Börsipäev 13. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Täna pole küll 13. ja reede, kuid see-eest erinevaid uudiseid lugedes võib mõnedel selline tunne jääda küll. Haiti pealinna tabanud 7-palline väga tugev maavärin on suure osa linnast rusudesse jätnud ning väga professionaalsete ja kõrgetasemeliste küberrünnakute tõttu Google'i (GOOG) Hiina lehekülje vastu on Google kaalumas Hiina turult üldse lahkumist. Halb uudis Google'ile ja hiinlastele, suurepärane uudis Baidu.com'ile (BIDU). BIDU peaks olema tänane staaraktsia, kes teeb läbi börsil võimsa tõusu.

Olulisi makroraporteid täna muidu USAst tulemas ei ole. Eesti aja järgi kell 17.30 näeme naftavarude raportit ning kell 21 avaldatakse Treasury eelarve numbrid ning Föderaalreservi Beeži raamatu sisu (kuid neid eriti ei jälgita).

-

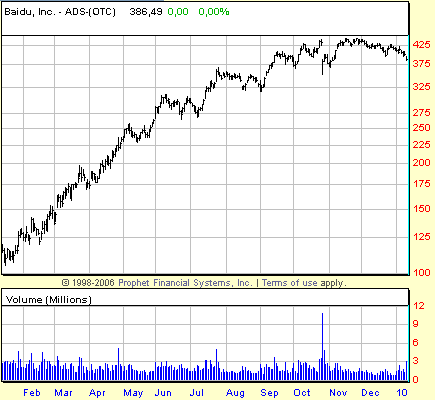

Panen siia ka BIDU aktsiagraafiku:

-

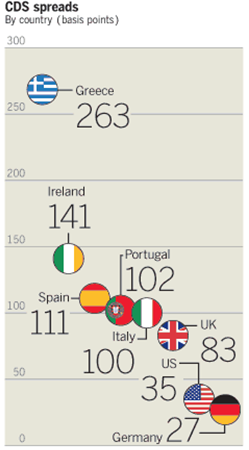

Keskpankade raha printimine ja suured eelarve puudujäägid on tõstnud esimest korda riikide pankrotiriski ettevõtetest kõrgemale:

Markit’s iTraxx Europe index of 125 companies was on Tuesday trading at 63 basis points, or $63,000 to insure $10m of debt over five years. This compares with 71.5bp, or $71,500, for Markit’s SovX index of 15 European industrialised nations.

Lääne-Euroopas on pankrotioht kõige suurem Kreekas, mida osad võrdlevad Lehmaniga (loe siit):

Allikas: FT

-

Saksamaa statistikaameti kohaselt kahanes riigi SKT 2009. aastal -5% ehk 0.2 protsendipunkti võrra enam Bloombergi küsitletud analüütikute konsensusest. Uudis ei näi aga väga häirivat investoreid ning DAX jätkab hommikuse miinuse vähendamist.

-

Kui palju tänasele staaraktsiale siis eilsele 7% järelturu tõusule lisaks pakute?

-

ma oleks BIDU suhtes päris ettevaatlik, tasuks nädala ja eelmise nädala lõpu uudist ikka ka läbi lugeda

-

BIDU hetkel kauplemas juba üle +8% tõusus $419 tasemel. GOOG hetkel indikeerimas avanemist $580 tasemelt.

-

BIDU-ga on alati nalja saanud enne opts. reedet, hakka või kahtlustama

-

Kuna Google sai eelmisel aastal Hiinast ca protsendi oma tuludest, siis soovitavad analüütikud kasutada langust Google'i aktsia hinnas ostmiseks. Näiteks DB kirjutab:

We estimate the China market generated <$200mn in 2009E revs, or 1.1% of net revs(0.8% of gross). Despite not breaking out the profitability of the business, we think China generated modest profits at best -- less than $0.15 in EPS. On the current 23x 2010 P/E multiple, this would imply an equity impact of $4/share.We acknowledge the long term implications of withdrawing from China, but the financial impact on Google is minimal in the near term. With a rebound in online ad spending, we believe fundamentals remain robust, and would be buyers on the current share weakness. We think the current pull back offers an attractive buying opportunity, esp. heading into earnings next week.

-

no way ta sellise kasvu ja mahuga turult välja astub, pigem arvaks, et tegu on pr-ga, et ennetada-vaigistada kriitikat.

-

BIDU hetkel siis juba +16% @ new all-time high $448.

Tõusu aitab kütta mitme erineva faktori koosmõju alates Google'i võimalikust lahkumisest, Hiina turuosa endale võitmisest ning lõpetades tõigaga, et tegu on optsioonide lõppemise nädalaga, mis tähendab, et kui mõni institutsioon oli välja kirjutanud kõrge strike'iga ostuoptsioone, ei jää neil midagi muud üle, kui aktsiaid lihtsalt kokku osta. Viimaste andmete põhjal oli 10% floatist lühikeseks müüdud ja lisaks on uus all-time high ligi meelitams TA ja momentumraha. -

BIDU jaanuari optsioonide open interest on suurim kusagil 420 kandis, ei ole kindel, aga tavaliselt on vist suurim open interest ikka raha peal (at the money - ATM) optsioonidel, mitte neil, mis veel eile parasjagu rahast väljas olid

-

Ja miks kõrgema strike'iga ostuoptsioonide omanikud aktsiaid peaksid ostma (kui need on rahast väljas)?

-

Henno, üldiselt nii ta on jah - eriti kui optsioonireede lähemale hakkab tiksuma (toimub lihtsalt poolautomaatne positsioonide ümbermängimine). Aga kui aktsia tõuseb või kukub väga kiiresti loetud päevade jooksul, siis võidakse sellest oluliselt erineda. Viimase viie börsipäevaga on aktsia kukkunud 420 alt eile õhtuks 386ni, mis võiks aidata seda eripära pisut selgitada.

-

Kreeka asub lääne euroopas:O ?

-

punane, kui mõni institutsioon on jätnud oma callid kõrgematel strike'idel katmata (kuivõrd tõenäoline on ikka aktsia tõus 386 pealt näiteks üle 420 või 430 või 440 ainult 3 päevaga??), siis eile täiesti väärtusetuid ostuoptsioone käes hoidnud investoritel on nüüd õigus nt ostuoptsiooni välja kirjutanud vastaspoolelt osta aktsiat 420, 430, 440ga jne. Kui vastaspoolel on callid katmata, on see tema mure need aktsiad kõrgema hinnaga endale portfelli osta.

Aga laias laastus oli see lihtsalt üks õhkuvisatud mõte, mis võib aidata paanilist ostusurvet eelturul siin selgitada, kuid tegelike järelduste tegemiseks olekski vaja teada erinevate institutsioonide optsiooniraamatute seisu/sisu... -

UBS valab veel õli juurde ja tõstab Baidu.com (BIDU) soovituse 'osta' peale ning hinnasihi $523 peale.

-

USA tähtsamate indeksite futuurid alustavad päeva eilsete sulgumistasemete juurest.

Saksamaa DAX +0,46%

Prantsusmaa CAC 40 +0,12%

Inglismaa FTSE 100 -0,09%

Hispaania IBEX 35 +0,26%

Rootsi OMX 30 +0,36%

Venemaa MICEX +1,08%

Poola WIG +0,35%Aasia turud:

Jaapani Nikkei 225 -1,32%

Hongkongi Hang Seng -2,59%

Hiina Shanghai A (kodumaine) -3,10%

Hiina Shanghai B (välismaine) -0,88%

Lõuna-Korea Kosdaq -0,68%

Tai Set 50 +0,20%

India Sensex 30 +0,50% -

Market Likely to Resume Its Upward Climb

By Rev Shark

RealMoney.com Contributor

1/13/2010 8:36 AM EST

"The art of war teaches us to rely not on the likelihood of the enemy's not coming, but on our own readiness to receive him; not on the chance of his not attacking, but rather on the fact that we have made our position unassailable."

-- Sun Tzu

After six straight days of gains, the S&P 500 finally suffered some profit-taking on Tuesday. The selling was actually more aggressive than the indices showed as big-cap technology stocks continued their recent underperformance and some of the recent small-cap leaders took some hits.

The market has been so strong for so long that there tends to be a number of folks who very quickly begin to wonder if maybe this time we really are going to see a significant top. All it takes is one day or so of weakness to cause the overanxious bears to start talking about how this market is ready to fall apart. They quickly breathe a sigh of relief over any weakness because they have been abused by this market for as long as they have anticipated a top.

Unfortunately, for our ursine friends, one day of weakness in a market that has been marching straight up and is technically extended isn't particularly significant. That doesn't mean that a more severe correction won't develop, but there is still nothing in the action to indicate that the very strong uptrend is about to end.

What complicates matters even more at this point is that we are about to enter fourth-quarter earnings season. Earnings season often produces a theme like "sell the good news" or "buy the bad news," depending on the level of expectations. Back in July, as second-quarter earnings reports were released, we had a tremendously strong response. Meredith Whitney kicked it off with bullish comments about Goldman Sachs (GS) , which then produced a very good report, but it was a surprisingly strong report form Intel (INTC) that really caused things to move.

Third-quarter earnings season was much more mixed. A number of reports, including Intel's, appeared to be quite strong but then sold off subsequently. Oddly, while many individual reports saw a "sell the news" reaction, the broad market held up extremely well, and we rallied nicely in the early part of October. We then reversed around mid-month and ended the month close to where we started.

Intel reports on Thursday night, and that should be our first good clue as to the market move. Obviously, with the market trending up steadily since mid-November, expectations are rather high. Even more worrisome is that bullish sentiment is moving toward stratospheric levels. In the latest Investors Intelligence poll, bullish sentiment has moved to 53.4% from 48.3%, and bearish sentiment has declined to 15.9%. There is no doubt that there is a very high level of complacency, and that is a dangerous condition when we enter earnings season.

The market is rebounding a bit this morning. There is some drama over the possibility of Google (GOOG) leaving the China market, which is causing a big positive reaction in Baidu (BIDU) , but it is the upcoming earnings season that is going to determine our overall direction over the next few weeks.

Presently, the market is still extended and ripe for some profit-taking, but this has been a market with extremely shallow pullbacks for some time. I've taken a more defensive stance, but there still are some bullish chart patterns in individual stocks, and I'll be happy to buy them as they set up.

Earnings season is going to be particularly interesting, and we will need to be prepared to move quickly as events unfold.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: CFI +6.9% (light volume), FUL +2.9%, KFT +2.2%, LLTC +2.1%, WPI +1.5%, TQNT +1.0%... Select metals/mining related names showing strength: RTP +2.3% (upgraded to Buy at Canaccord), BHP +2.0% (upgraded to Buy at Canaccord), BBL +2.0%, GOLD +1.7%, GFI +1.6%, AU +1.4%... Other news: MRNA +77.7% (Reports Potent Anti-Tumor Activity Against Multiple Targets in Liver and Bladder Cancer), BIDU +16.7% and SOHU +4.4% (Google to end China censorship after e-mail breach - AP; also upgraded to Buy at Deutsche), HYTM +12.0% (reports published paper sponsored by Hythiam to develop advanced tools for use in its Catasys program), BCRX + 7.1% (BioCryst Pharm's partner Shionogi receives marketing and manufacturing approval For Peramivir in Japan), TPI +6.2% (Receives Chinese SFDA Approval for Ofloxacin and Fleroxacin), CLNE +4.8% (Cramer makes positive comments on MadMoney), NFLX +4.2% (light volume; announces Movies, TV episodes streamed from Netflix headed to Nintendo's Wii console this spring), ASML +3.7% (still checking), PLX +3.2% (European Medicines Agency's COMP adopts positive opinion for the Orphan Drug designation for Protalix's taliglucerase alfa), SVA +2.6% (obtains fifth H1N1 vaccine order from Chinese central government ), NOK +2.6% (still checking for anything specific), OEH +2.5% (announces pricing of common share offering at $10.00/share), ERIC +2.4% (Ericsson seals TeliaSonera 4G deal - The Local), SNE +2.1% (still checking), MEE +1.6% (begins development of new metallurgical coal mine; also upgraded to Buy at BofA/Merrill), AA +1.5% (modestly rebounding)... Analyst comments: JOYG +2.8% (upgraded to Buy from Neutral at UBS), IACI +2.2% (upgraded to Buy from Neutral at Goldman), WU +2.1% (initiated with an Overweight at Morgan Stanley), WYN +1.8% (upgraded to Buy at Deutsche), AZN +1.7% (upgraded to Neutral from Underperform at Credit Suisse), CHL +1.6% (initiated with a Outperform at Bernstein), PCS +1.6% (upgraded to Hold at Deutsche), UPS +1.3% (upgraded to Outperform from Sector Perform at RBC Capital), V +1.0% (initiated with an Overweight at Morgan Stanley).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: FMBI -3.2% (also announces proposed $150 mln common stock offering)... Other news: HEV -4.6% (light volume; discloses that it and Fisker Automotive have ceased discussions with respect to the feasibility of a business relationship concerning the Fisker Karma vehicle program), EPB -4.5% (announces 8 mln common share offering), NGLS -4.2% (announces a 5.25 mln share common unit offering), CCME -3.2% (China MediaExpress and Starr International Company announce $30 million private placement), GOOG -2.2% (Google to end China censorship after e-mail breach - AP), LUNA -2.1% (pulling back from yesterday's midday surge higher)... Analyst comments: AFFX -9.5% (downgraded to Underweight at Barclays), ECOL -2.3% (downgraded to Sector Perform from Outperform at RBC Capital; also trading ex dividend), CHU -1.1% (initiated with a Underperform at Bernstein), PCU -1.0% (downgraded to Underperform from Neutral at BofA/Merrill). -

Baidu eelturul tehtud tõusust lastakse korralikult õhku välja ja 10% tõusu veel jäänud. Google'il ei lasta esialgu ära vajuda & hetkel -2.4%.

-

Jim Cramer on täna RealMoney all üllitanud teksti pealkirjaga 'Nat Gas is Happening With or Without Obama'. Meeldib meilegi maagaasisektor ning meie omalt poolt pooldame pikaajaliste investeeringute tegemist USA suuruselt teise maagaasitootjasse Chesapeake Energy'sse (CHK).

-

Baidu üsna radioaktiivne hetkel, kel närvi võib proovida

http://www.thestreet.com/_yahoo/story/10660528/1/baidu-soars-as-google-rethinks-china.html?cm_ven=YAHOO&cm_cat=FREE&cm_ite=NA -

Toornafta varud suurenesid oodatust rohekm:

Dept of Energy reports that crude oil inventories had a build of 3699K (consensus is a build of 1500K); gasoline inventories had a build of 3791K (consensus is a build of 1700K); distillate inventories had a build of 1353K (consensus is a draw of 1300K).

-

White House bank-tax proposal to target liabilities, sources say - WSJ

Ilmselt on selle uudise taga finantsi tugevus ja finants ühtlasi ka kogu turu tõusu vedanud. REIT ka tugevad. -

$21 bln 10-year Note Auction Results- Yield: 3.754% (3.763% expected); Bid/Cover: 3.00x (6-auction Avg 2.85x, prior 2.62x); Indirect Bidders: 29.0% (6-auction avg 45.7%, prior 34.9%)

-

Ja taaskord olukord, kus turu tõusu taga on käive S&P 500 futuurides ja SPY-s. Turu kogukäive siinkohal suht nigel.

-

ERX ja ERY hetkel mõlemad +0.3% tõusus, XLE +0.10%.

-

Fed's Evans says still sees extended period of low-interest rates - DJ

Fed's Evans says economy must improve in strongly sustainable fashion before fed chances policy - Reuters

2 minuti pärast Beige Book ja Treasury Budget väljas. -

Bank of America (BAC) said to reduce cash component of bonuses to 15%-- Bloomberg

-

Beige Book: Credit Quality Still Worsening Since Last Report - DJ

Fed's Beige Book: Economic Activity Low, But Improving Slightly - DJ -

December Treasury Budget -$91.9 bln vs -$92.0 bln consensus

-

S&P lowers various California debt ratings

Standard & Poor's Ratings Services lowered to 'A-' from 'A' its ratings and underlying ratings (SPURs) on California's $63.9 billion of general obligation (GO) debt, and to 'BBB+' from 'A-' its ratings and SPURs on the state's $9.4 billion of appropriation-backed lease revenue bonds. We also lowered to 'A-' from 'A' our rating on the state's $1.9 billion proposition 1A receivables program bonds, and to 'A-2' from 'A-1'our rating on the state's $2 billion commercial paper (CP) program. At the same time, we affirmed our 'SP-1' short-term rating on the state's $8.8 billion in revenue anticipation notes (RANs). The outlook is negative. Our 'A+' ratings and SPURs on the state's roughly $8.06 billion of sales tax-supported GO economic recovery bonds are not affected. These ratings have a stable outlook. The rating actions reflect our view of the state's credit quality in light of its severe fiscal imbalance and the impending recurrence of a cash deficiency if the state's revenue and spending trajectories continue. -

Kas VTAL viimaste päevade tõusul mõni uudis ka taga on

-

VTAL astub täna publiku ette Needhami Growth stock konverentsil, muid uudised ei paista. Käive üsna õhuke nii, et kui keegi kergelt ostmas, siis ka kerge hinda liigutama.

-

Hetkel tundub nagu kellelgi oleks juba makroandmed olemas, kummaline liikumine täna. Eriti mõistmatuks jääb jällegi futuuride ja SPY üsna korralik käive vs Hr. Turu lahja käive.