Börsipäev 19. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Täna USAst mingeid olulisi makroandmeid ei tule. See-eest saame aga pilgud pöörata tulemuste ootustele, mille kajastamisel on traditsioniiliselt teist aastat juba abiks LHV Finantsportaalis avaldatav ja jooksvalt uuendatav tulemuste tabel - link siin.

Täna enne turgu teatavad oma tulemused Citigroup (C), Forest Labs (FRX) ja TD Ameritrade (AMTD). Pärast turu sulgemist näeme IBMi viimaseid numbreid.

-

Evans HSBC'st soovitab olla overweight USAs ja underweight Hiinas/Aasias. Põhjuseks negatiivne investorite meelestatus USA ja ülipositiivne meelestatus Aasia osas; ootus, et Föderaalreserv intressimäärasid ei tõsta (ei ole kunagi tõstnud, kui töötusmäär on üle 8%, hetkel on see 10%) ning samal ajal ootab, et Aasias hakkavad intressimäärad ülespoole liikuma (Hiina juba teinud samme selleks). Sektoritest eelistab Evans tarbimist, finantsi ja IT'd. Regioon, mis Evansile kõige vähem meeldib, on India.

Aasta esimese kahe kvartali jooksul ootab globaalset ca 10%list korrektsiooni aktsiaturgudel, kuid usub, et aasta lõpetatakse võrreldes aasta algusega ca 15% kõrgemal.

-

They came to Goldman Sachs’ oracle in search of wisdom and were told to buy lots of equities

Goldman picks energy, raw materials, industrials, household goods, cars and construction as its preferred sectors.

Forecasts for FTSE 100 at end of 2010:

Charles Stanley 4,700

Morgan Stanley 5,000

Brewin Dolphin 5,000-5,500

Seven Investment Management 5,500

S & P Equities 5,674

Hargreaves Lansdowne 5,750

Barclays Wealth 5,800

Killik & Co 5,850

Citigroup 6,000

The present level of the index is 5,494 -

Saaga Jaapani ühe suurima lennufirma ümber on läbi & Japan Airlines andis täna sisse pankrotiavalduse. Väljaspool finantssektori on tegu väidetavalt Jaapani suurima pankrotiga alates Teisest maailmasõjast (osad kasumilikud liinid jäävad küll tööle, kuid näiteks kaotatakse 15700 töökohta).

-

Mis selle Evans'i track record ka on? Ma võin ka öelda, et võiks olla overweight kreeka pankades ja ise ka veidi overweight, sest paksud poisid meeldivad naistele... ;)

-

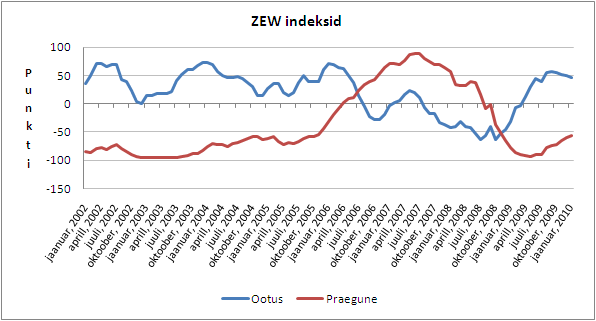

Saksa investorid ja analüütikud on riigi järgmise kuue kuu majanduskliima suhtes muutunud jaanuaris taaskord veidi negatiivsemaks. ZEW ootuste indeks langes 50.4 punktilt 47.2 punktile (neljandat kuud järjest), samal ajal kui Bloombergi küsitletud analüütikud olid numbriks oodanud 50. Ehkki jooksva olukorra hinnang paranes -60.6-lt punktilt -56.6 punktile, jäi seegi 0.4 punkti võrra oodatust nõrgemaks. Prognoositust negatiivsem statistika on kukutanud euro ennelõuna 1.44 tasemelt nüüdseks 1.4305 peale.

-

Karum6mm,

Nende track recorditega on nii, et neid on pea võimatu kvantitatiivselt määrata. Ainuüksi juba seetõttu, et neid prognoose tehakse väga palju ja muudetakse tihti. Kui öeldakse, et turud võivad jätkata tõusu, kuid ootame 10%list langust, mida kasutada ostmiseks... siis mis see call tegelikult on? Kui turud langevad, on call pihta läinud ja kui tõusevad, siis öeldakse ka, et ajutist langust ei tulnud, kuid kokkuvõttes me ju ootasimegi tõusu... Nii et nende track recorditega on väga keerulised lood.

Aga pigem lihtsalt tähtis see, et mees analüüsimaja aksiainvesteeringute strateegia koostamisel eesotsas ning hea olla kursis selliste meeste nägemustega (eks siis ka teab, kuidas on nad enda ja oma klientide raha paigutanud). -

Joel, mina klassifitseerin sellised sõnavõtud sell-side hülgemölaks, millel on paremal juhul hariduslik väärtus. Track-record'itegga on nii, et võib võtta konkreetse mehe buy ja sell soovitused ning paigutada need näiteks vastava aktsia graafikule. Ma garanteerin - huumorit saab rohkem kui rubla eest...

-

Siin graafikul strateegide aasta alguse S&P500 prognoos (keskmine) ja S&P tase aasta lõpus:

Allikas: Bloomberg

Näiteks eelmise aasta alguses ootasid strateegid, et S&P tõuseb 1078 punkti peale. 31.12.2009 oli SPX 1115, mis ei ole üldse halb tulemus. Totaalne ämber oli muidugi 2008 ja eks seda heidetakse veel mõnda aega neile ette. Reeglina tasub strateegide arvamusi rohkem kuulata tavalises kasvufaasis, kuna nende mudelid põhinevad osaliselt trendide ekstrapoleerimisel ja pöördepunkte märgatakse harva. Kui eeldada, et oleme uue kasvafaasi alguses, siis peaks analüütikute prognoosid nüüd täpsemad olema.

-

Ehk siis siit võib järeldada, et strateegid oskavad ainult ~1,1 koefitsendiga eelmise aasta sulgemisväärtusi läbi korrutada? :)

-

Impendium, see kõige riskivabam, sest isegi kui turg alla läheb, saab mingi ootamatu sündmusega seda põhjendada. Mulle tundub küll, et see 1,1 koefitsent on Wall Streeti teadlik poliitika sõltumata riskidest.

-

Folly of forecasting and useless data

Never invest on the basis of forecasts. As for analysts, he notes that the average forecasting error in the US analyst community between 2001 and 2006 was 47 per cent over 12 months and 93 per cent over 24 months. -

Kuskilt investeerimiskirjandusest (Swensen?) on jäänud meelde ka uurimus, et pankade analytic desk-id viivad kokkuvõttes way rohkem raha välja, kui sisse toovad.

-

See 9%-12%lise tõusu pakkumine on analüütiku jaoks nii-öelda kõige riskivabam ning seetõttu lähebki suurem osa just seda teed. Ajalugu on lihtsalt näidanud, et see on aktsiaturgude aasta keskmiseks tootluseks...

-

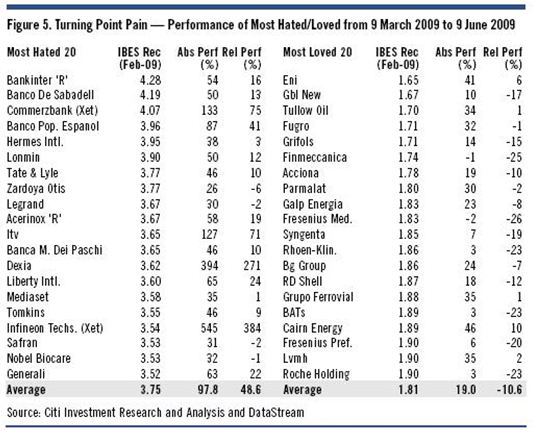

Citil on üks graafik, kus on välja toodud analüütikute enim armastatud & vihatud aktsiad märtsi põhjade juures:

Allikas: Citigroup

Seega strateegia põhja tabada puhtalt analüütikute soovituste järgi oleks kolme kuuga toonud 19% tootlust vs enim vihatud aktsiate 98% ralli :). Lühiajalise tootluse puhul tasub muidugi arvestada, et analüütikud ootavad sageli enne kvartalitulemused/ettevõtte prognoosid ära, et oleks numbrid, mille põhjal oma prognoose teha & mõningane viiteaeg on loomulik. Samuti öeldakse: A quality bias seems embedded in their DNA.

Aga Citi toonitamas sama asja, et sellel aastal tasub neid rohkem kuulata, kuna keskkond on muutunud:

We think that we have had our fair share of turning points for a while. Investors would have done well to ignore analysts in 2009. But, it could be dangerous to pursue a similar strategy into 2010.

-

Citigroup reports EPS in-line, misses on revs

Reports Q4 (Dec) loss of $7.6 bln or $0.33 per share, in-line with the First Call consensus of ($0.33). Losses were $1.4 bln or $0.06 per share excluding the repayment and exit of TARP. Citigroup fourth quarter revenues were $5.4 billion, or $15.5 billion excluding the loss on the repayment of TARP and exiting the loss-sharing agreement, compared to First Call consensus of $18.4 bln. Revenues were down from $20.4 billion in the prior quarter which included a $1.4 billion gain from the extinguishment of debt associated with the exchange offers. Tier 1 Capital Ratio is 11.7% and Tier 1 Common Ratio is 9.6%. Allowance for Loan Losses stands at $36.0 Billion, or 6.1%, the provision for loan losses in the fourth quarter was $8.2 billion, down 36% from the prior year and 10% from the prior quarter. Fourth quarter net credit losses of $7.1 billion were down $0.8 billion from the prior quarter, marking the second consecutive quarter of improvement. Fourth quarter managed revenues were $7.9 billion, or $17.9 billion excluding a $10.1 billion pre-tax loss associated with the TARP repayment and exiting the loss-sharing agreement. Citigroup fourth quarter consumer managed net credit losses were $8.9 billion, down 6% sequentially, driven by lower losses across most consumer lending portfolios, due in part to loss mitigation efforts. Total corporate net credit losses declined sequentially to $1.1 billion in the fourth quarter, from $1.5 billion, reflecting continued stabilization in corporate credit quality, and declines in the size of the portfolio.

-

Citigroup prelim ($0.33) vs ($0.33) First Call consensus

Citigroup says Net Credit Losses Lower for Second Consecutive Quarter -

Tulemustetabel nüüd hommikuste teatajatega uuendatud - link siin.

-

Saksamaa DAX -0.23%

Prantsusmaa CAC 40 -0.46%

Inglismaa FTSE 100 -0.24%

Hispaania IBEX 35 -0.03%

Rootsi OMX 30 -0.86%

Venemaa MICEX -1.09%

Poola WIG -0.22%Aasia turud:

Jaapani Nikkei 225 -0.83%

Hongkongi Hang Seng +1.02%

Hiina Shanghai A (kodumaine) +0.30%

Hiina Shanghai B (välismaine) -0.26%

Lõuna-Korea Kosdaq -0.72%

Tai Set 50 -1.55%

India Sensex 30 -0.88% -

Earnings and Elections Make for Tricky Trading

By Rev Shark

RealMoney.com Contributor

1/19/2010 8:43 AM EST

If "con" is the opposite of "pro," is Congress the opposite of progress?

-- Author unknown

We kicked off earnings season last week with some poor reactions to strong reports, but the bulls have plenty of opportunities to redeem themselves this week. It is still early in reporting season, but a theme often develops as market players have the same reflexive response as more news rolls out.

The weak action on Friday was our first real selling in a while, and it wasn't bad enough to do any real technical damage, but since it came on an exceptionally strong report from Intel (INTC) we have to be on guard. The S&P 500 is still above its first important technical support at 1130 and can dip even further without causing too much of a breakdown, but heightened vigilance is certainly necessary.

We have a very interesting twist at work this week which is the senatorial election in Massachusetts. The market usually has a mixed reaction to election results. Today's special election seems unusually important to the market for the simple reason that it will help create political gridlock if the Democrats no longer have a filibuster-proof majority of 60 seats. The market's preference now, especially with so many tax proposals being developed, is that the politicians be unable to pass anything. This isn't so much a preference for Republicans over Democrats but rather a desire that politicians be rendered powerless.

A number of folks believe that we will see a positive market reaction if Brown wins in Massachusetts tonight. Obviously the health reform will be put in jeopardy, which will help medical stocks, but also a tax on banks, a stock transaction tax and climate legislation will face much stiffer headwinds than they already do. The polls show that Brown is favored, and I'll be looking for the optimistic bulls to place some bets on his victory later in the day.

Even without the political drama, earnings season is always tricky as the mood can shift so quickly. This is already a market that seems to have a propensity to go from doom and gloom to euphoria in a matter of minutes, but the reaction to Intel and JPMorgan (JPM) is going to have market players thinking about selling more aggressively into good news. If Intel can't do better on that superb report, then how can we expect a stock that is just meeting expectations to perform well?

One positive I see is that a lot of charts look very interesting, especially after some profit-taking and consolidation. There is no question we have some extended technical setups, but a good shakeout would give us some promising setups.

We have a little weakness this morning on an in-line report form Citigroup (C) . We have IBM (IBM) and the election results tonight, which should keep us on our toes.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: OMN +5.1%, PH +3.0% ... M&A news: ADG +51.1% (announces definitive merger agreement with Chemring Group plc), CFL +32.1% (Tyco Int'l to acquire Broadview Security for $42.50/share in cash and stock), CBY +5.7% (Cadbury accepts Kraft offer - WSJ)... Select European drug names showing strength: GSK +1.5%, AZN +1.4%... Select metals/mining related names showing strength: BBL +1.8%, GOLD +1.3%, VALE +1.2%... Other news: NBS +19.9% (still checking), ENT +18.5% (approved the conversion of the Trust to a corporation), GNVC +14.9% (enters collaboration on hearing loss treatments with Novartis), BLDP +12.5% (Ballard Power, Dantherm, Danfoss invest to create fuel cell backup power systems capability), TGB +11.8% (continued strength from last Friday's ~15% jump), PFSW +11.1% (continued strength from last week's ~100% surge higher), MRNA +10.8% (demonstrates significantly reduced off-target activity for proprietary RNAi-based compounds), HLCS +7.1% (announces the sale of a Helicos(R) Genetic Analysis System to the Turku Centre for Biotechnology), CRDC +5.0% (Cardica's C-Port Flex-A Anastomosis System to be used for development of surgical robot in Japan), OSG +4.8% (mentioned positively in Barron's), CACA +4.5% (Chardan 2008 China Acquisition closes its business combination bith DAL Group and changes its name to DJSP Enterprises), ASPS +2.6% (Cramer makes positive comments on MadMoney), OSIS +2.0% (awarded ~$35 mln contract for installation of baggage handling and inline hold baggage inspection systems), NAT +1.5% (mentioned positively in Barron's), CB +1.3% (mentioned positively in Barron's)... Analyst comments: CIEN +6.6% (upgraded to Outperform from Neutral at Credit Suisse), SHFL +3.4% (upgraded to Buy at KeyBanc Capital Mkts), HT +2.8% (upgraded to Outperform at Baird), VECO +2.8% (added to Top Picks Live list at Citigroup), SXCI +1.9% (upgraded to Outperform from Mkt Perform at JMP Securities), SHPGY +1.6% (upgraded to Buy at Jefferies), LPX +1.5% (upgraded to Outperform from Sector Perform at RBC Capital), MCD +1.2% (upgraded MCD to Outperform at Credit Suisse).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: EDU -4.7%, FAST -4.1%, C -2.9%, PGN -1.8%, AVGO -1.3% (also registers to sell 25 mln shares of common stock for shareholders in an S-1 filing)... M&A news: KFT -2.8% (Cadbury accepts Kraft offer - WSJ)... Select financial names showing weakness: NBG -3.1%, GNW -2.9% (downgraded to Neutral at BofA/Merrill), UBS -2.3%, ING -2.1%, CS -2.0%, HBC -1.8% (downgraded to Underperform at Exane BNP Paribas), ... Select oil/gas stocks trading lower: STO -3.2% (downgraded to Hold at Collins Stewart), E -2.7%, BHI -1.8%, SLB -1.0%... Other news: RXII -9.9% (announces that new pre-clinical data using proprietary rxRNA compounds was presented at the Keystone Symposia's RNA Silencing), SAY -4.4% (Lax Indian rules still problem after Satyam fraud - AP), ABB -3.2% (still checking), PRGN -1.9% (files 9.2 mln share secondary, priced at $5.08 in an F-3 filing), BIDU -1.2% (announces that Chief Technology Officer Yinan Li has resigned for personal reasons)... Analyst comments: RDY -3.4% (downgraded to Sell at Deutsche), IMAX -3.2% (downgraded to Sell at Merriman), PWR -2.9% (downgraded to Underperform at FBR), JASO -2.9% (downgraded to Neutral at Broadpoint AmTech Research), S -2.6% (downgraded to Underperform at Bernstein), DAI -1.8% (downgraded to Neutral at Nomura), BKC -1.6% (downgraded to Neutral from Outperform at Credit Suisse), AKS -1.0% (downgraded to Hold at Deutsche). -

Seabreeze'i hedge fondi juht Doug Kass on RealMoney.com all kirjutamas, et ostab Citigroupi (C) tulemustejärgselt nii Citi (C) kui ka viimastel päevadel langenud Bank of America (BAC) aktsiaid.

-

US House Dem leader Hoyer says healthcare bill could pass US congress within 15 days; refuses to speculate on future of healthcare if Dems lose special election for Senate seat - Reuters

-

January NAHB Housing Index 15 vs 17 consensus, prior 16

-

IBM prelim $3.59 vs $3.47 First Call consensus; revs $27.2 mln vs $26.96 bln First Call consensus

IBM sees FY10 Earnings-per-share expectations of at least $11.00 vs 10.88 First Call consensus