Börsipäev 30. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

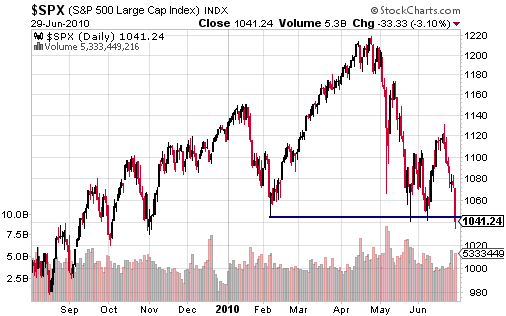

Lisaks Hiina oodatust madalamatele juhtivatele indikaatoritele aitas eile USA tarbijate suurenenud pessimism riigi majanduse ja tööturu taastumise suhtes korraldada turgudel korraliku verevalmise, mille tulemusel S&P500 indeks taandus -3,1% kaheksa kuu põhjadele. Aasia turud on täna hommikul samuti miinuses, olles siiski kosunud päeva põhjadest. USA futuurid kauplevad hetkel 0,2-0,3% plusspoolel.

USA makro osas langeb tähelepanu juunikuu ADP Employment numbrile (kl 15.15), mis peaks näitama 61 000 töökoha loomist erasektoris (va põllumajandus) ehk 6000 võrra enam võrreldes maikuuga. Kell 16.45 avaldatakse Chicago PMI (ootus 59,0 vs maikuu 59,7) ja 17.30 toornafta varude raport.

-

Eilse suure languspäevaga vajusid USA indeksid selle aasta madalaimale sulgumistasemele. Veebruarikuus nähtud põhju testiti korra mai lõpus, siis juuni alguses ja nüüd siis uuesti juuni lõpus:

-

head-and-shoulders way to go

-

Eile suutis S&P500 indeksis ainult üks aktsia plusspoolel lõpetada (kukkujate arv oli suurim alates 1990. aastast. Ainult 29.09.2008 oli müük sama laiapõhjaline). Bespoke toob välja, mis tavaliselt nõnda laiapõhjalistele müügipäevadele järgnenud on:

-

Tuletaks täna veelkord meelde, et homme kukub Euroopa Keskpanga 442 miljardi euro suuruse krediidiprogrammi tähtaeg, mille raames said eurotsooni pangad aastaks 1%lise intressiga laenu võtta. Täna tasub jälgida, milliseks kujuneb pankade huvi uue 3 kuulise krediidiprogrammi vastu. Nagu eilses börsipäevas Erko mainis, siis summat alla ca $200 miljardi tõlgendatakse ilmselt positiivse märgina. Kui suureks pankade huvi kujuneb, peaks selguma umbes kahe tunni pärast.

-

Ja kõikide nende abipakettide tasustal tasub tähele panna, et täna lõppev Q2 oleks ilmselt läinud ajalukku perioodina, kus võlakriis oleks finantsturgudel uue kaose tekitanud, kui Euroopa Liit, IMF ja Euroopa Keskpank ei oleks oma abiga sekkunud. Nõnda halb oli (on?) paraku olukord.

-

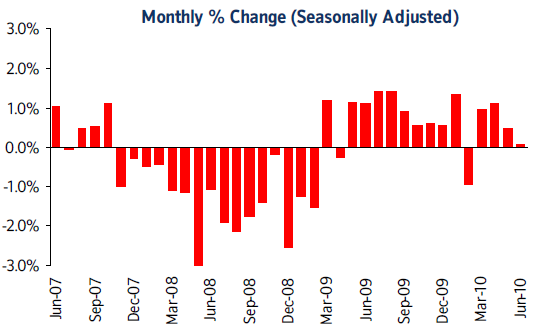

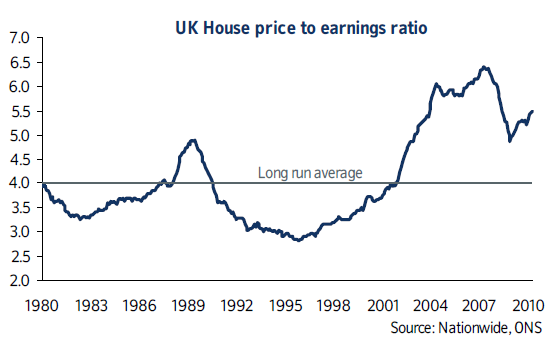

Kinnisvara hinnatõus Suurbritannias on hakanud vaikselt järele andma, kerkides juunis 0,1% võrreldes maiga. Aastataguse perioodi baasil on inflatsioon siiski ligi 9%, ent arvestades mullu suvel alanud tugevat tõusu, hakkab kõrgem baas seda arvatavasti allapoole tooma. Kui nõudlus on jäänud laias laastus stabiilseks, siis Nationwide andmetel on pakkumine kasvanud tänu valitsuse otsusele kaotada Home Information Packs (HIP) ehk seni müüja suhtes kehtinud nõue avaldada kinnisvara kohta tasuta olulist informatsiooni, mis aitaks ostjal vältida võimalikke üllatusi müügiprotsessi lõpus.

Teine oluline mõjutegur saab olema valitsuse eelarvepoliitika ja fiskaalkärped, eriti just muutused kapitalimaksu osas, mis mõjutab kinnisvaraturgu kõige otsesemalt. 22. juunil avalikustatud eelarvekava raames otsustati kapitalimaksu tõsta 18%lt 28%le, mis osutus siiski kardetust väiksemaks, kuna vahepealt spkuleeriti selle jõudmist koguni tulumaksuga ühele tasemele ehk 40%le.

via Nationwide: Looking beyond the short-term, the spending cuts and tax increases in the Budget will clearly put a squeeze on household disposable incomes, which are undoubtedly an important driver of house prices. Given the already elevated level of the house price to earnings ratio, this limits the scope for property values to maintain the very strong upward momentum that we have seen over the last year. However, the acceleration of the fiscal consolidation means that interest rates are likely to be lower than they otherwise would have been, which should provide some offsetting support to households and mortgage affordability.

-

FRANKFURT, June 30 (Reuters) - The European Central Bank lent banks 131.9 billion euros ($161.4 billion) in three-month funds on Wednesday, below expectations, as banks face the repayment of close to half a trillion euros in 12-month funds.

The relatively low demand should help ease concerns about bank finances which have rocked stock markets this week. -

....ning euro teeb korraliku hüppe ülespoole

-

http://www.e24.ee/?id=282060

Omab see turule mingit mõju? -

Eilne laiapõhjaline müük ei toonud kaasa vaid seda, et S&P 500 indeks kukkus läbi tehnilistest tasemetest, vaid ühtlasi langes indeksi P/E viimase aasta madalaimale tasemele. Ehk siis indeksi P/E on praegu ca 15.0644x. Allolev graafik peaks öeldut vast sõnadest paremini demonstreerima.

Allikas: Bloomberg

-

Küll on ikka elu tore, et maailmas on vähemalt üks piiramatu ressurss: raha. Seda on alati täpselt nii palju kui parasjagu vaja on ja kui puudu tuleb, siis saab alati juurde tekitada.

Ja tänane lugemisvara Remarque'ilt -

Kristjan, sa ikka seda tead, et toetus- ja vastupanutasemeid joonistatakse väga paksu pliiatsiga. Seega S&P tehnilisest feilamisest rääkida on veel varavõitu.

-

Karum6mm, olen täiesti nõus.

Tegelikult ei mõelnudki, et järgmised paar kuud näeme punaseid indekseid. Pigem üritasin välja tuua mõtte, et tehniliselt vaadatuna on turgudel huvitav ning sama võib öelda ka fundamentaalide kohta (kui me arvestame P/E suhatarvu). -

Iga jumala kord kui ma kuulen fraasi "(tehniliselt/fundamentaalselt) on turul huvitavad ajad" ajab see mul...

ah, las olla, minujaoks on selge et see mittemidagiütlev dogma käiakse välja siis kui mitte midagi asjalikku ei osata öelda -

Nigga, ma pean ka tehnilist analüüsi kohati täielikuks esoteerikaks (Elliott Wave - no PLEASE tõesti!). Samas endal on õnnestunud sellega kohati toredat taskuraha teenida ;)

-

Seega tõmmati turgudelt täna ära ca 310 mlrd eurot (442-132), päris kena kopikas teine.

-

Minu jaoks on piir tehnilise/fundmantaalse indikatsiooni vahel järjest segasemaks muutunud. Veel kolm aastat tagasi arvasin ma teadvat, kuidas mustsõstrad musträstastest eraldi hoida, aga enam pole ma selles kuigi kindel. Näiteks kasvõi selline triviaalne küsimus, kas P/E suhtarv tuleks lugeda fundamentaal- või tehniliste indikaatorite kilda kuuluvaks? Alumine pool viitaks fundamentaalile, aga vp hind on ju puhtalt tehniline nähtus? Jah, leidub muidugi puhtaid tehnilisi surrogaat-näitajaid ja ka selgelt puhtaid fundamentaalne, aga nende miksimisel saadavad asjad panevad vahel kukalt kratsima.

-

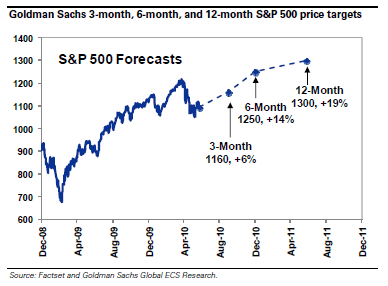

Goldman Sachs avaldas 28. juunil oma nägemuse turgudest käesoleva aasta teiseks pooleks. Endiselt prognoosib analüüsimaja, et S&P 500 indeks lõpetab aasta ca 1250 punkti juures (ehk turud tõusevad aasta lõpuks praeguselt tasemelt ca 20%).

GSi hinnangul kasvab USA majandus Q3 ja Q4 jooksul y-o-y baasil 1.5%. Seejuures ei usuta baasintressimäära tõusu enne 2012. aastat – „A low rate/low inflation macro backdrop has historically been associated with positive S&P 500 returns.”

Paar võõrkeelset lauset GSi analüüsist:

Earnings - Our operating EPS estimates for the S&P 500 remain $78 for 2010 and $93 for 2011. Our pre-provision and pre-write-down estimates equal $83 and $93, respectively, reflecting annual growth rates of 15% and 12%. Our earnings estimates imply negative revisions to bottom-up consensus EPS estimates of $82 in 2010 and $97 in 2011.

Valuation - We anticipate the market will rise by 6% to 1160 over the next three months, rise 14% toreach 1250 by year-end 2010, and reach 1300 in 12-months representing a return of 19%.The S&P 500 currently trades at 12.2x our pre-provision and write-down NTM EPS estimate.Should the market reach 1250 it would reflect a P/E multiple of 13.4x NTM EPS.

-

Palkamine erasektoris on juunis oluliselt väiksem võrreldes maikuuga ning futuurid annavad järele, hetkel kauplevad nullis

June ADP Employment Change +13K vs. +61K Briefing.com consensus; prior revised to +57K from +55K

-

Euroopa turud:

Saksamaa DAX -0,12%

Pantsusmaa CAC 40 -0,63%

Suurbritannia FTSE100 -0,27%

Hispaania IBEX 35 +0,03%

Rootsi OMX 30 +0,32%

Venemaa MICEX -1,28%

Poola WIG -0,53%Aasia turud:

Jaapani Nikkei 225 -1,96%

Hong Kongi Hang Seng -0,59%

Hiina Shanghai A (kodumaine) -1,19%

Hiina Shanghai B (välismaine) -0,19%

Lõuna-Korea Kosdaq +0,50%

Tai Set 50 -0,46%

India Sensex 30 +0,95% -

A Broken Market

By Rev Shark

RealMoney.com Contributor

6/30/2010 8:28 AM EDT

Not being able to govern events, I govern myself.

-- Michel de Montaigne

It is the last day of the second quarter of 2010, and it has not been a good one. We started off well, as the amazing light-volume levitation off the February low continued into April, but at the end of the month the market underwent its first real change in character since the bottom in March 2009.

The most notable characteristic of this market as it rallied for over a year was the light volume and the propensity for "V"-shaped bounces. Numerous times it looked like the indices were going to break down, but just as we started to crack we would reverse and go straight back up on declining volume. The rally this past March was a particularly good example.

Computerized trading has received much of the blame for this rather peculiar technical action, but the flood of liquidity caused by bailouts and stimulus plans also was a driving force. With interest rates near zero, there was just too much cash looking for a place to go, and much of it was parked in the stock market.

At the end of April, things changed. There has been a major political shift as the economy continues to struggle despite massive spending and worry grows over the huge budget deficit. The flood of liquidity has dried up and the dip-buyers who pounced on every little pullback no longer have the ability to run the market straight back up after every slight pause.

Since the end of April, the market has suffered three failed bounce attempts and has been turned back almost exactly at key resistance points a number of times. Suddenly the overhead resistance that was completely irrelevant during the market rally is having a significant impact, and market players are again intently focused on key support and resistance points.

Yesterday we breached another important support level. This was the low of the year for the S&P 500 at 1040. We did manage to bounce enough in the final minutes of trading to close above that level, but it was a technical victory for the bears.

At this point there is no question that we are caught in the grips of a nasty downtrend. The S&P 500 is down close to 15% from its highs; the big question is whether we are falling into another bear market or whether this just an ugly correction that will overcome in the near term.

The bearish perspective is a compendium of recent headlines. The news flow has been terrible -- economic stats weak, Europe a shambles, China struggle, oil leaking in the Gulf, and so on. During our yearlong rally, we blithely shrugged off all the worries and concerns about the slow economic recovery. The high unemployment rate was a nagging problem, but the market was capable of ignoring it for a long time. The mood has shifted now and we no longer are capable of ignoring bad news so easily because we no longer seem to have this endless flow of capital to push us.

The bullish case here is that although we are going through a rough patch, things have improved. Maybe the market was a bit ahead of itself, but there is slow but steady improvement, and the problems in Europe and China won't kill the recovery here. The bulls are particularly optimistic about upcoming earnings reports and believe that once we see some solid numbers and good guidance, we will find our footing and turn back up.

For now the bears have the benefit of the doubt. We are overdue for some sort of oversold bounce, but make no mistake about it -- this is a broken market in a downtrend. We need to respect that beyond all else. The biggest danger in a downtrend comes when you keep trying to anticipate a bottom that doesn't come. There is nothing wrong with looking for bounces and countertrend plays, but nothing can cause more damage than constantly trying to call the exact bottom.

We have a little bounce shaping up this morning. Asian was weak again overnight, particularly Japan, but Europe bounced a bit as the ECB funding operation eased fears of debt crisis.

Hopefully we'll have some upside trading opportunities as an oversold bounce develops, but be careful out there and make sure you keep a tight watch on positions. This is a market that has some major problems.

-----------------------------------

Briefing.com vahendusel:

Ülespoole avanevad:

M&A news: STST +40.0% (Boeing to acquire Argon ST for $34.50/share in cash), ABII +21.1% (Celgene to acquire Abraxis BioScience for ~$71.93 in cash and stock), .

Select financial related names showing strength: BCS +4.8%, LYG +3.7%, STD +3.0%, COF +2.4%, C +2.4% (Cramer makes positive comments on MadMoney), DB +2.2%, UBS +2.0%, CS +1.9%, BAC +1.5%, HBC +1.3%, RF +1.0%, HIG +1.0%.

Select oil/gas related names showing strength: BP +4.8% (traded higher overseas), STO +1.5%, RIG +1.3%, E +1.3%, TOT +0.8%.

Select European drug names trading higher: GSK +1.4%, SNY +1.1%, NVS +0.8%.

Casino/gaming related names modestly rebounding: MPEL +2.6%, WYNN +1.2%, LVS +1.0%

Other news: ANX +14.9% (light volume; announces 9-month stability data results for ANX-530), TSLA +6.7% (new IPO seeing continued strength), PT +6.4% (TEF discloses it increased offer for stake of of BRASILCEL, N.V. from the company), ADES +5.8% (Arch Coal licenses ADA-ES Coal Enhancement Technology), ALV +4.4% (still checking for anything specific), ACN +0.9% (Cramer makes positive comments on MadMoney), .

Analyst comments: LPX +3.9% (upgraded to Outperform from Underperform at Scotia Capital), BTU +2.0% (upgraded to Buy from Hold at Deutsche Bank), F +1.2% (Hearing upgraded to Hold from Sell at Citigroup).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: AM -5.2%, GIS -4.2%, MON -1.6%.

M&A news: CELG -5.2% (Celgene to acquire Abraxis BioScience for ~$71.93 in cash and stock).

Select metals/mining stocks trading lower: BBL -1.8%, RTP -1.7%, GSS -1.6%, BHP 1.1%, GOLD -0.7%.

Other news: TIBB -42.0% (North American Financial Holdings to invest $175 million in TIB Financial), ETRM -22.9% (approved a 1-for-6 reverse split of its common stock effective upon close of July 9), STEM -8.1% (announces $6 million equity financing), MELA -3.6% (announces proposed public offering of common stock), GHDX -2.1% (light volume; files to sell 10 mln shares of common stock).

Analyst comments: FTE -1.5% (light volume; downgraded to Neutral from Buy at Goldman). -

June Chicago PMI 59.1 vs. 59.0 Briefing.com consensus; prior 59.7

-

Briefing.com vahendusel:

Department of Energy reports that crude oil inventories had a draw of 2007K (consensus is a draw of 1000K);

gasoline inventories had build a of 537K (consensus is a draw of 400K);

distillate inventories had a build of 2457K (consensus is a build of 950K).

-

CNBC reports Senator Reid says no senate vote on FinReg until after July 4th, also reports Rep Frank says Financial reform bill is "not amendable"

-

Moody's places Spain's Aaa sovereign rating on review for possible downgrade

-

Fidelity National Information Services: Moody's confirms FIS' CFR at Ba1; Outlook is Stable

-

2 kvartali kokkuvõte:

Reviewing the performance of global equities during the second quarter, the U.S. markets registered losses between 9.4% and 11.3%, outperforming Shanghai which suffered a 22.9% plunge. Volatility as measured by the VIX soared 93.8% for the quarter as fear crept back into the market, and the cost of protection almost doubled.. It should be noted that South Korea's Kospi was the only major market to close in positive territory (+0.3%). Looking at Europe, France's CAC and Britain's FTSE dropped 13.4%, while Germany's DAX outperformed with only a 3.1% decline. Reviewing the currencies, the safe haven plays of the dollar (+6.1%) and yen (+5.4%) were winners, while the euro (-9.4%) suffered the heaviest losses.