Börsipäev 7. september

Kommentaari jätmiseks loo konto või logi sisse

-

Labour Day tõttu olid USA turud eile suletud ning Aasias pole ka seepärast suuremaid liikumisi tehtud. Hang Seng +0.01%, CSI 300 +0,07%. Jaapani Nikkei on aga jeeni tugevnemise tõttu veidi rohkem punases (-0.8%). USA futuurid kauplevad hetkel nulli lähedal.

Kuna Ühendriikidest olulist makrot täna oodata pole, koondub Euroopa sessioonil tähelepanu Saksamaa juulikuu tehastetellimustele.

-

Täna pidasid oma igakuise kohtumise nii Jaapani kui ka Austraalia keskpank, kelle otsused jätta intressimäärad samadele tasemetele olid ootuspärased (Jaapan vastavalt 0.1% ja Austraalia 4.5%). Deutsche Bank juhib aga tähelepanu, et Austraalia keskpank on oma avaldusse toonud taaskord fraasi "for the time being". Eelnevatel kordadel on seda kasutatud 2010.a veebruaris ja ka 2009.a septembris, millele järgnenud kuud on aga toonud intressimäära kergitamise. Seetõttu oodatakse, et Austraalia keskpank kavatseb enne aasta lõppu intressimäärasid tõsta veel ühel-kahel korral, vaatamata tänases avalduses tõdetud suurenenud ebakindlusele globaalsetel turgudel. Homme teatab oma intressimäära otsuse Kanada keskpank ning seal oodatakse tõstmist 0.75% pealt 1.00% peale.

-

Morgan Stanley tõstis Nokia (NOK) aktsia soovituse "overvweighti" peale (varasema "underweighti" pealt) ning hinnasihiks on varasema 6.5 euro asemel 9 eurot. Aktsia kaupleb praegu +2.8% plussis 7.38 euro juures.

-

Bespoke on välja toonud 3. septembri seisuga aktsiaturgude tootlikkuse üle maailma riikide kaupa. Eesti hoiab tublit kolmandat kohta ehk aktsiaturu muutus aasta algusest on +41.94%. Hiina YTD muutus on -18.97% ning USA aktsiaturud on aasta algusega võrreldes peaaegu samal tasemel (-1.24%).

-

Endisest HP (HPQ) tegevjuhist Mark Hurdist sai rivaali Oracle (ORCL) juhatuse liige. Analüütikute hinnangul on see Oracle jaoks väga positiivne, sest väga suure teadmiste ja kogemustega tööstusharu kohta on Hurd mees, kes võib Oracle positsiooni turul märkimisväärselt parandada. Näiteks UBS analüütiku Brent Hilli sõnul viib Hurd Oracle täiesti uuele tasemele.

-

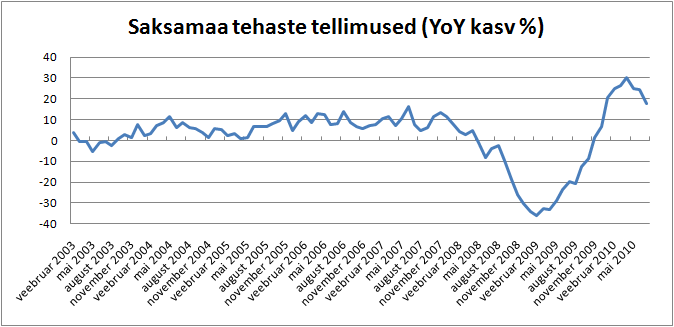

Saksamaa tehaste tellimused langesid juulis mom 2.2% vs analüütikute oodatud 0.5% suurune tõus.

-

Vallole täienduseks lisan siia juurde ka graafiku tellimuste aastasest kasvust, mis on jätkuvalt märkimisväärne võrreldes varasemate aastatega, kuid mõistagi ei saanud selline tempo jäädavalt kesta ning normaliseerumist oli oodata varem või hiljem. Kasvu aeglustumise asemel on aga tellimuste maht kuu baasil hoopis kahanema hakanud ning siin mängib olulist rolli nõudluse vähenemine eksporditurgudel, millele Saksamaa majandus on tugevalt orienteeritud. Seega kui teine kvartal oli Saksamaa majanduse jaoks üle ootuste tugev, siis antud näitaja põhjal võiks eeldada, et seda auru on kolmandas kvartali vähemaks jäämas.

-

Oracle upgraded to Conviction Buy from Buy at Goldman. Target $27.

-

Jeen tegi USA dollari vastu uue 15 aasta tipu ¥83,55 juures, läbides 24. augusti tipu ¥83,59.

-

Gapping up

General news: NOK + 2.7% (strength being attributed to tier 1 firm upgrade), SYT + 2.4% (traded higher overseas), PLX +2.0% (announces the appointment of Tzvi Palash as the COO).Analyst comments: GDOT +2.3% (light volume; initiated with an Overweight at JP Morgan, initiated with an Overweight at Piper Jaffray).

Gapping down

In reaction to disappointing earnings/guidance: CSKI -27.8%, PIKE -7.1%.Select financial related names showing weakness: BCS -5.1% (discloses John Varley intends to step down as Group Chief Executive; will be succeeded by Robert Diamond), IRE -4.5%, CS -3.4%, PMI -3.3%, BBVA -3.2%, ING -3.1%, STD -3.0%, RBS -3.0%, LYG -2.9%, DB -2.8%, DB -2.6%, NBG -2.5%, PUK -2.4%, UBS -2.2%, RDN -2.0%, USB -1.8%, AIB -1.5%, AIG -1.4%.

Select metals/mining stocks under pressure after Australian PM Julia Gillard secured a second term, raising the likelihood for a heavy tax on mining sector profits: RTP -3.8%, BBL -2.8%, BHP -2.5%, TCK -1.8%, FCX -1.5%, MT -1.4%, VALE -1.1%, AA -0.9%.

Select oil/gas related names showing weakness: SDRL -3.6%, TOT -2.5%, SU -2.5%, STO -1.9%, RDS.A -1.8%, SD -1.4%.

Select European drug names trading lower: GSK -2.4%, SNY -1.2%.

Other news: IDIX -51.8% (received verbal notice from FDA that the IDX184 and IDX320 programs have been placed on clinical hold; Conference call at 8:30 am ET), TIVO -3.7% (still checking), CCL -2.9% and RCL -2.6% (still checking for anything specific).

Analyst comments: GR -2.1% (downgraded to Neutral from Buy at Goldman), JKS -1.8% (downgraded to Hold at Auriga).

-

Rev Shark: Bulls Face a Tough Test

09/07/2010 7:33 AMEvery gain made by individuals or society is almost instantly taken for granted.

-- Aldous HuxleyThe question we face this week is whether we can build on the surprising and strong three-day rally into the Labor Day weekend. The mood was quite upbeat and worries about a double-dip recession were put aside as economic reports came in a bit better than expected. Bonds reversed after much talk of a bubble and the major indices even managed to cut through some technical resistance.

The primary driving force behind the rally was that market players had simply become too negative. They were chasing bonds for safety and were acting like the economy was doomed. The fact that we rallied so aggressively on only slightly positive economic data was a clear indication that the mood had simply become too sour.

Now things become much more challenging as market players return to work, volume picks up and we have to deal with a market that has become slightly overbought after three straight-up days. After last week's move, it is extremely difficult to find charts that are offering enticing entry points. Some of the best stocks with the best earnings growth made parabolic moves last week as underinvested market players scrambled to add some long exposure.

If we step back and look at the big picture, the rally last week did a nice job of cutting through resistance levels in the S&P 500 at 1080 (which was the 50-day simple moving average) and at 1100. The next big hurdles are the 200-day simple moving average at 1115 and then the August high just under 1130.

It is that August high that we need to surpass to put this market back in an uptrend, and that achievement is likely to be difficult until we build a better base of support. Despite the good action last week, not much really changed from a fundamental standpoint. Market players had become a bit too negative and were out of position for a bounce. The negative sentiment is probably the biggest positive this market has going for it, but until earnings season starts in early October, we are going to be dancing around to each and every economic report.

The political situation adds a little drama to the situation. Over the weekend President Obama proposed a number of "pro-business" initiatives. The cynics see it as an election ploy, but anything pro-business is good for the market at this point. However, what this market really wants is gridlock in Washington, and that is a good possibility. A lot of folks are looking for the election results to be a positive driver into the end of the year.

Banks were weak overnight in Europe as worries about poor visibility started to emerge again. Mining stocks were also weak on renewed concern over a mining tax in Australia after Prime Minister July Gillard secured a second term.

The bulls grabbed the ball last week and put some points on the scoreboard, but the upside becomes much tougher now. If we can consolidate and hold above the 50-day simple moving average at 1080, we will be in good shape for an eventual attack on the August highs. If we are unable to hold 1080, the bears will start to push hard once again. The news flow is likely to be slow and there is still much nervousness about the health of the economy. That nervousness can easily accelerate once again if the bulls don't do a good job of defending last week's gains.

-

USA turud alustamas päeva mõne minuti pärast ca -0,4% kuni -0,6% punases

Euroopa turud:

Saksamaa DAX -0,66%

Pantsusmaa CAC 40 -1.13%

Suurbritannia FTSE100 -0,65%

Hispaania IBEX 35 -1.29%

Rootsi OMX 30 -0,70%

Venemaa MICEX -0,64%

Poola WIG -0,49%Aasia turud:

Jaapani Nikkei 225 -0,81%

Hong Kongi Hang Seng +0,22%

Hiina Shanghai A (kodumaine) +0,07%

Hiina Shanghai B (välismaine) +0,82%

Lõuna-Korea Kosdaq -0.54%

Tai Set 50 -0.92%

India Sensex 30 +0,46% -

Kätte on jõudnud aeg, kui analüüsimajad ka S&P 500 indeksi käimasoleva aasta prognoosi allapoole toovad (siiani on seda teinud aga vaid kolm analüüsimaja). Oppenheimer langetas täna S&P 2010. aasta prognoosi 1,300 punkti pealt 1,225 punktile ehk aasta lõpuks peaks indeks kallinema praeguselt tasemelt ca 12%. Barclays ootab S&P indeksi näiduks aasta lõpuks varasema 1,210 punkti asemel 1,120 ning Birinyi Associates sihiks on 1,325 punkti asemel nüüd 1,225 punkti. Lisasin alla ka ühe öeldut demonstreeriva graafiku

-

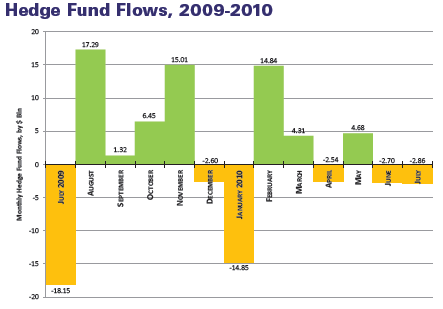

Bloomberg Brief avaldas täna oma riskifondide raporti - käesoleva aasta juulis „voolas“ riskifondidest välja ca $2.9 miljardit (0.2% koguvaradest). Tegu on suurima langusega jaanuarikuust saati, kui fondidest võeti välja koguni $14.85 miljardit.

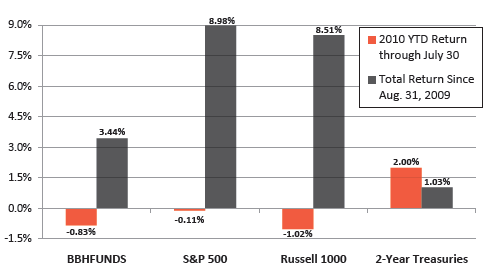

Bloomberti hinnangul peaks pärast vaikset augustit trend jätkuma septembris. Oluliselt paremat tulemust on viimastel kuudel näidanud aga tooraineid kauplevad fondid, kuhu tehti juulis lisainvesteeringuid $3.8 miljardi väärtuses. Aktsiate suhtes on fondijuhid aga endiselt skeptilised. All on graafik Bloombergi terminalis kajastuvate fondide tootlusest (BBHFUNDS), mida võrreldakse indeksite ja 2-aastase võlakirja tootlusega.

-

U.S. Steel (X) ticks back to highs as Najarian on CNBC discusses takeover rumors, citing MT as potential suitor... guests highlight high short-interest

-

Morgan Stanley langetas täna dollari prognoose euro suhtes. Aasta lõpuks oodatakse EUR/USD valuutakursiks $1.36, 2011. aasta 1. kvartali lõpuks $1.32, 2. kvartali lõpuks $1.28, 3. kvartali lõpuks $1.26 ja neljanda kvartali lõpuks $1.24. Hetkel kaupleb euro dollari suhtes ca $1.27 tasemel.

-

$33 bln 3-year Note Auction Results: Yield 0.790% (expected 0.791%); Bid/Cover 3.21x (Prior 3.31x, 12-auction avg 3.10x); Indirect Bidders 42.4% (Prior 40.5%, 12-auction avg 50.4%)

-

Hewlett-Packard sues Mark Hurd for misappropriating trade secrets - CNBC

-

Euro saab dollari vastu täna korralikul peksa. Päevast miinust on kogunenud juba a 1.5% jagu ja jõutud tasemele €1=$1.268.

-

LHV konsensus on progoosinud S&P500 indeksi suuruseks 1252,83 punkti ... ehk kui suured majad on oma prognoose langetanud ja/või langetamas, siis LHV konsensus seda ilmselt tegema ei pea. Märkimata ei saa jätta ka fakti, et konsensus paigutas jalgpalli MM prognoosis Hispaania 2.kohale (napilt kaotas ennustuses esikoha Brasiiliale 3.06 protsendipunkitga). OMXT indeksi suuruseks aasta lõpuks prognoositi 579,16 punkti.

Mis selle loo moraal võiks olla? Ilmselt tõsiasi, et LHV konsensus kokku on asjalikud sellid ja LHV foorumeid (ja börsipäevade kommentaare - resp. LHV poistele) soovitaks investeerimishuvilistel tähelepanelikult lugeda. -

Meredith Whitney Sees A 10% Drop In Wall Street Headcount And "Dramatic" Declines In Payouts In 18 Months

http://www.zerohedge.com/article/meredith-whitney-sees-10-drop-wall-street-headcount-and-dramatic-declines-payouts-18-months?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+zerohedge%2Ffeed+%28zero+hedge+-+on+a+long+enough+timeline%2C+the+survival+rate+for+everyone+drops+to+zero%29 -

Nagu hundist räägid, ...

- POT: Reportedly CNOOC and ChemChina are in talks about Potash bid with ZhongChuan - Chinese press; Up 3% after hours on chatter bid price may be around $185/shr