Börsipäev 9. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

2. kvartali tulemuste hooaeg sai eile avapaugu ja esimesena oma numbreid näitama jõudnud Alcoa (AA) valmistas positiivse üllatuse, kus ootusi löödi nii tulude kui ka aktsiapõhise kasumi real. Konkreetsetest numbritest olulisem on aga järgmine lause:

Revenues of $4.2 billion, up 2% from 1Q09, but down 41% from 2Q08 on economic downturn and 49% drop in metal price.

Ehk kui metalli hindade kõikumisega tulemused läbi korrigeerida, suudeti näidata kasvu ka eelmise aasta 2. kvartali suhtes (41% tulude langust vs 49% metalli hindade langust) - mahud on tõusnud. Ja see on hea märk.

-

USA rikkurite seas üheks rohelise energia esikõnelejaks tõusnud T. Boone Picken's on otsustanud oma Texase tuulepargi rajamise pooleli jätta. Teade avalikustati teisipäeval, kuid pikem lugu selest ilmus WSJ's täna. Tuulepargi rajamise seiskumine on osaliselt tingitud ka teiste energiakandjate, eriti gaasi, hinnalangusest. Nüüd tuleb Picken'sil vaid mõelda, mida tellitud 667 tuuleturbiiniga peale hakata.

-

"Silver is set to outperform gold, argued Citigroup in a note published Thursday, with the broker saying investment flows into gold are moderating while the outlook for silver is improving. The ratio for gold-to-silver prices should return to its historical norm between 55 and 60 from the current 69, it said. It upgraded Fresnillo and Peter Hambro Mining to buy from hold, downgraded Randgold Resources to hold from buy and upgraded Hochschild Mining to hold from sell on reduced balance sheet concerns and the silver outlook." (marketwatch.com)

-

Ühed viimase aja populaarsemad kauplemisinstrumendid FAS ja FAZ on täna kordades kallimad. Tegemist on tehnilise muudatusega, aktsiate kogust on vähendatud ning selle võrra on hind kallim.

Reverse split:

FAS 5:1 (viis vana aktsiat= 1 uus aktsia)

FAZ 10:1 (10 vana aktsiat = 1 uus aktsia)

Splitijärgsete aktsiatega alustatakse kauplemist täna, LHV kontodel toimub vastav korporatiivsündmus enne regulaarse turu avanemist. Kõik orderid antud aktsiatele tühistatakse. -

Bank of England jättis intressimäära muutmata:

"The Bank of England on Thursday held its key lending rate unchanged at a record low of 0.5%, the central bank announced Thursday. The decision by the rate-setting Monetary Policy Committee was widely anticipated. The central bank also said it would maintain its asset-purchase plan at 125 billion pounds. Many economists had expected the bank to boost the size of the program to 150 billion pounds."

-

Üks väga hea kommentaar Hiina alumiiniumi nõudluse kohta RealMoney'st. Valitsuse kulutustega on tõepoolest võimalik tekitada lausa sõnulkirjeldamatult suurt ostuhuvi. Tundub, et Hiinale on toormaterjalid USA võlakirjade asemel rohkem meeldima hakanud.

Howard Simons: It's almost difficult to comprehend how the aluminum market has been distorted by Chinese stockpiling in recent months. Here are the monthly import numbers in thousands of metric tons:

Nov. 2008: 54.48

Dec. 2008: 68.90

Jan. 2009: 56.36

Feb. 2009: 60.07

Mar. 2009: 147.18

Apr. 2009: 439.90

May 2009: 331.74

-

Tunni aja pärast ehk tund enne USA turgude avanemist avaldatakse möödunud nädala esmaste töötu abiraha taotlejate numbrid. Ootuseks on 603 000, nädal enne seda oli näit 614 000. Oodatust parem number aitas aktsiaturule kaasa ja kehvem number jälle rõhuks eile õhtul alustatud rallikatset.

-

Target (TGT) reports Jun same store sales -6.2% vs -5.9% Briefing.com consensus; expects to meet or exceed current consensus of $0.64 for Q2.

-

Initial Claims 565K vs 603K consensus, prior revised to 617K from 614K; Continuing Claims rises to 6.883 mln from 6.70 mln

-

Alan Farley on teinud juunikuu võrreldavate poodide müügist RM all hea ülevaate. Panen selle ka siia:

Costco (COST) -6.0% vs -6.1%

Stage Stores (SSI) -12.6% vs -8.8%

Buckle (BKE) +9.6% vs +12.4%

Children's Place (PLCE) -12.0% vs -8.6%

Limited (LTD) -12.0% vs -8.1%

Bon-Ton Stores (BONT) -8.0% vs -8.0%

FRED Fred's (FRED) +0.2% vs -0.5%

Dillard's (DDS) -14% vs -10.3%

BJ BJ's Wholesale (BJ) -7.5% vs -7.4%

Macy's (M) -8.9% vs -8.8%

American Eagle (AEO) -11% vs -7.8%

Abercrombie (ANF) -32% vs -27.8%

Gap (GPS) reports -10.0% vs -8.3%

Aeropostale (ARO) +12.0% vs +10.2%

Nordstrom (JWN) -10.0% vs -10.6%

Target (TGT) -6.2% vs -5.9%Seega paljud on müügiootustele alla jäänud, kuid seda siiski mitte väga suurelt.

-

Huvitav lause Morgani suu läbi:

In addition, monthly employment data are inherently more noisy than commonly perceived. The Bureau of Labor Statistics reports that the typical standard error in monthly non-farm payrolls is 107,000, which, with offsetting errors, means that June's decline is not significantly different from May's.

-

USA alustab päeva tänast kauplemispäeva pärast Alcoa oodatust paremaid tulemusi ning kardetust väiksemat esmaste töötu abiraha taotlejate numbrit optimisminoodiga. Suurimad indeksid 0.8% kuni 1.0% plussis.

Euroopa turud:

Saksamaa DAX +1.93%

Prantsusmaa CAC 40 +1.53%

Inglismaa FTSE 100 +1.02%

Hispaania IBEX 35 +1.59%

Venemaa MICEX +1.22%

Poola WIG +1.10%Aasia turud:

Jaapani Nikkei 225 -1.38%

Hong Kongi Hang Seng +0.39%

Hiina Shanghai A (kodumaine) +1.37%

Hiina Shanghai B (välismaine) +0.97%

Lõuna-Korea Kosdaq -0.57%

Tai Set 50 +1.22%

India Sensex 30 -0.08% -

Stay Flexible

By Rev Shark

RealMoney.com Contributor

7/9/2009 8:29 AM EDT

The wise adapt themselves to circumstances, as water molds itself to the pitcher.

-- Chinese proverb

The market is gapping up a little this morning as Alcoa's (AA) loss wasn't quite as big as expected and oil and commodities bounce after being drubbed the last few days. On the other hand, same-store sales reports are trickling in and overall are looking quite poor. More than half of the reports I see so far have missed already low consensus estimates. That is putting some pressure on retail, which helped lead the anemic bounce we saw on Wednesday.

The most important thing about the market right now is that we have shifted into a downtrending mode. The Nasdaq is in better shape than the other indices, but the S&P 500 and the Russell 2000 are just barely clinging to support levels at the highs seen back in April.

The big change is that we aren't seeing much interest at all in dip-buying. We did have a little last-hour jump on Wednesday, but it isn't anything like what we experienced back in May and June. Back then, once the dip-buying started, the underinvested bulls on the sidelines would start chasing us higher and that would squeeze the shorts and give us some strong upside momentum. Now it looks like the bears are gaining confidence and are lining up to short strength, and the bulls are looking for exit points.

At this juncture, the market is still oversold and conditions are in place for some upside, but the weakness of the bounce attempt yesterday was troubling. All that we ended up with was some flat action that helped to alleviate the oversold pressure.

Adjust your mindset. This is no longer a market where we can give a poor-performing long position room to prove itself. If it starts to falter, the danger is that it is going to accelerate to the downside and put you in a hole quickly. When stocks start to break down in a market that is rolling over, the easiest way to get in trouble is to wait for the overall market to bail you out.

That doesn't mean there won't be some upside trades, but you have to think in terms of quick flips. Breakouts won't gain momentum like they do in a better market. There will be a few strong stocks here and there, but the hot pockets of momentum like we enjoyed in May and June will have very limited life spans.

Change your mindset and you'll do just fine in navigating a market that is showing strong signs of a more sustained downtrend. Inflexibility is your biggest enemy. There is no question that the market is not acting as well as it was a month ago. Acknowledge and embrace that fact, and you'll be able to find new ways to profit.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance/SSS: COMS +7.4%, AA +7.1%, GYMB +6.1% (light volume), CHTT +4.1%, SCSC +3.9%, CPKI +3.3%, ARO +2.7%, ANF +2.0% (light volume)... M&A news: NTAP +4.4% (NetApp declines to revise bid for Data Domain; merger agreement terminated), IPCR +4.2% (IPC Holdings to be acquired by Validus for $7.50 in cash and 0.9727 Validus voting common shares)... Select metals/mining/commodity related names showing strength boosted by AA results: CENX +7.0%, AKS +5.7%, AAUK +5.2%, BBL +4.0%, BHP +3.4%, GOLD +3.1%, X +2.6%, MT +2.4%, ACH +2.3%, FCX +2.2%... Select financial names showing strength: SNV +7.5%, HBAN +5.9%, RBS +4.4% (ANZ Bank raises A$2.2 bln via share purchase plan - DJ), GS +2.2% (upgraded to Buy at BofA/Merrill), C +1.9%, BAC +1.9%... Select oil/gas related names trading higher: SNP +3.8%, PBR +2.4%, RDS.A +1.1%... Other news: RIGL +33.5% (Rigel Pharma's R788 significantly improves rheumatoid arthritis in Ph. 2b clinical trial ), NVAX +13.5% (Cadila Pharmaceuticals Launches Joint Venture With Novavax in India), HGSI +8.8% (says data published in The New England Journal of Medicine support use of Raxibacumab for the treatment of inhalation anthrax), SAY +7.7% (signs 5-year contract with GlaxoSmithKline - DJ), DNDN +6.4% (still checking), CME +2.7% (modestly rebounding from its past 2 day 30+ point drop), BEZ +2.5% (Cramer makes positive comments on MadMoney), GE +2.1% (still checking for anything specific), LVS +2.0% (reconfirms Singapore opening timeline), WAG +0.9% (increases quarterly dividend by 22.2% to 13.75 cents/share)... Analyst comments: KBH +3.7% (upgraded to Outperform at Credit Suisse), CPKI +3.4% (upgraded to Buy at B.Riley), SAP +2.9% (upgraded to Buy at BofA/Merrill), ICE +2.1% (upgraded to Neutral from Sell at Pali Capital), HOT +1.6% (upgraded to Market Perform at FBR Capital), RIMM +1.3% (upgraded to Buy from Hold at Kaufman), APA +1.0% (upgraded to Outperform from Underperform at Calyon).

Allapoole avanevad:

In reaction to disappointing earnings/guidance/SSS: SIMO -9.9% , VRGY -9.8% (also announces proposed $110 mln convertible senior notes offering), EXAC -7.6% , HOTT -7.4% , PLCE -3.8%, ATI -2.5% (also announces voluntary contribution to U.S defined benefit pension plan)... M&A news: ELX -15.5% (rejects Broadcom's $11 offer; also guides Q4 EPS to high end of range, revs slightly above consensus), DDUP -1.5% (agrees to be acquired by EMC for $33.50 per share, terminates merger agreement with NetApp; also downgraded to Neutral at Baird)... Other news: MAPP -18.6% (MAP Pharma announces termination of Pediatric Asthma Collaboration), KMT -5.8% (announces its intention to offer 6.5 mln shares of common stock), AIG -5.3% (still checking), RNST -3.1% (files shelf registration statement for $150 mln of securities)... Analyst comments: RNOW -1.9% (downgraded to Hold at Deutsche Bank). -

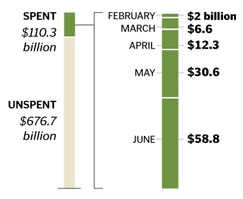

WaPo's hea graafik, kust näha USA valitsuse fiskaalstiimulite kasutamise suurenemist (reservi kasvava tööpuudusega võitlemiseks on veel küllaga):

-

WSJ'i kirjutab negatiivselt USA kinnisvarasektorist:

The U.S. housing market is facing new downward pressure as holders of subprime-mortgage bonds flood the market with foreclosed homes at prices that are much lower than where many banks are willing to sell.

While nationwide figures are scarce, a review of thousands of foreclosures in the Atlanta area shows that trusts managing pools of securitized mortgages sold six times as many properties as banks during the six months ended March 31. And homes dumped by subprime bondholders sold for thousands of dollars less on average than bank-owned properties, the data show.

-

May Wholesale Inventories -0.8% vs -1.0% consensus, prior revised to -1.3% from -1.4%

-

Seppälä poodides võib mõnes kohas näha hinnasiltide juures sellist lauset: "Kui sa nüüd ka ei osta, kas sa kunagi üldse midagi ostetud saad?".

Ma ei tea miks, aga kui ma seda lauset loen, lähevad mu mõtted CHK juurde. Buy low, sell high.

Esmaspäeval julges küll ettevaatlikult, kuid positiivse alatooniga, kommenteerida maagaasiettevõtete atraktiivsust ka šõumees Cramer: "You've had to buy these stocks when they are weakest. I know that they are not "done" being weak. But I know that they are better buys than sells down here. "

-

Alcoa on turu avanemise korralikust plussist juba punasesse vajunud ja muu turg liigub samas suunas.

-

Natural gas inventory showed a build of 75 bcf, analysts were expecting a build of 85 bcf, ranging from a build of 74 bcf to a build of 100 bcf.

-

Joel, kui tõenäoliseks pead, et CHK teeb lähitulevikus secondary?

-

Notable Calls'is täna tähelepanu saanud AXL kaupleb päeva tippude lähedal ning on ka turu avanemisest alates tugevas plussis.

-

Danelk, see on väga hea küsimus. Tõenäoliselt secondary ikka ka tuleb, kuid omaette küsimus on, et millises mahus. Kapitalikulutusi ja võlamakseid on vaja finantseerida. Kui aasta jooksul õnnestub mõistlike hindadega mõningaid varasid maha müüa, siis võib secondary ka ära jääda, mis aktsiale oleks kindlasti positiivne. Arvestades aga juhtkonna senist tegevust, kus capexit on juba väga tugevasti kärbitud, ei tohiks ka võimalikud secondary'd siiski väga suurt dilutionit kaasa tuua ega ka aktsiasse investeerimise atraktiivsust oluliselt vähendada.