Börsipäev 10. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Täna toimub Euroopa Keskpanga igakuine kohtumine, millelt väga suurt mõju turgudele ei oodata, kui just ei otsustata intressimäära praeguselt 1% pealt langetama hakata. Kuna eelmisel kohtumisel üritas Trichet ajakirjanikele puust ja punaseks selgeks teha, et Euroopa Keskpank ei hakka valitsuste võlakirjasid ostma, kuid kõigest mõned päevad hiljem teatati osalemisest mahukas likviidsusprogrammis ja otsusest siiski finantseerida riikide eelarveid, siis täna tuleb teha korralikku selgitustööd. Ühtlasi värskendatakse kvartaalseid makroprognoose. Hetkel oodatakse euroala 2010.a SKT tõusuks 0,8% ja 2011.a kasvuks 1,5% ning inflatsiooniks vastavalt 1,2% ja 1,5%. Euroopa Keskpanga intressiotsus avalikustatakse kl 14.45 ja pressikonverents algab kl 15.30

-

USA makrostatistika osas langeb tähelepanu möödunud nädala esmakordse töötuabiraha taotlejate arvule (kl 15.30), mille suurusjärguks prognoosib konsensus 450 000 ehk üsna pisikest muutust võrreldes nädalataguse 453 000-ga. Kestvate töötuabiraha taotlejate arvuks prognoositakse 4,6 mln (eelmisel nädalal 4,666 mln). Samal ajal avaldatakse ka USA aprillikuu kaubandusbilanss, mille defitsiidiks oodatakse 41,3 miljardit dollarit (märtsis -40,4 mld USD).

-

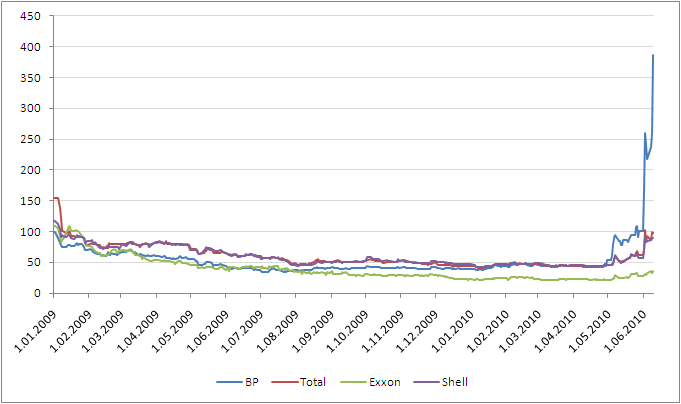

Nagu Joel eilse börsipäev lõpus juba välja tõi, kukkus BP aktsia USA turul pea 16% 14 aasta põhjade juurde, kuna Obama administratsioon üritab lisaks lekke likvideerimis- ja juriidilistele kuludele esitada arvet regiooni majandusele tekitatud kahju eest, kaasaarvatud palkade maksmist naftatööstuse töötajatele peatatud puurimistegevuse tõttu. Vaadates viimase CDS-i, tuleb paratamatult tunnistada, et turuosalisi ei hirmuta enam mitte dividendide kärpimise võimalus, vaid maksejõulisus ja pankrotioht....vähemalt panustatakse CDSi turul sellele. Kui mai alguses läks AA krediidireitinguga BP viie aastase võla kindlustamine maksma ca 50 000 eurot aastas siis eilse sulgumisega oli hind kallinenud 386 000 euroni aastas.

Erinevate naftaettevõtete 5a EUR CDS-d

-

Ühtlasi pole keegi veel aru saanud, kui palju naftat merre ikkagi jõuab. BP esialgne pakkumine oli 1000 barrelit päevas. Valitsuse ametnikud pakuvad pärast BP-lt saadudHD videomaterjali vaatamist, et tegelik maht võib olla kuni 100 000 barrelit päevas. TimesOnline: Gulf oil spill 'may top 100,000 barrels a day

-

HD videomaterjali link ei toimi.

-

tänud, nüüd on korras

-

Inglise Keskpank otsustas täna jätta baasintressimäär 0.5% peale ja uut kvantitatiivse lõdvendamise programmi ei tutvustanud. Tegu oli ootuspärast otsusega ja rohkem tasub tähelepanu pöörata varsti algavale ECB pressikonverentsile.

-

Euroopa Keskpank jätab oma intressimäärad oodatult 1.0% peale. Põnevam osa muidugi alles ees - kell 15.30 algav Euroopa Keskpanga konverentsikõne. Link konverentsikõnele on siin.

-

Briefing.com:

Initial Claims 456K vs 450K Briefing.com consensus, prior revised to 459K from 453K

Continuing Claims falls to 4.462 mln from 4.717 mln -

USA turud alustavad päeva igaljuhul optimistlikult. Indeksite futuurid on ca 0,8% kuni 1,2% kõrgemal ning ka energiahinnad on ca 1% jagu plussis. Nafta on sellega jõudnud üle $75 piiri.

Euroopa turud:

Saksamaa DAX +0,20%

Pantsusmaa CAC 40 +0,42%

Suurbritannia FTSE100 -0,21%

Hispaania IBEX 35 +1,26%

Rootsi OMX 30 +1,07%

Venemaa MICEX +0,24%

Poola WIG +0.34%Aasia turud:

Jaapani Nikkei 225 +1,10%

Hong Kongi Hang Seng +0,06%

Hiina Shanghai A (kodumaine) -0,83%

Hiina Shanghai B (välismaine) -0,35%

Lõuna-Korea Kosdaq +0,95%

Tai Set 50 +0,52%

India Sensex 30 +1,59% -

Downtrend Dilemma

By Rev Shark

RealMoney.com Contributor

6/10/2010 8:50 AM EDT

"There is no comparison between that which is lost by not succeeding and that lost by not trying."

-- Sir Francis Bacon

Yesterday morning, it looked like the bulls were set for a decent bounce attempt. They made a half-hearted try and then just gave it up. We had some decent action at midday, but then there was some rumbling about a possible bankruptcy filing by BP (BP) , which killed the positive sentiment that was developing.

The big worry over BP is that the political pressures are just too great. The market is afraid that the uncertainties will hang over not just BP but other off-shore drillers for a long time come. So far, BP has simply accepted responsibility, but the company is now starting to push back some as it possibly faces huge consequential damages such as the fallout caused by a moratorium on further offshore drilling.

It was the BP issue that killed the market yesterday afternoon, but to make sure that trading stays extremely difficult, we have good news for the euro this morning, which is producing a decent gap to the upside. The ECB kept interest rates unchanged at 1% as expected, but the news that drove the euro up was a comment by the head of China's national pension fund that the euro would gradually stabilize. One of the reasons he sees that the euro will recover, however, is because the U.S. fiscal deficit is so big that it will temper the role of the dollar as a safe haven.

So, once again, we are starting the morning with some positives. The problem is that we haven't managed to follow through with strong closes lately. Three of the last four trading days have seen closes at the lows. The hallmark of a weak market is when market players are afraid to carry overnight exposure.

Technically, we are oversold and at key support levels, so conditions are still good for some sort of bounce, but we have to keep in mind the bigger picture which is that we are undergoing a major correction and have yet to show many signs of finding a lasting low.

The dilemma in a downtrending market is that while we want to participate in some of the big bounces that are likely to occur we don't want to be sucked into believing that we are going to go straight up again.

What the market needs to make a turn isn't just one or two days of decent gains but signs that it can build on those gains a few days afterward. It is the following through after the initial bounce that tells us that there is real buying and a change in market sentiment.

The easiest mistake to make in a downtrend is to believe that a bounce is an end to the correction. Psychologically, that is what we want to believe after going through a period of pain, and it is easy to shrug off negatives that may still exist.

The best way to avoid that problem is to stay extremely defensive with your money management. Keep those stops tight and don't hesitate to book some gains when you have them. If the market does follow through down the road and the trend shows signs of turning up, you can quickly add more long exposure. It isn't important that you be fully long at the exact bottom. It is far more important that you manage your risk and wait for conditions that suggest the trend has changed.

It is going to be interesting to see if we can build on this early strength. The bulls have been trying to ignite a bounce lately but have not been able to gain much momentum. It certainly has been nothing like the V-shaped bounces we saw so often during the market uptrend, but that is what happens when the market undergoes a major change in character.

-----------------------------------

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: APWR +12.2%, MW +5.5%, ALOG +2.5%, MEAS +2.0% (light volume).

M&A news: PMACA +12.1% (Old Republic to acquire PMA Capital; ORI to offer ~$7.10/share for PMA Capital).

Select financial related names showing strength: BBVA +5.0%, LYG +4.9%, STD +4.8% (Cramer makes positive comments on MadMoney), ING +4.5%, RBS +4.0%, PUK +3.5%, HBC +2.9%, IRE +2.8%, CS +2.3%, NBG +2.3%, DB +1.8%, WFC +1.7%, BAC +1.7%, C +1.6%, .

Select metals/mining stocks trading higher: RTP +4.8%, BBL +4.5%, MT +3.8%, MTL +3.5%, GSS +3.0%, TCK +3.0%, GOLD +1.8, VALE +1.4%.

Select oil/gas related names showing strength: BP +10.7% (says it is not aware of any reason for share price decline yesterday; provides update on GoM oil spill response in 6-K), RIG +7.0%, APC +6.2%, ATPG +4.1%, REP +3.4%, BEXP +2.8%, WFT +2.4%, CHK +2.4%, HERO +2.3%, E +2.1%, SLB +2.0%, DO +1.7%, RDS.A +1.2%.

Other news: ARMH +12.8% (trading over 12% higher premarket following renewed speculation that Apple (AAPL) may be interest in the co), DEER +5.9% (signs $12 mln supply contracts, announces record sales growth in the North American markets, continues stock buyback ), ALV +5.5% (started an in-house textile cushions operation in its airbag module facility in Jiading, Shanghai), LOGI +3.8% (still checking), IMMU +2.6% (announces preclinical results of pretargeted imaging and therapy of cancer), DNDN +1.8% (Dendreon at Needham Conference Summary), SYMC +1.7% (light volume; extends agreement with HP to distribute Norton Internet Security on consumer PCs worldwide), CNP +1.2% (prices 22.0 mln common shares at $12.90/share), .

Analyst comments: ORCL +1.0% (light volume; initiated with an Outperform at Morgan Keegan).

Alllapoole avanevad:

Select gold related names modestly lower in early trade: EGO -1.3%, GFI -0.9%, GLD -0.5%, NEM -0.5%, HMY -0.5%.

Other news: KID -4.1% (prices secondary offering of 4.4 mln shares on behalf of selling stockholder at $7.25/share). -

Goldman Sachs on hetkel -2.5% ja aitab turu optimismi jahutada. Nõrkust seostatakse FT looga, kus räägitakse, et SEC on agressiivsemalt GSilt infot nõutamas.

Briefing: The weakness follows an FT report that said the SEC has stepped up its inquiries into a mortgage-backed deal by GS that was not part of the civil fraud charges filed against the bank in April. This news follows reports yesterday that an Australian hedge fund sued Goldman Sachs for $56 mln over a subprime investment. -

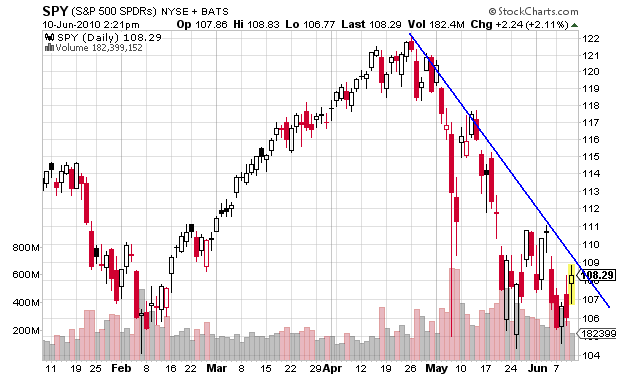

Üks pilt siia tehnilist analüüsi vaatavatele kauplejatele/investoritele. Kui aprillikuu tipust downtrendi joont tõmmata, siis võib öelda, et oleme tänase ralliga selle joone alla jõudnud.