Börsipäev 30. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

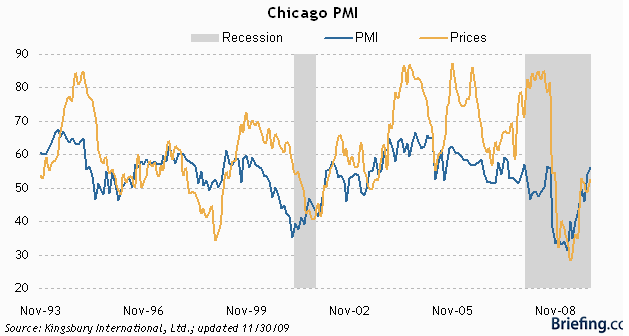

Täna kell 16.45 avaldatakse detsembrikuu Chicago PMI näitaja, mis heidab valgust tööstustoodangu võimalikele muutustele USAs. Ootuseks on 55.1 punkti. Mida suurem näitaja, seda agressiivsemat taastumist näeme ning mida väiksem näitaja, seda leebemat.

Graafik Briefingu vahendusel ka siia:

-

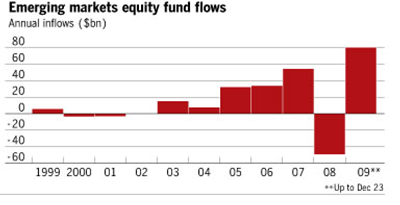

Hetkel on konsensus kindlal arvamusel, et maailmamajanduse kasvumootoriks pärast kriisi on arenguriigid - kõrged ootused kajastuvad ka arenguriikide aktsiates, kuhu on sellel aastal liikunud rekordiline rahasumma (loe pikemalt siit):

-

Arenevatest turgudest omakorda eelistavad fondijuhid järgmisel aastal enim Venemaad (valuatsioon on võrreldes teistega odavam):

Russia is the leading “overweight” holding among the world’s largest developing-nation mutual funds, EPFR Global data show. More than 95 percent of analyst ratings on Russian stocks are “buy” or “hold,” the highest level since Bloomberg began tracking the data in 1997. Goldman Sachs Group Inc. says Russia is the most attractive emerging market for 2010 and Troika Dialog, the nation’s oldest investment bank, predicts equities will climb about 40 percent. (link siin).

-

Selle 95% juures tuleb muidugi arvestada sellega, et neid ettevõtteid katavad enamjaolt analüütikud, kes otsivad ostuvõimalusi välisturgudel. Ettevõtted, mis ei ole atraktiivsed ning vääriksid müü-soovitust, jäetakse lihtsalt katmata.

-

Mõned superkarud ka turule ikka jäänud. Hedge-fondi juht E. Sprott, kes on viimase üheksa aastaga oma investeeringute väärtust 496% tõstnud, ootab jätkuvalt uusi põhjasid:

The Toronto-based money manager, whose Sprott Hedge Fund returned about 496 percent in the past nine years as the S&P 500 lost 32 percent in Canadian dollar terms, said the index’s 66 percent rally since March 9 reflects investors misinterpreting economic data. He’s predicting the gauge will fall 40 percent to below 676.53, the 12-year low reached on March 9. (link)

-

Üle mitme-mitme päeva näha turgudel pisut närvilisemat liikumist. Euroopa turud ca -0.6% ning USA futuurid hetkel -0.5%.

-

Kes TA'st ja Fibonaccist lugu peab, siis võib oodata, et S&P500 tõuseb 2010. aasta jooksul 1226 punkti peale. Iroonilisel kombel on see ka 12 suurema analüüsimaja S&P500 indeksi keskmine aastalõpuprognoos - link Bloombergi loole siin.

-

90-ndate retsessiooni ajal õnnestus Hispaania pankadel maksejõuetutelt klientidelt kinnisvara akumuleerides ning hiljem majanduse taastudes aktsepteeritavatel hinnatasemetel müües hoida turul ära järsemat hinnalangust ning vältida mahukaid mahakirjutamisi bilansis. Siiani on see strateegia töötanud ka praeguse kriisi ajal, kui majade hinnad on viimase 12 kuuga alanenud vaid 9%. WSJ kirjutab eilses artiklis, et edasi läheb Hispaania finantsasutustel elu raskemaks, kuna likviidsusvajadus ja keskpanga karmimad tagatisereeglid sunnivad kinnisvarast lahti ütlema. Väheaktiivne turg võib aga paljastada vara tegeliku väärtuse bilansis ning tuua 2010. aasta esimesel poolel finantssektorile suuri kahjumeid. Seda eriti väiksemate säästupankade osas, kelle kuulub 70% finantsinstitutsioonide 30 miljardi euro suurusest kinnisvaraportfellist.

-

USA indeksite futuurid indikeerivad avanemist -0,3% madalamal

Euroopa turud:

Saksamaa DAX -0,9%

Prantsusmaa CAC 40 -0,46%

Inglismaa FTSE 100 -0,32%

Hispaania IBEX 35 -0,72%

Rootsi OMX 30 -0,77%

Venemaa MICEX -0.55%

Poola WIG -0,56%Aasia turud:

Jaapani Nikkei 225 -0,86%

Hongkongi Hang Seng -0,01%

Hiina Shanghai A (kodumaine) +1,59%

Hiina Shanghai B (välismaine) +0,08%

Lõuna-Korea Kosdaq +1,57%

Tai Set 50 -1,18%

India Sensex 30 -0,33% -

Rev Shark: Closing the Year

12/30/2009 8:52 AMBy three methods we may learn wisdom: First, by reflection, which is noblest; second, by imitation, which is easiest; and third by experience, which is the bitterest.

-- ConfuciusWith only two days of trading left in 2009, the market is at a very interesting juncture. We've been enjoying a good old-fashioned Santa Claus rally over the last seven days, but that has left us technically extended on very light volume.

When the market goes up on light volume, it is much more vulnerable to a sharp pullback because there is less underlying support. When the folks who have racked up some recent profits try to protect them, there aren't going to be a lot of buyers rushing in to snap up their shares. It is a very thin market, and a lot of folks just aren't interested in being involved at this point.

The end-of-the-year pressures that can easily keep stocks elevated are making trading particularly difficult. Many market players want to delay profits until next year, and shorts may want to cover and take losses this year. We also have window-dressing pressure caused by money managers who want to make sure they finish the year strongly so they can collect as many fees as possible. When you throw in the fact that we have the lightest volume of the year, it makes for very random and whippy trading.

Extended markets on light volume have been the norm this year, which has made this one of the more difficult markets for those who don't just buy and hold. Since the bottom in March, this market has consistently made V-shaped moves and has stayed extended far longer than many people felt was reasonable.

When the bounce started back in March, the conventional thinking was that we were just going to experience a good bear-market bounce that would be sharp but wouldn't last too long, but we kept going and going and soon the belief with that we were in a bull market.

Many folks still believe that all we've had this year is a very big bear-market bounce. I think the bounce has been too big and too strong to be dismissed as just a countertrend rally, but assigning labels is not always a good idea, as it can blind you to what is really happening and make you less flexible.

It has been a truly remarkable year, far better than the vast majority thought it would be, especially when we were in the depths of gloom back in March. The problem with the market is that it always seems to go too far in either direction; the main challenge in 2010 is going to be trying to figure out how much upside we have left.

That is business for next week. Right now we need to focus on the fact that this extended market is showing some weakness this morning. Is this going to trigger some profit-taking for those who want to finish the year on a high note, or will window dressing and performance anxiety give us some underlying bids that hold us aloft? As I've discussed, I've hedged a bit and am looking for some selling before the closing bell tomorrow.

-

Gapping down:

Select European financials showing weakness: DB -3.6%, IRE -3.1%, AIB -2.7%, RBS -2.2% (Icelandic bank Glitnir 'owes Royal Bank of Scotland 500 mln pounds' - UK DailyMail), BCS -1.9%, ING -1.7%... Select metals/mining names trading lower: TIE -3.1%, CENX -2.6%, MT -2.3%, HL -2.2%, AKS -1.6%, RTP -1.4%, X -1.4%, NUE -1.2%... Other news: CBAK -21.4% (CFO said company hasn't won any orders from Google - Bloomberg.com), CAF -11.9% (trading ex dividend), TSRA -10.0% (ITC issues notice of final determination in Tessera's DRAM action), TRMA -9.1% (amends credit facility; provides preliminary outlook on Q4 2009), CIEN -3.9% (receives Investment Canada Act approval of proposed acquisition of Nortel's optical and carrier ethernet assets).

Gapping up

Select security/scanner related names showing continued strength: OSIS +3.8% (CNBC commentators discuss OSIS as play on report of body scanners at airports), LLL +2.4% (may benefit from any requirement that airports get more security equipment - Bloomberg.com), ASEI +1.2%... Other news: KFRC +11.6% (KGS suspension terminated by Department of Interior), CGEN +3.9% (raises gross proceeds of $20 mln through sale of ordinary shares), HIT +3.5% (traded higher overseas; ended 2009 on a high, following two separate news reports - Xinhua News Agency), OSK +2.6% (was awarded on Dec. 22, 2009, a $258,364,288 firm-fixed-price contract for the purchase of 728 new M1075 trucks; Co also announces additional contracts - DoD)... Analyst comments: NVDA +1.6% (upgraded to Buy at Kaufman), MRVL +0.9% (upgraded to Buy at Kaufman).

-

December Chicago PMI 60.0 vs 55.1 consensus, prior 56.1

-

Area around NASDAQ being cordoned off because of suspicious van in area - CNBC

-

Nasdaq evacuation cancelled - Fox Business

-

$32 bln, 7-year Note Auction: Yield 3.345% (3.372% expected); Bid/Cover: 2.72x (Prior 2.76x, 10-auction Avg 2.56x); Indirect Bidding 44.7% (Prior 62.5%, 10-auction Avg 50.7%)

-

USGS reports 5.8 magnitude earthquake in Baja California, Mexico region