Börsipäev 12. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

USA makro osas jätkub sarnaselt eilsele vaikelu - Eesti aja järgi kell 15.30 on välja tulemas üksnes USA novembrikuu kaubandusdefitsiit, mille suurusjärguks oodatakse ca $34.5 miljardit.

Kuigi Alcoa (AA) aktsia kukkus eilsel järelturul tulemuste peale ca 5%, siis Morgan Stanley analüütikud on olnud varmad oma ostusoovitust kinnitama ning on väljas $22lise hinnasihiga, öeldes, et tulemustejärgset nõrkust tuleks hoopis ostmiseks ära kasutada. Morgan Stanley ütleb, et nende overweight soovitus on kogu aeg põhinenenud tsükli keskpaigas teenitavatel kasumitel ning praegu oleme alles tsükli algusfaasis, mistõttu on järgnevatel kvartalitel kasumid suurenemas.

Morgan Stanley AA aktsiate soetamise kohta eilse languse järel: "We believe risk reward remains skewed 3:1 to the upside."

Alumiiniumituru kohta tervikuna prognoosis Alcoa juhtkond aastal 2010 ca 10%list nõudluse kasvu. -

Ameerika Ettevõtlusinstituudi majandusteadlane ja endine IMF ametnik Desmond Lachman, kes võtab meedias majandusteemadel üsna aktiivselt sõna, kirjutab FT-s ilmunud artiklis, et Kreeka täbarale finantsseisule pole muud rohtu kui astuda välja eurotsoonist, võtta tagasi oma vana rahaühik ja seda devalveerides päästa majandust veel sügavamasse langusesse sattumisest, mida hakkavad põhjustama Maastrichti kriteeriumite nimel tehtavad poliitilised kärped. Artiklit on võimalik lugeda siit.

-

Nafta hinna suhtes on arvamused väga erinevad. Eile ütles D. Parrilla (BofA Merrill Lynch) Bloombergis: “If you don’t hold commodities, you’re not flat, you’re short. The risks are skewed to the upside.” Parrilla sõnul jõuab nafta hind aasta lõpuks 100 dollari juurde (ja kuld järgneva 18. kuu jooksul koguni 1500 dollari juurde).

Täna kirjutavab Deutsche Banki toorainete meeskond:

We expect that 2010 will mark the transition back to the traditional fundamentals relating to oil supply, demand and inventories in contrast tofinancial, currency and equity market drivers that we believe dominated oil price trends last year. In our view, this would mean that rallies in the oil priceabove USD80/barrel will only become sustainable in 2011.

Allikas: Deutsche Bank

-

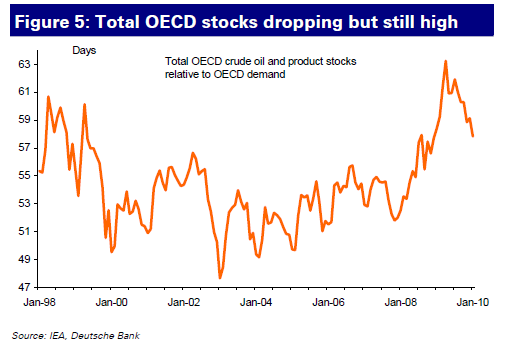

Miku kommentaarile lisaks tahaksin siia panna ka ühe graafiku USA mootorkütuse varude kohta päevades - hoolimata majanduskriisist ja väiksemast tarbimisest (mis vähendab murru nimetajat) ja suurematest varudest (mis suurendab murru lugejat), on mootorkütuse varud USAs viimase mitme aasta keskmise lähedal. Kui aga tarbimine peaks suurenema, on see näitaja kiiresti allapoole tulemas.

-

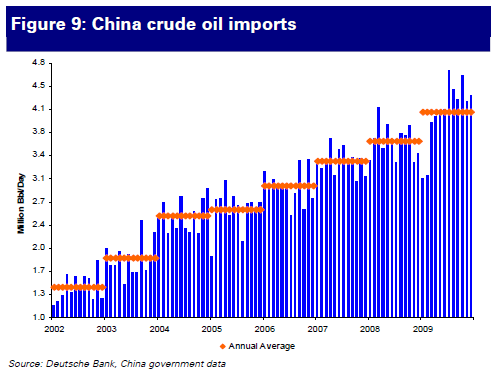

& väljaspool USA näeb väga ilus välja Hiina nafta impordi kasv:

Allikas: Deutsche Bank

-

Hartford Financial (HIG) raises guidance, sees EPS of $1.45-1.60 vs $0.83 First Call consensus

-

Tänase päeva suurimaks langeja-börsiks on Kreeka ca 5% kuni 6%lise miinusega.

Saksamaa DAX -1,60%

Prantsusmaa CAC 40 -1,23%

Inglismaa FTSE 100 -1,15%

Hispaania IBEX 35 -0,79%

Rootsi OMX 30 -0,92%

Venemaa MICEX -1,28%

Poola WIG -1,12%Aasia turud:

Jaapani Nikkei 225 +0,75%

Hongkongi Hang Seng -0,38%

Hiina Shanghai A (kodumaine) +1,91%

Hiina Shanghai B (välismaine) +1,22%

Lõuna-Korea Kosdaq -0,42%

Tai Set 50 -0,43%

India Sensex 30 -0,59% -

Get Ready for the Roller Coaster

By Rev Shark

RealMoney.com Contributor

1/12/2010 8:24 AM EST

Fasten your seat belts. It's going to be a bumpy night.

-- Bette Davis in All About Eve

The S&P 500 is 6-and-0 for 2010, but the bears have some negative news this morning and may finally put some points on the scoreboard. Alcoa (AA) kicked off earnings season with a disappointing report. Aluminum stocks have been extremely hot lately, but AA posted earnings of 1 cent a share vs. expectations of 6 cents. That news is hitting the metals sector, which has been one of the strongest in the market recently.

The other negative news out there is that China central bank raised the yield on one-year bills more than expected. There has been quite a bit of speculation lately that China would be tightening economic policy to avoid an overheated economy. The news this morning appears to confirm that talk.

The good news about the China tightening is that it is an indication that Chinese central planners do believe that a recovery is sustainable without further government intervention. Stocks in Shanghai traded higher overnight but virtually all other markets overseas are trading down this morning.

I've been writing quite a bit lately about how the market was becoming increasingly extended and in danger of a pullback. While it was very important to stay vigilant and protect gains, we shouldn't have gotten overly bearish until there was some notably poor price action. This morning it finally looks like we are going to get the first real efforts by the bears this year.

Now that the bears have a weak open, can they build on it? The technically extended nature of the market leaves us quite vulnerable to a sharp spike lower, but the key is going to be whether the dip-buyers are still interested in jumping in. They have barely let the market go red over the past couple of weeks before they jumped in. Ironically, when we have sharper drops like we are seeing this morning the dip-buyers will often lose their conviction. The idea of buying weakness always sounds great when we are going straight up, but it tends to lose its appeal when we have some real weakness.

We have to see whether the earnings report from Alcoa sets the mood for earnings season. Over the last three quarters, stocks have performed well as they reported earnings, but we are now trading at higher prices and that increases the danger of a "sell the news" reaction. Alcoa may just be an aberration, but we often see a persistent earnings theme emerge during reporting season.

Tighten up your seat belts and fasten on your trading helmets, the ride is about to become much bumpier.

---------------------------

Ülespoole avaneva:

In reaction to strong earnings/guidance: ELX +12.2% (also upgraded to Outperform at Morgan Keegan), CRUS +11.8% (also upgraded to Strong Buy at Needham), SVU +5.7%, PVH +4.0% (also added to Top Picks Live list at Citigroup), INFY +4.0% (also upgraded to Buy from Underperform at BofA/Merrill) ... M&A news: ZRBA +91.1% (announces merger agreement with Woodstream Corp; ZRBA shareholders to receive $9.00 cash per share)... Other news: VLNC +19.6% (confirms a $3.1 mln purchase order from The Tanfield Group to deliver advanced battery modules for both lines of fully electric vehicles in its range, the Smith Edison and Smith Newton), STXS +11.3% (notified of the FDA approval of an additional magnetic irrigated catheter), VICL +9.5% (Vical licensee AnGes MG reaches agreement with FDA for Phase 3 Trial of Collategene angiogenesis product), SCLN +8.3% (SciClone Pharma and Sigma-Tau announce positive preliminary results in clinical study examining ZADAXIN'S ability to enhance response to H1N1 vaccine), CTFO +4.6% (announces it received rmb 4 million technology innovation funds for TransPLE product), NVAX +3.6% (announces positive preclinical results for its Respiratory Syncytial Virus vaccine candidate), MMR +3.6% (continued momentum), YRCW +3.4% (S&P raises ratings on YRC Worldwide to 'CCC-' from 'SD'), TM +3.2% and HMC +3.3% (still checking), GME +1.9% (announces capital allocation strategy including $300 mln share repurchase program), JCI +1.1% (Cramer makes positive comments on MadMoney)... Analyst comments: MGM +5.5% (upgraded to Buy at Goldman), MTG +2.9% (initated with Buy at Goldman), PG +0.8% (upgraded to Buy at BofA/Merrill).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: MFLX -14.3%, ATSI -13.6% (light volume), ERTS -9.1%, KFN -9.0%, AA -6.6% (also downgraded to Underperform from Market Perform at BMO Capital Markets), WDFC -4.0%, KBH -2.9%, CVX -1.2%... Select oil/gas related names stocks showing weakness following CVX guidance: RDS.A -2.1%, TOT -2.1%, SLB -2.1%, FTO -2.0%, VLO -1.9%, MUR -1.8%, HAL -1.8%, PBR -1.6%, STO -1.6%, BP -1.6%, COP -1.5%, TSO -1.3%, SUN -1.3%, MRO -1.2%... Select metals/mining related names trading lower: GFI -3.3%, AU -3.3%, MT -3.1%, RTP -3.0% (Miners shun China in iron ore price talks - FT), BBL -1.8%... Select video game related names ticking lower following disappointing ERTS guidance: ATVI -1.9%, THQI -1.2%... Select financials showing weakness: AIB -8.2%, IRE -6.2% (Bank of Ireland will review capital post-NAMA - DJ), UBS -3.2%, ING -3.1%, DB -2.6%, STD -2.2%, BCS -1.5%CS -0.9%... Other news: HT -11.9% (announces public offering of 35,000,000 common shares), AEC -6.5% (announces a 4.5 mln share common stock offering), OEH -5.6% (light volume; announces 10 mln share common stock offering), TLP -5.0% (announces offering of 1,750,000 common units), LGCY -4.7% (announces sale of fuel cell power modules to Advanced Public Transportation Systems bv in Europe), PEIX -4.0% (pulling back from this week's 100% surge higher), CRM -3.9% (announces a $500 mln convertible sr notes offering), NLST -1.7% (files for $30 mln mixed securities shelf offering), AKS -1.6% (announces price increase for carbon steel products)... Analyst comments: MYGN -4.2% (downgraded to Underperform at Oppenheimer), FDO -3.8% (downgraded to Sell at Goldman), GPS -3.0% (downgraded to Sell at Goldman), PMCS -2.9% (downgraded to Underperform from Neutral at BofA/Merrill), CHS -2.4% (downgraded to Neutral from Outperform at Credit Suisse), XLNX -2.1% (downgraded to Neutral from Buy at BofA/Merrill), NYB -2.0% (downgraded to Neutral from Buy at BofA/Merril), MSCC -1.9% (downgraded to Hold from Buy at Jefferies), SMTC -1.8% (downgraded to Underperform from Neutral at BofA/Merrill), FNFG -1.3% (downgraded to Neutral from Buy at Goldman). -

võisin valest näha, aga mõni hetk tagasi nägin AAPL müügi poolel 208 pealt 49600 suurust pakki

-

Fitch affirms Saudi Arabia at 'AA-'; outlook stable

-

EU mulling tough rules for derivatives clearing houses - DJ

-

$40 bln 3-year Note Auction Results: Yield- 1.490% (1.513% expected); Bid/Cover- 2.98x (12-auction avg 2.72x, prior 2.98x); Indirect Bidders- 38.0% (12-auction avg 48.5%, prior 60.9%)

Oksjoni tulemused annavad hetkel turule kergelt tuge. -

American Intl: US House panel issues subpoena for NY Fed's AIG documents - DJ

-

SPY'l pole senini veel 2010. aastal olnud ühtegi languspäeva. 6 järjestikuse tõusupäeva järel on languspäev kosutav ning tõenäoliselt pullide ostuisu taas üles vürtsitamas.

-

NASDAQ Prices $1 Billion Senior Notes Offering