Börsipäev 19. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

Reedene kauplemispäev oli tavapärasest huvitavam ning närvilisus, mis tabas pangandussektori aktsiate liikumist pärast teadet, et USA Finantsinspektsioon SEC on leidnud Goldman Sachsi tegevuses subprime kriisi ajal ebakohaseid tegusid, ei olnud nähtud juba üle aasta aja. Goldman Sachsi (GS) aktsia liikumine ja üle 10%line päevane kukkumine meenutas juba 2008. aasta sügisesi aegu. Seega kindlasti tuleb tänagi põnev päev ning Goldman Sachsiga seotud uudistel ja liikumistel tasuks silma peal hoida.

Makroandmetest on täna kell 17.00 oodata üksnes märtsikuu juhtivate indikaatorite muutust, kus ootuseks on +1.0%. Hommikune eelturg USAs on igaljuhul punane ning S&P500 indeksi futuurid on kukkunud praeguseks hetkes 0.45% ja Nasdaq100 futuurid 0.35%. Nafta on langenud 1.8% ja kaupleb $81.8 pealt barrelist. -

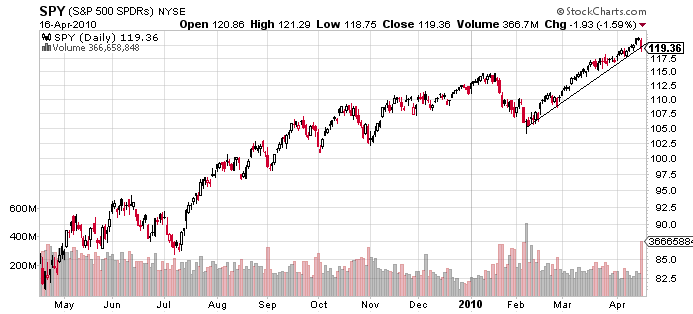

Kui S&P500 indeksi reedese kukkumise järel sai veel öelda, et lühiajaline tõusutrend jäi murdmata, siis kui futuuride poolt indikeeritud langus ka regulaarkauplemise alguseni välja kestab, on see tõusutrendi joone säilimine juba tõsise kahtluse all.

Goldman Sachsi aktsiagraafikut vaadates ei saa tõusutrendist enam aga rääkida. Küll tasub aga vaadata, kuidas reageeritakse nädalavahetusel tulnud teadetele, et erinevad organisatsioonid, asutused ja kogunisti riigid on SECi poolt Goldman Sachsile esitatud süüdistuste vastu kõrgendatud huvi tundnud. Link ühele sellisele Bloombergi loole on siin.

-

Aasias tegid täna suurima kukkumise Hiina börsid (ca -5%), kuna valitsus tutvustas üsna karme meetmeid, et peatada spekuleerimine kinnisvarasektoris:

China told banks to stop loans for third-home purchases in cities with excessive property price gains and suspend lending to non-residents without tax returns or proof of social security contributions in that city, according to a statement by the State Council on April 17. Local governments may also limit the number of units that can be bought, according to the statement. (bloomberg)

Kohaliku meedia sõnul oli juba täna uudise peale näha kinnisvarasektoris paanilist müüki ja enim mullistunud linnades ei välistata ca 10% korrektsiooni. Siin nt. Morgan Stanley seisukoht, et Hiina kinnisvaraturg on selgelt mullistunud & õhku on vaja välja lasta:

According to our own estimates, the average house price to per capita annual income is 29 times as of December 2009. Assuming two working people are buying one apartment together, using the maximum leverage (80% mortgage), at the most preferential interest rate (4.16%), for the longest borrowing period (30 years), this still translates into ~45% of their gross monthly income dedicated to the mortgage payment. This is clearly too high a ratio, especially when compared to the US’s ~40% at its property bubble peak before 2008.

-

IMF peaks käesoleval nädalal avalikustama järjekordse globaalse majandusraporti ning juba mitmed ajalehed teavad kirjutada, et selle raames kavatsetakse maailma kasvuprognoosi tõsta jaanuari 3.9%-lt 4.1%-le. 2011.a oodatakse väidetavalt kasvu kiirenemist 4.3%le. Ülespoole võidakse korrigeerida arenevate turgude ja USA majanduskasvu, allapoole aga Saksamaa ja kogu eurotsooni ootusi. Kaks artiklit sellel teemal siin ja siin

-

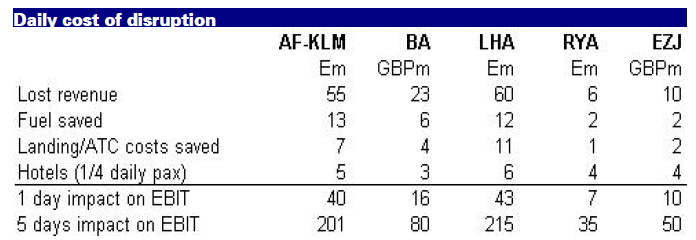

Euroopas on viiendat päeva suletud mitmed lennujaamad ja lennufirmade aktsiad jätkavad kukkumist. Deutsche Banki hinnangul elavad lennufirmad erakordse müügitulude languse siiski üle ja nõrkust sektoris peaks kasutama ostmiseks:

Today is the fifth day that European airspace will be closed. Even after the terrorist attracks of September 11th 2001, US airspace was closed for just two days before limited services resumed. However, this is not as bad as 9/11 which depressed air travel demand for six months. We do expect share prices for European airlines to fall sharply today but we would recommend buying on weakness. Air travel will rebound sharply once airspace restrictions are lifted.

-

mis võiksid atraktiivsemad lennufirmad hetkel olla?

-

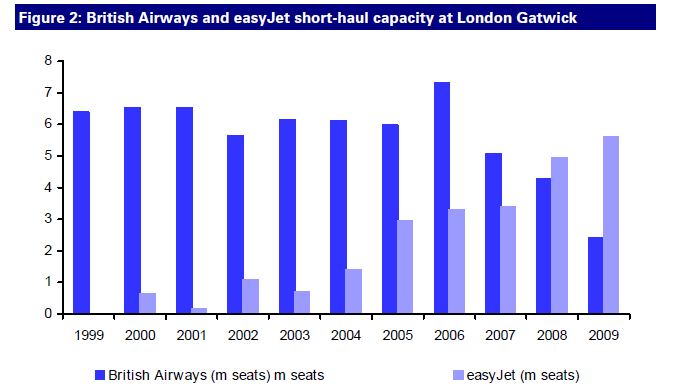

Euroopas on pigem usku odavlennufirmade edusse. Seda, et nende ärimudel töötab paremini, näitab hästi näiteks see graafik:

Allikas: Deutsche Bank

Konsensuse 2010 ja 2010 epsi hinnangul kaupleb näiteks Easyjet ca 15x ja 11x hinna ja kasumi suhtarvu juures, mis võrreldes nt Ryanairiga on märgatavalt soodsam. Easyjetil ka suht hea bilansileht.

-

SECi süüdistused Goldman Sachsi vastu on tegelikult turu jaoks olulised ka põhjusel, et varasemalt on GSi peetud pühaks lehmaks, keda väga tihedate sidemete tõttu USA tipp-poliitikaga, USA keskpangaga, SECi endaga jt on arvatud justkui ettevõtteks, kelle tegevusi väga tugevalt ei juleta kritiseerida. Reedene näitas siiski, et päris nii ei ole ning kui süüdistused lendavad juba Goldman Sacshi suunas, kardetakse nende levimist ka teistele panganimedele. Üks sellelaadne video Bloombergis ka siin.

-

Siin nt nimekiri pankadest, kelle käest SEC palus eelmisel aastal selgitust CDOde müümise kohta:

In February, the Financial Times revealed that the SEC last year sent subpoenas to banks including Bank of America, Merrill Lynch, Barclays, Citigroup, Credit Suisse, Deutsche Bank, Goldman, Morgan Stanley and UBS, seeking information about the marketing of CDOs. (allikas: FT)

-

Barron'si hinnangul oli GSi reedene kukkumine liiga võimas ja aktsia valuatsioon on liiga odavaks muutunud:

Goldman now has one of the lowest price/earnings ratios of any large company in the Standard & Poor's 500 index -- even lower than those of cigarette makers like Altria (MO) and Reynolds American. (RAI). Goldman's valuation seems too low because, say what you will about the firm, it doesn't make a product that kills - loe pikemalt siit.

-

Siiani on 1Q10 tulemused USA ettevõtete seas väga korralikud olnud - 73% on kasumiga ootusi löönud ja 79.4% on tuludega ootusi ületanud. Heade tulemuste peale on keskmine tulemuste päeval tehtud liikumine olnud siiski -0.36% (enne reedest oli number positiivne).

-

Citigroupilt (C) samuti oodatust paremad numbrid:

Citigroup prelim $0.15 vs $0.00 Thomson Reuters consensus; revs $25.4 bln vs $20.77 bln Thomson Reuters consensus

-

Huvitav, kas C teeb täna oma reedese kukkumise tasa või on inimeste karjaskäitumine täiesti ettearvamatu?

-

Tänasest alates hõlbustab Q1 '10 tulemuste jälgimist ka meie tulemuste tabel, kus toome ära kõik tähtsamad numbrid raporteerivad ettevõtted. Link tulemuste tabelile on siin.

-

Aasia ja Euroopa olid korralikult punased ning ka USAs algab päev miinuspoolelt. Hetkel S&P500 indeksi futuurid ca -0.4%, Nasdaq100 indeksi futuurid ca -0.2% ning nafta -2.9% @ $80.8 barrelist.

Euroopa turud:

Saksamaa DAX -0.40%

Prantsusmaa CAC 40 -0.65%

Inglismaa FTSE 100 -0.73%

Hispaania IBEX 35 -0.82%

Rootsi OMX 30 -1.01%

Venemaa MICEX -3.33%

Poola WIG -2.87%Aasia turud:

Jaapani Nikkei 225 -1.74%

Hong Kongi Hang Seng -2.10%

Hiina Shanghai A (kodumaine) -4.80%

Hiina Shanghai B (välismaine) -3.67%

Lõuna-Korea Kosdaq -1.13%

Tai Set 50 -1.21%

India Sensex 30 -1.08% -

Here's the Dip -- Will the Buyers Bite?

By Rev Shark

RealMoney.com Contributor

4/19/2010 8:44 AM EDT

The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails.

-- William Arthur Ward

The selloff triggered by fraud charges against Goldman Sachs (GS) is continuing this morning as overseas markets react and rumors swirl about action against other banks. Adding to the problem is a 4.8% drop of Chinese shares in Shanghai, the biggest loss in eight months, as local governments take steps to crack down on real estate speculation. China stocks have had cooling momentum for a couple of weeks now and have been signaling some potentially bad news.

So is the market undergoing a negative change in character, or is this just another hiccup that will be quickly forgotten as the dip-buyers jump in and drive us back to highs? Betting against "V"-shaped recoveries in this market has been a losing game for over a year now -- will it be different this time?

Many market players, including me, thought that the dip back in January was going to be different, but we ended up with an even stronger bounce than we had seen during the 2009 run. "V"-shaped recoveries to new highs are not considered to be typical market action, but they have been the norm in this market for quite some time.

After just a one-day pullback, it is premature to talk about "V"-shaped bounces, but the issue here is the tenacity of the dip-buyers. The dip-buying approach has worked extremely well for a very long time; the only drawback to the approach has been that there haven't been that many pullbacks to jump on.

Market players are not going to give up easily on dip-buying until they have been caught leaning the wrong way. So far they have only be rewarded, so I would not be at all surprised to see them jump in on this Monday-morning weakness, especially when it is widely known that Mondays have been the best-performing day of the week by far.

The other positive the bulls have going for them is that the focus is going to stay on earnings for the next couple of weeks. Probably the most important call of the earnings season is going to be Apple (AAPL) on Tuesday night. Until that is out of the way, the bears are probably going to be a little hesitant to press their bets. We haven't had too much of a "sell the news" reaction to good earnings news so far, but conditions are still good for it to occur.

The biggest negative this market faces right now it that after the run over the last two months, we are still very technically extended and don't have much support. We went straight up on light volume most of the way, and that just doesn't create much support. The best support on the charts is 1150 on the S&P 500 -- the January highs. That is a long way down, and given the dip-buying inclination of traders we are not likely to get there very quickly.

Obviously with the selling pressure we are seeing now, we need to take some defensive action to make sure we don't let losses get out of hand. Even if you are looking for a quick recovery in this market, it is extremely important to stay disciplined and take stops and lock in gains in accordance with your trading plan.

The market has yet to undergo a major change in character, and earnings season may delay any significant downside, but we need to increase our vigilance and defensiveness. Nothing is more important than protecting your capital, and if we start to slip we need to move quickly to do so.

-----------------------------

Briefing.com

Ülespoole avanevad:

In reaction to strong earnings/guidance: IDSA +4.8%, HAS +2.6% (light volume), PHG +1.0%, ACI +0.8%.

M&A news: CRN +29.9% (The GEO Group to buy Cornell Companies in $685 mln deal; transaction implies GEO to pay premium of 35% at $24.96 per share, based on Friday's closing prices).

Other news: EPCT +9.4% (announced that the commercial launch of Ceplene), YMI +4.4% (announces pivotal preclinical efficacy data for the JAK1/2 inhibitor CYT387 published in Blood, the Journal of the American Society of Hematology), TASR +1.7% (receives order for 250 TASER X26 units), LDK +1.2% (reaches milestone of 2.0 gigawats annualized capacity at its wafer plant), RSH +0.8% (RadioShack sale talk heats up - NY Post).

Analyst comments: WBCO +3.5% (upgraded to Outperform from Sector Perform at RBC Capital), S +2.2% (upgraded to Outperform from Market Perform at Wells Fargo), FST +1.5% (upgraded to Buy from Neutral at Goldman- added to Conviction Buy list).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: SPF -8.3%, MMR -5.5%, OKSB -3.4%, LLY -2.4%, HAL -1.1%.

Select financial related names showing weakness: BPOP -3.4%, NBG -3.0%, UBS -2.7% (SEC probes other soured deals - WSJ), HBC -2.6%, BCS -2.5%, ING -2.5%, BBVA -2.3%, ALL -2.2%, PUK -1.7% (Prudential dismisses defection fears - FT), STD -1.7%, BAC -1.5%, AIG -1.4%, CS -1.4%, GS -0.7% (Germany, UK demand Goldman Sachs probe - Reuters; removed from FBR Top Picks list).

Select metals/mining stocks trading lower: SLW -3.0%, IAG -2.4%, BBL -2.3%, BHP -2.3%, RTP -2.1%, GOLD -2.0%, MT -1.5%, ABX -1.2%, GLD -0.3%.

Select oil/gas related names showing weakness as crude oil extends its sell off from Friday's session: STO -3.0%, BP -2.3%, TOT -1.8%, RDS.A -1.7%, PBR -1.6%, E -1.6%, COP -1.4%, REP -1.4%.

Select airlines trading lower with continued flight disruptions from ash: CAL -3.2%, LCC -2.8%, AMR -2.2%, DAL -1.1%, UAUA -1.0%.

Other news: RNN -12.0% (pulling back from past three trading day run-up), TNE -9.8% (trading ex dividend), BVX -7.8% (announces $3 mln private placement), ZN -6.9% (discloses letter to shareholders providing investor update; will purchase AME's drilling rig for an initial payment of $7 mln and series of $1 mln additional payments), RYAAY -4.7% (traded lower overseas), XCO -3.7% (filed for a ~64.287 mln share common stock offering by selling shareholders), RCL -3.5% and CCL -3.1% (still checking for anything specific), ABB -2.3% (still checking).

Analyst comments: ESE -5.0% (downgraded to Underperform from Sector Perform at RBC Capital Mkts; tgt lowered to $24 from $32 ), PALM -4.1% (Departure & retention actions likely a sign acq not pending - UBS; downgraded to Underperform at Morgan Keegan), SNDK -2.4% (downgraded to Underperform from Sector Perform at Pacific Crest), KG -2.3% (downgraded to Sell from Neutral at Goldman ), CVE -2.1% (downgraded to Market Perform from Outperform at BMO Capital Markets), PT -1.9% (downgraded to Hold from Buy at Citigroup), MRX -1.9% (downgraded to Neutral from Buy at Goldman), LPNT -0.9% (downgraded to Sell from Neutral at Goldman). -

Thomas Weisel on veel enne hommeõhtuseid tulemusi kergitamas AAPL hinnasihti. Uueks sihiks konsensuse ülemine äär ehk $300.

-

Juhtivate indikaatorite numbri oleme jätnud siia panemata, kuid parandame selle vea nüüd. Numbrid olid igaljuhul oodatust paremad.

Briefing: March Leading Indicators +1.4% vs +1.1% consensus, prior revised to +0.4% from +0.1%. -

American Intl jumps on heavy volume as Bloomberg reports that Congressmen Cummings, Defazio say SEC should widen GS probe and that AIG-GS trades should be probed

-

Ja taas kord on turg põhjadest kobedalt kosunud ning enamus indeksitest kergelt tõusus. Kas viimane tund toob muutusi tavapärasesse pilti?

-

ECB's Weber tells lawmakers Greece may need up to EUR80 bln, source says - WSJ

-

IBM prelim $1.97 vs $1.93 Thomson Reuters consensus; revs $22.9 bln vs $22.75 bln Thomson Reuters consensus

IBM raises FY10 EPS guidance to at least $11.20 vs at least $11 previously and the $11.12 consensus

Esimese hooga müüdi $129.50 peale, kuigi esmapilgul väga korralikud tulemused.

Tulemuste ootuses kauples juba pealpool $133 taset, ootused olid juba väga kõrgel aga eks konverentsikõne annab kindla suuna.