Börsipäev 17. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Täna kell 15.30 teatatakse möödunud nädala esmaste töötu abiraha taotlejate arv - ootuseks on 465 000. See näitaja on tulnud üha madalamale, kuid selleks, et olla kindel, et riigis ollakse uusi töökohti juurde loomas, peaks see langema ca 400 000 juurde. Kestvate töötu abiraha taotlejate numbrilt oodatakse täna 5.18 miljonilist näitu. Kell 17 teatatakse novembrikuu juhtivate indikaatorite muutus (ootus 0.7%) ning Philadelphia Fedi äriväljavaadete detsembrikuu küsitluse näitaja (ootus 16 punkti).

Öösel on euro dollari vastu korralikult nõrgenenud EUR/USD -0.9% @ €1=$1.44. S&P500 futuurid on hetkel -0.4% @ 1105.5 punkti. -

Citigroup (C) teatas eile õhtul veel aktsiaemissioonist, kus turult üritatakse tõsta $17 miljardit, müües aktsiaid hinnaga $3.15. Oktoobri keskel kauples Citigroupi aktsia veel $4.8 peal, seega kahe kuuga langust ca 35%. Igaljuhul seconday tuli oodatust madalamale ning Citigroupi (C) aktsiaga on oodata järgnevatel päevadel põnevat kauplemist. Kindlasti on ka palju momentumkauplejaid nüüd aktsiat radaril hoidmas.

-

Eile õhtul alustas Verizoni (VZ) katmist ostusoovitusega ja $40lise hinnasihiga Deutsche Bank. Teadupärast kuulub Verizon Wirelessist 44% Vodafone'ile (VOD), seega on see julgustav märk kindlasti ka Vodafone'i investoritele.

-

Eurole on negatiivselt mõjumas Kreeka riigireitingu langetamine S&P poolt, mis tuli varem kui paljud olid arvanud, sest reitingugentuuri viimases teadaandest öeldi, et valitsusele antakse aega 60 päeva oma finantsseisu parandamiseks midagi ette võtta. Tegelikult oli otsus ilmselt juba siililegi selge, kuna selleni jõudmiseks kulus kõigest 9 päeva. Lisaks ähvardatakse praegust BBB+ reitingut veelgi madalamale langetada.

-

Väga korralik ralli dollari poolt. EUR/USD täna juba -1.35% ja €1=$1.434.

-

Saxo on järgmiseks aastaks prognoosimas kulla kukkumist 870 dollarile, jüaani 5%-list devalveerimist dollari suhtes, USDJPY kursiks 110 ja USA sotsiaalkindlustusfondi maksejõuetust. Ülejäänud huvitavaid nägemusi võib lähemalt lugeda siit. Kui täpsed olid aga Saxo prognoosid tänavuseks aastaks, saab näha siin

-

Initial Claims 480K vs 465K consensus, prior revised to 473K from 474K

Continuing Claims flat at 5.186 mln from 5.181 mln -

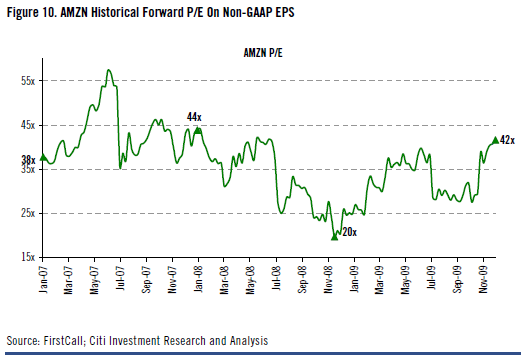

Amazon (AMZN) kaupleb eelturul +0.66%. Citi tõstis eile Amazoni sihi 140 dollari pealt 170 peale. Citi analüütikud on kindlad, et Kindlest on saanud "iPod of the Book World" & analüüsis tuuakse välja neli lühiajalist arengut:

- eCommerce Channel Checks suggestaccelerating Online Retail and AMZN market share gains – 73% Y/Y holiday SSS growth on AMZN’s platform, per Channel Advisor;

- comScore Traffic Analysisshows accelerating AMZN Website trends – 19% Y/Y visitor growth in Oct. & Nov. vs. 18% Y/Y in Q2 and 9% Y/Y in Q2;

- Quarterly eShopping Cart analysis continues to highlight AMZN Selection Superiority and Competitive Pricing Position; and

- NPD Video Game Console & Software QTD Sales Trends indicate Less Worse – though clearly still weak (down 24% Y/Y/down 8% Y/Y) – trends.

Citi tunneb Amazoni puhul enim muret valuatsiooni pärast. Nt Amazoni forward P/E:

-

No Energy, No Leadership

By Rev Shark

RealMoney.com Contributor

12/17/2009 8:22 AM EST

Energy is an eternal delight, and he who desires, but acts not, breeds pestilence.

-- William Blake

The most notable characteristic of this market lately has been its lack of energy. While we have been holding up quite well, there has been no real vigor. Market leadership has been almost nonexistent, and much of the movement seems random at best.

We have had some brief bursts of momentum in a few of the big-cap technology names like Google (GOOG) and Priceline (PCLN) , but others like Apple (AAPL) and Amazon (AMZN) have been quite mixed. A few solar energy stocks have shown some life lately, but finding some hot pockets of momentum has been quite a struggle.

What makes the market particularly tricky is that there isn't any bearish energy either. We have some mild selling, but breadth has been pretty good and the major indices are hovering just under their highs. While the indices aren't showing much strength, they aren't showing much weakness either.

The reaction to the Fed interest rate decision yesterday was a good example of this market's lack of energy. The Fed didn't do anything surprising, and some would even say that their policy statement was on the upbeat side, but the market flopped around a bit and then gave us a mild "sell the news" reaction. The bears had an opportunity to jam us down once the selling commenced but didn't accomplish much.

We have a weak open shaping up this morning. The dollar is stronger because of problems in Greece and some spin that maybe the Fed will raise rates a little sooner than later. FedEx (FDX) issued poor earnings and guidance, and that is generating a negative response.

However the biggest problem is that financials are weighing on the market this morning. Citi (C) saw weak demand for its secondary, which it prices at just $3.15. Meredith Whitney is adding to the pressure by cutting her earnings estimates to below consensus on Goldman Sachs (GS) and Morgan Stanley (MS) .

The bulls have not been able to capitalize on their upside opportunities lately, and now the bears have an opportunity to show what they have this morning.

I want to see the market shake off some of its lethargy and give us some better trading action. Unfortunately, with so little energy from the bulls, we may have to look to the bears to shake things up with some downside action. At least if we pull back a bit it might get the dip-buyers interested and action once again.

We are looking at a poor start this morning, but that may be what we need to get this market back on track for some positive end-of-the-year action.

----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: RAD +4.5%, PIR +4.0%, PAYX +3.2%, APOG +2.5%, FSLR +2.1%, GIS +1.2%, DHR +0.7%... M&A news: FUN +28.3% (Cedar Fair, LP agrees to be acquired by affiliate of Apollo Global Management for $11.50/share cash)... Select solar names ticking higher following FSLR results: CSIQ +1.9%, SOLF +1.6%, LDK +1.5% (partners with GPR-SBTFC for developing and constructing 100 MW of PV plants in Europe in 2010)... Other news: DPTR +9.4% (announces a settlement on the California Offshore Lease Litigation), APWR +7.1% (Shenyang power, US-REG and Cielo wind sign definitive agreement for 600 MW West Texas Wind farm project), HEB +6.9% (addresses Ampligen manufacturing issues), HXL +3.3% (Cramer makes positive comments on MadMoney), AONE +3.2% (A123 Systems and SAIC Motor form joint venture), MFA +1.7% (declared quarterly dividend of $0.27 per share of common stock, up from $0.25 per share of common stock)... Analyst comments: CA +1.8% (upgraded to Buy at Jefferies), LNC +1.8% (upgraded to Overweight from Equal Weight at Morgan Staanley), MHK +1.3% (upgraded to Overweight from Neutral at JP Morgan).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: HOV -8.9%, NDSN -4.3%, MATK -3.7%, FDX -3.3%... Select financial related names showing weakness: C -8.4% (confirms it prices $17 bln common stock offering at $3.15 per share and prices $3.5 bln of tangible equity units at $100 each), LYG -5.4%, IRE -5.0%, AIB -3.9%, AIG -3.8% (AIG said to plan Hong Kong listing for Asian life insurance unit - NY Times), DB -3.7% (Deutsche Bank eyes bid for RBS Sempra, source says - Reuters.com), STD -3.2%, UBS -3.0%, CS -2.7%, STI -2.6%, HBC -2.3%, RBS -1.9%, GS -1.8% (est cut by Meredith Whitney), MS -1.6% (est cut by Meredith Whitney)... Select oil/gas names trading lower: STO -2.3%, PTR -2.2%, TOT -2.1%, SU -2.0%, PBR -1.9%, BP -1.8%, E -1.7%... Select metals/mining related names showing weakness: DROOY -4.8%, AEM -4.1%, HL -3.9%, GSS -3.6%, RTP -3.3% (China attacks proposed iron ore venture - WSJ), GG -2.8%, GDX -2.8%, NEM -2.7%, ABX -2.7%, VALE -2.4%, GLD -2.1%, NGG -1.9%, BBL -1.5%... Other news: ANDS -18.4% (announces that ANA598 demonstrates positive 4-Week results at 200 mg BID), YONG -9.5% (announces it prices its public offering of 8 mln shares of common stock at $7.50/share), SQNM -7.9% (Xenomics' preliminary investigation leads the company to believe Sequenom willfully manipulated its down syndrome data in its presentations), END -6.3% (filed for a $500 mln mixed shelf offering), EZCH -6.1% (prices 3,863,050 common shares at $10.50/share), CXPO -5.8% (priced its public offering of 20,000,000 shares of Crimson Exploration common stock at the price of $5.00 per share), CNO -5.6% (announces pricing of public common stock offering of $4.75), NANO -2.7% (announces it intends to offer shares of common stock), OSIP -2.6% (Confirms that FDA Advisory Committee recommends against approving Tarceva for first-line maintenance use in advanced non-small cell lung cancer; downgraded to Hold from Buy at Lazard), FTE -2.1% (still checking), MET -0.8% (Moody's lowers MetLife ratings (senior debt to A3); stable outlook)... Analyst comments: PCS -5.1% (initiated with Underweight at Barclays, initiated with Sell at Deutsche), HOG -4.6% (downgraded to Sell from Neutral at Goldman; added to Conviction Sell list- Reuters), LEAP -2.5% (initiated with Underweight at Barclays), SHPGY -2.0% (downgraded to Neutral at UBS). -

Euroopa turud:

Saksamaa DAX -0,69%

Prantsusmaa CAC 40 -0,79%

Inglismaa FTSE 100 -1,13%

Hispaania IBEX 35 -1,20%

Rootsi OMX 30 -0,99%

Venemaa MICEX -1,67%

Poola WIG -0,83%Aasia turud:

Jaapani Nikkei 225 -0,13%

Hongkongi Hang Seng -1,22%

Hiina Shanghai A (kodumaine) -2,34%

Hiina Shanghai B (välismaine) -2,37%

Lõuna-Korea Kosdaq +0,61%

Tai Set 50 -0,08%

India Sensex 30 -0,11% -

November Leading Indicators +0.9% vs +0.7%, prior +0.3%

December Philly Fed 20.4 vs. 16.0 consensus; prior 16.7 -

Former Fed Chairman Greenspan, in prepared testimony, warns U.S. faces threat of unprecedented fiscal crisis over the horizon - Reuters

-

Citigroup: U.S. Treasury TARP Chief Allison says will execute Citigroup share sales after next 90 days to achieve best possible price for American public - Reuters

-

Treasury on ka treideriks hakanud ja seega usub, et järgmise 90 päeva jooksul hind tõuseb :D Neil oli võimalusi küllaga, et aktsiaid müüa $5 lähedalt, ometi jäeti see kasutamata.

-

Pole jõudnud täpsemalt vaadata aga HOV kvartalitulemus paistis küll korralik ämber olevat, kuid aktsia -10% langusest juba pea 0 tagasi ostetud. XHB samuti positiivsel poolel.

XLF samuti üsna hooga kosumas, samas jällegi tavapärane pilt kus käibe ära kukkumisel turg rallib. -

Pole päris pikka aega näinud kõrgendatud huvi puttide soetamisel, täna jäi silma selline lõik:

iShares MSCI Emerging Markets Index (EEM) Dec 40 puts are seeing interest with 11.6K contracts trading vs. open int of 72.6K, pushing implied vol up around 2 points to ~35%; -

As expected Senate panel votes 16-7 to confirm Bernanke for 2nd term

-

Kui maagaasivarudelt oodati idaranniku ja põhja-USA osariikides möllanud külma nädala tõttu suurt langust, siis languse suurus üllatas ka optimiste. Kui oodatud languse vahemikuks prognoositi 163 kuni 200 bcf (keskmiseks ootuseks oli 178 bcf), siis reaalselt langesid varud 207 bcf'i. Tõsi, varud on võrreldes ajalooliste keskmistega jätkuvalt kõrged, kuid vahe on vähenemas.

Kui naftahind on täna üle 1.5% miinuspoolel, siis tõusev maagaasihind on varude raporti peale tõusnud üle 5.5% ning aidanud kaasa ka maagaasisektori ettevõtete aktsiahindade tõusule. Kuna Chesapeake Energy'l (CHK) on väga suur osa 2010. aasta toodangust veel ette müümata, siis tõusvad maagaasihinnad on sõna otseses mõttes vesi nende veskile. -

Aktsiad hoiavad tegelikult veel üsna hästi võrreldes USD järjekordse tipuga. USD EUR-i vastu juba +1.58% tõusnud.

-

Fed's Fisher says going to be a while before economy resumes robust pace of growth, likely to have subpar growth for some time into future - Reuters

Ja turg astub sammu üles. Kas see peaks nüüd positiivne kommentaar olema? -

Ja eelnevalt välja toodud huvi EEM puttide vastu saab veel täiendust.

iShares MSCI Emerging Markets Index (EEM) puts are seeing interest with ~2x the number of puts trading vs calls (99.4K vs 46.1K). Most notable are the EEM Dec 39 puts (volume: 21.8K, open int: 39.8K, implied vol: ~41%, prev day implied vol: 31%); -

LDK Solar warns on ability to continue as going concern - DJ

LDK Solar to offer 18.9 mln American Depositary Shares - DJ -

Viimase kuu aja SPY graafik näeb välja nagu mingi väheaktiivse ADR'i graafik.. iga päev gap kuskile ja siis päev otsa väikeses vahemikus kauplemist.. Ehk siis hinnad panase paika vaikse ajal futuuridega kaubeldes ja päeva jooksul "õige" kauplemise ajal ei toimu mitte halligi.

Kusjuures see paistab väga hästi väga ka treidimises, viimane kuu aega on olnud turg äärmiselt mõttetu.. mitte midagi ei toimu, mitte miski ei tööta, mitte kedagi ei huvita mitte miski, täielik apaatsus valitseb.

Usun, et selline vaikus kestab aasta lõpuni. Esiteks on päris arvestatav osa inimestest juba järgmisest nädalast eemal või vähemalt ei ole nii aktiivsed. Teiseks, kõik on huvitatud, et turg jääks suhteliselt tippude lähedale püsima, et saaks ilusaid tootlusnumbreid näidata selle aasta kohta jne. Aga nii kui kell uut aastat lööb, läheb ilmselt uuesti rabelemiseks. Suunda ma öelda ei oska ja ega eriti ei huvitagi. Aga seda tahaks küll näha, et börsil jälle elu sisse tuleks. -

Turul ikka viimasel ajal väga mõtetu tiksumine. Turg nii õhuke, et suurema huvi puhul oleks liikumine kummalegi poole üsna kiire tulema. Ja nõustun JIM-ga, et suurem liikumine tulemas pigem aasta alguses.

-

ORCL täna peale turgu tulemustega, sealt ka selgem seisukoht JAVA suhtes.

-

Vähemalt koolitajad näitavad teed ja liiguvad kuhu vaja. Suurelt.

-

Täna peale turgu raporteerimas: ACN, APSG, DRI, HEI, NKE, ORCL, PALM, ZQK, RIMM, SCS ja TTWO.

Tehnoloogia ilmselt homme käitumas vastavalt tulemustele. -

Citigroup (C) on siis täna veenvalt tegemas ettevõtte ajaloo suurimat päevast kauplemismahtu.

-

Oracle prelim $0.39 vs $0.36 First Call consensus; revs $5.87 bln vs $5.69 bln First Call consensus

Take-Two sees FY10 $(0.40)-(0.60) vs ($0.42) First Call consensus; sees revs $1.0-1.20 bln vs $1.13 bln First Call consensus

Take-Two sees Q1 $(0.40)-(0.50) vs ($0.47) First Call consensus; sees revs $210-260 mln vs $226.61 mln First Call consensus

Palm prelim ($0.54) vs ($0.32) First Call consensus; revs $302.0 mln vs $266.17 mln First Call consensus

Research In Motion prelim $1.10 vs $1.04 First Call consensus; revs $3.92 bln vs $3.78 bln First Call consensus

RIMM ja ORCL peale tulemusi korralikult rallimas. -

Palm non-GAAP EPS was ($0.37) vs ($0.32) First Call consensus