Börsipäev 14. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

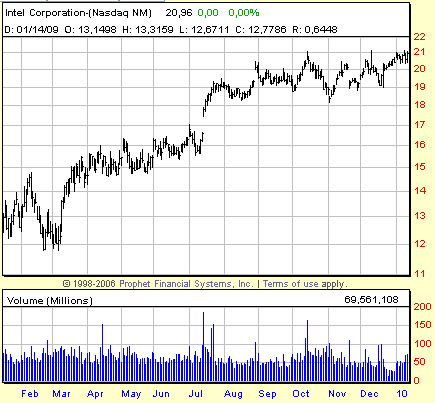

Vaiksed päevad hakkavad börsil nüüd tasapisi läbi saama ning iga mööduva päevaga jõuame lähemale tulemuste hooajale. Järgmisel nädalal on tulemas juba mitmete oluliste ettevõtete tulemused, kuid täna õhtul pärast turu sulgemist näeme Inteli (INTC) kvartalinumbreid. Intelilt oodatakse ca $0.30list EPSi ja müügitulu ca $10.16 miljardit.

Makroandmete poole pealt avaldatakse täna kell 15.30 möödunud nädala esmaste tööötu abiraha taotlejate arv (ootus 436 000 - number vahemikus 400-450 tähendab reeglina umbkaudu, et töökohtade kaotamisi ja loomisi on umbes samapalju. Mida väiksem esmaste töötu abiraha taotlejate arv, seda parem uudis aktsiaturule). Kestvate töötu abiraha taotlejate arvult oodatakse langemist 4.75 miljonini. Detsembrikuu jaemüügilt oodatakse 0.5%list kasvu (ilma autodeta +0.3%). Kell 17.00 avaldatakse detsembrikuu ärivarude muutus, kus oodatakse varude ca 0.3%list kasvamist.

-

Marc Faber ei väsi välja toomast, miks USA on oma fiskaal- ja rahapoliitikaga hukule määratud - nõnda ka Bloombergi esmaspäevases intervjuus. Aktsiaturgudest juttu tehes on ta üha rohkem veendunud lähiaja korrektsioonis. Muuhulgas nendib Faber, et kui ta oleks nõus võtma suurt riski, panustaks ta praegu S&P 500 langusele. Sest ehkki turg näib uskuvat momentumi jätkumisse, juhib Faber tähelepanu teatud tehnoloogia- ja finantssektori aktsiatele, mille tagasihoidlikum sooritus viimastel kuudel ananb vihje turu suurenenud nõrkusest. Teiseks ja kolmandaks pole tema sõnul aktsiaturgudele minevikus tavaliselt nulliga lõppevad ja Kongressi valimise aastad soodsalt mõjunud.

-

Citigroup usub, et aastal 2011 ECB intressimäärade kallale ei lähe - link siin.

-

Täna kell 14.45 avalikustab Euroopa Keskpank intressimääraotsuse ning kell 15.30 korraldatakse pressikonverents, kus Trichet ilmselt nendib, et praegune laenumäär on majanduskeskkonnale sobilik, ega vihja madalate inflatsiooniootuste tõttu intresside võimalikku tõstmist lähitulevikus.

Teema, mis on ka keskpanga liikmete esinemistes viimasel ajal üha tugevamalt märkimist leidnud, on Kreeka fiskaalne ebastabiilsus. Sellele lisaks viitas Euroopa Komisjon hiljuti oma raportis riigi ebausaldatavale statistikale, mis võib viia eelmiste aastate defitsiidi- ja võlanäitajate revideerimiseni. Näis, kas karmikäelisema hoiaku võtab oma kommentaarides ka Trichet.

-

Peale õhtuseid INTC tulemusi on ka finantssektorist tulemas tulemuste avalöök. Homme hommikul Eesti aja järgi kell 14:00 avaldab kvartalitulemused ka JPM, mis teeb ühtlasi sissejuhatuse finantssektori viimase kvartali tegemistele.

-

Kutsume kindlasti kõiki julgelt 2010. aasta üheksa erineva näitaja prognoosivõistlusele - aega kuni esmaspäevani oma numbrid kirja panna - link vastavale foorumile siin.

-

Globaalne arvutimüük on olnud tugev:

Global PC market leaps back to double-digit growth in the fourth quarter, led by a record quarter in the U.S., according to IDC

Led by a holiday season featuring price cuts of unprecedented duration, the U.S. PC market established a new record of nearly 20.7 million units shipped in the fourth quarter of 2009 (4Q09), resulting in year-on-year growth of 24%. Other regions also experienced solid growth, particularly emerging markets in Asia/Pacific and Latin America, leading the global market to 15.2% year-on-year growth for the quarter. According to IDC's Worldwide Quarterly PC Tracker, this marked the first quarter of double-digit volume growth since 3Q08. The fourth quarter results cap a strong second half of 2009, further cementing signs of a market revival and ending the year with year-on-year growth of 2.3%. In addition to the continuation of price declines throughout the year, other factors were in play for the fourth quarter. Following a stream of improving economic indicators which began in 3Q09, a release of pent-up demand was evident as buyers focused on a vast array of value-oriented notebooks that dominated the channel landscape in the holiday season. -

Ootustele vastavalt jättis ECB intressimäära 1.0% peale. Konverentsikõne, nagu erko juba kirjutas, toimub kell 15.30.

-

Ladenburg Thalmann initiates Bank of America (BAC), JP Morgan (JPM), and Wells Fargo (WFC) with Buy ratings. Firm says their positive view reflects their expectation that the worst of the financial crisis is past, and despite several overhanging challenges in 2010, the big banks have strengthened balance sheets, businesses and managements and are positioned to capitalize on profitable growth opportunities as they emerge. Firm expects positive momentum to be established soon and a return to normalized earnings on a run-rate basis should be achieved by 2012 (briefing).

Bank of America (BAC) sai meie poolt eile samuti ostusoovituse & pikemalt saab ettevõttega tutvuda Pro all.

-

Poole neljast algavat EKP pressikonverentsi on võimalik jälgida siit.

-

Detsembri jaemüük kehv:

December Retail Sales -0.3% vs +0.5% consensus, prior revised to +1.8% from +1.3%

December Retail Sales ex-auto -0.2% vs +0.3% consensus, prior revised to +1.9% from +1.2%

Siiani on räägitud, et jõulumüük ikka korralik olnud, kuid tundub, et kõrge tööpuudus, suur võlakoormus & külmad ilmad hoidsid kokkuvõttes detsembris tarbijaid poodidest veel eemal.

-

Esmased töötu abiraha taotlused vastavad suht ootustele, mis näitab, et ilmselt suuri erinevusi möödunud nädalal töökohtade loomises & kadumises ei olnud:

Initial Claims 444K vs 437K consensus, prior revised to 433K from 434K

Continuing Claims falls to 4.596 mln from 4.807 mln; 4.75 mln consensus

-

Fitch says U.S. retail credit card defaults hit near-record levels with no relief in sight

Päris huvitav statement Fitch poolt. -

Morgan Stanley kommenteerib väga positiivselt Oracle Corpi (ORCL) aktsiat & tõstab hinnasihi 29 dollari pealt 31 dollarile & lisab Oracle parimate ideed hulka:

Notable Callsis kolm katalüsaatorit välja toodud (loe pikemalt siit): 1) imminent closure on the Sun acq., whose benefits are being largely overlooked, 2) a return to organic growth in Oracle’s core as early as Q3, and 3) positive revisions. Morgan Stanley's FY11 EPS of $1.94 is well above cons. of $1.72, which does not reflect a) accretion from Sun, and strong execution should enable ORCL to meet/exceed its $0.15 target, and b) the level of improvement in the core bus. that they anticipate. With ORCL trading at 12X our CY11 EPS – a sub hardware multiple on software EPS and 25% below large-cap tech – they should see multiple expansion with accelerating growth and pos. revisions, driving the stock to firm's $31 PT based on 15x CY11 EPS of $2.09.

Oracle kaupleb eelturul +2.1% @ $25.27.

-

USA futuurid alustavad päeva kerges ca 0.2% kuni 0.3%lises miinuses.

Saksamaa DAX +0.48%

Prantsusmaa CAC 40 +0.32%

Inglismaa FTSE 100 +0.47%

Hispaania IBEX 35 -0.12%

Rootsi OMX 30 +0.41%

Venemaa MICEX +1.08%

Poola WIG -0.21%Aasia turud:

Jaapani Nikkei 225 +1.61%

Hongkongi Hang Seng -0.15%

Hiina Shanghai A (kodumaine) +1.35%

Hiina Shanghai B (välismaine) +1.12%

Lõuna-Korea Kosdaq +1.47%

Tai Set 50 +0.35%

India Sensex 30 +0.43% -

Here Come Earnings

By Rev Shark

RealMoney.com Contributor

1/14/2010 8:36 AM EST

Before everything else, getting ready is the secret to success.

-- Henry Ford

After eight days of trading, 2010 is looking much like 2009. We have had straight-up action on declining volume, aggressive dip-buying on very shallow pullbacks and quick recoveries just when it looked like we were ready to roll over. This very buoyant action on Wall Street in the face of a tepid economic recovery on Main Street confused many investors for much of 2009. Many are still confused by the strength of the market, but the sentiment polls now show that the pessimists have stopped fighting the trend and have largely capitulated.

In fact, the most worrisome thing about this market is the very high level of complacency. There is very little fear that the market is going to pull back, and that makes for very dangerous conditions as quarterly earnings start to roll out. Now is the time to become mentally prepared for earnings season.

The market acted well the last two quarters as earnings were reported, but the level of skepticism about the health of the economy was much higher six months ago. Investors were poorly positioned for strong earnings, and that's why we went almost straight up back in July when second-quarter earnings were reported.

We had a positive reaction again in November as third-quarter earnings were reported, but the pace of the advance has slowed. We continue to wedge slowly higher on declining volume and we still have days like Wednesday when the bears are run over by the frisky buyers, but after a tremendous rally over the last nine months, the action is becoming more mixed.

And that is the setup as Intel (INTC) and JPMorgan (JPM) kick off earnings season. Most of the important earnings reports will hit over the next two weeks, and they will determine the character of the market action. There have been few earnings warnings so far and the market seems to be quite optimistic that numbers will meet expectations, but we don't have much of a "wall of worry" to climb anymore and we're set up for a "sell the news" reaction.

Intel has really set the stage for earnings season the last two quarters and will probably do so again tonight when it reports. Back in July, Intel surprised the market with a very strong report and drove everything straight up. In October, Intel surprised the market once again and gapped up initially but then traded down for several weeks. We had a number of stocks that were sold on good earnings news, but the broad market shrugged off those responses and continued to act well.

We need to be ready for some very interesting action starting after the close today. This morning we have a little weakness on news reports that the Obama administration is ready to propose a "financial crisis responsibility fee" on some of the big banks. There are doubts that such a bill will pass the Senate, but it goes to show how politicians are pandering to populist anger about bonuses and the recent success on Wall Street.

Plenty of stocks are acting well and the bears still look quite toothless, but earnings season can be full of land mines -- stay extremely nimble and vigilant as the news is digested.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: WSM +4.0%, SAP +3.2%, CVM +3.2%, ICLK +2.6% (light volume)... Select European drug names showing strength: SNY +1.3%, AZN +1.2%, SHPGY +1.1%... Other news: LAB +43.9% (announces agreement to sell NYSE designated market maker; redemption of all its outstanding indebtedness; authorization of stock repurchase), BNVI +24.2% (Announces Publication of "Positive Results" From the Phase 1B Clinical Trial of Bezielle for Metastatic Breast Cancer), EAG +11.1% (receives $9.8 mln in TACOM orders for crew protection kits, spare parts and field services), SNSS +11.1% (announces publication of nonclinical Voreloxin data in leukemias; studies demonstrate Voreloxin acts synergistically with cytarabine and induces bone marrow aplasia), CPBY +8.8% (reports Q4 contracts of ~$36.73 million), ETRM +7.4% (announces weight loss, hypertension and diabetes data from EMPOWER and ENABLE studies), JRJC +6.0% (still checking), HNSN +5.5% (Hansen Medical, Luna and Intuitive Surgical entered into a series of transactions), RNWK +3.6% (RealNetworks' founder Rob Glaser steps down as CEO), ARST +3.3% (Cramer makes positive comments on MadMoney), SQM +2.1% (Cramer makes positive comments on MadMoney), ORCL +1.8% (up in sympathy with SAP), FMBI +1.5% (prices ~16.4 million shares of common stock at $11.00 per share), CPTS +1.2% (light volume; profiled in New America section of IBD), DPZ +1.2% (Cramer makes positive comments on MadMoney)... Analyst comments: TSN +2.2% (upgraded to Outperform at Credit Suisse), PPG +1.5% (upgraded to Buy from Hold at Citigroup), BWLD +1.5% (upgraded to Buy at MKM Partners), MT +0.9% (upgraded to Outperform at Exane BNP Paribas).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: SEED -6.0%, CPKI -5.8%, BGG -4.0% (light volume), SMSI -3.6%... M&A news: DDRX -0.8% (Green Mountain Coffee Roasters and Diedrich Coffee receive requests for additional information from FTC)... Select oil/gas related names showing weakness: AMX -3.0%, PTR -2.1%, PBR -1.4%, BP -1.3%, TOT -1.1%... Other news: ROSG -28.8% (to raise $5.1 mln in registered direct offering), ATBC -26.8% (thinly traded; unit discloses it consented to the issuance of a Consent Order), MED -13.3% (securities litigation law firm is investigating potential violations of the federal securities laws by Medifast), CTIC -9.0% (announces institutional investors purchase $30 mln of preferred stock and warrants), ZLC -8.7% (announced that Neal Goldberg, Chief Executive Officer and member of the Board of Directors, have left the co effective immediately), SHAW -7.4% (still checking), KYN -6.7% (announces 5.5 mln common share public offering), PKX -2.5% (Goverment in overdrive to launch Posco plant - Economic Times), FPL -1.9% (halts capital expenditures in Florida; Credit Suisse discusses a rate case gone bad for FPL; tgt lowered to $56), MON -1.7% (has voluntarily cooperated with regulators to address their questions about its business and the broader agriculture industry)... Analyst comments: NFLX -3.6% (downgraded to Sell from Hold at Lazard Capital), TOL -1.9% (downgraded to Equal Weight at Barclays), CREE -1.4% (downgraded to Hold at Morgan Joseph), PCS -1.3% (downgraded to Neutral from Outperform at Macquarie), SSL -0.4% (downgraded to Underweight from Overweight at HSBC). -

Jaemüügi kohta veel niipalju, et kuna 2008. aasta lõpus tegi jaemüük järsu kukkumise, siis on detsembri kasvunumbrid võrreldes eelmise aastaga ilusad (+5.4%) & siit otsib turg kohe ka lohutust:

-

AAPL put 210-le jaanuar

-

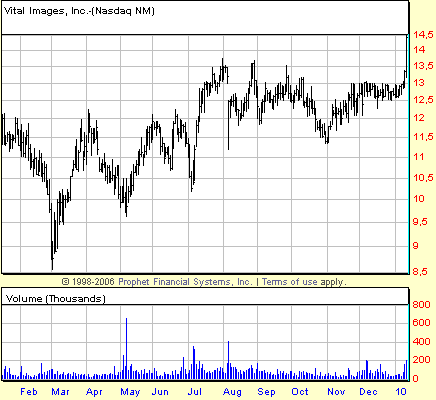

ktammin,

Küsisid eilses börsipäeva foorumis Vital Imagesi (VTAL) tõusu kohta, mis sai teisipäeva hilistel tundidel alguse ja jätkus terve eilse päeva. Põhjus selles peitub Craig-Hallumi poolt 12. jaanuari õhtutundidel antud ostusoovituses ja $18lises hinnasihis. Kuna ettevõtte osas pole just kuigi palju optimiste, on selline asi tõsiseks ostukatalüsaatoriks.

-

US unemployment rate will not drop below 8 pct until 2012, according to Congressional Budget Office - Reuters

-

Ettevõtete varud kasvasid novembris:

November Business Inventories +0.4% vs +0.3% consensus, prior revised to +0.4% from +0.2%

Ökonomistid ootavad, et varud jätkavad lähiajal kasvu, kuna ettevõtted on nõudluse kasvu osas optimistlikud.

-

CFTC'S Chilton says position limit proposals to err on the high side, according to Reuters insider

-

IMF head says world recovery stronger than expected, but fragile - DJ

-

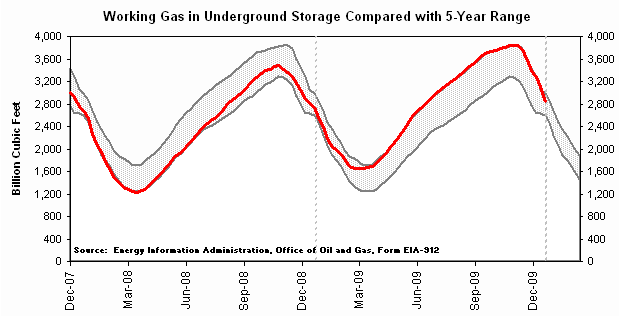

Natural gas inventory showed a draw of 266 bcf, analysts were expecting a draw of 260 bcf, with 20 ests ranging from a draw of 272 bcf to a draw of 195 bcf.

-

Varud vähenevad külmade ilmadega väga kiiresti ning täna avaldatud number viib näidu 5-aasta keskmisest vaid 4.4% kaugusele (ida-osariikides ollakse juba 5-aasta varude tasemel).

-

Economic adviser Volcker says US fiscal accounts "plainly overextended" - DJ

-

$13 bln 30-year Bond Auction Results- Yield: 4.64% (4.689% expected); Bid/Cover: 2.68x (10-auction avg 2.45x, prior 2.45x); Indirect Bidders: 40.7% (10-auction avg 42.6%, prior 40.5%)

-

CFTC unveils proposals to limit big energy traders - Reuters

Reuters reports the top U.S. futures market regulator moved on Thursday to limit the role of big traders in once high-flying energy markets, unveiling proposals to put a hard cap on the size of positions that dealers can hold but offering a limited exemption for big financial hedgers. The long awaited proposals, part of the Obama administration's push to overhaul financial markets, will apply to the four most-traded energy contracts on the two major exchanges. But it remains to be seen if the limits -- which it said would affect only the 10 biggest position holders if implemented today -- are sufficient to satisfy lawmakers who have clamored for regulatory action since oil prices surged to a record $147 in 2008. The Commodity Futures Trading Commission's proposals, subject to a 90-day period of public comment before approval, would give it the power to limit big trader positions based on a percentage of futures and options open interest across all contract months on both the New York Mercantile Exchangeand the IntercontinentalExchange . While more rigid, the limits did not appear strenuous compared to the exchange's own guidelines: A CFTC official said that if the rules were applied today, for example, the limit for NYMEX crude oil contracts across all months would be 98,100 contracts. The NYMEX's own so-called "accountability levels", which were frequently exceeded, is 20,000 contracts across all months. -

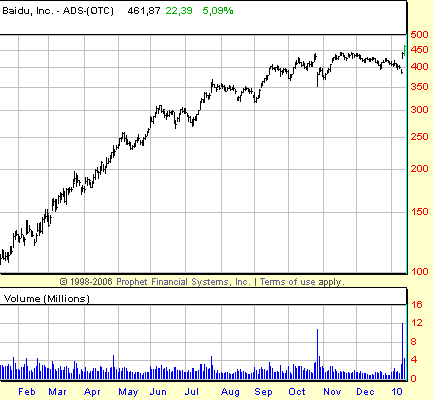

Baidu.com (BIDU) on teist päeva tugevas tõusus ning kahe päevaga on kokku tõustud juba ca $75 ehk 20%. Põhjuseks siis Google'i kahe päeva tagune teada võimalikust plaanist Hiinast lahkuda, millest kirjutasin siin (link) ja eilses börsipäevas.

-

HP Feb 45 puts are seeing interest ahead of earnings on Jan 28 before the open (volume: 1820, open int: 180, implied vol: ~43%, prev day implied vol: 41%)

-

Fed's Fisher, on CNBC, reiterates that there is a recovery underway, but its tepid

-

Deutsche Bank made comments regarding reports indicating Germany may cut solar subsidies by 16%-17% in April. The firm said, if true, the cuts would be significantly worse than expectations not only in size but also in timing.

TAN - -

Joel tõi välja Baidu tugevuse. Päris huvitav aga Google - kui teisipäeval sulges GOOG enne Hiina avaldust 590.28 dollari juures & tegi kolmapäeval esialgu kukkumise, siis hetkel on aktsia juba ca 592 dollari juurde liikunud.

-

Terra Industries (TRA) drops ~3 points in afterhours after CF withdraws offer .

-

Intelilt ilusad numbrid:

Intel prelim $0.40 vs $0.30 First Call consensus; revs $10.6 bln vs $10.17 bln First Call consensus

Intel sees Q1 revs $9.7-10.1 bln vs $9.35 bln First Call consensus;undefined$ mln -

Intel --CORRECTION-- Q1 revenues expected in the range of $9.3-10.1 bln

-

INTC konverentsikõne ajal vajuma hakanud ja hetkel künnab juba kergelt punast $21.40 tasemel.