Börsipäev 4. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Kogu päeva külgsuunas triivinud USA indekseid tabas viimasel tunnil tugevam müügisurve peamiselt energia-, finants- ja materjalide sektoris ning S&P500 sulgus kokkuvõttes -0.8% madalamal. Aasias on täna hommikul kaubeldud ilma domineeriva suunata.

Selle nädala kõige oodatum makrouudis saabub Eesti aja järgi kell 15.30, milleks on novembrikuu tööjõuturu raport. Oktoobri numbrite osas pani konsensus tugevasti mööda, kui 0.1 protsendipunktise vähenemise asemel kerkis tööpuudus USA-s 0.4 protsendipunkti 10.2%ni - kõrgeim tase alates 1983. aastast. Seekord usutakse, et töötusemäär jääb samale tasemele püsima, kui töökohtasid kadus läinud kuul 125 000. Tegemist oleks järjekorras 23. kuuga, mil töökohtade arv vöhenes – pikim kaotuse seeria alates 1930-ndatest.

-

Goldman Sachs on väljas 2010. aasta tooraineturu väljavaatega, mida on võimalik täies mahus lugeda ZeroHedge vahendusel. Analüüsimaja arvates domineerivad edaspidi turgusid kolm väljakasvavat trendi:

- Differentiation between commodities driven by the extent of supply constraints that will likely drive greater price dispersion across the commodity complex;

- Resource realignment as emerging markets are forced to bid away scarce commodities from the developed economies, especially when supply constraints are more restrictive, which shifts the focus away from the sustainability of higher prices and towards the sustainability of higher growth;

- Increasing macroeconomic correlations as resource realignment will likely increase the relevance of commodity prices and supply to the broader macroeconomic environment.

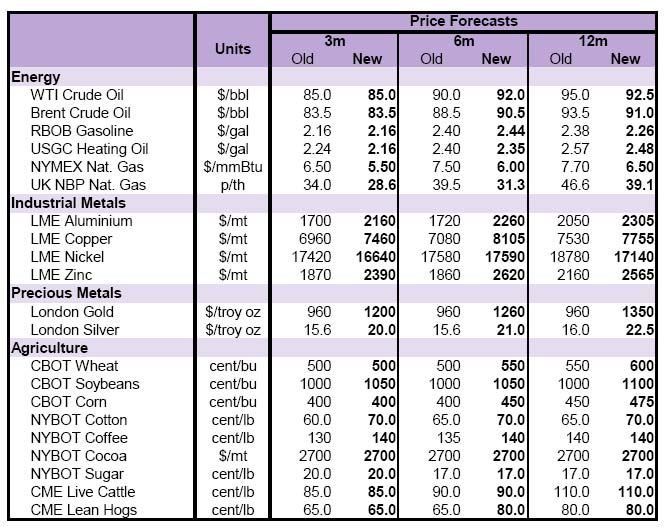

Kokkuvõttev tabel 2010.a hinnaprognoosidest:

-

USA futuurid kauplemas hetkel 0.1% plussis ning ilmselt loodetakse kuulda konsensusest väiksemat töökohtade kadu tänu viimaste nädalate töötuabiraha taotlejate arvu kahanemisele. Euroopa turgudel on enne raportit meeleolu seevastu kergelt negatiivne. 125 000-st konsensust hindavad liialt pessimistlikuks ka mitmed analüüsimajad:

Morgan Stanley -75K

BNP Paribas -130K

JP Morgan -100K

Credit Suisse -50K

Goldman Sachs -100K

Deutsche Bank -90K

Bank of America -125K

HSBC Markets -140K

Saxo -139K -

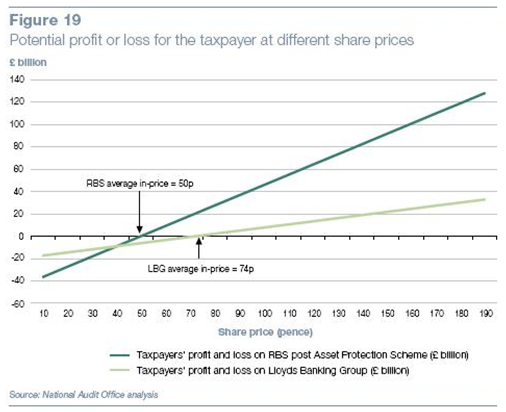

Briti National Audit Office’i tänase raporti põhjal on Briti pankade päästmiseks kulutatud £850 miljardit naela (võrdluseks UK 2008 SKP oli 2660 miljardit dollarit).

NAO andmetel on maksumaksjad RBSi ja Lloyds Banking Groupi päästmisest saanud 18 miljardit naela kahjumit (27.11.2009 aktsia hindadega). Hea uudis on see, et kui RBSi ja Lloydsi aktsia tõusevad 10 senti, siis maksumaksjad saavad vastavalt 9 miljardit naela ja 3 miljardit naela lisa aktsiate müügist. Väga karm, kuidas kõik britid sõltuvad kahe aktsia käekäigust!

Funny how we’re all in it together now, eh? (loe pikemalt siit)

-

Makro väga hea:

November Nonfarm Payrolls -11K vs -125K consensus, October revised to -111K from -190K

November Average Hourly Earnings M/M +0.1% vs +0.2% consensus, prior +0.3%

November Unemployment Rate 10.0% vs. 10.2% consensus; prior 10.2%

November Average Weekly Hours 33.2 vs 33.1 consensus, prior 33.0

-

CORRECTION-- September nonfarm payroll revised to -139K from -219K

October was revised from -190,000 to -111,000.

-

Ehk siis pole mitte kellelgi mitte mingit mõtet uskuda seda muinasjuttu, mida USA statamet ajab.

PS Ausalt hindan vaikselt kasvõi Vene statameti sõnu rohkem, kui USA oma. -

EUR/USD tugeva tööjõuraporti peale 1.5'st allapoole kukkunud. Oodatakse intressimäärade tõusu?

-

Eur/usd viinud omakorda kulla tagasi alla 1200

-

Rev Shark: The Trend Is Your Friend ... Until It's Not

12/04/2009 8:11 AM

You may be deceived if you trust too much, but you will live in torment if you don't trust enough.

-- Frank CraneAs the year winds down, market players are wondering whether they can trust this market to keep on running. We have been going almost straight up since March, and now we are in the seasonally strongest time of the year, with many money managers trying to gain some relative performance. Is now the time to start worrying about the health of the market and to start anticipating a pullback?

What has been so remarkable is that despite the gloom of high unemployment and the tepid economic recovery on Main Street, the stock market just keeps on chugging higher. So many market players think it is just a matter of time before the market returns to reality and starts to struggle.

The bears have been underestimating how powerful the forces of 0% interest rates and high liquidity are. It is impossible to generate yield on idle cash, and all that money from bailouts and stimulus has to go somewhere ... so what better place than the stock markets?

It is very easy to underestimate those forces, especially since they are unaffected by all the fundamental bearish arguments. As long as stocks continue to act well, all the talk about the problems we will surely face down the road is irrelevant.

I've always tried not to over-anticipate a change in trend. The biggest mistake that many investors make is that they start anticipating that the market will change direction way too early. We always think the market is going to share our opinion of what is reasonable and will stop moving in just one direction, but the market often goes further than we think is reasonable or realistic.

While we should always give the benefit of doubt to the prevailing trend, that doesn't mean we should be oblivious to warning signs. In my trading, the foremost warning sign that I pay attention to is the condition of individual stock charts. If I'm not finding charts I like, then I automatically become more cautious, because I put less money to work. If the market is narrow like this one has been, there will automatically be fewer stocks to choose from. That forces me to be more cautious even when the indices are still in pretty good technical shape.

Other things like weakness in financials and underperformance of small-caps will also automatically force you to be more cautious because the charts simply won't be very inviting.

A lot of folks have been having great difficulty trusting this market all year, and that is going to continue to be the case for a long time. But as we've seen, that doesn't mean the market can't keep on running. The important thing is to let the charts be your guide -- when more and more individual stocks look poor, the more cautious we will be. That might not get you out at the precise top in the market, but you will more likely avoid being too cautious too early.

We have the jobs report coming up at 8:30 a.m. EST, which is going to set the tone for today. Bank of America (BAC - commentary - Trade Now) priced its secondary offering at $15 and it is trading up from there about 30 cents. It isn't a great response, but the deal is done and we'll have to watch to see if BAC continues to hold that pricing.

I'm a bit concerned about this market because of how narrow it has been lately. I still see some good trading in some small areas like China, but the reaction to the jobs news today is going to tell us some important things about this market.

No positions.

-

Ludicrous Forecast!

12/4/2009 8:50 AM EST

Gun to my head, we have seen the highs for the day.

Doug Kass -

Euroopa on tööjõuturu statistika peale roninud -0.5%-lisest miinusest välja ning S&P500 futuur indikeerib avanemist +1.12% kõrgemal

Euroopa turud:

Saksamaa DAX +0,87%

Prantsusmaa CAC 40 +1,14%

Inglismaa FTSE 100 +0,60%

Hispaania IBEX 35 +0,75%

Rootsi OMX 30 +1,20%

Venemaa MICEX +1,72%

Poola WIG +0,54%Aasia turud:

Jaapani Nikkei 225 +0,45%

Hongkongi Hang Seng -0,25%

Hiina Shanghai A (kodumaine) +1,62%

Hiina Shanghai B (välismaine) -0,49%

Lõuna-Korea Kosdaq +0,65%

Tai Set 50 -0,91%

India Sensex 30 -0,49% -

Gapping down in reaction to disappointing earnings/guidance: TTWO -31.8% (also downgraded to Market Perform from Outperform at Wells Fargo, downgraded to Sell from Buy at Kaufman Bros, downgraded to Hold at Brean Murray, downgraded to Neutral from Buy at MKM Partners), SWHC -12.7% (also downgraded to Neutral at Merriman, target lowered to $7.50 at Northland Securities, downgraded to Neutral from Outperform at Cowen), VSNT -12.3%, MENT -7.7%, SIRO -3.7%, NOVL -3.5%, DMND -3.2%... Select gold names showing weakness with strength in the dollar: IAG -3.5%, ABX -2.8% (says Appeals court remands decision to District Court on Cortez Hills project ), GDX -2.6%, KGC -2.3%, AUY -2.2%, GG -2.1%, EGO -2.0%, GLD -1.8%, AU -1.3%, GFI -1.1%... Other news: ZIOP -9.8% (announces commencement of public offering), GSS -7.6% (files preliminary prospectus; expects to raise gross proceeds of approximately $75 million), ICLR -6.1% (receives warning letter from FDA relating to two studies), REG -5.2% (announces equity offering will not have an impact on FY2010 guidance from yesterday), WES -5.1% (announces public offering of 6 mln common units), NBG -3.3% (still checking), DD -2.5% (updates its commercialization timelines for Optimum GAT corn and soybeans; reaffirms outlook for greater than 15% compounded annual earnings growth of Agriculture & Nutrition business segment through 2013), NRGP -1.4% (files $300 mln common units shelf offering in an S-3), BAC -0.6% (confirms pricing of common equivalent securities at $15)... Analyst comments: ENDP -4.5% (downgraded to Mkt Perform at Wells Fargo).

Gapping up in reaction to strong earnings/guidance: BIG +13.0%, LAVA +7.3%, MRVL +6.5%, AVGO +2.0%... Select financials trading higher: HBAN +4.1%, RF +3.3%, BCS +2.9%, RBS +2.8%, GNW +2.5%, COF +2.4%, BBV +2.3%, STD +1.7%, MS +1.7%, DB +1.2%... Select metals/mining names showing strength: RTP +2.3%, MT +2.2%, GOLD +1.3%, HMY +1.2%... Select oil/gas related names showing strength: PBR +1.8%, BP +1.7%, SLB +1.6%, E +1.6%, RDS.A +1.2%, TOT +1.0%... Select casino names trading higher: LVS +4.2%, MGM +3.2%, WYNN +2.3%... Select European drug names seeing early strength: AZN +3.3% (announces US FDA approves SEROQUEL XR for add-on treatment of major depressive disorder), SHPGY +2.1%, SNY +2.1%, GSK +2.0%... Other news: DEER +6.7% (light volume; signs $29.3 mln distribution agreement with the second largest consumer electronics retailer in China for 2010 product delivery), JAVA +6.3% (Oracle proposes to create separate entity that house's JAVA's MySQL database - NYPost), LDK +5.0% (LDK Solar, Q-Cells reach deal to continue solar wafer supply contract - DJ), SOLF +5.0% (signs agreement to build 100MW solar power plant in Jiayuguan City, Gansu Province), MANT +2.3%, OSK +1.8% and HRS +1.2% (Cramer makes positive comments on MadMoney)... Analyst comments: SNV +6.7% (upgraded to Mkt Perform at FBR), ADCT +3.3% (upgraded to Buy at Argus), AKAM +2.7% (upgraded to Buy from Hold at Citigroup), JNPR +2.2% (added to Conviction Buy from Buy at Goldman - Reuters), SNDK +1.9% (initiated with an Outperform at JMP Securities), BCS +1.3% (upgraded to Neutral at JPMorgan), FSLR +1.1% (upgraded to Buy at Collins Stewart), V +0.9% (initiated with an Outperform at Oppenheimer).

-

October Factory Orders +0.6% vs 0.0% consensus, prior revised to +1.6% from +0.9%