Börsipäev 12. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

Reedene tõus USA börsidel ning nädalavahetusel avaldatud oodatust paremad Hiina ekspordinäitajad on vedanud Aasias indekseid kõrgemale ning Euroopa futuure vaadates tõotab siingi tänane päev alata positiivse noodiga. USA indeksite futuurid on seevastu kauplemas 0,4% punases.

Olulisi majandusuudiseid täna USA-st ega ka Euroopast oodata ei ole (mainimist vääriks vast ainsana Suubritannia esimese kvartali SKT lõpliku näidu avaldamine). Seevastu hilisõhtul pärast turgude sulgemist teeb tulemustehooaja avalöögi maailma üks suurimaid alumiiniumitootjaid Alcoa, kelle teise kvartali käibeks oodatakse 5,047 miljardit dollarit ja aktsiakasumiks 0,12 dollarit (mullu samal ajal olid need näitajad vastavalt 3,93 mld ja -0,26 USD ning esimeses kvartalis 5,238 mld ning 0,10 USD).

-

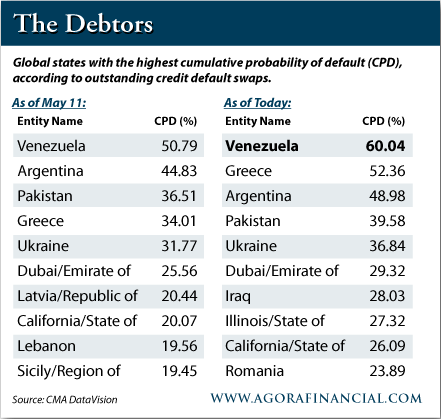

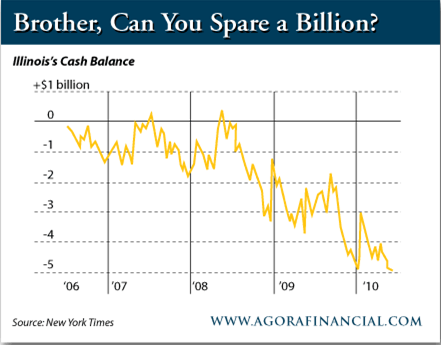

Oleme siin börsipäeva foorumis päris mitu korda maininud USA osariikide hiigelsuuri eelarvedefitsiite, kuid olukord on jõudmas kriitilise piirini. Alla olen lisanud graafiku, mis näitab riikide/osariikide kumulatiivset maksevõimetuse tõenäosust (inglise k. „cumulatuve probability of default“ ehk „CPD“) seisuga 6. juuli 2010.

Nagu näha, siis tõenäosus, et USA osariigid Illinois ja California jätavad oma võlausaldajad hooletusse on peaaegu sama suur, kui see on Iraagis. Rumeeniat peavad investorid aga Californiast "stabiilsemaks".

Illinoisi rahapositsioon oli möödunud nädalal -$5 miljardit. Paraku on ka osariigi prognoositud eelarvedefitsiit ca $12 miljardit.

Allikas: agorafinancial.com

-

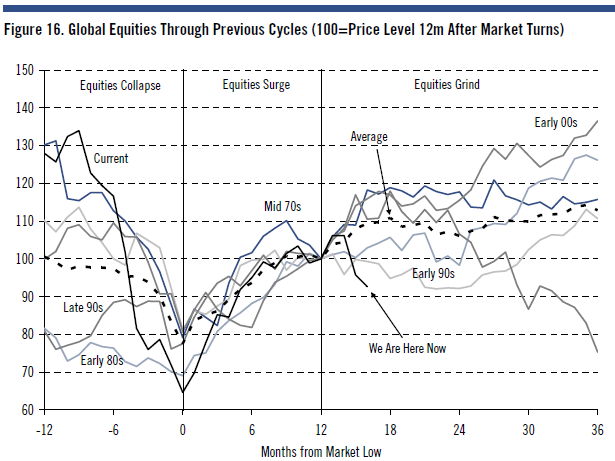

Mitmete juhtivate majandusindikaatorite pehmenemine, mis on viimasel ajal investorite sentimenti kahjustanud, on Citigroupi arvates tsükli praeguses faasis täiesti normaalne nähtus, leides aset ka varasemates retsessioonijärgsetes taastumistes. Nagu allolevalt graafikult võib näha, läbivad globaalsed aktsiaturud esimesel aastal tugeva tõusu, kuid teisel ja kolmandal aastal kulgetakse kõrgemale juba rahulikumas tempos.

Analüüsimaja arvates viitavad indikaatorid ettevõtete aktsiakasumite kasvu aeglustumisele, kuid mitte langusele. Ühtlasi ollakse seda meelt, et 20%line EPSi kasv 2011. aastal on saavutatav ning uuesti majanduslangusesse sattumine ebatõenäoline, mistõttu pakub turg nende meelest head ostuvõimalust. Globaalsed aktsiaturud kauplevad hektel 10kordsel 2011.a oodataval kasumil.

Isegi kui maailmamajanduses peakski topeltpõhi tekkima, jääb ettevõtete bottom line tänu kriisi jooksul kärbitud kuludele majanduskeskkonna muutustele oodatust vastupidavamaks. Citi enda stressitest näitas, et nõrgapoolne majanduskasv aitab saavutada 20%list aktsiakasumi kasvu. Double dip stsenaariumi korral (5-6%lise nominaalse kasvu asemel suureneb globaalne SKT 3%) jääb ettevõtete EPS muutumatuks. Langusesse satuksid ettevõtete kasumid, kui globaalne nominaalne SKT peaks tegema tugeva taandumise ja kukkuma -1%.

-

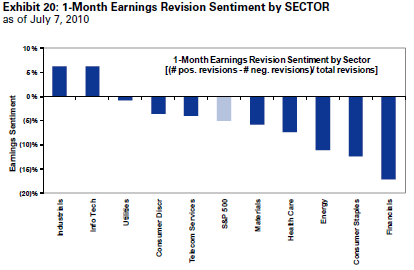

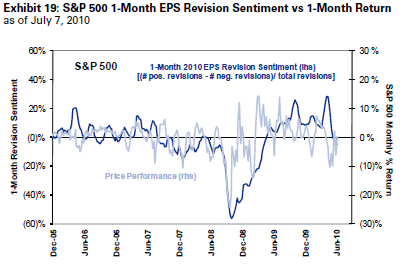

Goldman Sachs avaldas reedel huvitavat statistikat – S&P 500 indeksi viimase nädala ca 5%line tõus on analüüsimajad selgelt ettevaatlikumaks teinud ning aktsiahinna reitinguid ja hinnasihte on pigem langetama hakatud.

Lisasin alla graafiku, mis näitab nii-öelda EPS revideerimise sentimenti ((# hinnasihtide tõstmine - # hinnasihtide langetamine) / # kõik hinnasihtide muutused). Sektoripõhiselt vaadatuna on enim hinnasihte langetatud finantssektoris ja tõstetud tööstussektoris. S&P 500 indeksisse kuuluvate ettevõtete hinnasihte on samas enne tulemustehooaega kärbitud.

Allikas: Goldman Sachs

-

http://pragcap.com/rare-interview-with-john-hussman-why-he-is-bearish-right-now

"The problem with the forward earnings estimates is that they are very frequently so dead wrong as to be irresponsible."

Kas kuskilt oleks võimalik näha analüüsimajade SP500 EPSi prognoose 2008. aastaks? -

klmike, siin üks graafik analüütikute ootustest ((# hinnasihtide tõstmine - # hinnasihtide langetamine)/ # kõik hinnasihtide muutused) ja turu (S&P 500 indeksi) tegelikust suunast. Perioodil detsember 2005 kuni juuni 2008 oli prognoositud EPS'i ja turu suund üpriski sama trendiga, kuid viimastel aastatel on korrelatsioon tõepoolest oluliselt langenud.

Allikas: Goldman Sachs

-

Kui siin täna Goldman Sachsi analüüsidest juba niipalju juttu on olnud, siis lisan siia ka nende reedeõhtuse analüüsi kokkuvõtte Saksamaa börsil kauplevast VolksWagenist, mida GS analüüsimaja peab väga heaks ostukandidaadiks ja üheks tugevaimaks aktsiaks autotööstusest. Volkswagen on Goldman Sachsi "veendumusega ostunimekirjas" ning reedel kergitati veel hinnasihti €126 pealt €132 peale.

In our view, VW is one of the best positioned automotive companies tocope with, and to take advantage of, the significant structural challengesfacing the global automotive industry. We expect these to drive furtherconsolidation in a ‘race’ for economies of scale. With VW trading at 20%2011E EV/sales, we believe the market neither recognizes the value of itsbusiness footprint (a well balanced geographic exposure) nor thestructural transformation of the business model’s profitability. In this notewe identify eight key value drivers. We reiterate our Conviction Buy andraise our 12-month price target to €132 from €126.

-

Component Stocks' Correlation to S&P 500 at Highest Level Since '87 Crash... In recent weeks, stocks in the Standard & Poor's 500-stock index have shown an increasing tendency to move in the same direction at the same time. Last week, those stocks' tendency to move in the same direction as the index hit an extreme not seen since October 1987

WSJ

Suhteliselt täpselt näitab turu praegust seisu. Midagi ei toimu ja mitte miski ei liigu, sest kogu turg liigub nagunii koos. -

Kuigi hommiku poole olid USA indeksite futuurid ca 0.5% miinuses, siis 15 minutit enne USA börsi avanemist on tagasi jõutud reedeste sulgumistasemete juurde.

Euroopa turud:

Saksamaa DAX +0,25%

Pantsusmaa CAC 40 +0,10%

Suurbritannia FTSE100 +0,22%

Hispaania IBEX 35 -1,11%

Rootsi OMX 30 -0,08%

Venemaa MICEX +1,57%

Poola WIG +0,83%Aasia turud:

Jaapani Nikkei 225 -0,39%

Hong Kongi Hang Seng +0,44%

Hiina Shanghai A (kodumaine) +0,80%

Hiina Shanghai B (välismaine) +0,82%

Lõuna-Korea Kosdaq +0,92%

Tai Set 50 -0,32%

India Sensex 30 +0,58% -

And We're Off

By Rev Shark

RealMoney.com Contributor

7/12/2010 8:59 AM EDT

"My report card always said, 'Jim finishes first and then disrupts the other students'"

-- Jim Carrey

We kick off second-quarter earnings season this week, and that means we must now consider a number of new factors as we navigate the market. Earnings season isn't just about whether a company exceeds earnings estimates. What is even more important is the level of expectations that exists as the news hits. We can rally on bad news if expectations are low enough or selloff on good news if market players are expecting too much. The great difficultly is trying to determine what the market is really expecting and/or has already priced in. Quite often, we don't know those things until we see the way that stocks react to the news.

The big rally last week raises the chance of a sell-the-news reaction to earnings this week and with some significant technical overhead looming, it would not be at all surprising to see some pullbacks and consolidation. On the other hand, we are still well off the highs we hit in April, and some nervousness and lowered expectations have been priced in over the past few months. The tone of reports is going to determine whether the recent bounce is the start of a change in trend or just an oversold bounce that is going to fizzle.

During earnings season we need to watch to see if a theme emerges. The first thing we have to look for is whether there is an inclination to sell or buy the earnings news. The most dangerous thing you can do is assume that missing or beating analyst expectations is the only thing that is going to determine the direction in which a stock will move. Chasing a good report or trying to short a bad one can be costly if all you do is look at the numbers and forget the role of expectations. I always laugh a little when experienced market players are puzzled about why a stock is selling off when the company seems to have solid numbers. It is all about expectations.

Another area we need to watch is forward guidance. This quarter, I'm going to be particularly interested in seeing what companies say about the prospects for business in Europe. We've been wrestling with economic issues there for a while now, but the most important test will be whether companies use that as an excuse for poor results or to cut forward guidance.

What has been most interesting about earnings reports over the past year is that they have generally been quite strong, even though we have had such a poor economy. That was probably caused to some extent by lower expectations, but there have been some surprisingly positive earnings despite the persistent economic gloom. There is some danger now that market players are too complacent, but we'll see what emerges as reports roll out.

Generally, I avoid gambling on reports. I don't think that there is much edge when you have to try to guess not only whether a report will exceed expectations but what those expectations really might be. There are lots of very big and well informed funds that have much better information than any individual trader will have, so I see little edge trying to compete with them.

What I prefer to do is buy after the fact. The market typically takes some time to fully price in very strong earnings reports, and that will allow for some lower-risk entries if you understand the report and are able to move quickly. That will be my focus, especially as the smaller companies report results.

We have a fairly quiet Monday morning so far. There is some minor selling, but I see quite a bit of analyst activity and upgrades of stocks such as Qualcomm (QCOM) , SanDisk (SNDK) , Microsoft (MSFT) , Yahoo! (YHOO) and FedEx (FDX) . The first big earnings report comes from Intel (INTC) on Tuesday night, so we may just drift and consolidate a bit while we wait for that news.

-----------------------------------

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: TUES +10.2% (light volume).

M&A news: HEW +30.6% (Aon to acquire Hewitt Associates for $50.00/share in cash and stock ).

Other news: WY +6.6% (declares special dividend; upgraded to Buy from Neutral at UBS), BP +3.3% (shares higher in pre-market trade, helped by takeover rumors; co also provided update on GoM oil spill in 6-K filing; cost of the response to date amounts to ~$3.5 bln), AA +1.6% (early strength ahead of tonight's earnings release).

Analyst comments: QCOM +1.9% (added to Conviction Buy list at Goldman ), SNDK +1.6% (upgraded to Buy from Neutral at UBS), MON +1.5% (upgraded to Buy from Hold at Citigroup), MDT +0.8% (upgraded to Outperform from Market Perform at BMO Capital), YHOO +0.7% (upgraded to Buy from Hold at Needham; tgt $20).

Allapoole avanevad:

M&A news: AON -7.7% (Aon to acquire Hewitt Associates for $50.00/share in cash and stock ).

Select financial related names showing weakness: AIB -4.5%, IRE -2.9%, STD -2.5%, DB -2.2%, LYG -2.4%, BBVA -2.1%, BCS -2.0%, NBG -1.6%, UBS -1.2%, ING -1.0%.

Select metals/mining stocks trading lower: RTP -3.3%, BBL -2.4%, MT -2.3%, BHP -2.3%, GG -1.1%, AUY -1.0%, GOLD -0.4%, .

Select oil/gas related names showing weakness: TOT -1.6%, REP -1.3%, RDS.A -1.2%, E -1.1%, STO -0.8%, XOM -0.6%

Other news: ABB -4.6% (trading ex dividend), NOK -1.1% (still checking for anything specific).

Analyst comments: GLW -1.8% (downgraded to Neutral from Buy at Goldman Sachs), VCI -1.3% (downgraded to Neutral from Outperform at Baird), -

GS on täna jõudnud ka Qualcommi (QCOM) oma "veendumusega ostunimekirja" lisada. Hinnasihiks $43, mis on turuhinnast ca 25% kõrgemal.

We are adding Buy-rated Qualcomm to the Conviction List as a key beneficiary of accelerating smartphone growth, particularly in Android. While Qualcomm’s chipsets are in about 1/3 of overall handsets, they are in 80% of Android-based smartphones. Moreover, Qualcomm’s Android ASPs are more than double its average ASP. We estimate that every 1% share shift from feature phones to Android-based smartphones translates to $0.06 in EPS upside. While we expect a relatively inline quarter, we see upside into F4Q, where our EPS is $0.60 vs. the Street at $0.57. In addition, our FY11 (Sep) EPS estimate of $2.68 is above the Street at $2.51.

-

S&P affirms United Kingdom 'AAA/A-1+' Sovereign Ratings; Outlook Remains Negative

-

Apple: Consumer Report says can't recommend iPhone 4 because of its problem with its reception, according to CNBC

-

IMAX and United Cinemas enter joint venture partnership for up to five new IMAX theatres in Japan

IMAX and United Cinemas, today announced a joint venture agreement to install up to five digital IMAX(R) theatre systems in Japan. Three of the systems are confirmed, with two scheduled to be installed in time for the launch of Harry Potter and the Deathly Hallows this November, and the third scheduled to be installed in either late 2010 or some time in 2011. Under the terms of the agreement, the companies will have an option to install two additional IMAX theatre systems in Japan at a later date. The deal brings the total number of confirmed joint-venture IMAX theatres scheduled to be operating in Japan by the end of 2010 to eight, compared to four at the end of 2009. -

$35 bln 3-year Note Auction Results: Yield 1.055% (expected 1.053%); Bid/Cover 3.20x (Prior 3.23x, 12-auction avg 3.01x); Indirect Bidders 40.6% (Prior 46.7%, 12-auction avg 53.3%)

-

Novellus prelim $0.66 vs $0.60 Thomson Reuters consensus; revs $321.4 mln vs $312.01 mln Thomson Reuters consensus.

CSX prelim $1.07 vs $0.98 Thomson Reuters consensus; revs $2.7 bln vs $2.63 bln Thomson Reuters consensus. -

Ja Alcoa numbrid ka:

Alcoa prelim $0.13 vs $0.12 Thomson Reuters consensus; revs $5.19 bln vs $5.05 bln Thomson Reuters consensus