Börsipäev 21. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Kõik eilsed tulemused ja aktsiate liikumised taas meie tulemuste tabelisse kantud - link on siin, hoidke silm peal.

USAst ootame täna Eesti aja järgi kell 15.30 esmaste töötu abiraha taotlejate numbrit (ootus 440 000, mis oleks võrreldes möödunud nädalaga veidi madalam), kestvate töötu abiraha taotlejate numbrit (ootus 4.6 miljonit ehk sama, mis eelmisel korral). Kell 17.00 avaldatakse detsembrikuu juhtivate indikaatorite muutus (ootus +0.7%. Mida suurem tõus, seda võimsamat majanduse taastumist indikeerib), Philadelphia jaanuarikuu Fedi äriväljavaadete küsitluselt oodatakse 18.8 punktilist näitu, mis oleks küll pisut vähem kui detsembris, kuid oluliselt rohkem võrreldes novembri, oktoobri, septembri ja augustiga.

-

Olles Ebay aktsiate omanik, huvitaks mind spetsialistide arvamus Ebay näitajate kohta.

Üllatas oodatava kasumiga aktsia kohta. Tuli 0.44 ja oodati 0.40.

Mulle tundub, et 2008 aasta alguses tehtud muudatused on ennast ära tasumas ja korvi on USA "muna" kõrvale tulemas järjest enam teisi "mune". Rahvusvaheline müük kasvab.

Samas on hoo uuesti sisse saanud kasutajate registreerumine.

Kulud on küll tõusnud ag atundub, et õigesse kohta - Marketingi. -

Eesti 2009. aasta kassapõhise aruande järgi siis riigi defitsiidiks 1.6 miljardit. See peaks siis protsentuaalselt tegema SKP'st ca 0.7%-0.8%, millele lisandub KOV'ide defitsiit. Pole paha.

-

Maailma aktsiaturgudele pakub tuge täna avaldatud Hiina 4Q09 SKP 10.7% kasv yoy - kuna edaspidi on eelmise aasta baas madal, siis peaks nüüd paar kvartalit väga ilusaid yoy numbreid Hiinast tulema (turul kasvavad sellega ka hirmud ülekuumenemisest, mistõttu Hiina börsid on ise raskustest ilusate numbrite peale tõusu jätkamisega). Pikemalt kajastame Hiinas toimuvat meie foorumis siin.

-

suhtlesin huvi pärast "kriisiinvestor" J. Hemptoniga, millal tema kogemuste kohaselt sellist mustast august ronivat turgu müüma hakata: "I have generally sold crisis stocks too early... but there are the odd country which relapses. You could buy Argentina on many crises - get the five times bounce and give it all back.

Made 10x on Indonesia and 5x on Korea - my best two. But lost 90 plus percent in Argentina on a relapse". -

ma nii lambist pakuks Venemaa siitkandist "odd country" potentsiaaliga ja meie ehk (loodetavasti) selline Tshiili sarnane come-back?

-

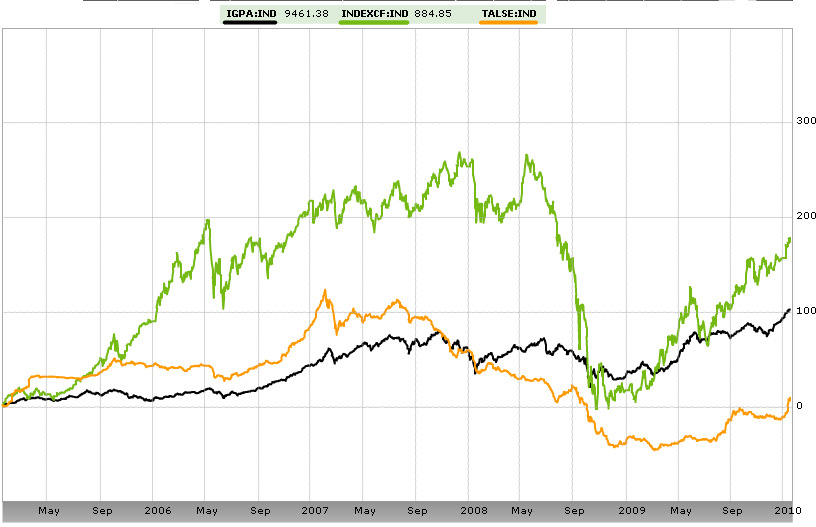

Võrdluseks ka Tšiili (must), Venemaa (roheline) ja Eesti (oranž) börside viimase viie aasta tootlused, mis näitavad samuti, mis skaalal Venemaa börs kõigub:

-

Goldman Sachs

-

Heidi Purga

-

Goldman Sachs prelim $8.20 vs $5.20 First Call consensus; revs $9.62 bln vs $9.65 bln First Call consensus

-

Palju Heidi Purga prelim?

-

Sõltub sellest, milliseid mõõte küsid Madis?

-

http://www.sloleht.ee/multimedia/blog/22a1d1c4-0959-416b-b90e-17fb5542c955.jpg

-

Joel, sain juba vastuse. Aitäh.

-

Initial Claims 482K vs 440K consensus, prior revised to 446K from 444K

Continuing Claims falls to 4.599 mln from 4.617 mln -

4. kvartali tulemuste tabel nüüd tänaste eelturu teatajatega täiendatud.

-

Saksamaa DAX +0.30%

Prantsusmaa CAC 40 +0.56%

Inglismaa FTSE 100 +0.29%

Hispaania IBEX 35 -0.11%

Rootsi OMX 30 +0.52%

Venemaa MICEX -0.39%

Poola WIG -0.68%Aasia turud:

Jaapani Nikkei 225 +1.22%

Hongkongi Hang Seng -1.99%

Hiina Shanghai A (kodumaine) +0.22%

Hiina Shanghai B (välismaine) +1.09%

Lõuna-Korea Kosdaq +0.90%

Tai Set 50 -2.03%

India Sensex 30 -2.42% -

H. Purga Best B4 Over?

-

Dealing With the Headwinds

By Rev Shark

RealMoney.com Contributor

1/21/2010 8:06 AM EST

Excess generally causes reaction, and produces a change in the opposite direction, whether it be in the seasons, or in individuals, or in governments.

-- Plato

The fourth-quarter earnings reports we have seen so far have been quite positive, but the market reaction has been quite poor. We had a sharp jump on Tuesday, but that was driven by speculation over the Massachusetts election rather than earnings reports. Good news from the likes of Intel (INTC) and IBM (IBM) have been sold and the broad market indices have been under pressure. We have had better action in the financials as they have reported, but it's mainly smaller regional banks that are acting the best.

The Obama administration's primary response to the shocking election loss in Massachusetts has been to shift the focus of debate to banks and Wall Street. A set of proposals that will restrict the size of banks and put limits on trading is expected. Bank of America (BAC) , Wells Fargo (WFC) , JPMorgan (JPM) , Morgan Stanley (MS) , Citigroup (C) and Goldman Sachs (GS) are all expected to be affected by the new rules.

There are some very good arguments for these rules, but my concern is that the anti-Wall Street efforts will spill over and hurt market players who were victims rather than perpetrators of the reckless excesses that helped cause many or our economic problems. The financial industry is such an easy target for politicians that chances of collateral damage are quite high.

We are very likely to see anti-Wall Street rhetoric build. So far it has not had any negative impact on market action, but the fact that the market has acted so well for so long just makes it a better target for politicians who want to fan the flames of class warfare.

Of more immediate concern is earnings season. We have Goldman coming up this morning and then Google (GOOG) tonight. It is going to be very interesting to see if these stocks, which have been struggling a bit lately, suffer from a "sell the news" reaction like Intel and IBM saw. Both of those stocks were very strong into their reports so the setup is quite different.

The reaction to these key reports is extremely important because the overall technical picture is starting to show some cracks. We are still just barely off recent highs, but we have seen some distribution as we have sold off on higher volume. We bounced back late in the day on Wednesday, which helped, but the selling squalls have been more intense than we have seen in a while.

We still have not suffered any really notable breakdowns, but there is an absence of any strong market leadership. China stocks, which were the hottest momentum sector for a while, have slowed considerably on news of attempts by the Chinese central banks to cool things off. Other hot groups like solar energy and bulk shipping have cooled off as well.

The dollar has rallied to its highest levels since early September, and that is putting considerable pressure on oil, gold, steel and commodity sectors that led us for much of the last three months.

Technology stocks have had some good earnings reports, but they have not been able to gain any notable upside traction. Financials have had the best performance lately but they aren't exactly flying.

We'll see how it goes as earnings reports come out. The news has been pretty good but the reactions haven't been. If that theme continues, we will need to boost our defensive efforts.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: STX +12.6%, EBAY +8.0%, FCS +6.9%, PLXS +6.8% (also upgraded to Buy at Needham), FITB +6.6%, EL +6.1%, PNRA +4.4%, KEY +4.3%, FFIV +4.0% (also upgraded to Buy at BofA/Merrill), DOX +3.8% (also upgraded to Buy at BofA/Merrill), UNH +3.6% (light volume), SBUX +3.5% (also upgraded to Buy at Deutsche), XRX +3.3%, NITE +2.8%, CAL +2.8%, LUV +2.4%, GS +1.0%... Other news: STKL +15.5% (signs contract with major ethanol producer in China), WDC +3.9% and SNDK +2.5% (trading up in sympathy with STX), AUXL +3.2% (Auxilium Pharma and Pfizer announce Commencement of European Regulatory Review of XIAFLEXTM for the Treatment of Dupuytren's Contractur), STEC +2.5% (rebounding from yesterday's 10%+drop), SCHW +1.5% (prices 26.316 mln common share offering at $19.00/share), APC +1.4% (announces the Tweneboa-2 appraisal well, offshore Ghana, encountered more than 105 feet of net pay in stacked reservoir sands), ORCL +1.0% (European Commission unconditionally approves Oracle's acquisition of Sun)... Analyst comments: AAI +2.6% (upgraded to Buy from Sell at Argus),PPO +2.4% (upgraded to Outperform from Market Perform at William Blair), CL +1.8% (added to Conviction Buy List at Goldman), SYMC +1.0% (upgraded to Outperform from Neutral at Macquarie).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: BBI -31.5% (also downgraded to Neutral at Janney), TSS -14.2%, LM -6.6%, SVA -4.5% (also announces offering of 8,650,000 Common Shares), SWKS -3.5%, WGOV -2.2% (light volume), KMP -1.5% (light volume), FCX -1.0%... Select financials showing weakness: RBS -4.0%, BCS -3.9%, NBG -3.2% (Greece not seeking aid to plug debt hole - AP), STD -2.5%, LYG -2.4%, RY -1.7%, DB -1.0%... Select metals/mining names trading lower: RTP -4.1%, SLW -2.2%, GFI -2.2%, BBL -1.8%, MT -1.8%, BHP -1.7%, GOLD -1.5%, AUY -1.3%, AU -1.1%, SLV -0.9%... Other news: ISPH -20.0% (announces results of phase 3 PROLACRIA trial for dry eye), CAMP -7.9% (files for ~2.4 mln share common stock offering by selling stockholders), GRMN -5.9% (Nokia releases new version of Ovi Maps for smartphones at no extra cost), AMAG -1.0% (prices 3.6 mln common shares at $48.25/share)... Analyst comments: PCX -3.6% (downgraded to Sell at Citigroup), MEE -3.0% (downgraded to Sell at Citigroup), CNX -2.5% (downgraded to Hold at Citigroup), ACI -2.4% (downgraded to Sell at Citigroup), MET -2.3% (downgraded to Neutral from Buy at BofA/Merrill), PRU -1.3% (downgraded to Hold from Buy at Citigroup), BSX -1.2% (downgraded to Market Perform from Outperform at Bernstein), MS -0.8% (downgraded to Mkt Perform at Keefe, Bruyette). -

Barclays, Lloyds may need 25 billion pounds to bolster capital - Bloomberg.com

-

January Philadelphia Fed 15.2 vs 18.0 consensus, December 22.5

December Leading Indicators +1.1% vs +0.7% consensus, prior revised to +1.0% from +0.9%

Piladelphia Fedi äriväljavaadete küsitluse oodatust nõrgemaid tulemusi võib seostada viimase tunni aja nõrkusega.

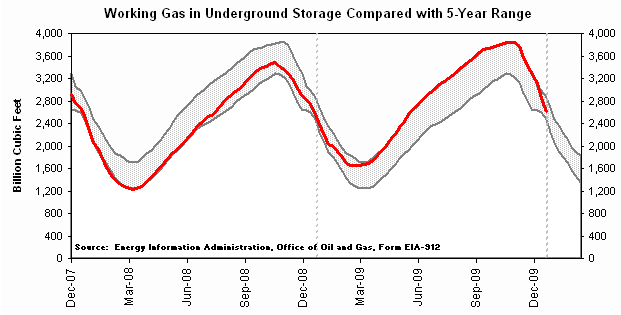

Maagaasivarud jätkavad külma talve, madala pakkumise ja taastuva tööstusnõudluse tõttu kiiret vähenemist:

Natural gas inventory showed a draw of 245 bcf, analysts were expecting a draw of 230 bcf, with ests ranging from a draw of 255 bcf to a draw of 198 bcf. -

Panen siia taaskord graafiku maagaasivarude kohta, kus punane joon näitab praeguseid varusid ning hall vahemik 5 aasta miinimum ja maksimumvarusid. Viimase nädala varude vähenemine tõi praegused varud viimase 5 aasta keskmise võrdluses juba 0.2% keskmisest allapoole. Suured ülejäägid varudes on likvideeritud väga lühikese ajaga. Suurema gaasitarbimisega ida-osariikides on praegused varud keskmisest juba 3.8% allpool.

-

kui nüüd SP-l 1120 läbitakse peaks mõtlema hakama

-

ja kirjavigade pärast ei nori, kogemata :)

-

Nasdaqi töus siis aasta algusega 0 protsenti, vörreldes Tallinna börsi 33 prontsendi körval jookseb mul juhe kokku.

-

Obama pani korraliku pommi. Osad treiderid arvavad, et see on ka turu viimase aja nõrkuse põhjus.

Obama proposes to limit bank proprietary trading

Pangad saavad kõige rohkem pihta, kuid siin on üks artikkel, mile kohaselt Goldman Sachsi see uudis ei pruugigi puudutada: http://ftalphaville.ft.com/blog/2010/01/21/131501/whither-goldmans-prop-desk/ -

btw, alates tänasest on minu seisukoht, et Obama on tropp.

-

Bank of America ka suht tugevas languses, hmm. Jama

See Obama trikk ilmselt annab veel pikemat aega valusalt tunda, ei tea peaks positsiooni likvideerima. Kasum ja kahjum null, a ikkagi see raha oleks teenind Tallinnas head kasumit. Närvi ajab see Obama -

US Pay Czar Kenneth Feinberg says has about 45 days to determine if he will exercise his authority to claw back pay at any company that had received TARP funds - Reuters

-

PTEC + 18 ?? millest selline liikumine?

-

White House says Obama bank plans not returning to Glass-Steagall - Reuters

-

Goldman Sachs: Hearing defended at Rochedale (Bove)

-

Mis mõttes Obama tropp on?

Jahutud ju küll, et midagi tuleb ette võtta ja nurisetud, et selles suunas on tehtud vähe tööd. Nüüd, kus hakatakse liigutama, on kõik jama?

Pangad keetsid selle supi kokku, mis toimus. Ju on märkke, et keedetakse riigi rahadega uut kisselli, mida keegi hiljem ära ei jõua süüa.

Poliitik peab rahvale näitama, et pangad lihtsalt ei pääse. -

stocker, vaata mida Buffett näiteks täna arvas: http://www.cnbc.com/id/34953353

Kõik pangad ei põhjustanud seda jama, kuid TARP raha sunniti kõik võtma. Nüüd karistatakse neid selle eest, et TARP raha võtsid.

btw, müüsin täna BAC ja C ja ostsin GS juurde. -

kas tuleb karupüksid välja otsida...

-

No jah, kui Merrill-i ülevõtmist BofA poolt mõtled, siis küll, kuid huvitav, mille eest siis need suured kingad hiljuti rahvast tänasid, et nende sektor päästeti.

Too big to fail oli aasta tagasi põhi jutt ja nüüd tuleb välja, et tegelikult ei olnud? -

Rep Barney Frank, on CNBC, says he would support these changes with a long term time frame

-

NY Fed pushing banks to clear more buyside swaps, sources say - DJ

-

Google prelim $6.79 vs $6.50 First Call consensus; revs $4.95 bln vs $4.92 bln First Call consensus

-

American Express prelim $0.59 vs $0.57 First Call consensus; revs $6.5 bln vs $6.14 bln First Call consensus