Börsipäev 6. oktoober

Kommentaari jätmiseks loo konto või logi sisse

-

Oodatust parem teenustesektori ISM ning lootus, et FED kavatseb vagunit täiendavalt veel tagant lükata tekitas eile USA turgudel korraliku ostuhuvi ning seda enam kui kahe kuu kõrgeimate käivete juures. Kui septembris võis näha päevasid, mil NYSE käive oli 3,5 miljardit aktsiat, siis teisipäeval vahetas omanikku 4,9 miljardit aktsiat. S&P 500 indeks sulgus 2,1%, Dow Jones +1,8% ja Nasdaq 2,4% kõrgemal. Dollar jätkab aga võimaliku QE valguses odavnemist, kaubeldes euro suhtes kaheksa kuu madalailmal tasemel ($1,385), vedades kulla hinda iga päevaga uute rekorditeni (hetkel 1346USD).

Aasia indeksid on pärast USA sessiooni samuti kõrgemal kauplemas: Nikkei 225 +1,7%, Hang Seng +1,1%, S&P/ASX 200 +1,8%. USA futuurid liikumas hetkel 0,1% kuni 0,2% plusspoolel.

Tänastest makrouudistest on tähtsamad eurotsooni teise kvartali SKT teine hinnang (kl 12.00), mille osas suuremat revideerimise riski ei tohiks olla. Saksamaa augustikuu töötleva tööstuse tellimuste number tehakse aga teatavaks kell 13.00 ning konsensus ootab pärast ootamatut -2,2%-list langust juulis kuu baasil 1,0%list kasvu. USA-s aga jälgitakse septembrikuu erasektori tööhõive muutust (kl 15.15), et saada veidikenegi aimu, milliseks võib pilt kujuneda reedese tööjõuraportiga.

-

Samal ajal kui investorid on aktsiaid kokku ostmas, kasutavad insaiderid juba mitmendat nädalat seda võimalust müümiseks. Zerohedge tõi eile välja, et kui eelmisel nädalal oli müüjate-ostjate suhe 1411-1 siis sel nädalal juba 2341-1 (ost 177K USD vs müük 414 mln USD), mis peaks kvartalitulemuste eel kahtlemata ettevaatlikuks tegema. Näiteks Oracle, kelle hiljuti avaldatud tulemused olid tublisti üle ootuste ning lisaks anti konsensust kõrgem Q2 käibeprognoos, siis 52 nädala tippudel kaupleva aktsia valuatsioon annab juhtidele põhjust müüa. Teist nädalat järjest on ORCL insaiderid müüjate nimekirja eesotsas olnud...eelmisel nädalal müüdi $223 mln ja see nädal veel $135 mln väärtuses aktsiaid. Lähemalt uurida siin

-

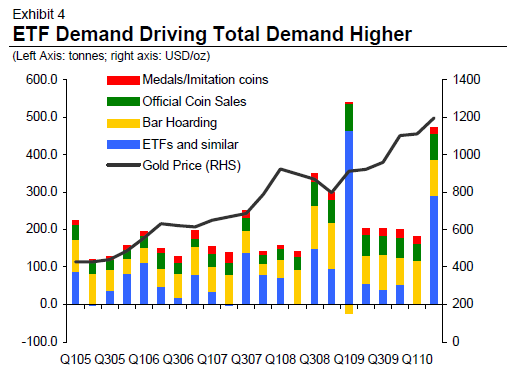

FED-i võimalik rahatrükk ning sellest tulenev dollari nõrkus on ajendanud Morgan Stanley't tõstma kulla 2011. a baasprognoosi 14,3% kõrgemale 1315 USD peale ning bull-case stsenaariumi puhul koguni 1512 dollari peale. Kulla suurenenud nõudluse taga on eelkõige investeerimisnõudlus, mis 2002. aastal moodustas kogunõudlusest 14%, kuid küündis 2009.a juba 41%-ni.

With the Fed indicating that current US economic conditions (including low rates of resource utilization, subdued inflation

trends and stable inflation expectations) warrant “exceptionally low levels for the federal funds rate for an extended period,” we

expect that investment demand will now strongly support high gold prices for longer than we previously anticipated. Consequently, we are forecasting that gold investment demand, as a share of total gold demand, will rise further, to 46.9% in 2010 and 48.9% in 2011, as a direct consequence of this increased demand for hybrid assets.

-

Eurotsooni teise kvartali SKT numbritesse muutusi ei tulnud: aasta baasil kasvas 16 riigi majandus 1,9% ja kvartali baasil 1,0%.

-

Samal ajal kui vasakul ja paremal keskpangad majanduse stimuleerimisega jätkavad või vähemalt seda tõsiselt kaaluvad siis Euroopa keskpank on sellel rindel jäänud oma kolleegidest oluliselt konservatiivsemaks, suunates pilgu rahapoliitika edasise normaliseerimisele. See aga aitab eurol edasi tugevneda, ähvardades paraku regiooni majanduskasvu pidurada.

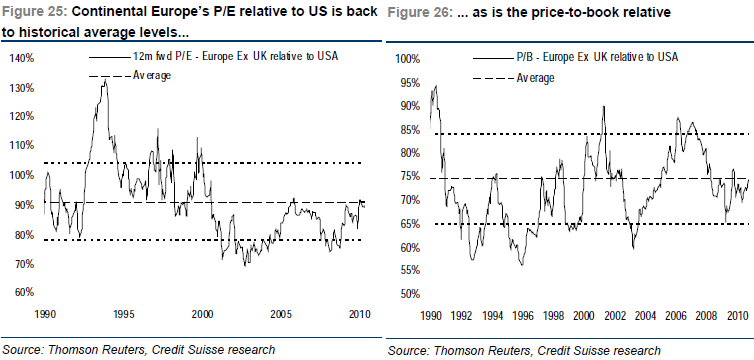

Mais tõstis Credit Suisse kontinentaal-Euroopa soovituse overweight tasemele, kuna hindas euro tuleviku osas valitsevanud hirmu ülereageeringuks. Alates sellest hetkest on antud regioon MSCI World indeksi tootlust ületanud 10%, ent nüüd otsustatakse alljärgnevatel põhjustel osakaalu taas benchmarki juurde langetada.

(1) Euro strength and QE2. We calculate that since its June low, the 7% rise in euro trade-weighted has reduced real GDP by 0.5%, nominal GDP by 1.0% and EPS by 8%. Moreover, the strong euro increases deflationary pressures and thus sovereign risk in peripheral Europe. The US and the UK are likely to implement QE2 by year-end and Japan has announced QE, while the ECB is

potentially withdrawing liquidity; thus the risk is the euro overshoots (€/$ 1.45-1.50). The strong euro has already led to a peak in relative earnings momentum(2) Economic momentum relative to other regions has just peaked. The record gap between European and US consumer confidence is likely to close. Continental Europe is tightening fiscal policy by marginally more than we

anticipated, while the US and Japan are doing signficantly less. Aggregate leverage in Continental Europe has risen to be above that of the US. European consumer confidence and EPS tend to lag the US by 13 months and 9 months, respectively.(3) Sovereign risk. Continental Europe relative performance and the euro have decoupled from rising sovereign CDS spreads.

(4) Sentiment is no longer depressed. Risk appetite is now at neutral levels, compared to extremely low levels in May (1 st dev below average). Relative inflows are back to neutral levels.

(5) Valuation is now neutral on P/B, P/E and sector-adjusted P/E relatives, while they were at clearly cheap levels in May.

(6) Politics: many countries have weak coalitions/minority governments (the Netherlands, Belgium, Italy, Spain, Portugal and Ireland), potentially limiting structural reform.

-

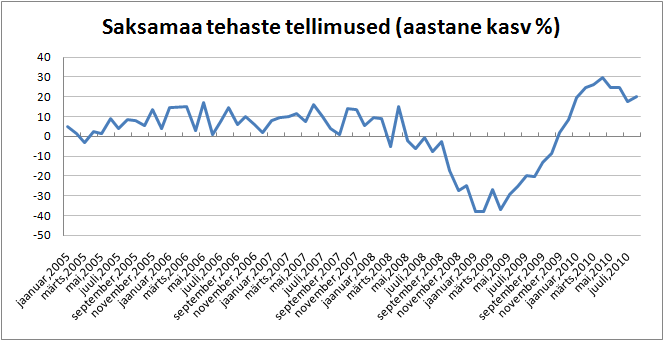

Saksamaa tehastetellimused kujunesid ootustest oluliselt tugevamaks, millele lisaks revideeriti juulikuu langust väiksemaks. Augustikuu aastaseks kasvuks kujunes 20,3% vs oodatud 17,2% (juuli revideeriti 17,7% pealt 18,4% peale) ning kuu baasil suurenesid tellimused 3,4% vs oodatud 0,9% (juuli revideeriti -2,2% pealt -1,6% peale). Euro käis selle peale $1,388 tasemel, kuid nüüd on pisut järgi andnud.

-

IRELAND'S RATING CUT TO A+ BY FITCH; OUTLOOK NEGATIVE

-

MBA Mortgage Applications out at -0.2% vs. -0.8% prior read

-

Kedagi ehmatas Iirimaa reitingu langetus päris ära.

10.a võlakirjade yield...

-

Toyota ütles, et kavatseb pakkuda Lexuste ostjatele kuni $3000 suurust allahindlust ning toetada ostjaid liisingumaksetel. Lexus, mis on valitsenud USA luksusautode turgu rohkem kui kümme aastat on selle aastal müünud vähem sõidukeid kui Mercedes. Lexuse müük on kasvanud sellel aastal 8.7% vs üleüldise turu kasv 10.3%.

Iseasi muidugi, kas $3000 suurune toetus suurendab Lexuste müüki, sest praegu on keskmine mudelite alghind ca $54 000, kõige odavama Lexuse alghind on $32 145.

-

Sept. ADP Employment Change -39K vs +18K Briefing.com consensus; prior -10K

-

USD/JPY kukkus läbi ¥82,86 taseme, mis tähistas jeeni jaoks 15 aasta tippu. Tänane põhi on hetkeseisuga ¥82,78. Jaapani keskpank paiskas 15. septembril müüki 2,2 triljonit jeeni.

-

USA 10. aastase võlakirja yield on ADP peale liikunud 2,45% pealt 2,41% peale 2009.a jaanuari tasemele

-

Gapping down

In reaction to disappointing earnings/guidance: EQIX -25.6% (also downgraded by multiple analysts), DMND -5.8% , COST -2.2%, YUM -1.0%.

Select EQIX peers are trading lower in sympathy: SVVS -9.8%, RAX -8.4%, TMRK -6.3%.

Other news: WL -8.4% (seeing continued weakness; Hearing attributed to reports that the co is trying to raise capital), GMR -5.2% (announces amendment to $372 mln syndicated credit facility), UTA -4.9% (appoints new independent audit firm), CHSP -4.7% (announces proposed public offering of 6.5 mln common shares ), SLG -4.5% (operating partnership announces exchangeable senior notes offering), MTB -2.9% (Allied Irish Banks confirms proposed disposal of the M&T shareholding), ERIC -2.2% (traded lower overseas), ALTR -1.9% (early weakness attributed to tier 1 firm downgrade), OPEN -1.8% (Cramer makes cautious comments on MadMoney), BBVA -1.1% (trading ex dividend).

Analyst comments: FFIV -2.6% (downgraded to Neutral from Buy at Gleacher), CGNX -2.6% (light volume; downgraded to Neutral from Overweight at Piper Jaffray), ONNN -2.3% (downgraded to Neutral from Outperform at Credit Suisse), PCX -1.5% (downgraded to Hold from Buy at Brean Murray), JCP -1.4% (initiated with Underperform at FBR), TSO -1.3% (downgraded to Underperform from Market Perform at Raymond James), TLB -1.3% (downgraded to Underweight from Neutral at Piper Jaffray), CMG -1.1% (downgraded to Hold from Buy at Deutsche Bank), IRM -0.9% (downgraded to Market Perform from Outperform at Wells Fargo).

Gapping up

In reaction to strong earnings/guidance: OMEX +8.3%, MON +1.8%, FDO +1.0% (light volume).

M&A news: CRXL +1.1% (Crucell N.V. and Johnson & Johnson reach agreement on intended public offer of EUR24.75 per ordinary share of Crucell).

Select financial related names showing strength: NMR +4.9%, NBG +3.8%, IRE +3.0%, UBS +1.4%, DB +1.2%.

Select metals/mining stocks trading higher: RTP +1.8%, BBL +1.6%, BHP +1.4%, GG +1.0%, MT +0.9%, SLW +1.0%.

Select oil/gas related names showing strength: STO +2.5%, E +1.6%, SDRL +1.1%, DVN +0.8%, RIG +0.8%, BP +0.7%.

Other news: VITA +10.8% (ticking higher; announces presentation of Cortoss 24-Month pivotal study results), HAWK +9.4% (entered MOU with Essar Oilfield Services India for the sale of drilling rig Seahawk 2505), JASO +5.7% (Announces Supply Agreements With BP Solar for More Than 185 MW), GNVC +5.1% (receives second-year funding from SAIC for HIV and influenza vaccine development), NOK +1.9% (still checking), BT +1.8% (continued strength), AMSC +1.6% (announced that it has received the world's largest order for high temperature superconductor wire), CLX +0.7% (Cramer makes positive comments on MadMoney).

Analyst comments: MXIM +2.6% (upgraded to Outperform from Neutral at Credit Suisse).

-

USA futuurid on pärast ADP-d nulli lähedal liikunud, hetkel ES 0,11%, YN +0,13%, NQ -0,1%

Euroopa turud:

Saksamaa DAX +0,60%

Prantsusmaa CAC 40 +0,79%

Suurbritannia FTSE100 +0,63%

Hispaania IBEX 35 +0,65%

Rootsi OMX 30 +0,31%

Venemaa MICEX -0,29%

Poola WIG +0,17%Aasia turud:

Jaapani Nikkei 225 +1,81%

Hong Kongi Hang Seng +1,07%

Hiina Shanghai A (kodumaine) suletud

Hiina Shanghai B (välismaine) suletud

Lõuna-Korea Kosdaq +0,77%

Austraalia S&P/ASX 200 +1,73%

Tai Set 50 +1,27%

India Sensex 30 +0,66% -

Rev Shark: The Taste of Victory

10/06/2010 8:16 AMThe most dangerous moment comes with victory.

-- Napoleon BonaparteThe bulls had a clear victory on Tuesday. We had a classic breakout as we finally moved through the 1150 area with decisiveness. We look well positioned for further upside, but it could be dangerous if we are too overconfident.

The main characteristic of Tuesday's move was that so many market players were unprepared for it, as they had become more negative when the market had struggled on Monday. It was a good example of the market's ability to frustrate as many as it can. A lot of folks are still poorly positioned, and that bodes well for the bulls.

Technically, it is pretty clear sailing to the upside now. There is some minor resistance around 1175, but then it's the April levels, which are the highs of the year, that come into play. It would take quite a big move to jump that high, but the path is clear, and good earnings and QE II could provide the fuel that the bulls need to make it there.

Let's not get too far ahead yet, though, as the first order of business is to build on yesterday's strong action. The bulls need to follow through to show they mean business and to let the bears know that Tuesday wasn't just a one-day wonder.

We are a little overbought now and could use consolidation, so we don't need to have a big point gain. If we just hold fairly steady and not give back very much, the power of the uptrend will remain intact and will attract more momentum.

At this point, the bears' best hope is that we have lousy employment numbers on Friday. Even if we do, the problem is that it will increase the potential for another round of QE II. Fed member Evans made it quite clear in comments yesterday that he views the terrible job market as an excellent reason for the Fed to keep pumping up the liquidity.

Technically, there just isn't any compelling reason to be bullish right now. We had a decisive breakout and there is plenty of room to run to the upside. It is possible that we could reverse quickly, especially if we had some poor news, but that doesn't look like a very high-percentage bet.

The trick isn't to just be bullish, but to find the best places to put your money. The performance-chasing fund managers are going to go from the big-cap names like Apple (AAPL - commentary - Trade Now), Baidu (BIDU - commentary - Trade Now), Google (GOOG - commentary - Trade Now), Amazon (AMZN - commentary - Trade Now), etc. The momentum chasers will stick with things like F5 Networks (FFIV - commentary - Trade Now) and Chipotle (CMG - commentary - Trade Now). Small caps underperformed a bit so if that is your choice of vehicle you need to be particularly selective.

We have some slight weakness to start the day, which will be a good test of the dip buyers, who never had much of an opportunity yesterday. I'll be very surprised if we see a strong reversal today, although some consolidation and a slight pullback would be the perfect way for the market to rest.

-

Brian Sack, a senior official at the New York Fed, had this to say about the powers of quantitative easing in a speech he just delivered:

Nevertheless, balance sheet policy can still lower longer-term borrowing costs for many households and businesses, and it adds to household wealth by keeping asset prices higher than they otherwise would be.

:::::::::::::::::::::::::::::::::

Tule taevas appi! -

10-yr yield falls to 2.380%, 2-10-yr spread flattens below 200

-

Japanese yen touched a 15-yr high of 82.76 againt the dollar

-

National Retail Federation andmetel kasvab pühadehooaja jaemüük käesoleval aastal 2.3%, ulatudes $447.1 miljardini. Kuigi see jääb alla 10 aasta keskmisele, mis on 2.5% suurune kasv aastas, on tegu siiski parema näitajaga kui eelmise aasta 0.4%line kasv ja 2008. aasta 3.9%line langus. (link)

-

Netflix: Hearing initiated with an Underperform at boutique firm

Janney Montgomery andnud samuti täna SELL ja targetiks $110 -

Fitch Assigns Initial 'BB-' IDR to General Motors; Outlook Stable

-

TiVo jumps over a point; confirms United States Patent and Trademark Office has reaffirmed the validity of all claims of the Time Warp Patent at issue in the second reexamination of the patent at the request of EchoStar

-

Homme algab ametlikult 3. kvartali majandustulemuste hooaeg, kui avalöögi teevad Alcoa (AA) ja PepsiCo (PEP). UBS analüüsimaja kirjutas täna avaldatud analüüsis, et algaval 3. kvartali tulemuste hooajal tõstavad oodatust paremad tulemused tugevalt aktsiahindasid. Alloleval graafikul on kujutatud S&P 500 indeksisse kuuluvate ettevõtete FY 2011 EPS konsensusootus – trend on selgelt allapoole. UBS analüütikute sõnul kujuneb 3. kvartali tulemuste hooaeg suurepäraseks (eks me varsti saame teada).

-

Bloombergis tehakse juttu ühest huvitavast IPOst.

Ellington Financial on MBS’idesse investeeriv fond, mis plaanib IPO käigus tõsta $108 miljonit kapitali, müües seega 4.5 miljonit aktsiat. Turgudele on levinud aga uudis, et esimese müügipäevaga on investorid ostnud koguni 75% aktsiatest hinnaga $22 kuni $24. Homme ostetakse ilmselt ka veel olemasolevad aktsiad