Börsipäev 21. september

Kommentaari jätmiseks loo konto või logi sisse

-

September, mida aktsiaturgude puhul loetakse üldjuhul nigelaks kuuks, on USA turgudel kulgenud vaid tõusujoones. Seda ka eile, mil indeksid lõpetasid 1,4% kuni 1,7% kõrgemal. Aasias on sentiment taaskord pisut ettevaatlikum enne tänast FOMC kohtumist ning päeva alguse tugevus on praeguseks käest antud. Nikkei -0,24%, Hang Seng +0,12%, Shanghai Composite +0,05%. USA futuurid hetkel -0,2% punasesse liikunud.

S&P500

Euroopast täna ühtegi olulist makrosõnumit oodata pole. USA-s on aga üsna oluliseks infoks augustikuu uute eluasemete ehituste ja väljastatud ehituslubade arv, mis teatatakse kell 15.30. Veelgi enam oodatakse, mida ütleb FOMC (kl 21.15) oma tänaõhtuses avalduses. Turud oleksid seitsmendas taevas, kui kuuleksid uuest rahatrükist, kuid viimase aja makro on kohati olnud isegi oodatust parem, mistõttu ei pruugita järjekordset kvantitatiivset lõdvendamist isegi mitte mainida ja see võib peo meeleolu rikkuda.

-

Goldman Sachs langetas täna mitme euroopa panga reitinguid:

Credit Agrigole (ACA), Natixis SA (KN), Credito Valtellinese (CVAL) langetati neutraalse pealt müü peale. Santander SA (STD), Allied Irish Bank PLC (AIB) ja KBC Group NV (KBC) langetati osta pealt neutraalseks. BNP Paribas (BNP) tõsteti neutraalselt osta peale ja Swedbank AB (SWEDA) müü pealt neutraalseks.

GS on Tuesday made several changes to its ratings for European banks, saying that with Basel III now defined, it can realistically assess banks' capital positions. Goldman estimates that some European banks reach capital above its 2012 Core Tier 1 (CT1) target ratios of 9.8%, atop 20% of current market cap. But for others, it sees "comparative capital restraint as a valuation and operating disadvantage." In that regard, Goldman downgraded Credit Agrigole SA ACA , Natixis SA KN and Credito Valtellinese CVAL to sell from neutral. Santander SA STD SAN , Allied Irish Bank PLC AIB and KBC Group NV KBC were downgraded to neutral from buy. On the positive side, BNP Paribas BNP was lifted to buy from neutral and Swedbank AB SWEDA was upgraded to neutral from sell -

Morgan Stanley langetab täna Inteli (INTC) 3. kvartali müügitulu prognoosi ning ootab nüüd $10.9 miljardilist tulu vs Inteli poolt hiljuti langetatud prognoosivahemikku keskpunkti $11.0 miljardit.

Lowering Estimates, Remain EW: Following proprietary channel checks and Best Buy commentary indicating worse than expected demand for notebook MPUs, we are trimming our Q3 revenue estimate by $100 million (~1%) to $10,900 million, below the revised guidance midpoint of $11,000 million, and the consensus estimate of $11,052 million, closer to the low end of the guidance range of $10,800 to $11,200 million. We are $0.33 below consensus for CY11 and expect further cuts to consensus, but remain EW due to negative investor sentiment around iPad cannibalization and recent acquisitions. Also, we believe that Intel has a superior product portfolio relative to AMD. -

Lisaks eile avalikustatud 13 joint venture tehingule, teatas IMAX pärast turge juba järgmisest kokkuleppest:

Imax Corp, theater operator, signed its biggest deal in Asia: A subsidiary of South Korea's CJ CGV Co. agreed to install 15 Imax systems in China. Terms weren't disclosed, but Imax said in a late Monday statement that it would "trade a lower up-front fee than we receive in a typical sales deal" for "a larger share of the box office generated" by the theaters. The move gives Imax "increased participation in the growing box office in China, which has more than doubled" in the past two years, Imax said. CJ CGV already operates five Imax theaters in South Korea, Imax said. And under a joint venture the two companies disclosed in March, CJ CGV now has committed to opening a total of 35 Imax theaters, Imax said. Imax overall now has a total of 96 theaters scheduled to be open in China.

Hiina valitsus tahab suurendada riigi kinoekraanide arvu praeguselt 4000-lt 20 000-ni viie aasta pärast ja 40 000-ni kaheksa aasta pärast, sestap on mõistetav ka antud regioon olulisus IMAXi jaoks, kes teise kvartali seisuga opereeris Hiinas kõigest 36 kino.

-

Suurbritannia avaliku sektori võlg kasvas augustis oodatud £12,5 miljardi asemel £15,3 miljardit. Augusti lõpu seisuga on kogu avaliku sektori võlg £934,9 miljardit ehk 64% SKTst. 2009. aasta augustis oli koguvõlg £802,7 miljardit ehk 57,4% SKTst. Alates aprillist ehk uue finantsaasta algusest on eelarve defitsiit olnud kokku £43,5 miljardit. Eelmisel aastal samal perioodil oli defitsiit £49 miljardit.

Enne andmete avaldamist langes naelsterling dollari vastu 0,5%, kuid on praeguseks hetkeks kosunud ja kaupleb $1,5537 juures. -

Kas keegi võiks selle jutu lahti seletada?

Börs muudab kauplemist Tallinna börsil

21.09.2010, 11:09 Lisa kommentaar

NASDAQ OMX Balti börsidel on lähiajal toimumas mitmed kauplemisega seotud muudatused, mis mõjutavad kõiki turuosalisi. Mõlema kirjeldatud muudatuse juures on oluline, et investorid ja teised turuosalised muudatuse sisu ja mõju hinnata ning sellega arvestada oskaksid, teatas börs.

Alates 27. septembrist 2010 võetakse NASDAQ OMX Põhja- ja Baltimaade börsidel kasutusele volatiilsuslimiidid, mille eesmärgiks on vähendada

kauplemisintsidentide ja -anomaaliate esinemise tõenäosust.

Volatiilsuslimiidi rakendumisel peatub kauplemine vastavas tellimusraamatus ning järgneb oksjonieelne periood, mille jooksul tehingute automaatset sobitamist ei toimu. Oksjonieelne periood lõpeb alati oksjoniga ning seejärel taastub tavapärane kauplemine. Volatiilsuslimiit koosneb kahest komponendist:

- Dünaamiline volatiilsuslimiit - rakendub juhul, kui sisestatud

tehingutellimuse hind erineb oluliselt viimase tehingu hinnast (last sale

price). Balti aktsiatel on rakendumisläveks 10%. Oksjonieelse perioodi

pikkuseks on 60 sekundit.

- Staatiline volatiilsuslimiit - rakendub juhul, kui sisestatud

tehingutellimuse hind erineb oluliselt võrdlushinnast (selleks on tavaliselt

avaoksjoni hind). Balti aktsiatel on rakendumisläveks 15%. Oksjonieelse

perioodi pikkuseks on 180 sekundit. Volatiilsuslimiidid ei rakendu, kui sulgemisoksjonini jääb vähem kui 240 sekundit. -

Kreeka võlakirja oksjon läks suhteliselt hästi: müüdi €390 miljoni eest 3-kuulisi võlakirjasid tulususega 3,98% (juulis oli 4,05). Nõudluse-pakkumise suhe oli 6,25 vs 3,85 viimasel oksjonil juulis.

Iirimaa müüs täna €1 miljardi eest 8-aastaseid ja €500 miljardi eest 4-aastaseid võlakirjasid. Tulusused olid vastavalt 6,02% (juuni oksjonil 5,09%) ja 4,77% (maikuus 3,1%).

Euro on hetkel tõusmas: päevane tõus dollari vastu 0,58% ja hetkel kaubeldakse $1,3142 juures ja liigutakse reedel tehtud $1,3160 tipu suunas. -

Sel ajal kui investorid ostavad, tegelevad ettevõtete töötajad aktsiate müümisega. ZeroHedge toob välja, et kui 17. septembril lõppenud nädalal ostsid insaiderid 1,44 mln USD eest 7 erineva USA ettevõtte aktsiaid siis samal ajal müüdi 441 miljoni eest 98 ettevõtte aktsiaid, mis teeb ostetud ja müüdud aktsiate suhteks 290-1. Nädal varem oli see olnud 650-1, seega turgude silmis on toimunud vähemalt paranemine.

-

Lisaks Kreekale ja Iirimaale viis ka Hispaania läbi oma võlakirja oksjoni. Müügis olid 12-kuulised ja 18-kuulised võlakirjad, mida müüdi kokku €7 miljardi eest. Laenamine muutus kallimaks kummagi võlakirja puhul: 12-kuuliste tulusus tõusis 1,836% pealt 1,908% peale ja 18-kuuliste oma tõusis 2,078% pealt 2,146% peale. Eelneval kahel kuul olid tulusused langenud. Nõudmise-pakkumise suhe oli vastavalt 1,7 ja 2,9, mis on kergelt madalamad kui eelmistel kuudel.

-

Kinnisvarastatistika oodatust parem ning ES futuur kauplemas selle peale pisut kõrgemal @+0,15%

August Building Permits 569K vs 560K Briefing.com consensus; M/M +1.8%

August Housing Starts 598K vs 550K Briefing.com consensus; M/M +10.5% -

Gapping down

In reaction to disappointing earnings/guidance: GXDX -9.5%, CAG -7.9%, EXAR -7.0% (ticking lower).

Other news: CBZ -7.2% (announced a $100 mln convertible sr subordinated notes offering), TCAP -6.8% (announced the commencement of a public offering of 2 mln shares of common stock), CYS -6.3% (10 mln shares common stock offering; co intends to invest the net proceeds of the offering in Agency RMBS and for general corporate purposes), CWH -5.9% (announces proposed public offering of 5 mln common shares), HTS -5.6% (Announces Public Offering of 5,000,000 Shares of Common Stock), HCN -5.1% (announces proposed offering of 7,000,000 shares of common stock ), GORO -3.2% (executes $55.6 mln private placement to accelerate production profile and exploration), NOK -3.0% (under pressure following reports that the co is delaying the release of its N8 smartphone), .

Analyst comments: MMYT -5.2% (downgraded to Hold from Buy at Soleil), WFMI -3.7% (downgraded to Underperform from Neutral at Credit Suisse), MWW -1.8% (initiated with a Sell at UBS), SNDK -1.6% (downgraded to Neutral at Sterne Agee), MU -1.4% (downgraded to Neutral at Sterne Agee), SVNT -1.4% (downgraded to Market Perform from Outperform at Leerink), PUK -0.8% (initiated with an Underperform at Exane BNP Paribas ), COL -0.8% (downgraded to Hold from Buy at Argus).

Gapping up

In reaction to strong earnings/guidance: AAWW +8.8%, SWKS +2.1%, FDS +1.7%, AZO +1.1%.

Select European financial related names getting boost following better-than-feared bond auctions: IRE +5.8%, AIB +4.1%, NBG +3.4%.

Select oil/gas related names showing strength: NBR +3.0%, REP +2.4%, E +1.0%, TOT +0.5%.

Other news: ZOOM +19.8% (receives additional 500K units per month order from Beijing Tianyu), TNAV +14.6% (announces amendments to Sprint and Tele Atlas agreements; co guides Q1 in-line, guides FY11 below consensus), DVAX +5.9% (announces $30 mln at-the-market common stock purchase agreement), VVUS +5.5% (announces positive top-line results from a two-year study of QNEXA Controlled Release Capsules, an investigational therapy for treatment of obesity), RNN +4.2% (announces the publication of a research article in on the neuroprotective effects of clavulanic acid, the active pharmaceutical ingredient of Serdaxin), IVR +3.8% (declares Q3 dividend of $1.00, up from prior dividend of $0.74/share; upgraded to Buy at Wunderlich), AIXG +3.0% (still checking), BIOD +2.1% (reports results of Linjeta study versus insulin lispro), HIG +2.3% (also strength being attributed to tier 1 firm upgrade), VRNT +2.0% and NICE +2.0% (Cramer makes positive comments on MadMoney), ASML +1.7% (still checking for anything specific).

Analyst comments: MT +1.5% (upgraded to Buy from Neutral at MF Global).

-

USA futuurid stabiilselt kerget plussi hoidnud. Hetkel ES +0,20%, YM +0,20%, NQ +0,30%. Nafta kaupleb -0,8% @ 74,26 USD ja kuld -0,20% @1276,6USD.

Euroopa turud:

Saksamaa DAX +0,49%

Pantsusmaa CAC 40 +0,71%

Suurbritannia FTSE100 +0,44%

Hispaania IBEX 35 +1,23%

Rootsi OMX 30 +0,63%

Venemaa MICEX +0,95%

Poola WIG +1,07%Aasia turud:

Jaapani Nikkei 225 -0,25%

Hong Kongi Hang Seng +0,11%

Hiina Shanghai A (kodumaine) +0,11%

Hiina Shanghai B (välismaine) +0,48%

Lõuna-Korea Kosdaq +0,12%

Tai Set 50 +1,73%

India Sensex 30 +0,48% -

Rev Shark: The Fed Bazooka

09/21/2010 8:06 AMMost Americans have no real understanding of the operation of the international money lenders. The accounts of the Federal Reserve System have never been audited. It operates outside the control of Congress and manipulates the credit of the United States.

--Sen. Barry Goldwater

Although positive Mondays have been a frequent occurrence since March 2009, the power of the rally yesterday surprised many market players. We have already seen a very big move in the first three weeks of September, and the market had been wrestling with some significant overhead resistance at the August highs, so many investors were ready for a pullback. No particularly positive news kick-started the move, either. Once the buying started, though, the short squeeze kicked in -- along with the anxiety over being left behind -- and it was off to the races.

One of the toughest things about this sort of action is that you just can't apply a lot of logic to it. It's all about feelings and emotions, and in many ways it is actually highly irrational behavior. That is what makes the market such a challenging beast, and also so potentially profitable.

Investors, then, are now back facing a very familiar quandary. The Nasdaq has risen 12 of the last 13 days, and the market has gone from oversold and extremely negative to overbought and very positive. Can we expect this rally to continue much longer? The logical answer is "no," but logic has been proven wrong at least a half-dozen times in the last year or so.

Those with the perma-bull mentality don't have much difficult with their decisions. They simply keep believing that everything is wonderful and that stocks should continue to go up endlessly. Thus, theirs isn't a particularly helpful viewpoint, although -- at times -- it does happen to be the correct one.

The bears argue that this market is irrational -- that it's being artificially inflated, and that it's ignoring all the negatives in jobs, housing and the economy. They say we should be ready for a disaster, as market players will eventually come to their senses and run for the hills. The problem is that their collective timing is terrible. They may be right, but without proper timing the argument is useless.

Of course, the truth is somewhere in the middle. The situation is not nearly as positive as what market is suggesting right now, but it also isn't as gloomy as many of the bears would have you believe. There are currently forces at work providing momentum to the bulls, and we have to respect that and refrain from fighting it, even if we know without a doubt that matters really aren't all that fantastic.

Today, to add to the mix, we will see the latest interest-rate decision and policy statement from the Federal Open Market Committee. We all know the basic line: The economy is improving at a very slow pace, and there are still many obstacles. Still, the Fed does have a bazooka it can use, and that bazooka is known as quantitative easing. This involves little more than running the printing press and dumping dollars into the economy. That money has to go someplace, and one of the easiest places for it to flow is into the stock market.

It does seem the market highly anticipates quantitative easing -- commonly called QE -- to continue. One of the likely reasons stocks have rallied in the last few weeks is the good old saying about how we shouldn't fight the Fed, especially when it will probably use the QE bazooka and keep the cash flowing.

Ben Bernanke has made it pretty clear that this is the Fed's weapon of choice and that they won't be shy about using it, but we can't be certain of whether the Fed will keep on firing it.

So, it basically boils down to an extended and overbought market that could use a rest vs. the Fed's QE bazooka, and today's focus will be on any hints in the policy statement about the extent and timing of further QE. I suspect the market is going to chop around in front of the Fed today, and then react to the perception of what is going to happen as far as this goes.

The key will be watching the dip buyers. They haven't been able to buy weakness for three weeks now, so they have been inclined to buy very shallow pullbacks. If they start to hesitate, then the profit-taking can accelerate, but these players are usually pretty stubborn until some real weakness materializes. Once that happens they tend to lose their confidence quickly, and a slide could follow.

Watch the 1130 level on the S&P 500. That was our old resistance level, and it's now acting as major support. If the index trades back under that area, the bears will quickly proclaim a failed breakout and start to push. However, killing the recent momentum won't be easy.

We're seeing some slight selling in the early going, but it's all about the Fed announcement this afternoon, so we will just have to wait and see what happens.

-

BBC World news telekanalil algas Hard Talk kus hekifondimees Hugh Hendry vastab kysimustele ja pakub, et 80% neist fondidest kaob sest teenida on raske ja huvi nende vastu kaob koos lisaregulatsioonidega. Veidi on kavala olemisega tegelane.

-

SanDisk (SNDK) ticks off the lows; hearing Deutsche Bank out defending.

-

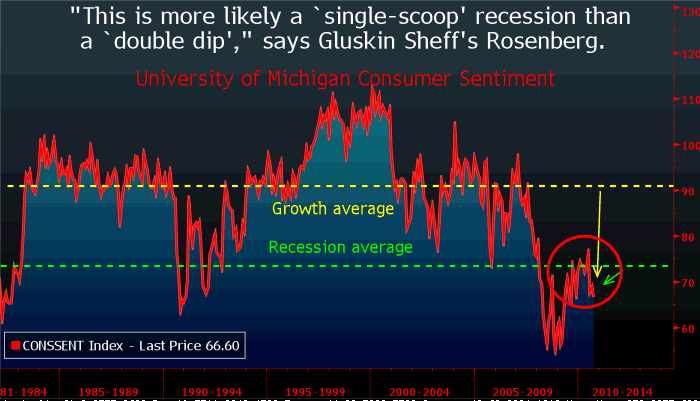

David Rosenberg võttis täna Bloombergis sõna. Ca $5.7 miljardit haldava Gluskin Sheff & Associates hinnangul ei moodusta USA majandus mitte topeltpõhja, vaid hoopiski nii-öelda kulbi kujulist põhja. All on graafik Reuters/University of Michigani tarbijasentimendi indeksist, mis moodustas septembrikuus uue aastasisese põhja ehk indeks langes 66.6 punktile (raport avaldati 17. septembril). Rosenbergi sõnul ei ole USA majandus stagnatsioonist taastunud.

-

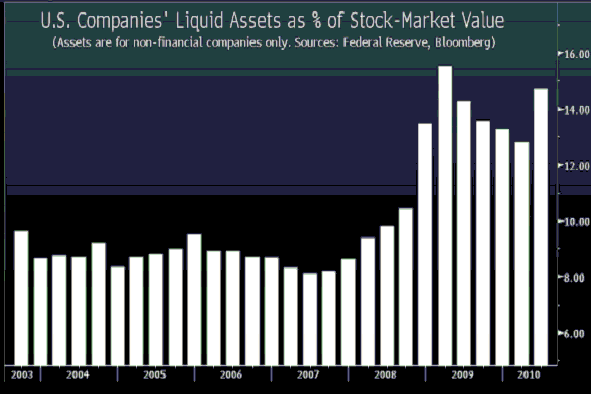

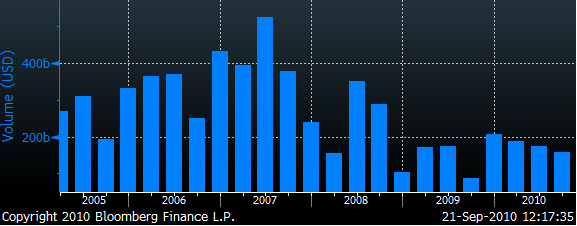

Viimastel kuudel on USA turgudel hüppeliselt kasvanud M&A aktiivsus ning põhjendus on sellele lihtne. Yardeni Research on koostanud alloleva tabeli, mis näitab USA ettevõtete (v.a finantssektor) likviidsete varade osakaalu turukapitalisatsioonist. USA ettevõtetel seisis 30. juuni seisuga bilansis kokku ca $1.85 triljonit, mis moodustas 14.7% turukapitalisatsioonist. Likviidsete varade osakaal kasvas esimese kvartaliga võrreldes 1.9 protsendipunkti.

Käimasoleval aastal on USA ettevõtted kulutanud M&A peale ca $520 miljardit. Viimase 5 aasta M&A aktiivsusest annab hea ülevaate allolev graafik.

-

Barclays usub Apple tulevikku ja nende arust on tänanegi hinnatase atraktiivne. Target $340

Barclays continues to believe Apple's valuation is very attractive and that shares can benefit driven by strong iPad demand, a new iPhone upgrade cycle, significant international expansion and a pipeline of new innovations. Firm reits their Overweight and $340 tgt. -

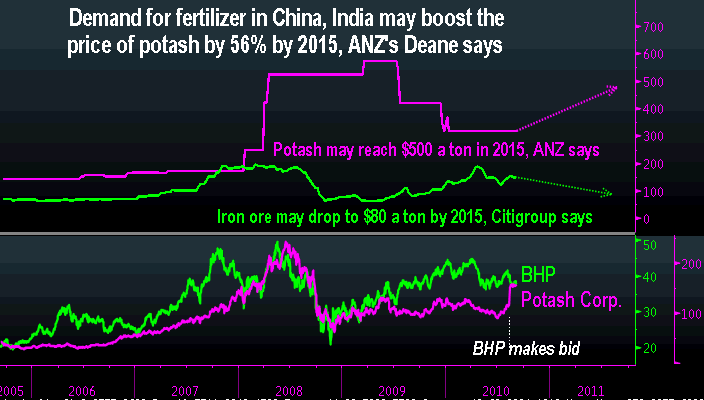

Finantsportaalis ilmus 17. augustil lugu Potash’ist, mida saab lugeda siit.

Australia & New Zealand Banking Group sõnul on Potash väärt oluliselt enam, kui $40 miljardit. Allolev graafik näitab kaaliumkarbonaadi ja rauamaagi hindu. ANZ sõnul võib kaaliumkarbonaat tänu Hiina ja India kasvavale nõudlusele maksta järgmise nelja aasta pärast ca $500 meetertonni kohta. ANZ sõnul ei avata enne 2015. aastat maailmas ka ühtegi uut suurt kaevandust, mis hindu allapoole tuua võiks. Samas prognoosib Citigroup, et rauamaagi hind võib aastal 2015 maksta praeguse $147 asemel hooposki $80. Kui tugineda nendele prognoosidele, siis on selge, miks BHP Billitonil on kibekiire tegevise mitmekesistamisega.

-

Mis asi on meetertonn?

Tõenäoliselt tõlge väljendist metric ton(ne), kus metric tähistab kümnendsüsteemi ehk siis tegemist on lihtsalt tonniga.

Või ma eksin? -

FOMC leaves fed funds rate at 0.00-0.25%, as expected

FOMC continues to anticipate that economic conditions are likely to warrant exceptionally low levels for the federal funds rate for an extended period -

Ostuöö

-

10-yr yield falls below 2.60% for the first time since September 2

-

Prudential (PRU): Headlines passing that co may buy two Japanese units from AIG; shares rally to HoD

-

Spot gold pushes to record high of $1290.35/oz