Börsipäev 18. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Tänaseks suuremaid majandusuudiseid USA erinevad ametid planeerinud ei ole. Tähtsaimaks sündmuseks võib pidada USA presidendi Barack Obama osavõttu Kopenhaageni kliimakõnelustest. Samuti tuletan meelde, et täna on detsembrikuu kolmas reede ehk siis optsioonireede, mil enamus aktsiaoptsioone lõppevad.

Eelturul on USA indeksite futuurid ca 0.2%-0.3% plusspoolel. -

Euroopas aga pälvib suuremat tähelepanu detsembrikuu IFO indeks (kell 11.00), mis peegeldab Saksamaa ettevõtete hinnangut riigi praegusele ja tuleviku majanduskliimale. Konsensus ootab kerget paranemist mõlemal rindel võrreldes novembrikuuga.

-

Intressimäärade tõstmist ei pea tingimata kartma, pigem vastupidi:

One day, quite possibly by the middle of next year, the US Federal Reserve will raise interest rates. It’s probably going to happen. Get over it. It could even be seen as a good thing. Because it will signal the Fed is convinced the economy is sufficiently robust to take the hit. And yet the perception among market players is that as soon as Mr Bernanke signals a tightening is round the corner, equities will plunge and bond yields soar. Sure, the yield curve will likely flatten from its current steep gradient as short term paper reflects a tighter monetary stance. But believing that equities will suddenly drop on the basis that something long-expected has finally come to pass does not show a very sharp understanding of the markets propensity to confound. Also, the idea is based on the reckoning that it is mainly ultra-loose monetary policy that is providing support to stocks (with a little help from a soft dollar boosting commodities and thereby resource companies). Apart from the fact that’s not a great advert for the market’s role as an efficient conduit for the allocation of capital, it misses the crucial point. What investors should be really concerned about is if the Fed doesn’t feel able to raise rates soonish. That would suggest equity investors have priced in a much rosier economic scenario than will prove to be the case. (Financial Times)

-

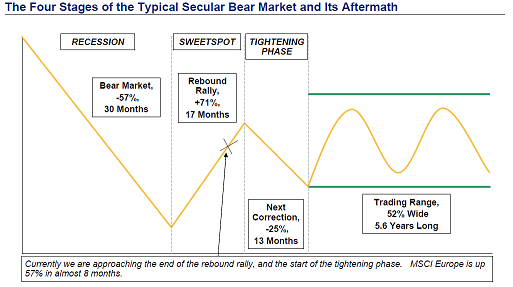

Lisaks veel eelmisele kommentaarile ühe Morgan Stanley graafiku, kus on hästi näha, et kui algab tightening phase, siis oodatakse ka suurema korrektsiooni algust, mis kestab ca aasta:

Kuna keskpangad pole viimastel kohtumistel retoorikat muutnud, siis peaksime praegu oleme jätkuvalt arbuusisuhkrus (selline nägemus väga paljudel hetkel).

-

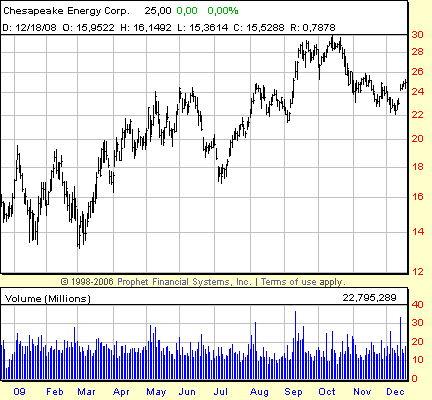

Jim Cramer pushis oma eilses MadMoney saates maagaasisektori ühe lipulaeva Chesapeake Energy (CHK) aktsiaid, öeldes, et nüüd kus Exxon Mobil (XOM) on XTO Energy (XTO) ülevõtuga kindlustanud endale suured maagaasireservid juhuks, kui üha enam masinaid peaks tavakütuse pealt üle minema maagaasi peale, tuleb ka Exxon Mobili konkurentidel nagu British Petroleum (BP), ConocoPhillips (COP) ja Chevron (CVX) selle peale üha tõsisemalt mõtlema hakata. Põhimõtteliselt on kõik kolm täiesti reaalsed kandidaadid, kes võiksid aja jooksul Chesapeake Energy (CHK) üle osta.

Chesapeake Energy (CHK) aktsiad meile meeldivad ja näeksime neid hea meelega ühe osana investori portfellist.

-

Economistis lühike & väga hea ülevaade maailmamajandusest. Praegust olukorda nimetatakse "suureks stabiliseerumiseks" & kriisist taastumise lõppvaatus seisab alles ees. Artiklis üks tähelepanek võlakoormuse vähendamise kohta:

For all the talk of deleveraging, American households’ debt, relative to their income, is only slightly below its peak and some 30% above its level a decade ago. British and Spanish households have adjusted even less, so the odds of prolonged weakness in private spending are even greater. And as their public-debt burden rises, rich-world governments will find it increasingly difficult to borrow still more to compensate.

-

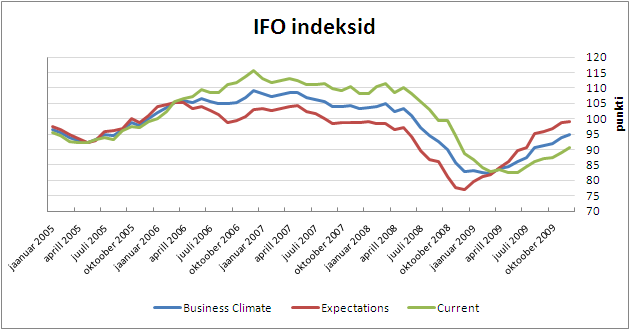

Saksa ettevõtete arvamus riigi majandusolukorrast jätkab paranemist, seda nii jooksva seisu kui ka tuleviku osas. Ärikliimat mõõtev indeks kerkis novembri 93.9 punktilt 94.7 punktile (Bloombergi konsensus 94.5), jooksvat hinnangut mõõtev indeks paranes 89.1 punktilt 90.5 punktile (konsensus 90.0) ja ootuste indeks 98.9 punktilt 99.1 punktile (konsensus 99.0).

Laias laastus konsensuse prognoosidele vastanud numbrid on jätnud turud võrdlemisi külmaks ning DAX jätkab pärast hommikust pooleprotsendilist hüpet külgsuunas triivimist.

-

Dr. Doom toob välja vahelduseks ka midagi positiivset, kuid seda muidugi endale omaselt:

“I’m positive on Brazil, but not as euphoric,” Roubini said. (loe pikemalt Bloombergist)

Analüütikud prognoosivad järgmisel aastal Brasiiliale 5% majanduskasvu ja riigis on valitsuse stiimulid üsna väiksed, mistõttu tundub see üks tugevaim arenguriik. Rahandusministeeriumi sõnul on stiimulid 1-1.5% SKPst vs näiteks Hiinas ca 13% SKPst. Kuna Brasiilia on suur toorainete eksportija, siis tasub sinna investeerida eeldusel, et nõudlus nafta, metallide jms järele paraneb. USA kaudu on võimalik Brasiiliasse investeerida nt läbi börsil kaubeldava fondi EWZ:

-

Hiina aktsiaturud täna teist päeva järjest üle 2% miinuses.

Euroopa turud:

Saksamaa DAX +0,65%

Prantsusmaa CAC 40 -0,04%

Inglismaa FTSE 100 +0,33%

Hispaania IBEX 35 +0,18%

Rootsi OMX 30 -0,18%

Venemaa MICEX +1,00%

Poola WIG +0,09%Aasia turud:

Jaapani Nikkei 225 -0,21%

Hongkongi Hang Seng -0,80%

Hiina Shanghai A (kodumaine) -2,05%

Hiina Shanghai B (välismaine) -2,87%

Lõuna-Korea Kosdaq +0,72%

Tai Set 50 -0,06%

India Sensex 30 -1,03% -

Up for Grabs

By Rev Shark

RealMoney.com Contributor

12/18/2009 8:33 AM EST

In every battle there comes a time when both sides consider themselves beaten, then he who continues the attack wins.

-- Ulysses S. Grant

On Thursday the bears finally managed to put some points on the scoreboard, but it was relatively mild and orderly selling. There were a number of negatives, including poor demand for the Citigroup (C) secondary offering, worse-than-expected weekly unemployment claims, poor earnings and guidance from FedEx (FDX) and a stronger dollar.

That is a pretty good lineup of negatives, but all the bears managed to do was push the indices back down into the middle of the recent trading range. There was no real panic-selling or any strong momentum to the downside.

The bears are in pretty good shape to press their slight advantage after the poor action on Thursday, but we saw strong earnings reports after the close from Research In Motion (RIMM) , Nike (NKE) and Oracle (ORCL) , and financials are trying to stabilize after digesting $53 billion in secondary offerings. If these positives persist, then the advantage is going to shift back to the bulls and leave the market in the middle of its recent trading range.

The problem this market has had lately is that there haven't been any strong trends or emotions. I was hopeful yesterday that the bears might press a bit and shake things up, but they just didn't seem to have much conviction, either.

We have had little leadership lately and few strong themes. We did see gold fall sharply as the dollar rallied, and banks have clearly been out of favor, but as far as the upside goes, the strength has been very random with a few big-cap names perking up here and there but no really dominant pockets of momentum.

It is going to be interesting to see if the strength in RIMM and ORCL might spark some love for the big-caps into the end of the year. If we are going to run a bit over the next two weeks, the most logical leaders are going to be Google (GOOG) , Apple (AAPL) , Amazon (AMZN) , RIMM, Priceline (PCLN) and other higher-beta big-cap names.

Both bulls and bears have had a chance to take control of this market recently, but it is still up for grabs. It is the bulls' turn again this morning, and I'm just rooting for some conviction so we can get a little trend working. It has been a very dull market lately, and if we don't have some better action soon, market players are going to lock in gains and sit on the sidelines while they enjoy the holidays.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: SMOD +12.4%, RIMM +11.0% (also upgraded to Hold at Deutsche, initiated with Hold at Standpoint), DEER +9.4%, KMX +8.6%, TTWO +6.8% (also upgraded to Hold at Kaufman, upgraded to Buy from Neutral at Sterne Agee), ORCL +4.2%, NKE +2.1%, APSG +1.0%... M&A news: JAV +13.8% (to be acquired by Myriad Pharmaceuticals)... Select financials trading higher: MFG +2.0%, STT +1.9% (upgraded to Outperform at Keefe Bruyette), GNW +1.7% (Northland Securities believes investors have a very cheap entry point with a visible path to $15.75, and with continued ROE growth, the stock could be worth $25-$30/share), STD +1.4%, BAC +1.1%, CS +1.0%... Select oil/gas related names showing strength: HES +2.8% (initiated with Buy at BofA/Merrill), BP +2.2% (raised to Buy from Neutral at Goldman- DJ), RIG +1.9%, CHK +1.8% (Cramer makes positive comments on MadMoney), RDS.A +1.7%, WFT +1.5%, APA +1.5% (initiated with Buy at BofA/Merrill), APC +1.2% (initiated with Buy at BofA/Merrill), STO +1.2%... Select metals/mining names showing early strength: GOLD +4.9%, RTP +2.2%, BHP +1.9%, BBL +1.8%, AUY +1.4%, GFI +1.3%... Other news: SENO +21.3% (announces that a jury delivered a verdict in favor of SenoRx in a lawsuit brought by Hologic), CRME +13.8% (announces investigational candidate, vernakalant, meets primary endpoint in European Comparator study), CELG +5.8% (Initial data from CALGB-Led study of treatment with continuous REVLIMID in patients with multiple myeloma following autologous stem cell transplant reported),RYAAY +4.0% (Ryanair ends talks with Boeing on 737 order - WSJ), SNY +2.9% (still checking), NOK +1.0% (up in sympathy with RIMM)... Analyst comments: ALTI +7.4% (initiated with Overweight at Weisel), DAN +2.7% (upgraded to Overweight at JPMorgan), EMC +2.5% (added to Conviction Buy list at Goldman- Reuters), ETFC +2.5% (resumed with a Buy at BofA/Merrill), STRI +2.4% (initiated with Outperform at Macquarie).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: AIQ -10.1%, PALM -6.1%, BCR -4.9% (also downgraded to Underweight at Piper, downgraded to Mkt Perform from Outperform at William Blair), ACN -1.3%, DRI -1.1%... M&A news: MYRX -3.2% (JAV to be acquired by Myriad Pharmaceuticals)... Other news: LDK -9.8% (hearing early weakness attributed to prcing of offering), KOG -8.4% (announces preliminary 2010 capex budget of $60 mln), ZLC -7.9% (WSJ reports the co canceled some orders with suppliers as it struggles under the weight of mounting debt and sales declines), CATY -4.5% (agreed to submit to the FRB for review and approval a plan to maintain sufficient capital ), SID -4.2% (confirms proposal for acquisition of Cimpor), LYG -2.4% (Lloyds chief sleeps easy as challenges loom - FT), PBR -1.2% (units get $809 mln loans from Brazil - Reuters.com)... Analyst comments: PLD -2.2% (downgraded to Sell from Neutral at UBS), NTAP -1.9% (cut to Neutral at Goldman; removed from Conviction Buy list- Reuters), CAL -1.4% (downgraded to Hold from Buy at Stifel Nicolaus), CTXS -1.0% (downgraded to Sell at MKM Partners). -

Wells Fargo (WFC) ja Citigroup (C) on turule toomas hulgaliselt uusi aktsiaid. Et säilitada ettevõtete senine mõju S&P500 indeksis, peavad indekseid jälgivad fondid Doug Kassi sõnul ostma tänase päeva lõpuks ca 45 miljonit Wells Fargo (WFC) aktsiat ja ca 650 miljonit Citigroupi (C) aktsiat.

Sellised indeksi reweighting'ud on tavapärased ja korrapärased nähtused ja üldiselt ei ole neile väga palju tähelepanu vaja pöörata (kui just mõni väike ettevõte esmakordselt nt Russell 2000 või 3000 indeksisse ei saa, mis toob kaasa reeglina korraliku liikumise aktsiahinnas), kuid sedapuhku tasuks kauplejatel WFC'l ja ehk eelkõige just C'l silma korralikult peal hoida, kuna kogused on märkimisväärsed.

-

Venemaalt jätkuvalt kehvad numbrid ja hoolimata poliitikute lubadustest & kõrgemast nafta hinnast ei suudeta stagnatsioonist lahti saada - novemrbis tõusis ametlik töötusemäär 8.1% peale oktoobri 7.7% juurest. Jaemüük kukkus1.3% mom (pikemalt siin) . MICEX on aga 0.7% plusspoolel, kuna nafta on täna 2.3% tõusnud ja kaupleb taas 74 dollarist kõrgemal.

-

Kui Kopenhaagenis toimuval kliimakonverentsil peaks mingi konkreetsem kokkulepe (raamistik tegutsemiseks) tulema CO2 osas, siis võib fookusesse sattuda ka NOxi vähendamine. Üks ettevõte, kes tegeleb NOx-i vähendamisega on Fuel Tecki (FTEK), mida oleme tutvustanud pikemalt Pro all. USAs on lubatud küll NOx-i vähendada, kuid kuna midagi konkreetset pole vastu võetud, siis FTEK pole eriti uusi tellimusi saanud ja kaupleb märtsi põhjade juures (ilmselt ootavad saastajad konkreetseid kvoote & ei soovi enne kapitaliinvesteeringuid teha). NOx-i regulatsioonidel tasub silm peal hoida & kui midagi konkreetsemat peaks sealt tulema, siis on FTEKil kindlasti korralikult tõusuruumi.

-

Eile sai juhitud tähelepanu EEM 40 strike puttide ostuhuvile, siis täna kaubeldakse vaevu strike peal.

-

kas keegi oskab SMOD-i liikumist täna kommenteerida. kas tasub veel hoida?

-

Tehnoloogia (vedur) ja energia on sektorid, mis hetkel turgu hoiavad, kuid viimane neist samuti juba üsna pajlu järgi andnud. Vana majandus vs teh. , kui teh. siit järgi annab siis tuleb turg tõenäoliselt üsna hooga alla. Hetkel veel vedur hoos.

-

Financial Select Sector SPDR (XLF) attempting to hold/lift off support at its three month close low/200 day ema at 14.01/13.93 -- session low 14.01

-

Bank of America CEO Moynihan on CNBC says co has to resume earnings money before restarting dividends; says he hasn't thought about the dividend of 2010 yet

Ja BAC rallib ülespoole:) -

S&P affirms Ireland 'AA/A-1+' ratings; outlook still negative

-

Kellel huvi võib CME graafikut vaadata, kus ligi 2 tundi on aktsiat hoitud 0.5 punktises vahemikus. Ilmekas pilt opt reede mängudest.

-

Iraq National Security Council says Iran violated Iraqi border - Bloomberg

-

Tundub, et hommikul väljakäidud mõtted WFC ja C reweightingu positiivsest mõjust on sedapuhku paika pidanud. Aga muidu üpriski igav optsioonireede päev, kus enamus suuremaid nimesid üritatakse tähtsamate strike'ide juurde sulguma panna.