Börsipäev 1. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

USAst on täna tulemas mitmeid makroandmeid. Kell 15.30 teatatakse kestvate töötu abiraha taotlejate annualiseeritud number (ootus 4.62 miljonit) ning esmaste töötu abiraha taotlejate annualiseeritud number (ootus 440 000). Tööjõuturu tervise hindamisel oleks oluline, et need oleksid võimalikult väikesed. Kell 17.00 teatatakse veebruarikuu ehituskulutuste muutus, kust oodatakse 1%list kulutuste langust. Samuti tuleb veel märtsikuu ISM indeks, millelt oodatakes võrreldes veebruariga marginaalset tõusu ning liikumist 56.5 pealt 57.0ni.

-

Bloomberg on teinud loo sellest, kuidas USA kohtumaja treppidel peetavad sundmüügi oksjonid on iga päevaga üha rohkem pakkujaid juurde saamas. Kui aasta tagasi oli neil treppidel oksjonist osavõtjaid vähem kui seal magavaid joodikuid ja kerjuseid, siis nüüd on oksjonitel osalejaid juba palju rohkem. Link Bloombergi loole siin.

-

Siin GSi peaökonomisti Jim O'Neilli arvamus Hiina majandusest.

"Speak to anyone involved at any level of the consumer business, whether it be Tesco, Walmart or Louis Vuitton, and their evidence backs up the data. Chinese consumption is probably growing at about 15 per cent, similar to a 2-3 per cent rate for the US consumer."

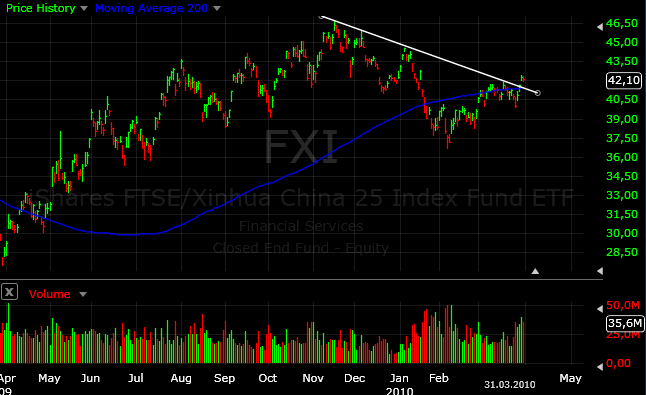

Nagu O'Neill ütles oma artiklis, siis on selge, et praegune sisetarbimise kasv Hiinas ei ole jätkusuutlik. Ülekuumenemise spekulatsioonid tõid aasta alguses järsult allapoole ka tuntud Hiina börsil kaubeldava fondi FXI. Viimastel päevadel on FXI aga langevast trendist jagu saanud ja liikunud 200päeva libisevast keskmisest taas ülespoole:

Kuna Hiina yoy kasvunumbrid aeglustuvad kindlasti aasta teises pooles, siis ootavad paljud analüütikud, et seda tõlgendatakse ülekuumenemisriskide vähenemisena, mis on aktsiaturgudel positiivne. Siin nt MSi värske arvamus:

What’s next: We think the stock market could break out in 2H 2010 with two potential catalysts: 1) as inflation starts to fall, tightening concerns will ease and growth will take better shape at the same time, potentially re-rating the market; 2) Rmb could start appreciating against the US$ early in 2H 2010, with a marginal revaluation of the currency, which could attract more liquidity into Hong Kong-listed China stocks.

Kindlasti siin suur risk, et Hiina keerab kraanid liiga palju kinni ja koos stiimulite lõppemisega lääneriikides võib majandus liigselt jahtuda.

-

Hirmutati, et 1. aprillist kaotavad senised paroolid kehtivuse, aga ikka sain sisse. Ju siis oli aprillinali.

-

Vanaema, see ei ole aprillinali, vaid pikendati kuni 5. aprillini.

https://www.lhv.ee/news/index.cfm?id=1205568 -

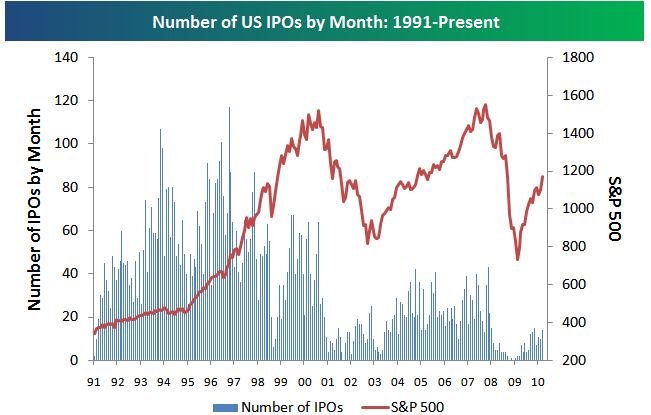

Bloomberg kirjutab, et Euroopa IPO turg on hoogu sisse saamas. Kui eelmisel aastal väljastati esmakordselt aktsiaid kõigest 10 miljardi dollari eest, siis sellel aastal ollakse juba pärast esimest kvartalit sellele numbrile lähedal. Siiani on pooled selle aasta IPOdest indeksite tootlusele siiski allapoole jäänud.

Eile tõi Bespoke välja, et ka USA börsidel on üha rohkem IPOsid näha, kuid võrreldes eelmiste börsirallidega on siiani IPOsid üllatavalt vähe olnud:

-

Täna jäi Bloombergist silma veel üks lugu, kus on positiivses võtmes kirjutatud elektriautodele akusid tootvast Polypore Internationalist (PPO). Kellele teema huvi pakub, siis soovitan seda linki lugeda.

-

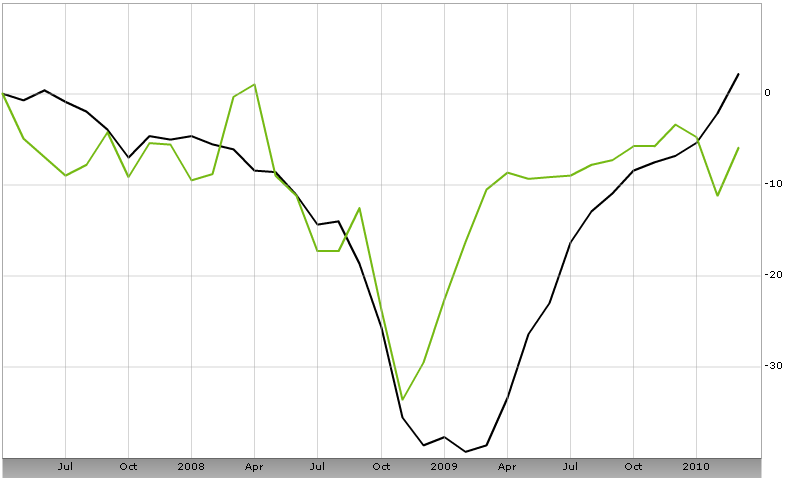

Märtsi PMIid Aasias ja Euroopas viitavad jätkuvalt V-kujulisele tööstustegevuse taastumisele (erand nt Kreeka, kus PMI viimase 11. kuu põhjades):

Euroala (must) ja Hiina PMI (roheline)

Allikas: Bloomberg

-

Eile pärast turgu kehvade tulemustega tulnud Research in Motion (RIMM) saab Goldman Sachsilt varasema "neutraalse" soovituse asemel "müü" soovituse.

Research In Motion was cut to sell from neutral by Goldman Sachs, which said its products will increasingly lose differentiation as the focus shifts from email, where RIM leads all competitors, to applications, where RIM lags both the iPhone from Apple and Android, an operating system of Google. With its North American business already in decline, the broker doesn't expect international strength to be enough of an offset. (allikas: marketwatch)

-

Esmased töötu abiraha taotlused langesid nädalaga 6000 võrra, mis vastas enamvähem ootustele:

Initial Claims 439K vs 440K consensus, prior revised to 445K from 442K

Continuing Claims falls to 4.662 mln from 4.668 mln

-

Turud nii Aasias, Euroopas kui ka USAs näevad 2010. aasta 2. kvartali esimesel kauplemispäeval välja väga rohelised. S&P500 indeksi futuur on kerkinud +0.6%, Nasdaq100 futuur +0.4% ning naftahind kogunisti +1.2% ning jõudnud tasemele $84.8 barrelist.

Euroopa turud:

Saksamaa DAX +1.16%

Prantsusmaa CAC 40 +1.39%

Inglismaa FTSE 100 +0.89%

Hispaania IBEX 35 +1.26%

Rootsi OMX 30 +1.55%

Venemaa MICEX +1.84%

Poola WIG +1.28%Aasia turud:

Jaapani Nikkei 225 +1.39%

Hong Kongi Hang Seng +1.40%

Hiina Shanghai A (kodumaine) +1.23%

Hiina Shanghai B (välismaine) +1.88%

Lõuna-Korea Kosdaq +0.67%

Tai Set 50 +1.88%

India Sensex 30 +0.94% -

New Quarter -- Same as the Old Quarter

By Rev Shark

RealMoney.com Contributor

4/1/2010 8:40 AM EDT

It is not the mountain we conquer, but ourselves.

-- Edmund Hillary

The first quarter of 2010 is now in the books, and it looked very much like most of 2009. The bulls weren't only victorious, they crushed the doubters and skeptics. The bulls pulled off yet another dramatic "V"-shaped bounce to new highs for the quarter.

At the end of January, it looked like a long-awaited correction was upon us, but just when we were on the brink of gaining some downside momentum, the buyers stepped up and drove us straight back up to new highs. There have been almost no pullbacks during the seven-week rally off the early-February lows, and even the bulls have become frustrated with the lack of buying opportunities recently.

Like many others, I was very surprised how easily the bulls drove this market back up. The sellers have been rendered inconsequential, and the worst thing you could do is try to fight this trend.

The most confusing thing about this market is the lack of any strong emotions. While there doesn't seem to be any worry or fear, there hasn't been much euphoria or wild greed either. We seem to have enough skepticism to keep climbing a wall of worry but not enough worry to produce any real pullbacks.

Riding an uptrend is usually much easier than it has been recently. The lack of volatility and consolidations and the perpetually overbought technical conditions make entries extremely difficult. The only way to put substantial capital to work is to chase stocks higher, and that simply isn't a viable methodology for many traders or investors.

If there is a lesson to be learned or reinforced this past quarter, it's that trends tend to last longer and go further than seems reasonable. I doubt that even the most bullish of bulls expected this market to be so completely one-sided. The key to navigating this market has been to respect the trend and to not keep trying to anticipate when it will end. That isn't easy to do when we have such consistently positive action and are struggling to put capital to work, but the market never wants to make it too easy for us.

We are kicking of the second quarter with another positive start. Economic reports from China and the eurozone were positive and all major overseas markets are in the green. Research In Motion's (RIMM) mediocre earnings report and a downgrade by Goldman is staying contained, and oil and commodities are leading us up in the early going.

It is going to be very light trading today and we have the big employment report tomorrow when we are closed, so market players may hold off on making any major bets. Weekly unemployment numbers are very close to expectations, and we have ticked down just slightly on the news.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: XRTX +14.6%, CNAM +9.2%, SPIR +6.9% (light volume), RYAAY +6.4%, AEHR +6.3%, PEIX +6.3% (light volume), KNDI +4.9% (light volume), MU +4.6%, KMX +2.6%, GPN +1.6% (also upgraded to Outperform from Market Perform at Barrington), SPU +1.2%... M&A news: NGA +34.4% (AZZ signs agreement to acquire North American Galvanizing & Coatings for $7.50/share in cash), LIHR +28.3% (rejects A$9.2 bln offer from NEM - Bloomberg), SKIL +4.2% (announces agreement on terms of a revised recommended acquisition for cash by private investor group)... Select financial related names showing strength: PUK +3.1%, ING +2.4%, LYG +2.3%, BCS +2.1%, UBS +2.0%... Select metals/mining stocks trading higher: RTP +4.0%, BBL +3.0%, BHP +2.5%, VALE +2.2%, GOLD +2.0%, GDX +1.1%, GLD +0.4%... Select casino related names trading higher: MGM +2.1%, LVS +1.6%... Other news: BGP +33.7% (Borders announces $700 mln revolving credit facility and $90 mln term loan; BGP meets $42.5 mln obligation), RDEA +9.5% (announces positive top-line results from a Phase 2b Study of RDEA594 given as monotherapy in the treatment of hyperuricemia in gout patients), TRMA +7.3% (entered into the Second Waiver to Amended and Restated Credit Agreement), LNG +6.8% (Cheniere Energy confirms J.P. Morgan and Cheniere Energy partnership in LNG market), AMAG +3.1% (AMAG Pharma and Takeda Pharma announce collaboration for Feraheme in all therapeutic indications in select ex-US territories, including Europe), RMBS +1.3% (Advanced Micro renews patent license agreement with Rambus), TOT +0.9% (announces second oil discovery on deep offshore block 17/06 in Angola), SNY +0.9% (settles 3 lawsuits over Eloxatin - AP)... Analyst comments: AIXG +2.7% (initiated with a Buy at UBS), MICC +1.9% (upgraded to Overweight from Neutral at JP Morgan), BEN +1.8% (upgraded to Buy from Hold at Citigroup), AB +1.2% (upgraded to Buy from Hold at Citigroup), BIDU +0.7% (Baidu target raised to $752 from $604 at Deutsche Bank),

Allapoole avanevad:

In reaction to disappointing earnings/guidance: NCOC -23.2% GRRF -21.6% , EFJI -8.5% , RINO -7.3% , RIMM -5.5% (also downgraded to Sell from Neutral at Goldman), MOS -1.8%... Other news: IDI -21.4% (intends to file a Form 12b-25 with the SEC on April 1, 2010, to delay the filing of its Annual Report on Form 10-K for the year ended December 31, 2009), IRE -5.6% (still checking for anything specific), CIM -5.1% (announced an 85 mln share common stock offering), NRP -4.7% (announces pricing of public offering of common units at $25.17/share), QKLS -4.7% (postpones earnings release date for fourth quarter and full year 2009 financial results), BRE -3.2% (announces offering of five mln shares of common stock)... Analyst comments: BLK -2.6% (downgraded to Hold from Buy at Deutsche Bank and downgraded to Sell from Buy at Citigroup). -

JPMorgan, kes erinevalt paljudest teistest analüüsimajadest ei tundnud isegi veebruari korrektsiooni ees mingit hirmu, on nüüd muutunud veelgi optimistlikumaks ning usub, et majandus suudab peagi edasi kasvada iseseisvalt. Aktsiaturgudel prognoositakse tugevuse jätkumist:

We are becoming more bullish on economic growth, both in terms of how fast economies will grow and in terms of confidence that it will actually happen. Activity data across much of the world have surprised on the upside in recent weeks. Most important is that they

are showing greater breadth across regions, sectors, and types of spending. The equity rally should extend into next month, on stronger economic data and the start of the 1Q reporting season, from which we expect good news. The 4Q US reporting season posted a 7% upside surprise: The final operating S&P 500 EPS was 7% above the expectation at the start of the reporting season. Quarterly earnings surprises tend to exhibit strong serial correlation, repeating 82% of the time. This points to another positive surprise in the 1Q reporting season. -

Turgudel korralik ralli käimas ning S&P500 on liikunud kõrgeimate tasemete juurde alates 2008. aasta septembri keskpaigast ehk viimase 18.5 kuu tippude juures.

-

Las Vegas Sands: Hearing UBS saying Macau March revenue growth came in below expectations

-

Märtsi tööstussektori ISM suurim alates 2004. aasta juulist:

March ISM Manufacturing 59.6 vs 57.0, February 56.5

-

February Construction Spending M/M -1.3% vs -1.0% consensus, prior revised to -1.4% from -0.6%

-

Goldman Sachs says lowers March US payrolls forecast to 200,000 gain from 275,000 gain - Reuters

-

Maagaasivarud kasvasid möödunud nädalal 12 bcfi võrra, mida oli võrreldes ootustega (19 bcf) siiski vähem.

Maagaasihind on uudise peale üle 5% plussi tõusnud. -

Bloombergi andmetel kasvas GM-i märtsi sesoonselt korrigeeritud müük ainult +15.9% vs. +25% konsensuse ootused.

-

Fed pidi lõpuks siiski tunnistama, et ka talle kehtivad USA seadused: Fed avalikustas Maiden Lane LLC sisu peale pikaleveninud vägikaikavedu Bloombergiga FOIA üle. Tuleb välja, et Maiden Lane'i portfell koosneb suuresti rämpsust... what a surprise? Täpsemalt saab lugeda siin: Fed Reveals Bear Stearns Assets It Swallowed in Firm’s Rescue. Kuna tegu on megasuure looga, siis ilmselt on see lähipäevil peamine jututeema.

-

Apr. 01 (Bloomberger) -- U.S. stock-index futures soared 6%, as the Federal Reserve boosted the discount rate it charges on loans to banks after the close of exchanges in New York.