Börsipäev 29. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

Täna kell 15.30 teatatakse USA 1. kvartali esialgne SKP näit. Keskmine ootus on -4.7%, kuid erinevate analüüsimajade näidud kõiguvad ausalt öeldes ikka seinast seina. Föderaalreservi ütelused intressimäärade ja võlakirjade ostmise ning majanduse stimuleerimise teemadel tulevad kell 21.15.

Tänased tähtsamad tulemuste avaldajad enne turgu on WYE, BHI, GD, HES, RDS.A, MT jt. Pärast turgu tulevad SBUX, V ja FSLR. -

Tulemuste tabel jätkab uuenemist ja soovitan pilku peal hoida siin.

-

Kui eile räägiti C ja BACi kapitali kaasamise vajadusest, siis tänaseks on selgunud, et stress-testi tulemustega kursis olevate inimeste sõnul võivad lisakapitali vajada juba kuus panka. Elame-näeme.

-

Seeking Alpha vahendusel pilt sellest, milliste riikide vahel jaguneb USA välisvõlg:

-

Bespoke on võtnud kokku turu reageeringud peale Fedi kohtumisi alates karuturu algusest:

-

Tänan selle tüütu tableti-foorumiteema kustutamise pärast! :) Ja just seetõttu, et see kustutamine kaotas ühtlasi ka minu hasardi lollustele vastu vaielda.

-

ole mureta ttrust, tabletikas juba küsis seebi teemas Alo meiliaadressi, niiet to be continued

-

:( Kurb.

-

Alo ei pea ju talle vastama :-D

-

USA 2009. aasta 1. kvartali SKP -6.1% vs oodatud -4.7%.

-

Nadi, aga turud väga hullult ei reageeri.

-

Nagu hommikul ütlesin, kõiguvad analüüsimajade poolt välja käidud SKP ootused seinast seina. Näiteks Deutsche Bank ootas täna -8.0%list näitu...

-

DB on USA makronäitajate osas konstantselt üks pessimistlikumaid olnud.

-

Kui Q3 08 oli eratarbimine -3.8% ja Q4 08 oli -4.3% (viimase 60 aasta jooksul polnud USAs kahte järjestikust vähemalt 3%lise langusega kvartalit olnud), siis Q1 09 oli see +2.2% - enam kui kaks korda parem tulemus oodatud +0.9%st.

-

A 23-month-old child from Texas has become the first to die from swine flu outside Mexico.

-

USA aktsiaturud avanevad pea protsendi jagu plusspoolel.

Saksamaa DAX +0.99%Prantsusmaa CAC 40 +1.34%

Inglismaa FTSE 100 +1.51%

Hispaania IBEX 35 +2.18%

Venemaa MICEX +1.34%

Poola WIG +2.90%

Aasia turud:

Jaapani Nikkei 225 N/A (börs suletud)

Hong Kongi Hang Seng +2.76%

Hiina Shanghai A (kodumaine) +2.78%

Hiina Shanghai B (välismaine) +2.73%

Lõuna-Korea Kosdaq +3.15%

Tai Set 50 +2.52%

India Sensex 30 +3.65%

-

Individual Stocks Regain Their Importance

By Rev Shark

RealMoney.com Contributor

4/29/2009 8:43 AM EDT

There is no security on earth, only opportunity.

-- Douglas MacArthur

The markets are set for a positive open this morning after some struggles yesterday. Nothing specific is driving the bounce, but we have first-quarter GDP figures and the FOMC interest rate decision today to serve as potential catalysts. Neither event is anticipated to be particularly significant, but this market has seen a strong inclination toward favorable reactions, and it looks like we are doing that this morning.

Although the indices were quite mixed yesterday, a high level of speculative action continues to roil under the surface. Traders are feeling confident and are seeking out action. This is quite different than what we saw for many months during the bear market, where a long-side trade in a stock would be nothing more than an intraday flip -- there were no sustained pockets of momentum to be found at all, and no real leadership.

That has changed, and right now the psychology is much more supportive of the trading of individual stocks for more than just a few minutes. Charts are developing better setups, and we are seeing the sort of action that we typically saw in bull markets.

I'm still not convinced that the bear market has ended, but at least for now the nature of the trading is much improved. I have been slow to embrace that, but all we can ever do in the market is focus on what is in front of us and put aside the thinking and emotions we had in the past.

My game plan now is simply to focus on trading in individual stocks and not to be quite as concerned about the major indices. We've had good opportunities in individual names lately, regardless of the big picture; that's what happens in healthy markets. Good stocks continue to act well even when the macro concerns are popping up. We aren't seeing the whole market suffer as a consequence of poor economic news, and that sure makes for some better trading.

I do think the market is unlikely to make much more progress in the near term, but a trading range would be very healthy and should still provide us with plenty of trading opportunities. It will be much more a stock-picker's market, but that is what we are trying to do here, so that isn't so bad.

We have a good start setting up, but the FOMC interest rate decision later today will likely jerk us around even if they don't make any changes in policy.

Good luck and go get 'em.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: MED +23.9%, CBI +15.4%, HA +14.6%, DWA +14.3% (upgraded to Buy at Lazard Capital Mkts), PSYS +13.2%, SLAB +12.1%, WYN +11.3%, JNY +10.9%, RGR +10.4%, DVAX +8.7%, Q +7.8%, LIFE +7.7%, AMX +7.6%, MPWR +6.5%, SI +6.5%, TWX +5.6%, STD +5.3% (light volume), SNY +4.4%, ZRAN +3.0%... Select financial names trading higher: RBS +11.5%, CIT +7.8%, FIG +7.5%, KEY +7.4%, BCS +7.0% (upgraded to Overweight at HSBC), C +6.6%, UBS +4.1%, BAC +3.9%, WFC +3.6%, AIG +3.0% (has moved to stave off the risk of default on $234 bln of derivatives by persuading a senior executive to rescind his resignation - FT), JPM +1.4%... Select metals/mining names showing strength: AAUK +6.9%, RTP +4.1%, BHP +1.8%... Select airlines rebounding: AMR +5.1%, DAL +5.0%, CAL +5.0%, JBLU +4.9%, LCC +2.3%... Other news: DNDN +126.9% (resumed trading after conf call; was halted intraday following 15+point drop; also upgraded by several analysts) ELN +12.3% (announce results of a study demonstrating that TYSABRI promoted regeneration and stabilization of damage done to the myelin sheath), CSIQ +9.9% (still checking), AUXL +8.9% (announced that the FDA has accepted for filing and granted priority review status to its BLA for XIAFLEX), TS +3.2% (still checking)... Analyst comments: UFS +6.9% (upgraded to Outperform from Sector Perform at RBC Capital Mkts), SQNM +1.7% (initiated with Buy at Auriga).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: ETFC -24.8% (also downgraded to Underperform at FBR Capital Markets), ROC -14.3%, VFC -9.5% (also downgraded to Neutral from Positive at Susquehanna Financial), CBAK -9.3%, MTG -9.1%, AET -8.0%, VPHM -8.0%, BWLD -7.6%, TXT -7.6%, TSS -7.6% (also downgraded to Market Perform at JMP), PMTC -7.4%, PNRA -5.7%, CRI -5.3%, CERN -5.0%, ZEUS -4.7% (light volume), CNP -4.6%, MT -4.4% (also proposes common stock, convertible note offering - DJ), WTS -3.8% (light volume), RFMD -3.8%, SAP -3.7%, GT -2.8%... Select drug and infectious disease related names pulling back: NVAX -6.3%, APT -5.7%, BCRX -4.3%... Other news: UTHR -1.4% (U.S. Food and Drug Administration extends action date for inhaled treprostinil (Tyvaso) new drug application by three months)... Analyst comments: M -2.6% (downgraded to Neutral at JPMorgan). -

Kui märtsi keskel kukkus USA valitsuse 10-aastase võlakirja tulusus Föderaalreservi massiivse võlakirjaostude teate peale 3% pealt 2.5% peale, siis tänaseks oleme viimase 5 kuu tippude ehk 3% alla tagasi jõudnud. Võlakirja tulususe tõusust võidab võlakirju võimendusega lühikeseks müüv Pro alt tuttav TBT.

-

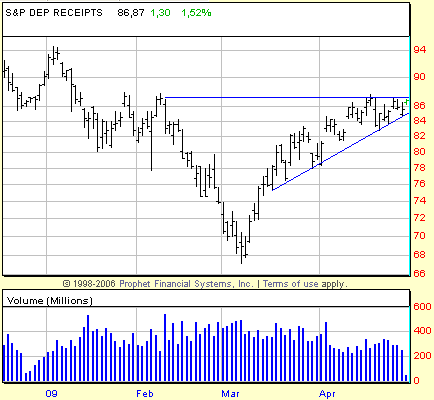

Tõsine ralli käimas turgudel, kuid ometi ei ole me jõudnud kaugemale kui taaskord selle juba mainitud vastupanutaseme alla.

-

QQQQ on samuti tehniliselt kenasti 200 päeva keskmise all. Poleks mingi ime, kui enne suvist langust siit veel +20% tehakse. 35 võib osutuda küll olulisemaks vastupanuks. Arvestades, et tõus on olnud päris äkiline.

-

Fed leaves target interest rate unchanged at 0-0.25%, as expected

Reaffirms Plan To Buy UP To $300B Treasurys By Fall

Fed says economic outlook has improved modestly since march, but likely to remain weak for a time

FOMC says Econ Has Continued To Contract But At Slower Pace

FOMC: Sees Gradual Resumption of Econ Growth

Fed says Econ Outlook Has Improved Modestly Since March Mtg -

Panen ka Briefingu kokkuvõtte siia:

Information received since the Federal Open Market Committee met in March indicates that the economy has continued to contract, though the pace of contraction appears to be somewhat slower. Household spending has shown signs of stabilizing but remains constrained by ongoing job losses, lower housing wealth, and tight credit. Weak sales prospects and difficulties in obtaining credit have led businesses to cut back on inventories, fixed investment, and staffing. Although the economic outlook has improved modestly since the March meeting, partly reflecting some easing of financial market conditions, economic activity is likely to remain weak for a time. Nonetheless, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability. In light of increasing economic slack here and abroad, the Committee expects that inflation will remain subdued. Moreover, the Committee sees some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term. In these circumstances, the Federal Reserve will employ all available tools to promote economic recovery and to preserve price stability. The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and anticipates that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period. As previously announced, to provide support to mortgage lending and housing markets and to improve overall conditions in private credit markets, the Federal Reserve will purchase a total of up to $1.25 trillion of agency mortgage-backed securities and up to $200 billion of agency debt by the end of the year. In addition, the Federal Reserve will buy up to $300 billion of Treasury securities by autumn. The Committee will continue to evaluate the timing and overall amounts of its purchases of securities in light of the evolving economic outlook and conditions in financial markets. The Federal Reserve is facilitating the extension of credit to households and businesses and supporting the functioning of financial markets through a range of liquidity programs. The Committee will continue to carefully monitor the size and composition of the Federal Reserve's balance sheet in light of financial and economic developments. -

Uutest suurematest võlakirja ostude plaanist Föderaalreserv ei rääkinud ning 10-aastase võlakirja tulusus tõusnud kiiresti juba 3.1% peale.

-

WHO raises pandemic alert level to phase 5 - WSJ