Börsipäev 13. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Rev Shark:

Don't Shortchange the Power of Emotions

12/13/04 8:31 AM ET"The best and safest thing is to keep a balance in your life, acknowledge the great powers around us and in us. If you can do that, and live that way, you are really a wise man."

-- Euripides

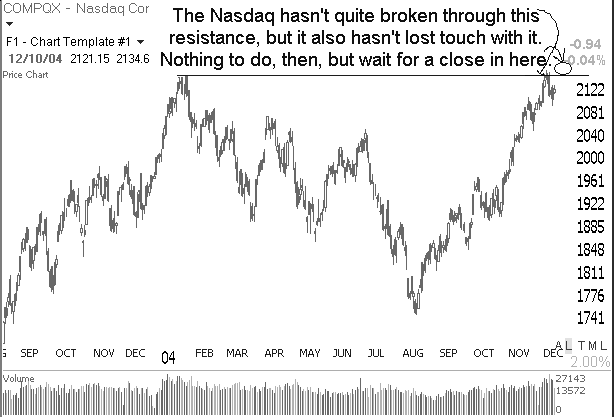

It becomes increasingly difficult to maintain a balanced view of a market that has made major moves since mid-August and are levitating just off their highs. The bears become more convinced that we are on the eve of destruction while the bulls become increasingly comfortable that nothing bad can happen and are even more inclined than usual to ignore even reasonable concerns.

In an environment like this, our job, more than ever, is to maintain balanced thinking and strive to understand both the bullish and bearish cases. Cold hard objectivity is never easy but it is even tougher when we are both financially and emotionally invested in one particular viewpoint.

Doug Kass over on Street Insight has done a good job setting out the bearish arguments. A mediocre economic recovery, struggling consumers, poor retail sales, interest rate pressures, overconfident market participants, the weak dollar, high valuations and so on are all reasons to be worried, according to Doug. As is generally the case, the bears sound pretty darn reasonable and logical.

The bullish case is much more difficult to appreciate, especially because it is premised more on the emotions of investors, rather than on fundamental arguments. Jim Cramer does a good job of discussing the emotionalism that helps support the market now. There are underinvested bulls, money managers hungry for performance points against their benchmarks, and positive seasonality supporting the market. One of the easiest things to overlook is the great power of momentum. Newton's law that objects in motion tend to stay in motion applies to the market as well as the physical world.

When we compare and contrast the arguments of the two sides, the thing that sticks out the most is that the bearish arguments are not conducive to accurate timing while the bullish case is much more short-term-orientated. We certainly can find things to worry about if we like, but it is extremely difficult to accurately guess when the broader market may start to worry about these things as well.

We need to balance our legitimate worries about fundamentals against the realities of the current market momentum. Neither should be underestimated, which means we have to stay particularly attuned to signs that the mood of the market may be changing.

As we start the week the bulls are feeling confident once again. The saga of Peoplesoft (PSFT:Nasdaq) and Oracle (ORCL:Nasdaq) is coming to an end, Nextel (NXTL:Nasdaq) is likely to be acquired, crude oil remains soft, the dollar is slipping a little and overseas markets are mostly higher. The big economic news this week is the FOMC interest rate decision on Tuesday at 2:15 p.m. EST. A rate hike is expected but as always the decision will stir up some emotions.

Gary B. Smith:

-

Gapping Up

PSFT +10.4% (agrees to be acquired by ORCL), ORCL +6% (reports NovQ, to buy PSFT), NVEC +13% (completes biosensor program phase), SJH +8% (to be acquired for $48/sh), GEPT +16% (receives order for 12 onboard aircraft surveillance systems), QTWW +12% (started with a Buy at Merriman), IMOS +7.6% (RBC upgrade), DSCO +7.4% (announces positive clinical data for Surfaxin), NGPS +6.8% (recent momentum), SIRI +6.7% (to be added to Nasdaq 100), HYGS +6.7% (to design and build a Hydrogen Generation System), JOBS +5.7% (continues Friday's momentum), IMAX +5.7% (guides higher, settles litigation with UCI), DNDN +4.7% (co's immunotherapy shows promise in advanced breast cancer), OSTK +4.5% (started with an Overweight at Lehman; tgt $90), TIBX +4.3% (Jefferies upgrade), AH +4.3% (US Army rushes to harden Iraq-bound vehicles - Reuters), TASR +3.8% (announces report describing Tasr's safety), TIVO +3.4% (The Ellen DeGeneres Show to give DVRs to audience)... Under $3: FTGX +14% (to buy Con Ed subsidiary for about $37 mln cash), MBAY +9.5% (announces deal with HarperCollins Publishers to offer downloadable audiobooks), AAC +7.4% (Ableauctions.com guides), CMGI +7.1%, IVAN +6.6% (Operations start at oil plant).

Gapping Down

ABTLE -23% (withdraws Y04 EPS guidance, Merriman downgrade), TUES -18% (guides lower), CAH -11% (announces global restructuring plan, cuts Y05 guidance), OVTI -3.5% (cut to Neutral at Next Generation following SEC inquiry disclosure), DITC -2.9% (First Albany downgrade)... Under $3: ULTE -55% (seeks to delay 10-Q filing), CNXT -10% (lowers guidance). -

arkok, kas tegemist on Sinu enda analüüsiga gappide põhjustes või on tegemist copy-pastega kuskilt veebist? või enda koostatud gappijate headlined lühivormis?

-

copy-pastega Briefing.com lehelt, tegemist on tasulise infokanaliga

-

Sama asi täiesti saadaval ka yahoo lehel

http://finance.yahoo.com/mp -

Raymond Jamesi Chief Market Strategist Jeff Saut kirjutab oma klientidele täna hommikul nii:

"...Late October to mid-December of 2004 has been a pretty good year! More than 900 Dow Wow points have been gained since the "bear trap" reversal low of October 25th. At that rate of gain, the DJIA will be over 17,000 a year from now. This only on Wall Street enthusiasm, which is now past its 25th day maximum performance peak and may soon find its near-carnival-like atmosphere threatened by this week's almost assured FOMC rate ratchet...."

- Turg avanes tugevalt ülespoole, saades toetust viimaks ometi toimunud PSFT + ORCL tehingust. Siis aga hakkas nafta seni teadmata põhjusel tugevnema ning pullid lõid araks. Praeguseks hetkeks on indeksid suurema osa hommikusest tugevusest tagasi andnud. Kukkumise hõngu oli tegelikult tunda juba eelturul, kuid headele uudistele rohkelt müüjaid leidus. Keskmise persp. sentiment on siiski jätkuvalt positiivne. Dollar on euro vastu veidi maad kaotamas jälle, kuid veel hetkel keegi sellele erilist tähelepanu ei pööra.

- Võiks ju öelda, et Tenet Healthcare (THC) pakkus neg. üllatuse aga pikemaajalised jälgijad on ilmselt juba selliste liikumistega harjunud. THC ei maalinud 2005. aasta suhtes eriti optimistlikku pilti aga eks seda oli ju ka oodata. Põhjus viimaste nädalate tõusu taga? Tuleb välja, et seda eriti polegi. Olen ise jätkuvalt THC aktsiate omanik.

- Märkasite, et Conexant (CNXT), mis andis hommikul hoiatuse on jälle plussi roninud?

- 3Com (COMS) ostis ära võrguturvalisusega tegeleva TippingPoint Techi (TPTI). Päris suur amps! INTZ, ISSX ning SNWL samas sektoris.

- Netflix (NFLX) jälle plussis! Tundub, et suur short interest teeb oma tööd? Roth Capital tõstis üle pika aja firma reitingut, kuid ülejäänud seltskond on jätkuvalt neg. LHV Pro soovitus.

- HealthTronics (HTRN) tõusis reedel üle 10% nign on ka täna siiani rohelises olnud. Homme toimub firma analüütikute päev ning Piper Jaffray tõstis selle eel oma hinnasihi $11 peale varasema $9 asemel.

- Sirius Satellite (SIRI) käive täna nõrgapoolne. Huvi hakkab vaibuma?

sB -

Omnivisionil (OVTI) probleeme sensoritega, huvitav kui tõsine asi on.

-

SEC-ga pigem siiski.

sB