Börsipäev 18.-19. jaanuar - tulemustesadu

Kommentaari jätmiseks loo konto või logi sisse

-

Koopia börsipäeva artiklist ka siia ....

Enne turgu teevad ilma olulised raporteerijad finantssektoris: Citigroup (C), Bank of America (BAC), Wells Fargo (WFC), Ameritrade (AMTD) ja Charles Schwab (SCH). Farmaatsiasektoris laekuvad Forest Labs (FRX) ja Abbot Labs (ABT) tulemused.

Peale turgu on oodata tõeliselt tihedat tulemustesadu olulistelt tegijatelt tehnoloogiasektoris: IBM (IBM), Yahoo! (YHOO), Advanced Micro Devices (AMD), Juniper Networks (JNPR), Motorola (MOT), Rambus (RMBS), Seagate (STX) jne.

Esimesed pääsukesed:

AMTD ületas, EPS 0.22 vs. ootus 0.19 ja käive 261,98 vs. ootus 247.11, aktsia eelturul +3,30%

-

Rev Shark:

Burden of Proof Lies With the Bulls

1/18/05 7:48 AM ETRemember how often you have postponed minding your interest, and let slip those opportunities the gods have given you ... (Y)ou have a set period assigned you to act in, and unless you improve it to brighten and compose your thoughts, it will quickly run off with you, and be lost beyond recovery.

-- Marcus Aurelius

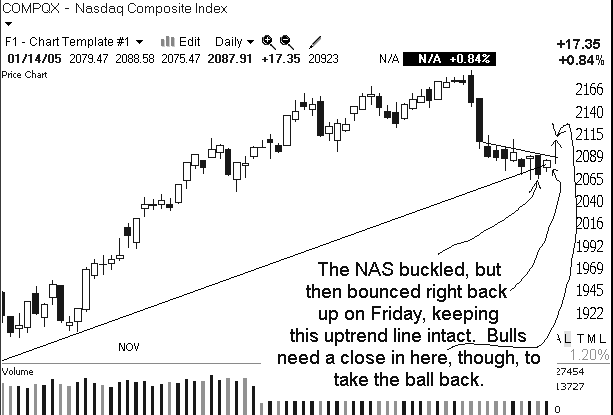

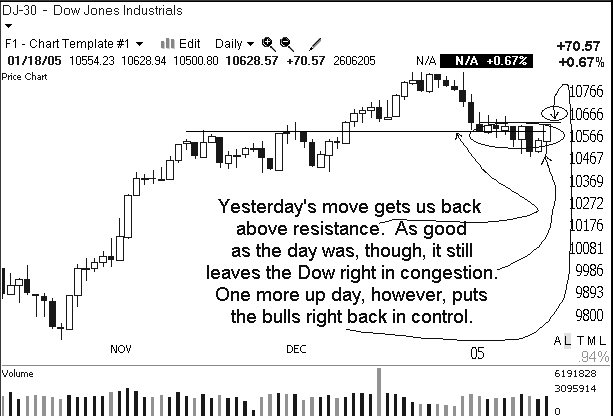

It seems like the market is almost always at an important turning point, but a good case can be made that this week really will be an important juncture. The shaky start to the new year has left the indices in a precarious position as we await a flood of earnings reports over the next two weeks.

All of the major indices need to compose themselves soon or we face another move downward. With the limited amount of support on the charts, there is plenty of room to pull back further. The slide slowed down last week, which is a positive, but the major indices need to regain some key technical levels before we can feel more confident about the market. The S&P 500 needs to climb over 1190 on a closing basis and the Nasdaq needs to regain the 2100 level.

The issue this week is whether earnings reports have sufficient juice to put the market back on track. One good thing about the sharp pullback to start the year is that it has helped, to some degree, to temper expectations. Good news should generally result in a positive reaction since it has not been priced in during the past couple weeks.

Earnings season holds the seeds of better action, but there are no guarantees that even good reports can turn the tide. What we need is a big positive accumulation day and then some follow-through. The market needs to move up 3% or 4% on much better-than-average volume and then have another good day within a week or so to prove it wasn't a fluke.

The burden of proof is squarely on the shoulders of the bulls right now. They have to compose themselves and capitalize on good news as it hits. If they are unable to take advantage of some solid earnings reports, they will be in trouble. The bulls have already squandered some of the seasonality that favors them, and if they continue to stumble, buyers will lose confidence and stay on the sidelines.

After the long weekend it looks like we are off to a hesitant start. Overseas markets are giving back gains they enjoyed while U.S. markets were closed Monday in observance of Martin Luther King Jr. Day. Crude oil is nudging back up over the $49-per-barrel mark and that is having a negative impact.

We have earnings tonight from IBM (IBM:NYSE) and Yahoo! (YHOO:Nasdaq), and the reaction to those reports should give us a good idea of the prevailing mood.

We'll see how things develop as the open approaches, but right now it looks like the beginning-of-the-week optimists are sleeping in, which isn't a bad thing.

Gary B. Smith:

-

Kajastame turul toimuvat täna ka chatis.

-

Gapping Up

MAY +10.3% (CEO resigns, upgrades from BofA, JP Morgan and OpCo), AMTD +6.4% (beats by $0.03; guides Y05 above consensus), LIFC +6.3% (guides for Q4 and '05), ADSX +5.7%, ANLT +3.8%, RHEO +3.7% (started with a Buy at Smith Barney; tgt $13), NVTL +3.7% (added to JP Morgan's Focus List), FCX +3.1% (beats by $0.09; beats on revs), RVSN +2.8% (mentioned in Barron's), YHOO +2% (to join with Verizon to offer a co-branded Internet-portal service to Verizon's broadband subscribers)... Under $3: IVAN +7.5% (reports 150% increase in 2004 production), TERN +6.7% (selected for cable VoIP deployment by Hong Kong's Wharf T&T), ASTM +4.8% (NY may establish stem cell fund - Newsday.com).

Gapping Down

JOBS -36% (lowers Q4 guidance), MCLD -12% (continues Friday's 8% drop), CMNT -12% (to be acquired by MCDTA), SMDI -9.7% (sees Q4 results below consensus), VIP -6.2% (announces debt to the treasury), JDSU -6.1% (sees revs at lower end of guidance), CHTR -5.9% (CEO resigns), NMSS -5.3% (First Albany downgrade), TTWO -5.3% (ERTS signs 15-year agreement with ESPN), STM -4.2%, TEVA -3.1%, TIBX -3% (JP Morgan downgrade), SIRI -2.8%, AMLN -2.5% (stock offering), NOK -2.4%. -

Millest see turg nüüd tuge sai, on see põhjendatav?

-

Turg paistab praegu tugev, ka tervis (breadth) järjest tugevnev. Nüüd tuleks ka päeva lõpuni seda tugevust hoida ja pilt muutuks tublisti paremaks.

-

Heade kvartalitulemuste ootuses Yahoo'lt (YHOO) on Google (GOOG) lõpuks 200$ tasemest läbi saanud ja päevasiseselt jõudnud ka juba uue kõigi aegade tipu teha. Google ise avaldab tulemused 1. veebruaril. Just lasti välja tasuta programm digitaalsete fotode haldamiseks.

-

Chart of the Day

Today's chart illustrates that, since 1960, higher earnings have tended to correlate with higher dividends. What is interesting, however, is that earnings have soared over the past couple of years, while dividends have increased at a slower pace. So why are cash-rich corporate boards holding back despite the dividend tax cut of 2003? The explanations range from executives that lack confidence in future earnings to shareholders that are not demanding enough of their corporate boards.

Events of the Day

February 02, 2005 - Groundhog Day -

kommentaariks veel nii palju, et suuremad kasumid on saavutatud paljuski ka "kunstlikul teel" ehk optsioone ei ole paljud firmad siiani kuludesse arvestanud.

-

Eile õhtul laekusid tulemused Advanced Micro Devices'ilt (AMD). Vaid 5% käibe kasvu juures jäi firma võla tasumise ja flash-mälude nõrga müügi tõttu kahjumisse. Siiski vastasid avaldatud tulemused nädala eest langetatud prognoosidele, ning järelturul langes aktsia vaid kergelt punasesse. Conference call'il kommenteeris CEO Hector Ruiz lõppenud kvartalit protsessorite osas tugevaks, kuid mälude osas trööstutuks (freaking dismal).

Käesolevaks kvartaliks prognoosis firma kiipide müügi samaks jäämist või langust, flash mälude müügi osas kindlat vähenemist. Samas loodetakse esimeses kvartalis taas kasumisse jõuda. Susquehanna Financial Group'i analüütiku Tai Nguyen'i arvates näeme aktsiat lühiajaliselt külgsuunas kauplemas, kuni muude kiipide müük flash'ide kaotuse tagasi teevad.

-

Seda sõltuvust oleks ilus vaadata logaritmilises teljestikus, seal ei paistaks kõrvalekalle sirgest üldse nii suurena. "Päeva graafiku" autorilt tahaks veel küsida, kumb sõltub kummast: dividend kasumist või kasum dividendist? Kui esimene oletus on õige, siis võiksid dividendid olla vertikaalteljel. Ja kindlasti tõmbaksime me logaritmilises teljestikus ka trendijoone teisiti. Kas selle "dividendi mahajäämuse" üheks põhjuseks pole see, et hetkel tahetakse rohkem investeerida ja vähem tarbida? Ja veel, kus paiknevad sellel graafikul teadaolevad aktsiaturu tõusuaastad ja paigalseisuaastad? Punktide lugemisega seda kindlaks ei tee, sest neid on rohkem kui 44 ja seega ei vasta igale punktile 1 aasta.

-

kikkigu keegi mind chatist välja pliiiiis.

sain kah käe valgeks... -

Rev Shark:

Keep an Eye on Yahoo! as a Major Tell

1/19/05 8:21 AM ET"The starting point of all achievement is desire. Keep this constantly in mind. Weak desires bring weak results, just as a small amount of fire makes a small amount of heat."

-- Napoleon Hill

Yesterday buyers demonstrated some desire to be in the market as earnings reports began to roll in. The weak start to the new year has helped lower expectations and made buying in front of earnings a bit less risky.

And buying in front of earnings does look like it was a pretty good idea, as last night's reports were generally pretty solid. It is now up to the bulls to fan the flicker of flames and see if they can get the fire roaring. To do so, the bulls need to demonstrate their conviction and show that they have a real desire to increase their buying. Until they do that, the bears are unlikely to be too worried.

Despite some better action the last couple of days we still have plenty of technical damage that needs to be repaired. The buying and the volume have not been good enough to shift the trend back up. We still have technical overhead to contend with and we don't have a strong enough surge in buying volume to give us comfort that upside follow-through is likely.

To complicate matters the next two weeks are the peak of earnings season. It is much tougher to measure trends and momentum when a major earnings report or two can shift market sentiment without warning. However, we can gather some clues about market sentiment as we see how good and bad earnings reports are treated. Yahoo! (YHOO:Nasdaq) will be a particularly good example today. The stock is gapping up and there are some positive analyst comments. If sellers jump in and use the strength to dump shares, this market is going to have a tough time moving but if the stock stays strong and holds gains, that bodes well for the broader market.

We have some early weakness again today, which worked out nicely yesterday. The less euphoric opens are more likely to attract buyers who are looking bargains. As we saw over the last two weeks, early strength is an invitation to sell, especially when we are caught in a downtrend.

We have another slew of earnings reports today. Optimism about how they will turn out generally helps to support the market but as we can see from the open this morning, this is not a market that is feeling overly confident.

Oil is trading down a little again, which should help a bit, and we have some economic reports that will help set the tone. The big question in my mind is whether the biotechnology sector can lead the Nasdaq higher if the semiconductors don't start acting better.

Gary B. Smith:

-

Ning täna taas chat.

-

Kuigi USA aastane tarbijahinnaindeksi kasv küündis 3,3 protsendini ja energiale tehtavad kulutused kerkisid 14 aasta kiireimas tempos, siis detsembrikuu tarbijahinnaindeks tõi turgudele kergendust. Energiakandjate hinnalangus tähendas jaemüügihindade 0,1% langust detsembris.

Internetisektor on avanemas plussis, seda tänu Yahoo (YHOO) eile õhtul avaldatud tugevatele majandustulemustele.

Pfizer (PFE) avaldas oma majandustulemused täna eelturul, firma tulud kasvasid aastaga 7% 14.92 miljardile dollarile, kasv tuli peamiselt tänu Lipitori müügiedule ja nõrgenenud dollarile.

Lucent Technologies (LU) teatas kasumist 4 senti aktsia kohta, seda 2,34 miljardi dollari suuruse käibe juures. Ootused olid kõrgemad ning aktsia on eelturul üle 4% miinuses.

Motorola (MOT) mobiilimüük ületas tunduvalt ootusi ning ka kasumimarginaal oli korralik, kuid järgmise kvartali prognoosid olid oodatust nõrgemad.

-

Gapping Up

CHKP +4.5% (reports Q4, guides), OSTK +4% (listings jump 50% following eBay price increase), YHOO +1.9% (beats by $0.02; Jefferies upgrade), PFE +1.6% (reports Q4; Celebrex revs above expectations), PMTC +8.3% (beats by $0.02; guides Q2 revs above consensus), ENMD +8% (announces clinical publication), ASTM +7.5% (stem cell stock continues momentum over last 2 weeks, +24% yesterday), IPIX +6% (Joins GTSI's InteGuard Physical Security Alliance), ESLR +4.2% (continues recent momentum).... Under $3: CDSS +8.7% (Avondale initiates with a $4.50 target).

Gapping Down

AL -9.8% (Novelis unit spin-off), RMBS -5.7% (misses by $0.02; revs in line), MOT -3.8% (reports Q4; downgrades from Piper and Raymond James), LU -3.8% (reports DecQ), NWAC -5.5% (misses by $0.12, ex items), IMOS -4.2% (reports Dec revs), SNDA -4.1% (shares sold by Asia Infrastructure Fund), BIVN -4% (stock offering), TASR -2.7%, NAVR -2.4% (stock offering), RMI -14% (reports DecQ). -

Järgmiseks nädalaks esimesed ideed LHV Pro all ning tuleb lähipäevil lisa.