Börsipäev 3. veebruar

Kommentaari jätmiseks loo konto või logi sisse

-

Meie tulemuste tabel jätkab uuenemist ning otselink sellele on siin. Täna on eelturult oodata eelkõige Black & Deckeri (BDK) ja Western Unioni (WU) numbreid ning järelturult Cisco Systemsi (CSCO) ja Visa (V) tulemusi.

Täna kell 15.15 teatatakse ADP tööjõuturu muutuse number jaanuarikuu jaoks. Põhimõtteliselt on tegu eelmänguga reedel USA Tööjõubüroo poolt avaldatava mitte-põllumajandussektoris loodud/kaotatud töökohtade numbrile. ADP ootuseks on -30 000. Selge on see, et turule meeldiks võimalikult väike miinus, veel parem oleks, kui number plussi jõuaks. ISM teenindusindeks avaldatakse kell 17.00, millelt oodatakse võrreldes detsembrikuu 49.8 punktilise näiduga taas üle 50 punkti piiri murda (mis näitaks laienemist) - seal on ametlikuks ootuseks 51.0 punkti. Eilse naftahinna ralli kontekstis on kindlasti oluline ka kell 17.30 avalikustatav naftavarude raport.

-

Euroopa komisjon kiidab Kreeka ambitsioonika eelarve defitsiidi vähendamise plaani (kolme aastaga 12.7% -> alla 3%) heaks, nentides et valmis peab olema täiendavate sammude astumiseks. Kreeka võlakirjaintresside alanemine ning euro tugevnemine viimastel päevadel peegeldavad küll hirmu ajutist leevenemist, ent plaani elluviimist hoitakse kindlasti kiivalt radaril ning kui peaksid tekkima võimalikud tagasilöögid ja ilmnema suutmatus seatud eesmärke täita, võib järgneda veelgi suurem müügisurve. Esimese raporti on Kreeka kohustatud tegema märtsis.

-

Kell 14.00 avaldati MBA kodulaenu taotluste muutus, mis on väga volatiilne nädalane näitaja, kuid tasuks siiski mainimist. Eelmise nädala MBA Mortgage Applications +21% vs üleeelmine nädal -10,9%.

-

Hispaania tõstis 2010 eelarvedefitsiidi prognoose 9.8%-ni SKP-st, mis on päris märgatav tõus eelnevast 8.1% tasemel seisnud prognoosist.

-

Halb reklaam Toyotale (Toyota Priuse isekiirenemise juhtum kiirusehoidja kasutamisel). Igasugused elektroonilised ja tarkvarapõhised probleemid on veel kõige hullemad - link siin.

-

Goldman Sachs tõstab BIDU hinnasihti:

Baidu.com target raised to $550 from $500 at Goldman -

January ADP Employment Change -22K vs -30K consensus

-

ADP osas olid ootused, et pluss? Euroopas turg alla tulnud...

-

Ilmselt ootused tõesti natuke kõrgemad - The ADP report implies no change in nonfarm payrolls.

-

M. Faberi tegevuskava veebruaris:

In the near term, should stock markets – following a brief rebound in the first few days of February – decline into the second half of February, I would buy some stocks for a rebound. And if stocks now fail to decline and continue to rally right away I would use strength to lighten up positions.

Faberi pikaajalsem nägemus USA majanduse kohta on jätkuvalt väga negatiivne:

In his latest GloomBoomDoom market commentary, the irrepressible pundit concludes that the US has basically two choices: default on obligations or massively monetize US debts and reduce the debt through inflation (link siin).

-

USA suuremate indeksite futuurid pool tundi enne kauplemise algust ca -0.3%.

Euroopa turud:

Saksamaa DAX -0.23%

Prantsusmaa CAC 40 +0.01%

Inglismaa FTSE 100 -0.07%

Hispaania IBEX 35 -1.17%

Rootsi OMX 30 -0.26%

Venemaa MICEX +0.58%

Poola WIG +0.45%Aasia turud:

Jaapani Nikkei 225 +0.32%

Hongkongi Hang Seng +2.22%

Hiina Shanghai A (kodumaine) +2.35%

Hiina Shanghai B (välismaine) +2.80%

Lõuna-Korea Kosdaq +2.11%

Tai Set 50 +2.31%

India Sensex 30 +2.06% -

To 'V' or Not to 'V'?

By Rev Shark

RealMoney.com Contributor

2/3/2010 8:54 AM EST

Doubt must be no more than vigilance, otherwise it can become dangerous.

-- George C. Lichtenberg

After a nasty breakdown, the bulls have put together a pretty good two-day bounce, with the action yesterday looking even better than Monday's. The S&P 500 is sitting at key resistance around 1100-1104, and the bulls are feeling much better now that they had a pretty good "V"-shaped bounce just like we saw so often in 2009.

While the bounce has helped to improve the mood, it hasn't repaired the technical damage that was done last week. We could bounce up the 50-day simple moving average at 1113 and still be technically broken.

The question we face here is an obvious one: Is the bounce going to fail this time, or are we going to pull off another "V"-ish move back to the highs that traps the poor bears once again?

Given the action in the market since last July, we can't just dismiss the chances that we are going to go straight back up. We had four occurrences -- in August, September, October and November -- in which we went up multiple days in a row and made new highs after a technical breach. Anyone who was looking for a failed bounced suffered badly.

What makes this particularly difficult is that a "V"-shaped bounce right back to the highs is just not what you normally expect to see. Typically when the market pulls back or breaks down, there are trapped longs who look to escape when the market bounces and bears who look to press shorts. That is what overhead resistance is all about -- as folks who suffered a loss are able to sell close to even, they are happy to get out and escape an unpleasant situation. They usually don't feel anxious to keep on buying more.

That didn't happen last year; we just went straight back up. Many market observers chalked that up to the large amount of liquidity that was created by the bailouts and stimulus plans, and as the market went straight up in 2009, it created a huge amount of performance anxiety among bulls who were chronically underinvested and trying to catch up with the indices. This group became tenacious dip-buyers, and every time we bounced they would pile in and chase things up in hopes of making up some relative performance.

So are conditions different now, or should we look for the same factors that drove the "V"-shaped bounces in 2009 to drive us again? With the market in negative territory for the year, there isn't any performance anxiety right now and there haven't been any new doses of liquidity introduced into the economy lately, but investors still have few good alternatives for their cash other than the market.

One thing that makes me less optimistic about a bounce back to highs this time is that the breakdown was much more severe than those we suffered in the latter part of 2009. All the high-momentum sectors such as China, bulk shipping, solar energy, gold, commodities and so on fell much harder and farther this time. The average stock looks much worse than the major indices. It takes more work to repair that type of damage, which is the main reason I think the recovery will not be so easy this time.

Another problem is that this market has no strong leadership. Usually during a correction we'll see a few areas that will maintain good relative strength and help to lead the market in a bounce. This time we have had some strength in regional banks, but that has weakened and now there really is nothing that we can point to as a safe haven. Strong markets need good leadership, and further upside will be more difficult until this market sees some.

So that's where we stand. We have a "V"-shaped bounce under way but we still face some formidable overhead resistance. The bulls are becoming more confident that this market is always going to recover with great ease, and the bears are having nightmares that this is going to turn out just like the last four market pullbacks with a move straight back to highs.

Our job here is to stay very vigilant and watch for signs that we won't pull off another "V"-shaped bounce. As Helene Meisler mentions in her column, it is still a bit early in the bounce to be overly bearish, but we need to watch the character of the action to see if this is going to be like 2009 or more of a struggle.

We have a slightly negative open on the way and overseas markets are mostly down.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: APKT +18.1% (also upgraded to Neutral from Underweight at Piper Jaffray, upgraded to Buy from Hold at Deutsche Bank), ATCO +13.6% (light volume) , NETL +10.8%, SOLR +9.3%, IRF +5.4%, TDSC +5.2% (light volume) , HMC +5.1%, SGI +4.8% (light volume) , NATL +4.6%, MYGN +4.3%, AIXG +4.1%, NWSA +3.5%, MTU +3.0%, JDSU +2.7%, FISV +2.6%, ACE +1.7%, NOV +1.5%, AFL +1.3%, BDK +1.1%, NLY +1.0%... M&A news: HDIX +84.3% (agrees to be acquired by Nipro Corporation for $11.50 per share; companies sign definitive agreement), SSTI +5.9% (Microchip Technology announces acquisition of Silicon Storage Technology for $2.85.share in cash)... Other news: DDSS +21.1% (receives FDA approval for OLEPTRO), BSTC +15.2% (confirms FDA approval of XIAFLEX for treatment of Dupuytren's contracture), AUXL +8.6% (FDA approves Xiaflex for debilitating hand condition), HERO +5.0% (Hearing strength attributed to positive newsletter mention), NBG +4.9% (Greece deficit plans endorsed by European Commission - BBC News), NTLS +3.6% (will replace Chattem in the S&P SmallCap 600 index), DAI +3.0% (trading higher in sympathy with HMC), PLL +2.2% (launches next generation blood filter that simultaneously reduces prions and leukocytes), URS +2.1% (Cramer makes positive comments on MadMoney), RDC +1.4% (Hearing strength attributed to positive newsletter mention), NOK +1.2% (New Ovi Maps with free navigation races past 1 million downloads in a week)... Analyst comments: IRF +5.4% (upgraded to Outperform from Market Perform at BMO Capital), UBS +2.9% (upgraded to Overweight from Neutral at JP Morgan), LXK +2.6% (added to Top Picks Live list at Citigroup, upgraded to Buy at Brean Murray), EXXI +2.5% (Morgan Keegan initiates with an Outperform), NDAQ +2.3% (added to Conviction Buy list at Goldman), CNQ +2.1% (added to Conviction Buy list at Goldman), BCS +2.1% (resumed with a Buy at BofA/Merrill ), BIDU +1.7% (target raised to $550 from $500 at Goldman), SCHW +1.5% (upgraded to Buy from Neutral at BofA/Merrill ), GRA +1.2% (upgraded to Buy from Hold at Jefferies), MCD +1.1% (added to Conviction Buy List at Goldman), ING +1.0% (initiated with an Outperform at Exane BNP Paribas), JCI +0.6% (upgraded to Neutral from Sell at Goldman).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: KNXA -14.1%, QSFT -9.3%, CHRW -8.7% (also downgraded to Hold from Buy at BB&T Capital Mkt), WU -8.2%, MTW -7.6%, R -7.6%, CTRP -6.9%, TSO -5.4% (also will suspend its quarterly dividend for the foreseeable future), RL -4.3%, ADS -4.0%, SEED -4.0%, VRSN -3.5%, WBSN -3.3%, SLAB -3.1%, MET -2.5%, IP -2.2%, PFE -1.8%, WAG -1.4%, TWX -1.2%... Select financials showing weakness: IRE -5.3%, STD -3.9%, BBVA -2.5%, RBS -1.5%, SAN -1.5%, CS -1.3%... Other news: CPT -9.2% (announces reduced development activity and related charges to earnings), BPZ -7.9% (intends to offer $140 million aggregate principal amount of convertible senior notes due 2015), ATPG -6.3% (continued weakness from yesterday's late sell-off following co update), MMLP -6.2% (announces 1.65 mln common unit offering), NMM -5.6% (prices its follow-on public offering of 3.5 mln common units at $15.51 ), TM -3.5% (says had complaints on new Prius brakes - Reuters.com), AZN -2.9% (trading ex dividend), UMPQ -2.1% (announces $215 mln public offering of common stock)... Analyst comments: MPWR -2.3% (downgraded to Underperform at Wedbush Morgan), ENI -2.2% (downgraded to Neutral from Overweight at JP Morgan ), LOW -2.1% (downgraded to Neutral from Buy at Goldman- Reuters), QSFT -2.1% (downgraded to Sell from Buy at Goldman), ARMH -1.7% (GC Research downgrades to Neutral from Overweight), AEE -1.4% (added to Conviction Sell list at Goldman ), CVS -1.1% (removed from Conviction Buy list at Goldman). -

Paanika Kreeka ümber tundub küll rahunevat, kuid üha rohkem on tähelepanu saamas Hispaania oma ülikõrge töötusemääraga (kandidaate Lõuna-Euroopas on veel palju). Siin on riigid, mis on enim "võlalõksus":

To assess which countries are in the trap, I took figures from the OECD economic outlook for growth rates and compared them with bond yields. This is a rough-and-ready measure but I think it gives a good idea of market concern. And market concern can be self-fulfilling - the costlier it is to service one's debt, the more markets worry it will not be serviced, and the higher the yield they demand (täpsemalt vt siit).

-

Leedu kolleegidelt tuli järgnev teade:

Today at 16:30 the opening bell in Nasdaq will be pressed by Lithuanian Prime-minister Andrius Kubilius

Kel võimalus, siis pange CNBC või Bloomberg mängima ja elage kaasa :)

-

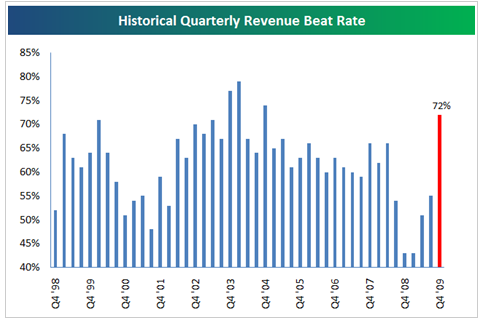

Päris paljud räägivad, et 4Q müügitulud on ok & positiivne üllatus on rohkem kasuminumbrites. Bespoke'ilt hea graafik, mis näitab, et ka müügitulud on olnud võrreldes konsensuse ootusega väga head (link):

-

lõhnab selliselt et täna ei pakugi AMZN head ostuvõimalust

-

Teenuste ISM jäi natuke konsensuse ootustele alla, kuid üle 50. punkit tase viitab jätkuvalt sektori kasvule (sektor sõltub vähem tsüklitest & rohkem rõhku tasub panna eilsele väga heale tööstussektori ISMile):

January ISM Services 50.5 vs 51.0 consensus, December 50.1

-

Energiavarude muutuse kohta siia ka pisut infot:

Dept of Energy reports that crude oil inventories had a build of 2317K (consensus is a build of 400K); gasoline inventories had a draw of 1306K (consensus is a build of 1400K); distillate inventories had a draw of 948K (consensus is a draw of 1150K). -

Ei saa aru miks see Nasdaqi avamine ja sulgemine alati nii suureks shõuks tehakse. See on ju tavaline rutiin.