Börsipäev 6. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Aktsiaturud on aasta alguses näidanud korralikku tugevust ning ostusurve ei taha vaibuda ka nõrkade makroandmete peale (eilne pending home sales). USAst on makroandmete poole pealt täna tulemas ADP detsembrikuu tööjõuraport, mis on siis prelüüdiks reedesele ametlikule tööjõuraportile. ADP numbrite järgi peaks kaduma riigist detsembris ca 75 000 töökohta. Kell 17.00 avalikustatakse ISM detsembrikuu teenindusindeks, millelt oodatakse 50.5 punkti (50 on see piir, kust ülevalpool algab kasv).Kolmapäevale traditsiooniliselt avaldatake kell 17.30 USA naftavarude raport, mis viimase aja külmade ilmade valguses on päris huvitav, et näha kas ja kui palju on varud nädalaga vähenenud.

-

EUR/USD, mis eile liikus 1,45 dollari lähedale, liikus hommikul järsult allapoole (hetkel 1,4335). Turule tuli üllatusena Euroopa Keskpanga täitevkommitee liikme Jürgen Starki kommentaar, et Euroopa Liit ei päästaks Kreekat fiskaalprobleemidest (varem on Brüssel lubanud Kreekat toetada). Kreekas esile kerkinud probleemidest & selle mõjust eurole saab pikemalt lugeda siit.

-

Ökonomistide 2010. prognoosid (link):

- Robert Shiller, Yale University: “Strategic default on mortgages will grow substantially over the next year, among prime borrowers, and become identified as a serious problem.

- Edward Glaeser, Harvard University: “Construction levels will stay low and my best guess is that housing prices — the 20 city Case-Shiller average — will be within 5% of current level, one side or the other.”

- Alan Blinder, Princeton University: “U.S. interest rates will go up across the board. Probably more at the long end than the short end.”

- Michael Feroli, J.P. Morgan Chase: “We’ll have above-trend growth, low inflation, and the fed on hold through 2010″

- Don Ratajczak, Morgan Keegan: “The odds of a double dip have gone from 1-in-3 to 1-in-5.”

- Anil Kashyap, University of Chicago: “The Democratic Party of Japan will be in a shambles. The economic program in Japan will be a complete mess by December.”

- Raghuram Rajan, University of Chicago: “There’s going to be a lot more noise made about China and its exchange rate. I won’t stick my neck out farther than that.”

-

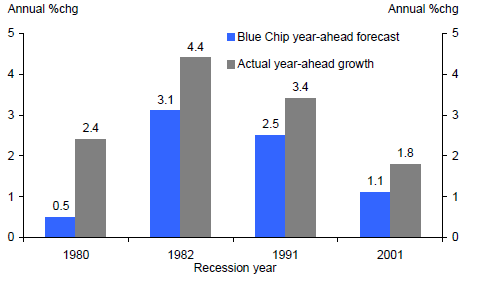

Ajaloos on konsensus tavaliselt majanduskasvu taastumist alahinnanud & paljud ökonomistid on seekord julgelt konsensusest kõrgemaid prognoose väljastanud (nt USA puhul räägitakse üha rohkem ca +4% SKP kasvust):

-

ADP küsitluse järgi kaotati detsembris erasektoris oodatust rohkem töökohti:

December ADP Employment Change -84K vs -75K consensus

November ADP revised to -145K from -169K

ADP raport on hea sissejuhatus reedesele tööjõuraportile, kus konsensus töökohtade kaotamist ei oota.

-

seekingalpha kohaselt oli konsensus 90 000

-

Erinevad küsitlused ilmselt (ise kasutame peamiselt briefingu numbreid) - turu jätab see raport igal juhul esialgu külmaks.

-

USA indeksite futuurid alustavad päeva nullilähedalt. Ära võib märkida gaasi ca 2%lise hinnahüppe.

Euroopa turud:

Saksamaa DAX +0,03%

Prantsusmaa CAC 40 +0,02%

Inglismaa FTSE 100 -0,18%

Hispaania IBEX 35 -0,14%

Rootsi OMX 30 N/A (börs suletud)

Venemaa MICEX N/A (börs suletud)

Poola WIG +0,07%Aasia turud:

Jaapani Nikkei 225 +0,46%

Hongkongi Hang Seng +0,62%

Hiina Shanghai A (kodumaine) -0,85%

Hiina Shanghai B (välismaine) -0,29%

Lõuna-Korea Kosdaq +1,13%

Tai Set 50 +0,55%

India Sensex 30 +0,08% -

Complacency Doesn't Always Bring a Countertrend Move

By Rev Shark

RealMoney.com Contributor

1/6/2010 8:50 AM EST

A positive attitude may not solve all your problems, but it will annoy enough people to make it worth the effort.

-- Herm Albright

The major indices have steadily moved higher since the first of November. Volume has been quite light at times, but we've had very limited pullbacks, and we even managed to break out to new recent highs without much of a struggle.

Positive seasonality has certainly helped keep the momentum going, but the most striking thing about the action is how confident and unconcerned market players have been. In fact, various sentiment polls show that bullishness is at its highest level in years.

When things look this good, some bears will always view it as a contrarian indicator. The idea is that with so much positive sentiment, most traders must already be heavily long, and that doesn't leave much buying power on the sidelines to drive us even higher.

Even though we had an amazingly long and persistent uptrend in 2009, it was one of the most hated rallies I have ever seen. Market players struggled the whole year, trying to reconcile the strong market action with high levels of worry about the overall economy. It was a classic case of climbing a "wall of worry."

As we enter 2010, the skeptics and pessimists are pretty worn out. They have fought the action for many months and were absolutely flattened by a market that was consistently overbought and extended on light volume.

So will the steadily increasing level of bullish complacency finally be a contrary indictor? The biggest problem with this argument is that it isn't a very precise timing device. We can run higher for a very long time on high levels of optimism, especially in an environment like we have had for months, where people are still recovering from the shock of the dramatic crash we suffered in 2008 and early 2009.

When bullish complacency is high, many market players will be poorly positioned if we do see some market weakness. Many will have to scramble to cut back positions and protect gains should we begin to falter. It can make for a very quick spike down once some selling kicks in.

As we continue to trend higher on light volume, the chances of a correction grow, but as I've written many times, markets tend to trend up or down much further and longer than seems reasonable to most of us. Trying to anticipate when a trend might end is the most dangerous thing you can do.

I don't try to anticipate a market turn; rather, I wait until some selling actually kicks in. If it really is a meaningful top or bottom, then the new trend will last for a while. We don't want to lose our hard-fought profits, so we should stay very vigilant and make sure we quickly lock in some gains when things do start to weaken.

Give the benefit of doubt to the bulls until they actually do something wrong. The price action will tell us when it's time to be more defensive, and so far there isn't much wrong with this market other than the fact that a lot of folks are pleased with it.

We have a very slight negative open on the way, and it's fairly quiet. Asian stocks we mostly up but Europe is mostly down.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: FDO +8.4%, CMFO +8.3%, TPX +6.6%, ANGO +6.5%... Select security/counter-terrorism related names are showing strength boosted by comments from Cramer on MadMoney: COGT +4.4%, ID +3.5%, NICE +3.0% (Cramer recommends this stock as another counter-terrorism play), ASEI +2.3%, OSIS +1.5%... Other news: NLST +10.6% (scheduled to make an investor presentation at the Needham 12th Annual Growth Stock Conference on January 14), ABAT +7.9% (continued strength from yesterday's pop), CPHD +6.5% (receives FDA clearance for first rapid and accurate surveillance test for vanA), BEXP +4.8% (announced that its operated State 36-1 #1H produced ~3,807 barrels of oil equivalent per day), USEG +4.5% ( announces initial production rate of ~3,807 BOE/D from the State 36-1 #1H well), ACH +4.5% (seeing early strength with Bloomberg reporting that co said snow 'had no impact' on production), IVN +1.6% (appoints Citi as adviser on strategic options to further enhance shareholder value), SAP +1.0% (still checking)... Analyst comments: BRKS +9.5% (upgraded to Overweight at Barclays), LOCM +8.6% (Leveraging existing website traffic, Local.com bulks up with small business customers - Merriman), BZ +6.4% (raised to Buy from Neutral at Goldman- DJ), CLNE +4.5% (upgraded to Buy at BofA/Merrill), SOLF +3.7% (target raised to $13 from $10 at Oppenheimer), FNSR +3.7% (upgraded to Overweight at Weisel), TSN +2.9% (upgraded to Outperform from Market Perform at BMO Capital Markets), CREE +2.3% (upgraded to Buy at BofA/Merrill), MMM +2.2% (added to Americas Conviction Buy list at Goldman- Reuters), MMC +2.2% (upgraded to Outperform at FBR Capital), ACI +2.0% (upgraded to Buy at UBS), DOW +1.6% (upgraded to Overweight at Barclays), CVA +1.5% (upgraded to Neutral at BofA/Merrill), SAI +1.2% (upgraded to Neutral from Underweight at JP Morgan), CERN +1.1% (upgraded to Outperform at Baird), KSS +1.0% (initiated with a Buy at Sterne Agee).

Allapoole avanevad:

In reaction to disappointing earnings/guidance/SSS: SONC -12.2% (also downgraded to Mkt Perform from Outperform at Morgan Keegan), WOR -6.3%, MON -3.4%, WAG -2.3%, MOS -0.6%... M&A news: KFT -1.6% (Kraft Foods had received valid acceptances of the Offer in respect of a total of 20,917,708 Cadbury shares representing ~1.52% of the existing issued share capital of Cadbury)... Other news: BZH -8.7% (announces it is commencing concurrent underwritten public offerings of common stock and mandatory convertible subordinated notes; reports new home orders and closings for the quarter ended December 31, 2009), GTE -4.2% (announces Dantayaco-1 exploration well results), AIB -3.5% (top the BarCap list of 20 banks that are "too big to fail" and are therefore likely to attract higher capital requirements as well as be called upon to match lending more closely with deposits - FT), ETP -2.9% (announces 7.5 mln common unit offering), T -2.1% (trading ex dividend), MT -2.1% (still checking), HALO -1.7% (files $100 mln mixed securities shelf offering), SYT -1.6% (still checking)... Analyst comments: IRBT -6.1% (downgraded to Underweight from Neutral at JP Morgan), LPX -6.0% (cut to Sell from Neutral by Goldman- DJ), CMC -3.3% (cut to Sell from Neutral at Goldman- Reuters), POOL -2.8% (downgraded to Underweight from Neutral at Piper), SNN -2.6% (downgraded to Neutral at Piper), DT -1.6% (downgraded to Sell at UBS), LMT -1.6% (cut to Sell from Neutral at Goldman- DJ), ERJ -1.6% (downgraded to Underweight at JPMorgan), IP -1.6% (removed from Americas Conviction Buy list at Goldman; keeps Buy rating- Reuters), LKQX -1.4% (downgraded to Neutral from Buy at Piper), WY -1.4% (cut to Neutral from Buy at Goldman- DJ). -

December ISM Services 50.1 vs 50.5 consensus, November 48.7 (ISM > 50 näitab olukorra paranemist USA teenindussektoris. See ISM ei ole muidugi võrreldes tööstussektoriga nii tsükliline & sellele pöörab turg reeglina vähem tähelepanu)

-

Möödunud nädala jooksul:

Toornafta varud +1.3 mln vs oodatud -1.0 mln barrelit

Mootorkütuse varud +3.7 mln vs oodatud +0.8 mln barrelit

Distillaatide varud -0.2 mln vs oodatud -1.9 mln barrelit -

Nafta tänaseks 10 kauplemissessiooni järjest ülespoole rühkinud ja hetkeks käidi ka $83 barrel tasemest kõrgemal. Naftaraport ei anna selliseks ralliks põhjust ( Joeli kommentaar ). Paistab, et täna jälle selline päev kus ostetakse kõike.

-

ComScore says U.S. retail e-commerce spending up 4% in holiday season - DJ

-

Some on FOMC said wind-dwon of MBS may hurt housing

Fed officials still concerned about weak labor market - DJ

FOMC members said more stimulus 'might become desireable'

One FOMC member thought asset purchases could be scaled back -

Kushi Resources, Inc. (OTCBB: KUSI) - saaksite kaubeldavate aktsiate nimekirja lisada? tundub huvitav!