Börsipäev 1. september

Kommentaari jätmiseks loo konto või logi sisse

-

Head kooliaasta algust kõigile mudilastele ja nende vanematele! 1. september tähistab nii "Teadmistepäeva" kui ka "Ülemaailmset rahupäeva". Lisaks sellele on see veel ka börsipäev : )

USAst on täna tulemas hulgaliselt makroandmeid. Eesti aja järgi kell 15.15 tuleb ADP hinnang USA erasektori augustikuu töökohtade muutuste kohta - ootus on ca +13 000. Kell 17.00 avaldatakse juulikuu ehituskulude muutuste määr (ootus -0.7%) ning ISM indeks (ootus 52.9 punkti). -

Sesoonselt korrigeeritult kasvas Austraalia teise kvartali SKP 1.2% QoQ, ületades sellega oodatud 0.9% kasvu. Aasta baasil kasvas sesoonselt korrigeeritud riigi majandus 3.3% vs oodatud 2.8% kasv.

-

Saksamaa ekspordisektor on küll tugev, kuid sisetarbimine on endiselt riigi nõrk külg. Juulis langes Saksamaa jaemüük mom 0.3%, konsensus aga ootas 0.5% suurust kasvu. Aastataguse ajaga võrreldes kasvas jaemüük 0.8%.

-

Eurotsooni tööstussektori kasvutempo aeglustus: 16-riigi tööstussektori aktiivsust mõõtva PMI indeksi väärtus langes augustis kuue kuu madalaimale tasemele ehk 55.1-ni vs juuli 56.7 (väärtus üle 50 näitab aktiivsuse kasvu sektoris).

-

UK PMI tootmisindeks langes 9 kuu madalaimale tasemele 54,3 punktini (oodati 57,0). Eelmise kuu näit korrigeeriti samuti alla 56,9 punkti peale. Kuigi näit püsib ülevalpool 50 taset - mis tähistab tootmissektori laienemist - on kasv aeglustumas märgatavalt. Mitme aasta tipp saavutati käesoleva aasta maikuus 58 punkti.

Naelsterling sattus enne indeksi avaldamist surve alla, kuid on päeva peale taastunud ja kaupleb hetkel 0,25% kõrgemal $1,5384 taseme juures. -

Taas on päevakorda tõusnud aktsiatehingute maksustamise teema USAs. Üks 31. augustil ilmunud lugu sellel teemal siin.

-

Euro kaupleb dollari vastu 1% kõrgemal $1,2805 taseme juures. Euro sai tuge Hispaania peaministri sõnavõtust, kus ta avaldas lootust, et Hiina jätkab Hispaania võlakirjade soetamist.

-

Kui eile tõstsid kuulujutud võimalikust ülevõtust SKSi aktsiat, siis täna on sama teema BKC'ga, mis on eelturul üle 15% plussi tõusnud. Link ka.

-

Ja mis ootused olid Macau gaming revenue kohta?

-

Random and Reactionary

By Rev Shark

RealMoney.com Contributor

9/1/2010 8:36 AM EDT

"Creativity is the ability to introduce order into the randomness of nature."

-- Eric Hoffer

The market is reacting favorably to overseas PMI reports. They were a little soft in Europe, but China posted PMI of 51.7 vs. estimates of 51.5. And although that isn't much of a beat, the market has been very worried about the recent streak of soft data, so it is a bit of a relief.

That is the focus at the moment, but we have the ISM number at 10:00 a.m. EDT, and obviously that is going to be a market mover. Expectations are for a decline to 52.7 from the 55.5 posted in July.

This market has been so random and data-sensitive lately that it takes great creativity to sort it all out. Sometimes we just have to acknowledge that we have no control over it and focus on ways to ride it out the best we can. That usually means staying short term and being defensive, because you just never know what will hit.

Yesterday we had a particularly good example of how the market is being pushed around. We had lackluster action all day, but according to ZeroHedge.com, in the 16 minutes from 3:59 p.m. EDT to 4:15 p.m. EDT, approximately 300,000 e-Mini S&P 500 contracts traded, which represented a total notional value of about $15 billion. That closing trade jerked us suddenly higher. Maybe it was just the computers squaring the books for the end of the month, but when trades of that size occur so suddenly, the market is going to be moved in very unusual and random fashion. There is no way to predict it, so we are left with no choice but to trade with a very high level of caution.

With that sort of manipulative trade occurring during what is one of the slowest weeks of the year, it is difficult to have a high level of conviction. The overall technical picture remains negative. We are still holding the important 1,040 area of the S&P 500, but there is some very tough overhead to contend with. Even with a gap up open this morning we still aren't even back to the first minor resistance around 1,067 or so.

Even though the technical picture is negative, the market is very susceptible to sharp spikes, which are keeping the bears from pressing their advantage. You just never know when you are going to walk into a sudden spike like we are seeing this morning.

We'll see what the data brings, but keep in mind that even though September tends to be a weak month seasonally, the first day of the month has a pretty good track record.

It is the bulls who have the burden of proof, and they are going to need to get this market back up over some resistance level to have a fighting chance. We are still a little oversold and the mood has been quite negative lately, so a positive reaction to mediocre data wouldn't be a major surprise. The key will be holding on to gains as the week progresses and we look forward to the big jobs report that is due on Friday.

Buckle up -- it's going to be bumpy out there.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: GIII +22.4%, CCUR +3.1%, JOYG +2.8%.

M&A news: SLRY +43.4% (to be acquired by Kenexa in an all cash tender offer and merger for $4.07 per share), BKC +17.0% (trading higher in premarket following reports that the co may be considering sale), SHPGY +2.0% (ticking higher following UK article suggesting that the co may be target of a bid), CASY +1.7% (Alimentation Couche-Tard increased offer to acquire Casey's General Stores to $38.50/share in cash).

Select financial related names showing strength: NBG +4.5%, SNV +3.8%, ING +3.2%, IRE +3.1%, AIB +3.1%, UBS +3.0%, DB +2.1%, BCS +2.0%, CS +1.7%, BAC +1.3%, RF +1.2%, C +1.1%, JPM +1.0%.

Select metals/mining stocks trading higher: SCCO +3.9%, MT +3.8%, RTP +3.1%, BHP +2.5%, GOLD +2.3%, AA +1.9%, GFI +1.6%.

Select oil/gas related names showing strength: SDRL +6.1%, REP +3.6%, ATW +3.2%, ATPG +3.0%, TOT +2.9%, RIG +2.9%, STO +2.9%, RDS.A +2.4%, E +2.3%, BP +1.6%, SNP +1.6%, PBR +1.6%.

Select European drug names trading higher: SNY +3.5%, GSK +2.5%, AZN +1.4%.

Other news: SRZ +24.4% (to receive $50 mln from HCP for 27 management contracts), LOCM +6.8% (announces material definitive agreement with Yahoo, as noted in an 8-K), ERIC +3.8% (checking for anything specific; joint venture Sony Ericsson held conference), IMMR +3.5% (light volume; announced that Toshiba Corporation has licensed Immersion's TouchSense system), ISLN +2.8% (Isilon Systems Unified Scale-Out Storage achieves VMware ready status), NFLX +2.7% (strength attributed to reports of relationship with AAPL on a new AAPL set-top box).

Analyst comments: CAGC +5.6% (initiated with a Mkt Outperform at Rodman & Renshaw), VECO +3.2% (initiated with Buy at Kaufman), MEE +3.1% (upgraded to Overweight from Neutral at HSBC), BCSI +2.1% (upgraded to Buy from Hold at Needham), AAPL +1.0% (assumed with an Outperform at JMP Securities).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: ARAY -5.8%, LTXC -4.7%, FAC -2.9% (light volume), APSG -1.6%, FORM -1.4%.

Other news: SFSF -2.8% (filed for a ~903.7K share common stock offering by selling shareholders).

Analyst comments: SKS -4.7% (pulling back from yesterday's 20% surge higher; also downgraded to Neutral from Overweight at JP Morgan). -

ISM tuli 56.3 punkti vs oodatud 52.8.

Ehituskulutuste muutus juulis -1.0% vs oodatud -0.5%. -

I vot bolshoje rally...

-

näu what?

-

mune loetakse õhtul

-

stocker, trailing stoppide kasutajad võivad mõne muna juba praegu üle lugeda :-D

-

BKC aktsiaga tehakse turul pulli. Hommikusest 16%lisest plussist on järgi jäänud veel 5%, kuna ülevõtja 3i Group eitab huvi BKC vastu. Samas... kinnitus oleks ju ainult hinda kergitanud.

-

Homme tuleb ilus tõusukene Tallinna börsil ka

-

Fed buys $900 mln of $25.788 mln submitted in the 2012 to 2013 maturity range

-

Joel sama pulli tehti eile SAKS ga.

-

1) BHP kägiseb, et pole põhjust POT-i bidi tõsta, kuna teisi bidijaid ei ole. Miks endaga võistelda.

2) Sept. 1 China’s Sinochem International Corp. hired HSBC Holdings Plc to advise it on options regarding Potash Corp. of Saskatchewan Inc., CNBC reported, citing the Wall Street Journal. Sinochem’s move doesn’t mean the company has decided to bid for Potash, CNBC said, according to WSJ.

3) Hind niigi üle bidi, kaks dg-d, BKC up ja down jooksutamine... Võiks rohkem tähelepanu saada, aga... -

Ilus soe päikesepaisteline ilm, ja aktsiad kah kohe tõusevad.

jarzzz, Tallinn ju tõusis täna. -

jarzzz

viimane tõus ja siis edasi alla -

NFLX ... kole, uudis...

-

Väga raju liikumine:

Apple says NFLX streaming available on Apple TV -

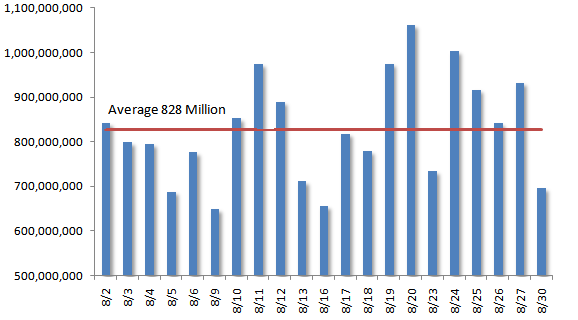

Aeglane augustikuu on tänaseks läbi saanud. Allpool on Bespoke graafik augustikuu käibest.

-

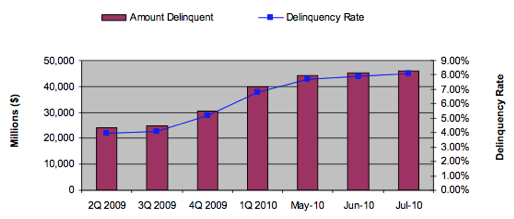

Standard & Poor’s avaldas täna raporti Commericial Mortgage Backed Security’itest. Allolevalt graafikult on näha, et kuigi käimasoleva aasta juulis määr kasvas, siis olukord on turul analüüsimaja sõnul tasapisi stabiliseerumas.