kuid et selliste sammudeni läheb tõenäoliselt veel palju aega (link siin).

-

Üks intervjuu üksikute allesjäänud karudega. Ed Rogers ütleb selles intervjuus, et enne aasta lõppu võib Jaapani aktsiaturg (ning ka teised turud) kukkuda 10% kuni 15% - link siin.

-

rõhk sõnal võib

ma väidan, et homme võib päike tõusta läänest! -

USD ignoreeris pāris hāsti Aasia turgude tōusu, nāis kauaks Bernanke sōnavōtu mōju kestab. sulgesin eilse shorti (1.4718, +67 pips) ja lāksin pikaks 1.4721, ja GBP/USD tasemelt 1.6005.

-

Cable, edaspidi kui võimalik, postita umbkaudselt ka suletud tehingu risk, kasum ilma riskita on suhteliselt sisutühi number.

-

Äkki on juba mõne muu foorumi all, aga reede puhul üks link tuleviku prognoosimisest: "15 Failed Predictions"

“I think there is a world market for maybe five computers.”--Thomas Watson, chairman of IBM, 1943 -

Täna küll ei julgeks väita, et eur/usd tõuseb. Hetkel kalduks pigem languse poole.

-

Jep, ikka alla, kui Ben juba sõrme vibutab.

Briefing

09.10.09 05:18 ET

Bernanke sees tighter policies as economy heals - Reuters

Reuters reports Federal Reserve Chairman Ben Bernanke said on Thursday that while the U.S. central bank's vast support for the economy will likely be needed for a while, the Fed will have to remove those measures as the economy heals to ward off inflation. "Accommodative policies will likely be warranted for an extended period," he said in remarks prepared for delivery at a monetary policy conference at the Fed. "At some point, however, as economic recovery takes hold, we will need to tighten monetary policy to prevent the emergence of an inflation problem down the road." Bernanke, in a detailed description of the bank's balance sheet -- which has ballooned from around $900 bln to near $2.1 trln -- said the Fed has the tools and the ability to pull back its flood of cash and loans to the economy and to raise interest rates when the time is right "When the economic outlook has improved sufficiently, we will be prepared to tighten the stance of monetary policy and eventually return our balance sheet to a more normal configuration," Bernanke said. As the economy appears to be pulling out of a painful and lengthy recession, observers are watching closely for signs of when and how quickly the Fed intends to pull back its help. Bernanke said the Fed could remove its easy money policies even while its balance sheet remains bloated. To do so, it would raise interest rates on reserve balances that banks keep at the Fed and by other actions -- specifically reverse repurchase agreements, term deposits to banks, and sales of holdings of longer-term assets. Those steps would drain cash from the system and help raise short-term interest rates, he said. -

GBP ei leia kuidagi ostjaid, vaatamata oodatust parematele majandustulemustele. kuuldavasti ollakse jālle murelikud QE poliitika edukuse pārast.

S/L 1.5910 -

Kogu nende forexi tehingute jaoks võiks täitsa eraldi teema teha, siia kaovad tehingud ära eri börsipäevade sisse kirjutatuna.

-

Enamust see niikuinii ei huvita. Kadugu pealegi.

-

Euroopa börsidel väga vaikne tiksumine. Soomes kaupleb Nokia aktsia +0.7% (€9.92). JPMorgan on lisanud aktsia oma kauplemisnimekirja €11 euro suuruse hinnasihiga ja Bernstein kinnitab „outperform“ soovitust hinnasihiga €12 eurot.

-

Story of the day - http://www.bloomberg.com/apps/news?pid=20601109&sid=

-

Kanada yllatas: +31K t'o'o'kohta ja -puudus langes 8,7lt 8,4%le

http://www.statcan.gc.ca/subjects-sujets/labour-travail/lfs-epa/lfs-epa-eng.htm -

Tehnoloogiasektoris on hinnasihtide tõstmise ralli lahti läinud. Täna tõstab Credit Suisse Google'i (GOOG) hinnasihi $475 pealt $600 peale.

-

Samal ajal kui tehnoloogiasektoris käib hinnasihtide tõstmise pidu, jäi silma tänane Auriga müügisoovituse kinnitus Inteli aktsiale, kus öeldakse, et nende arvates on head uudised juba aktsiasse sisse ära arvestatud.

Auriga notes that they clearly underestimated the magnitude and rapidity of the snapback in semiconductor fundamentals off depressed Q109 levels; that said, in their view, most of the good news is already in INTC stock. A PC refresh cycle in 2010 is now consensus thinking, but to the firm, this seems more dependent on market expansion, driven by a desire for new functionality or broader computing demands and not by simple replacement of old PCs. The firm notes that current macro environment leaves the firm less sanguine than many on prospects here and considers market expansion a lower-probability scenario than the stock would suggest. The firm notes that INTC is seeing strong product cycles in both Nehalem for servers and Atom for mobility. However, a broad mix shift toward low-end, consumer-oriented markets will likely offset unit strength moving forward, while INTC's entry into the fiercely competitive CE space will likely pressure margins. The firm maintains their Sell rating and $16 tgt ahead of INTC's 3Q09 earnings on Oct, 12. -

Euroopa turud:

Saksamaa DAX -0.30%

Prantsusmaa CAC 40 -0.42%

Inglismaa FTSE 100 -0.23%

Hispaania IBEX 35 0.74%

Rootsi OMX 30 +0.51%

Venemaa MICEX +0.63%

Poola WIG +0.03%Aasia turud:

Jaapani Nikkei 225 +1.87%

Hong Kongi Hang Seng +0.03%

Hiina Shanghai A (kodumaine) +4.76%

Hiina Shanghai B (välismaine) +3.56%

Lõuna-Korea Kosdaq +1.88%

Tai Set 50 +0.52%

India Sensex 30 -1.19% -

Forget the 'Facts'

By Rev Shark

RealMoney.com Contributor

10/9/2009 8:53 AM EDT

The truth is more important than the facts.

-- Frank Lloyd Wright

Yesterday, in response to some questions posed by Doug Kass on The Edge, Anirvan Banerji and Don Dion set forth some bullish arguments in support of this very strong market. While I tend to share some of Doug's skepticism about the ability of this market to keep running, the very positive responses he received make me appreciate how there are always two sides to the market. There is never a time in the market when there aren't highly intelligent, logical and insightful arguments for either side.

At times we are often inclined to dismiss those with views opposing our own as lacking insight and intellectual rigor. We will be tempted to dismiss them as not having a clear understanding of what is really happening. "How can those bulls not see what is so painfully obvious to us bears?"

Of course those on the other side of the market will feel equally secure in their own beliefs. "This market is acting extremely well and is merely reflecting the many economic improvements to come. How can those foolish bearish not appreciate what is really happening out there?"

Back and forth we go, and there will never be a shortage of proponents for whatever market case you want to make. We can line up two full football teams of highly respected pundits for both sides to battle back and forth, and neither is ever going to convince the other. The battle will always end in a murky tie until the market monster takes control and settles the debate.

In the end there is no way to know which argument will win out, and even if you could know who will be proved right, you need to have the proper timing in order to really profit.

My point here is that we always have to guard against being overly committed to one side of the market. Establishing who is "right" is an impossible task. All we really can do is monitor the action and try to react to it as it unfolds. Predicting how the market will act based on macroeconomic arguments is impossible. What will drive us will be emotions and feelings. Arguments about fundamentals only matter when certain conditions exists. Facts are a deceptive thing that will mislead us greatly if we don't understand the prevailing psychology of the market.

So do the bulls or the bears have the better arguments about this market right now? I don't know. My bias is to be bearish, simply because my personal experience leads to me to believe that the economy is still in extremely poor shape and not improving much. On the other hand, the market is acting like that doesn't matter, and it would be arrogant of me to think I know more than the market. I'm left with no choice but to respect the bullish case here until the market says otherwise. If I want, I can find some folks to provide arguments to back up this price action, but the fact that the market is acting well is all the confirmation the bulls need at this point.

We have a little softness this morning, but there isn't much going on out there at the moment. Google (GOOG) has an upgrade, but I don't see much else.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: SCIL +52.9% (thinly traded, light volume), RBC +3.1% ... M&A news: PSTA +11.8% (agrees to be acquired by Pulmuone for $2.70 per share in cash)... Other news: THLD +19.8% (Presents interim data from a Phase 1/2 clinical trial of TH-302), SRZ +11.5% (announces it has entered into an agreement to sell 21 wholly owned assisted living communities), HEB +6.7% (still checking), HTZ +6.4% (Cramer makes positive comments on MadMoney), SVNT +3.8% (priced underwritten offering of 4,300,000 shares of its common stock at a price of $13.29 per share; also upgraded to Outperform at Oppenheimer), MPEL +3.5% (still checking), NOK +2.1% and ERIC +1.8% (checking for anything specific), ELGX +2.0% (comments on alleged patent infringement)... Analyst comments: NTAP +4.1% (Solid analyst day guidance, macro demand improving - Merriman; upgraded to Buy at ThinkEquity), SE +3.6% (upgraded to Conviction Buy from Neutral by Goldman Sachs - DJ), AKS +2.6% (upgraded to Buy at Deutsche), TS +2.4% (initiated with Buy at UBS), LSI +2.0% (upgraded to Equal Weight from Underweight at Barclays Capital), RIMM +1.1% (upgraded to Outperform at Baird).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: PCBK -7.3% (thinly traded, light volume), INFY -3.6%... Select metals/mining names showing weakness with dollar rebounding: GFI -2.7%, HMY -2.4%, BBL -2.3%, AU -2.2%, BHP -1.9%, GOLD -1.7%, KGC -1.5%, SLW -1.4%, AEM -1.4%, NEM -1.3%, AUY -1.2%, GDX -1.2%, VALE -1.1%, ABX -1.1%, GG -1.0%... Other news: SPPI -15.8% (receives complete response letter from FDA for FUSILEV in advanced metastatic colorectal cancer), ACOR -10.6% (announces posting of briefing documents for October 14 FDA Advisory Committee meeting on Fampridine-SR), LXRX -6.2% (priced a 33.33 mln share common stock offering at $1.50/share), HOGS -5.1% (announces common stock offering, made pursuant to an effective shelf registration), STXS -4.7% (Announces Public Offering of Common Stock of up to $25 mln), TTM -3.4% (raises $750 mln to pay Jaguar-Land Rover debt - DJ), LYG -2.6% and RBS -1.4% (Royal Bank of Scotland and Lloyds loan levels probed - FT)... Analyst comments: AKAM -3.2% (downgraded to Market Weight at Thomas Weisel), ARO -3.1% (cut to Sell from Neutral by Goldman Sachs - DJ), SVU -2.9% (downgraded to Equal Weight at Barclays), LTD -2.6% (downgraded to Sell from Hold at Soleil), EP -2.4% (cut to Neutral from Buy by Goldman Sachs - DJ), HOT -1.9% (downgraded to Hold at Soleil), POT -1.3% (initiated with Sell at Dahlman Rose), EPB -1.1% (cut to Buy from Conviction Buy by Goldman Sachs - DJ), MT -1.0% (downgraded to Hold at RBS), BMY -0.9% (downgraded to Neutral from Outperform at Cowen). -

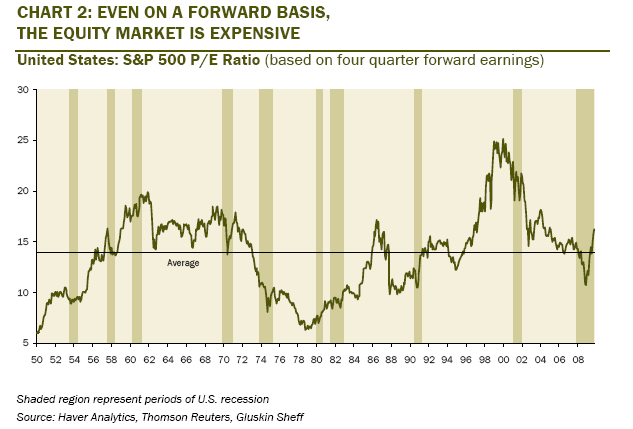

David Rosenberg, kes vähemalt üle päeva oma hommikustes turuülevaadetes kõrgele valuatsioonile tähelepanu juhib, võtab tänases raportis teema veelgi põhjalikumalt ette. Tabavalt on ta jõudnud järeldusele, et V-kujulises taastumises viitab täht „V“ P/E näitajate pretsedenditu tõusu tõttu valuatsioonile.

Kaks lõiku ettevaatava P/E teemal:

Bullish analysts like to dismiss the actual earnings because they are “depressed” and include too many writeoffs, which, of course, will never occur again. Fine, on a one-year forward (operating) earning estimates, the P/E ratio is now 16.2x, the highest it has been in nearly five years. During the last cycle, at the peak of the S&P 500 — October 2007 — the forward P/E was 14.3x and the highest it ever got was 15.4x. So hello? In just six short months, we have managed to take the multiple above the peak of the last cycle when the economic expansion was five years old, not five weeks old (and we may be a tad charitable on that assessment). It is hard to believe, but the S&P 500 is actually trading at peak multiples.

Now, about forward multiples. The consensus is usually overly-optimistic, which is why so many analysts love to do their analysis on “forward” earnings since the market almost always looks “attractively priced” on that basis. The reality is that the forward P/E multiple is now at 16.2x after bottoming at 11.7x at the market lows. The multiple has not been this high since February 2005 when the economic expansion was already nearly four-years old! Today’s stock market, on this basis, is now being priced as if we are late in the cycle — forget this mid-cycle valuation stuff.