Börsipäev 22. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

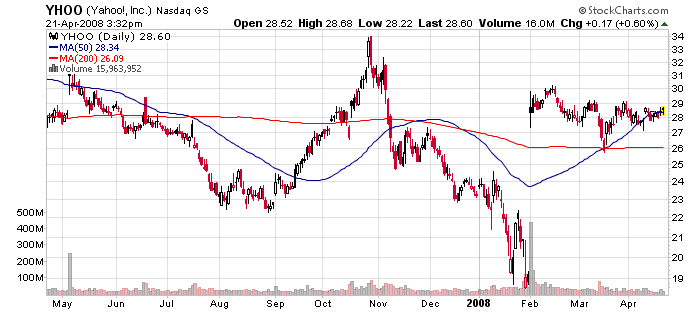

Täna pärast turu sulgemist avaldab oma 1. kvartali tulemused Yahoo (YHOO). Analüütikud ootavad keskmiselt kasumit aktsia kohta $0.09 ja käivet $1.33 miljardit. Citigroup on ettevõtet tulemuste eel kommenteerimas ja soovitab investoritel lisaks finantsnäitajatele keskenduda juhtkonna sõnadele... :

1)... Microsofti (MSFT) pakkumise ja teiste võimalike strateegiliste alternatiivide osas.

2)... üldiste trendide kohta: kas ja kuidas on jahtuv majandus mõjutamas antud tööstusharu?

3)... Project Panama käekäigu kohta.

4)... kuidas on möödunud testperiood uurimaks võimalust outsource’da otsingumootori reklaamid Google’le (GOOG) ja seeläbi oma rahavooge parandada.

Needham ootab konsensusele vastavaid tulemusi ja tuletab meelde, et kuigi Google’i tulemused suutsid ootusi suurelt lüüa, siis see ei pruugi veel tähendada häid tulemusi ka Yahoolt, sest... :

1)... Yahoo käive on rohkem sõltuv kallima hinnaklassi display reklaamidest.

2)... Google on suutnud oma turuosa erinevalt Yahoost kasvatada.

3)... ajalooliselt on korrelatsioon kahe firma tulemuste vahel olnud nõrk.

4)... Yahoo rahvusvaheline tuludebaas moodustab käibest väiksema osa võrreldes Google’ga.

-

Realmoney's kommenteeriti eile sõnaosavalt YHOO'd tulemuste-eelselt kui 'Do or Die' situatsioooni ehk et kui taaskord ollakse investoreid nõrkade numbritega petmas, pole ju põhjust Microsofti pakkumisele nii tuliselt vastu võidelda. Omaette küsimus on muidugi, et milline kardinaalne liigutus siis selle aasta alguses tehti, mis lubaks turuosa kasvu oodata? Parim, mida ettevõttelt võiks ehk oodata, oleks äri stabiliseerimine ja ka turuosa kaotamise lõpetamine.

-

Netflix (NFLX) tuli eile õhtul oma tulemustega, mille järel aktsia 14% sügaviku poole langes, peatudes 50-päeva keskmisel $33.8 juures. Ettevõte on küll olulist turuosa võtnud, kuid see ei pruugi kaua kesta. Pro-forma tulemused olid alla ootuste ning 2008. aasta kasumiprognoosilt kärbiti 13 senti küljest ära.

Tegu on kalli valuatsiooniga aktsiaga ning prognooside langetamine, võimalik konkurentsi tihenemine, ohud marginaalidele ei ole see, mida investorid kuulda tahavad. Peale järelturu kukkumist kauplevad aktsiad 22x 2008. aasta ja 18x 2009. aasta kasumit (hinna $33.8 peal ja arvestades $6 raha aktsia kohta), mis tähendab, et minu jaoks on tegu jätkuvalt päris kallilt hinnatud ettevõttega, seda enam, et olukord võib konkurentsi tugevnedes kiiresti halveneda. -

Lehmannilt täna 2 tugevat reitingumuudatust:

IBM (124.35) tõstetakse 'Overweight' peale ja antakse hinnasihiks $144. Lehmann usub, et IBMi puhul on tänased konsensusootused selgelt liialt konservatiivsed.

Apple'ile (AAPL) (168.16) antakse 'Overweight' soovitus ja hinnasihiks $195. Lehmann usub, et uued iPhone'id ning mitmed uued notebook'id aitavad Apple'i kasumeid kasvatada selle aasta teises pooles.

Teadupärast on Apple homsel järelturul oma tulemustega tulemas - seega peab Lehmanni usk (ja teadmised) ettevõtte numbritesse olema õige suur, sest muidu jäädaks päris lolli näoga olukorda hiljem analüüsima.

-

BJS pani üsna nigelad tulemused, eriti kui arvestada viimase aja aktsia kiiret tõusu. Firma süüdistas pricing pressure't Põhja-Ameerikas. Millised aktsiad oleks esimesed short kandidaadid selle peale?

-

WFT? SII? SLB?

-

WFT -l olid endal ka tulemused, muidu oleks esimene bet. SLB on hiiglane. SII - maybe.

Küsimuse muudab keeruliseks see, et mitmed lähedased ettevõtted on samuti praegu tulemustest teada andmas ja kõik ei räägi päris sama juttu. -

HES?

-

COST

-

sorry:D ei ole COST

-

HES on rohkem nafta ja üle kogu maailma, north america exposure suhteliselt väiksem.

-

Abe, BJS, mitte BJ ;)

-

RES, CPX, PDS?

-

Või koguni NOV?

-

McDonalds raporteeris 1Q kasumiks 81 senti võrreldes analüütikute 70 sendise ootusega.

McDonald's Corp posted higher quarterly profit, boosted by new menu items and strong overseas sales.

The world's largest restaurant chain operator had net income of $946.1 million, or 81 cents per share, in the first quarter, compared with its year-earlier net income of $762.4 million, or 62 cents per share. -

MRO

-

jim, kuigi ma ei ole BJS ega teiste tulemustega eriti kursis, pakuksin esimese hooga FTI, kuna BJS peaks olema üks klientidest. Samuti ehk DRQ.

-

CAM

-

ilmselt oleks hea short ka HAL, mis pakub sarnast tsementeerimisel

baseeruvat teenust. Ettevaatlikuks teeb, et ka HAL on pigem hiiglane. -

Loterii-allegrii lõppes seekord hoopis selle tulemusega, et ma hakkasin BJS $28.5 juurest hästi pisikeste jupikeste kaupa. Kõige lähedasemad peaks olema HAL ja WFT, aga mõlemal olid eile tulemused täitsa korralikud. HAL kinnitas veel lisaks, et hinnad on tõusuteel. Seega oli tõenäoliselt on miss ettevõttepõhine ja võiks eeldada bounce'i. Kus täpselt see tulema peaks, ei kujuta ette, sellepärast ostangi pisikeste juppide kaupa ja jätan kõvasti ruumi alla averagemiseks.

-

Averaged down BJS to $28.2.

-

According to Redbook:

U.S. same store sales fell 1.3% month-to-date for the week ending April 19, compared to previous month. Sales at stores opens at least a year rose 1.7% from the same week a year earlier. -

The Rally Is Great, but It's Not All Rosy

By Rev Shark

RealMoney.com Contributor

4/22/2008 8:32 AM EDT

To emphasize only the beautiful seems to me to be like a mathematical system that only concerns itself with positive numbers.

-- Paul Klee

The market action has certainly improved over the past week or so, but that doesn't mean we can assume that the worst is over. While we are presently enjoying a good rally attempt and have a good chance of some more upside in the near term, there are a number of concerns to contemplate.

One of the biggest worries about the sustainability of the recent market strength is the lack of volume. Yesterday we saw the lightest volume of the year, and volume has been consistently below its 50-day moving average for over a month.

Low volume doesn't mean stocks can't rally, but it does make the upside move less secure. Volume is fuel. It is an indication that big buyers are putting capital to work and are supporting the market. When stocks go up on higher volume, they have better technical support and are less likely to reverse their gains.

The fact that volume has not increased as the market has turned up is an indication that there is a lack of confidence and a hesitancy to deploy capital. That doesn't mean we can't continue to rally but it makes the move less trustworthy.

Another issue facing the market is leadership. We have had a two-tiered market for a while now. A few sectors such as energy, agriculture, mining and steel have had extremely strong momentum, with many of the strongest stocks in those groups making parabolic moves.

Some of the big-cap technology stocks, like Apple (AAPL) , Research In Motion (RIMM) and Amazon (AMZN) have had better momentum, especially following the surprise earnings from Google (GOOG) , but they haven't taken a clear leadership role.

Most of the rest of the market continues to flounder. Financials, for example, have had some rallies, but they remain in a downtrend and have yet to show signs that a bottom is near.

The danger of this narrow and increasingly extended market leadership is obvious. It is especially worrisome because of the inflationary pressures that are inherent in strong energy and agriculture. At some point there will be a day of reckoning as those price increases weigh on the broader economy.

A third worry is that there is little indication that our economic woes are at a bottom. Unemployment is growing, housing prices are falling and inflationary pressures are bubbling up. Many want to proclaim that the worst is behind us, but there is nothing to support that argument other than the triumph of hope over reality.

The market is in better shape at the moment, and with some big earnings reports coming up, that may help to sustain the positive sentiment for now. Just don't get too comfortable with the idea that it is clear sailing to new highs.

We have a little softness this morning as Texas Instruments (TXN) and Novellus (NVLS) issued slightly disappointing reports. Oil continues to hit record highs and we have housing data coming up.

-------------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: VLTR +12.1% (also upgraded to Outperform at Piper), ZRAN +11.2%, FOE +10.9%, WGOV +8.7%, CPO +6.4%, EAT +6.0%, JBLU +5.5%, BSX +5.1%, KCI +4.8%, MICC +4.4%, BTU +3.8%, LOGI +3.7%, NBR +3.4%, CE +3.2%, ALB +2.2%, LXK +2.0%, STLD +1.8%, T +1.6%, ARTC +1.3%, CR +1.2%, DD +1.0%, LMT +1.0%, HSC +1.0%... Other news: BMTI +10.1% (receives written communication from FDA confirming status of ongoing pivotal trial for GEM OS1), ICO +9.8% (still checking), FTEK +6.4% (Cramer makes positive comments on MadMoney), MHS +4.6% (Medco Health Solutions, UnitedHealth Group announce pharmacy services agreement; also upgraded to Buy at Jefferies and upgraded to Buy at Citigroup), TTEK +2.9% (Cramer makes positive comments on MadMoney), IFX +2.2% (prepares for disposal and deconsolidation of Qimonda; will record a write-down of euro 1 billion; FY08 EBIT guidance remains unchanged), VE +2.2% (still checking), AGU +1.4% (profiled in New America section of IBD)... Analyst upgrades: BRLC +13.2% (upgraded to Outperform at Baird), NCC +4.0% (upgraded to Buy at Deutsche Bank and upgraded to Outperform from Market Perform at Bernstein), BCSI +2.2% (upgraded to Buy at Stifel Nicolaus), LOCM +1.9% (initiated with a Buy at Morgan Joseph).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: OMCL -29.3% (also downgraded to Neutral at Broadpoint), BRKR -17.5% (announces foreign exchange losses in Q1 of 2008), BJS -14.6%, NFLX -13.5% (also removed from Alpha List at Piper and downgraded to Neutral at Credit Suisse), QI -13.2%, AAI -12.3% (also announces intention to offer $65 mln of Convertible Senior Notes due 2015 and to offer 14.25 mln shares of common stock), CSL -11.3%, UNH -10.1%, TLAB -8.6%, PKG -8.0%, AVY -6.4%, NVLS -5.0%, AXE -4.9%, COH -4.6%, VNUS -4.5%, CNI -4.3%, STI -3.9%, FDG -3.6%, CME -3.3%, GENZ -2.8% (announces the FDA has informed co that Myozyme produced at the 160L bioreactor scale and Myozyme produced at the 2000L scale should be classified as two products), CVTI -2.7%, USNA -2.6%, MCD -2.3%, TXN -2.3%, GNTX -1.8%... Select healthcare stocks showing weakness following UNH earnings results: CVH -4.3%, WLP -3.8%, AET -3.7%, WCG -1.4%... Select European financial names trading lower with weakness in overseas trading: RBS -3.9% (takes further write-downs, plans $23.78 bln rights issue - WSJ), BCS -3.5%, ING -2.2%, DB -1.5%... Other news: CIT -12.9% (announces concurrent offerings of common stock and convertible preferred stock, for an aggregate of $1 bln), CNB -6.5% (prices a 38 mln share common stock offering at $8/share), ALO -5.5% (to withdraw and resubmit its New Drug Application for EMBEDA)... Analyst downgrades: VNUS -4.5% (downgraded to Hold at Roth), MDTH -4.2% (downgraded to Hold at Stifel Nicolaus), SAY -3.4% (downgraded to Hold at Stifel Nicolaus), PER -1.8% (downgraded to Hold at Keybanc), AMLN -1.1% (downgraded to Underperform at BMO). -

Scaling out of BJS.

-

Flat.

-

Tundub et täna näeme ära 1,6 eur/usd taseme, hetkel uus tipp 1,5991.

-

1.5999 peal räägitakse suurest orderist.

Ehk mõni interveeriv order ja kindlasti kusagil ka terve hunnik barrier optsioone.

(lihtsalt mõtisklen) -

tuli ära! 1,6 ma mõtlen

-

Huvitav, sellele 1,6-le järgnes väga kiire liikumine 1,5975 juurde tagasi. Aga põnev tõesti, kes kuhu stopi pannud on.

-

Mnjah. Üpris hiljuti on hakatud ECB hawkis-t retoorikat arvestama ja leppima intressitõusuga. See pushib ka EURi üles ja ega kaua mingi kunstlik tase püsida ei saa.

-

EUR/USD 1.6 viisid toornafta $119.74-ni

-

Nagu hommikul Netflixi kasinad tulemused/prognoosid välja tõin, nii on ka ettevõte oma kukkumist eilse järelturu $33.8 pealt jätkanud ning kaupleb hetkel $30 eest. Mured ärikeskkonna osas on põhjendatud ning ümber saab neid lükata alles järgmise kvartali konkreetsete numbritega.

-

Yahoo! (YHOO) is set to report earnings after the close today with the markets abuzz that todays results will help clarify what the co's true worth is. To recap, on Feb 1st, MSFT proposed a $44.6 bln takeover bid for YHOO. This valued YHOO's shares at $31/share which at the time was a 62% premium. The proposal would allow YHOO shareholders to elect to receive cash or a fixed number of shares of MSFT common stock. At first glance it appeared that the deal would move pretty quickly but instead, it hit a snag as the argument for the true worth of YHOO grew. Shareholders did not want to accept a $31/share bid, looking more for what they peceived as a fair value deal in the $35-39 area. In response, YHOO mgmt looked to other alternatives to increase the co's net worth. Co has since started a joint venture with long time rival GOOG and discussed a plan under which TWX would fold its AOL unit into YHOO in exchange for a 20% stake. The GOOG JV will be interesting as the co is expected to comment on the effectiveness of the outsourcing of ad revs. GOOG did not comment on the results but we would expect YHOO to provide positive commentary and a bright outlook as they continue their case that their shares are worth more than $31/share. General expectations for the quarter are positive as it is believed that the co will pull out all the stops in order to beat their current consensus estimates (currently First Call consensus is EPS of $0.09 and Revs ex-tac of $1.32 bln). Recall last quarter the co was able to beat estimates with the help of lower stock comps and a lower tax rate and we would expect YHOO to see some surprise upside in these two categories this quarter as well. Other areas we will be paying attention to include SG&A (was 49.8% of revs in Q4), Operating Income (10.4% of revs in Q4) and shares outstanding (was 1.394 bln in Q4). We would also expect the co to boost its Y08 outlook. Current co guidance stands at total revs $7.2-8.0 bln; Revs ex-tac to be $5.35-5.95 bln; and Operating Income before depr, amort, and SBC comp of $1.725-1.975 bln. We would expect the conference call to be dominated by discussions of the MSFT offer, GOOG JV and AOL possibilities.