Börsipäev 22. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Uue nädala esimene päev on makrosõnumite kohalt kujunemas sama vaikseks nagu reede. Kui Aasias jäid indeksid veel roheliseks siis nafta kauplemine alla 70 dollari on negatiivselt mõjutamas energiasektorit Euroopas, kus turud liikunud lõunaks ca -1.5% madalamale võrreldes reedese sulgumisega. USA börsiindeksite futuurid indikeerivad avanemist -0.7% punases.

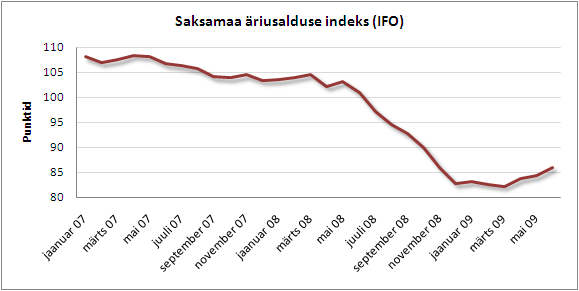

Eurotsoonis oli fookuses Saksamaa IFO indeks, mis jätkas tõusmist 26 aasta põhjadest kolmandat kuud järjest. 7000 juhi küsitluse põhjal koostatud indeks kerkis juunis 85.9 punktini maikuu 84.3 punktilt, peegeldades ärijuhtide lootust majandustingimuste paranemiseks, olgugi et Saksamaa sisemajanduse kogutoodang peaks tänavu vähenema üle 6% ja stagneeruma järgmisel aastal. Bloombergi küsitletud analüütikute mediaanootuseks oli 85 punkti.

-

Tug of War Continues

By Rev Shark

RealMoney.com Contributor

6/22/2009 8:51 AM EDT

It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.

-- Charles Darwin

Last week the market underwent its second mild correction since the rally began back in March. The last correction was in mid-May, and within a couple of weeks the market had righted itself and went on to break to a new recent high.

The current correction, which started last Monday, has so far been equally limited. After two days of selling, we found some support and have had a minor bounce; the action looked much better on Friday as some of the momentum returned to recent favorites that had been struggling.

But is the current pullback like the one in May -- quickly forgotten as buyers jump in -- or are we finally seeing signs that the rally off the March low is stumbling and ready for a more protracted pullback?

Let's examine the bullish case first. The major indices still have yet to do anything really negative. The S&P 500 has pulled back to some underlying support near its 200- and 50-day moving averages but has not taken out the May lows. While we have lost some upside momentum, the indices have not cracked technically.

Another positive for the bulls here is that the second quarter is winding down, and money managers will be looking to add some performance points to their retails. The dips in this market have been extremely shallow for so long because there are so many underinvested longs. They have not had an opportunity to buy any notable weakness, and with the end of the quarter out there, they are very likely to maintain some underlying bids so they can try to catch some opportunities before the end of June.

The market has also seen some healthy momentum trading. We have consistently had some very hot pockets of trading for a while now. The names have shifted around in groups like solar energy, low-priced biotechnology and small-cap China, but traders are hunting for action and they tend to get active again very fast, as we saw Friday when quite a few of the fast-moving, high-beta, stocks came back to life.

Overall, the bulls still look OK, although they are stumbling a bit and are showing some signs of stress ... which brings us to the bear case for this market. The primary argument for the bears right now is that the market has gone too far, too fast. While things may be "less bad" and the pace of decline is slowing, we don't have any signs of robust growth either. The market has been acting like a "V"-shaped economic recovery is occurring, but no one really seems believe that it will be very quick or easy.

The market has already fooled a lot of folks by staying stronger much longer than they anticipated. That is the nature of momentum, but this move also has many of the hallmarks of a typical bear-market rally. You simply aren't going to find companies that are seeing great revenue and EPS growth. You have cost-cutting and low expectations as drivers on the fundamental side, which is fine, but at some point, real growth is needed to keep the market running.

So we have a market that hasn't done too much wrong but that is showing some stress fractures. The end of the quarter may help to hold us up, but the fundamental improvement of the economy is being aggressively priced in, and you have to wonder how much more we can go on that basis when the phrase "green shoots" is getting to be a joke.

We have a little softness to start the day as European stocks saw pullbacks mainly due to weakness in commodities, and the World Bank forecasts that GDP in Europe, Japan and the U.S. will contract by 4.2% this year.

---------------------------------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: MRVL+3.2%... M&A news: SUAI +48.7% (light volume; Tower Group to acquire Specialty Underwriters' Alliance for $6.72 in Tower common stock), AAUK +7.1% (Xstrata seeks merger with Anglo American to cut costs - WSJ)... Other news: MEDX +12.1% (Patients with inoperable prostate disease recover after single dose of drug - The Independent), BCON +8.0% (agrees to accelerate funding of up to $14 million from Seaside 88), EMKR +6.0% (awarded a $5.7 mln Contract From the Air Force Research Laboratory for development of high-efficiency photovoltaic solar cells), LSI +5.3% (light volume; mentioned positively in Barron's), CLDA +1.9% (announces approval of Generic Name Vilazodone, first in a new class of experimental treatments for depression).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: WAG -5.9%, FMCN-1.6%... Select financial names showing weakness: DB -5.8%, IRE -5.2%, SLM -4.7%, ING -3.8%, AZ -3.5%, AXA -3.1%, UBS -2.7%, WFC -1.9%, CS -1.8%, BAC -1.7%, C -1.6%, RBS -1.1%... Select oil/gas names trading lower: BJS -7.2%, STO -4.4%, HAL -2.9%, TOT -2.5%, PBR -2.5%, E -2.1%, COP -2.0%, APA -1.8%, OXY -1.6%... Select metals/mining names showing weakness: RTP -5.7%, HMY -4.7%, MT -3.9%, BBL -2.9%, ABX -2.9%, SLV -2.6%, AUY -2.4%, GDX -2.2%, AU -2.1%, GOLD -2.1%, BHP -1.6%, GLD -1.1%... Select shipping names ticking lower: FRO -5.1%, EGLE -2.9%, EXM -2.3%, DRYS -2.3%, DSX -2.2%... Other news: LNET -9.5% (announces proposed private offering of $50 mln of convertible preferred stock), RGR -7.7% (Smith & Wesson and Sturm, Ruger mentioned negatively in Barron's), SLM -4.7% (still checking), SWHC -3.8% (Smith & Wesson and Sturm, Ruger mentioned negatively in Barron's), RIMM -2.7% (still checking), SI -2.3% (Siemens CEO says it's realistic that global econ approaching low - DJ; expects around $21 billion in new orders from Stimulus Programs worldwide), PRX -1.9% (filed for a $150 mln mixed shelf offering), CVS -1.1% (down in sympathy with WAG)... Analyst comments: ALU -5.1% (downgraded to Underperform at BofA/Merrill), NIHD -3.7% (downgraded to Neutral from Buy at Goldman- Reuters). -

Maailmapank on oma märtsikuus tehtud prognoosid maailma SKP kasvu kohta üle vaadanud ning nüüd on 2009. aasta majanduskasvu prognoosiks -2.9% varasema -1.7% asemel. Kasvu loodetakse uuesti nägema hakata selle aasta lõpus. Link siin.

-

Turg teeb kiirelt uusi põhju, müük on üsna laialdane -> energia ja toorained on langust vedamas ning ka tehnoloogiast pooljuhid, kes esimestel minutitel positiivsele poolele jõudsid on langusesse pööranud. Närvilisuse ulatust indikeerivad VIX ja VXN, mõlemal üle +10% tõusu ette näidata. S&P 500 on esimese 30 minutiga 903.50-ni müüdud, nasdaq juba üle 2% languses.

-

Nasdaq Comp near last week's low/early June gap bottom/May range top between 1785 and 1773

-

S&P500 ja Nasdaq100 juunikuu futuurid on nüüdseks aegunud ning nende puhul vaatame nüüd järgmist kvartalit ehk septembri futuure. Samuti on aegunud ka nafta juulikuu futuur ning seal vaatame nüüd augustikuu hindu.

-

Micex 10 indeks juba -8.10% languses ja Micex üldine -6.58%. Euroopa turud valdavalt üle 2% langust näitamas.

-

Kas kella 18.00 paiku tuleb jällegi tavapärane müügisurve kadumine ja kergelt väikse käibega tiksudes turu ülesost või on tänane närvilisus võtmas oma osa spekulantide rahakotist? Hetkel kõik tõusukatsed kiirelt alla müüdud ja S&P 500 flirtimas 900 punkti tasemega, kas sealt läbikukkumine võiks turud vabalangusesse lasta? Kindlasti paljudel stopid ka 900 st allpool, kuigi olulisem toetustase 870-880 vahemikus.

-

Hea ju saab odavalt osta jälle kui keegi selliste hindadega müümas on.

-

White House says 10% unemployment likely in "next couple months"

-

Viimaste minutite müük läks üsna paaniliseks ja turg lõpetas päeva põhjades, järgmised päevad saavad põnevad olema.

-

Ja Heinz!

Tore et on Juhaneid, kes oleks nõus veel selliselt tasemelt ostma.