Börsipäev 31. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

Täna avalikustatakse USA SKP 2. kvartali näit. Konsensus on 2.3% juures. Oodatust suurem number vähendaks muresid USA majanduse pärast ning oodatust väiksem vastupidiselt mõjuks negatiivselt. Samuti on tund enne turu avanemist esmaste töötu abirahade number, mida oodatakse suurusjärgus 395 000. Eelmine nädal oli number üle 400 tuhande ning kui ka seekord oleks näit sellest suurem, mõjuks see turgudele ilmselt negatiivselt.

Varahommikused futuurid pole pärast eilset suurt tõusu aktsiaturul aga praegu eriti liikunud. -

Paar päeva tagasi panin siia graafiku Eesti OMXT'st, kus oli kogunenud 20 languspäeva järjest. Ja et ainult negatiivne ei saaks kajastatud, panen nüüd OMXT graafiku siia uuesti, mis on kahe päevaga üle 5% plussis. Viimastel päevadel on võrreldes veebruari, märtsi, aprilliga ka pisut käivet taga olnud.

-

2.3% USA SKP kasvuks oleks väga hea tulemus. Analüütikud usuvad, et teise kvartali kasvu taga on põhiliselt maksusoodustused. Kongress lootis eelmisel kevadel toetada majanduskasvu ja tarbimist maksukompensatsiooni tšekkide näol. Täna avaldatav majanduskasv on kaugel majanduslangusest, kuid tarbijad ja investorid on mures, mis juhtub järgmistes kvartalites, kui maksusoodustused ära kaovad.

Pessimistlikult on meelestatud ka Deutsche Bank:

"Without the contribution from external trade, the GDP data would show an economy that would already be contracting," said Deutsche Bank which forecast a 1.0 percent growth rate. "Growth should recover only gradually next year unless there is more fiscal stimulus. There has been little over-investment in this cycle, which should help cushion some of the downside risk to the economy."

-

Kui jätkata makrouudistega, siis inflatsioon kiirenes Euroopas 4.1% peale ehk hinnatase on tõusnud 0.1% juunist saadik. Euroopa Keskpanga selle aasta inflatsioonimäära sihiks oli 2%, mis on rohkem kui kahekordselt ületatud.

-

Deutsche Bank (DB) täna avaldatud majandustulemustes kajastus 63-protsendiline netokasumi langus teises kvartalis. Peasüüdlasteks on varade mahakirjutamised ja tublisti langenud tulu. Sellegipoolest on paljud analüütikud üllatunud, sest prognoositud oli palju hullemat. Netotulu langes aastaga 39%.

-

Hiina valitsuse konservatiivne poliitika saab kiita ning riigi võlareiting tõstetakse S&P poolt A+ peale.

Bloomberg.com reports China's debt ratings were raised by Standard & Poor's after its foreign-exchange reserves surged to a record $1.8 trillion, helping the world's fastest-growing major economy withstand weaker U.S. demand for exports. China's long-term rating increased one level to A+, the fifth-highest grade, putting the country on a par with Italy. Hong Kong's rating rose the same margin to AA+. The nation's economy grew more than 10% for a 10th straight quarter in the three months through June and the currency reserves climbed by a third from a year earlier. An improved government balance sheet offers "greater resilience'' in the event of a sharp economic downturn, S&P said in a statement.

Meeldetuletuseks veel, et Hiinasse on võimalik investeerida näiteks läbi USA börsil kaubledava fondi sümboliga FXI. -

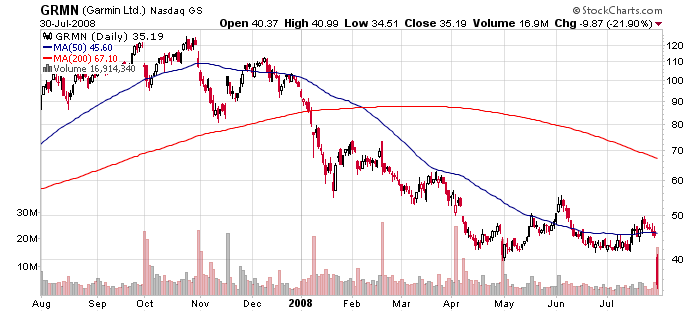

Garmin'i (GRMN) aktsia langes eile tervelt 20% võrra, sest ettevõtte jäi oma Q2 tulemustega turu ootustele alla igas elemendis. Minu arvates on tegemist hea näitega, mis juhtub momentum aktsiatega pärast esimesi kasvu pidurdumise märke. Umbes aasta eest uurisin ettevõtet lähemalt, kui aktsia hind kauples $100 tasemel, mis tähendas 30-40kordseid kasumikordajaid. Ometigi olid enamik analüütikutest firmast vaimustuses, tõstes võidu hinnasihte järjest kõrgemale.

Tänaseks on selge, et Personal Navigation Device turg on kiiresti jahtunud: navigatsiooniseade on muutunud samasuguseks laiatarbekaubaks nagu näiteks mobiiltelefon ning see tähendab langevaid hindu, mis omakorda tähendab langevaid marginaale tootjate jaoks. Eilsel konverentsikõnel prognoosis Garmin, et 2008. aastal langevad ASPd (keskmine toote müügihind) 25% võrra. Samas suudetakse sisendhindu langetada umbes 20% võrra. Lisaks ei ole kaasa aidanud ka nõrgenev tarbija, millele on viidanud oma kasumihoiatustes ka teised tarbeelektroonikat tootvad firmad.

Seega järjekordne näide, kuidas turu ootused paisuvad järjest kõrgemale, et ühel hetkel järsult lõhkeda.

-

Green Mountain Coffee (GMCR) beats by $0.04, reports revs in-line; guides FY08 EPS above consensus; guides FY09 EPS above consensus (38.52 )

Reports Q3 (Jun) earnings of $0.25 per share, $0.04 better than the First Call consensus of $0.21; revenues rose 43.3% year/year to $118.1 mln vs the $119.2 mln consensus. Co issues upside guidance for FY08, sees EPS of $0.79-0.81 vs. $0.77 consensus; co sees revs up 44-46%, which equates to approx $492-499 mln vs $497.82 mln consensus. Co issues upside guidance for FY09, sees EPS of $1.20-1.30 vs. $1.13 consensus.

Tegemist oli prognoositud arenguga, sest ootasime ka meie biitimist. Tegemist on aktsiaga, mis läks eile neutraalse soovitusena üles ka Pro alla. Olime kestva momentumiga arvestanud ning ka oma analüüsis ootasime järgmisest aastast 20%-list konsensuse kasumi löömist, mis tänase seisuga oli põhjendatud ootus. Hoiame arengutel silma peal ning ootame sobivat momenti., kuna tegemist on ettevõttega, milla kasumikasv võib sama kiiresti ära kukkuda, kui see tulnud on.

-

tunduks et IMCL võiks 65 pealt alla tulla 64 at least

-

Weekly Initial Jobless Claims 448K vs. 393K consensus; prior revised to 404K from 406K

Q2 GDP q/q-advanced +1.9% vs +2.3% consensus, prior +1.0%

Turud saatis laangusse eelkõige esmaste töötu abirahade hirmutavalt suur number... -

The Q4 GDP was revised to -0.2% compared to previous figure of +0.6% ... seega tehnilise definitsiooni kohaselt on USA vähemalt 1 kvartalis siiski majanduslangust näidanud

-

Mismoodi on seotud töötuse määr nafta hinnaga? Miks nafta hind selle uudise peale üles hüppas?

-

töötus - > USD/EUR -> naftahind

-

Dollar nõrgenes selle data peale lihtsalt.

-

Briefingu poolt Q2 kokkuvõte üpriski optimistlik

Q2 GDP Much Stronger Than Headline Suggests

The 1.9% increase in second quarter GDP was less than the expected 2.3% gain. However, this was due to a much larger-than-expected negative impact from inventories. The inventory calculation sliced a whopping 1.9% off the change. Real final sales, which economists consider a better measure of underlying demand, rose at a 3.9% annual rate... The underlying trends in consumer spending, business investment, exports, and government spending were generally better than forecast. Real personal consumption expenditures (consumer spending) rose at a 1.5% annual rate. Nonresidential construction was up at a 14.4% annual rate. Investment in software and equipment was weaker than expected, falling at a 3.4% annual rate... Strikingly, residential construction fell at "only" a 15.6% annual rate. That is down from about 25% the previous three quarters. This category is likely to go near flat in the third quarter, eliminating what has been a major negative on GDP. Government spending was up at a 3.4% annual rate, and exports continued to boom with a 9.2% annual rate of increase... The initial take on this number may be slightly disappointing, but the breakdown of the trends is encouraging. The negative impact from inventories won't continue. It may well reverse in the third quarter, and if the trends in other categories remain reasonably stable, the third quarter real GDP increase will exceed 3% (as it would have this quarter were it not for the inventory calculation)... The data are much stronger than the first glance would suggest. Even at a 1.9% annual rate of increase, however, and with the third quarter now setting up very nicely for a strong gain, perceptions of the underlying strength of the economy should improve over the next few months.

-

Briefing ongi überbullish alati :)

Aga Q2 on siiski ajalugu ja näiteks täna 16.45 laekuv juulikuu Chicago PMI, mis on ajalooliselt väha hästi ennustanud ette ka homme laekuvaid juuli ISM numbreid võib Q2 GDP mõju oluliselt pehmendada kui jätkub hea trend juulikuu datas ... Michigan Sentiment - Consumer Confidence - ADP ... -

The Technicals Look Better But Troubles Remain

By Rev Shark

RealMoney.com Contributor

7/31/2008 8:31 AM EDT

There are two kinds of people, those who finish what they start and so on.

--Robert Byrne

Substantial back-to-back rallies for the first time since April has market players feeling a bit more confident as the usual suspects rush to call a market bottom once again.

One of these days, the bottom-callers will get it right and maybe even it will be this time. But in a market like this, it is better to set the emotions and sensationalism aside and make sure you have a solid plan in place for dealing with things.

While we have seen some definite technical improvement with a technical follow through and a higher high in the major index charts, things under the surface are a bit more problematic.

First and foremost, this recent rally has been driven primarily by dead cat bounces in broken financial and energy stocks. We have little upside leadership.

This can be easily seen in the list of new highs, which only numbered about 80 or so yesterday versus 120 new lows. We just don't have many stocks hovering around highs which is what you want to see to indicate leadership.

Position traders have been complaining lately that if you have been waiting for chart setups, you have missed out on most of the strength in this market. The big moves have all been from bounces in broken stocks. These are not breakout moves or stocks moving out of bases.

That doesn't mean that the moves aren't tradable, but it does indicate that you better not be thinking about longer-term holds.

After the last two days, the bulls have the advantage and it is their game to lose. We are now a bit technically overbought and need to digest some gains so we can afford to pullback a bit. But the real test will come next week when we see if the buyers are willing to add further exposure.

In the short-term. things get very tricky because financials are extended and the only real leadership is biotechnology and some medical stocks. Biotechnology is getting a bid again after takeover talk for Imclone (IMCL) .

But what we need is some better action, particularly in technology. Technology stocks have been very disappointing relative to the broader market and can't seem to gain any traction, although they are the 'go to' group should the market broaden out.

The bulls have a pretty good looking bounce going, but so far it still qualifies as just another bear market rally. It certainly can run higher and the technical patterns support that, but we may need some backing and filling at this point, and we definitely need some better leadership to develop.

We have a slightly positive start as overseas markets were mostly up. Oil is pulling back a bit but gold is bouncing.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: PDGI +16.3% (also upgraded to Buy at Jefferies), MOT +13.3%, DXPE +13.0%, TTEK +12.6% (also awarded 2 energy projects for approx. $28 mln and awarded $64 mln BRAC design-build project contract), LKQX +12.3%, ARRS +12.0%, ANDE +10.5%, OIIM +9.4%, CGV +8.9%, GOLD +8.8%, TYC +8.2% (light volume), AMCC +7.9%, SHPGY +7.9%, MTZ +7.8% (also upgraded to Outperform at FBR), SYMC +6.7%, MRO +6.4% (also announces it is evaluating separation of businesses; decision expected during 4Q08), FSLR +6.3%, TRN +6.3%, WYN +5.8%, ITRI +5.0%, AZN +4.7%, SBUX +4.4%, FLS +4.4%, MUR +3.7%, GMR +3.6% (light volume), IP +3.6%, ESRX +3.6%, SWN +3.5%, FTE +3.5% (light volume), CVC +3.5%, ULBI +3.2%, OI +3.0%, TRCA +2.7%, WLL +2.5% (upgraded to Outperform at RBC), CIR +2.0%, NLY +1.3%, GG +1.3%... M&A news: IMCL +40.8% (Bristol-Myers Offers To Acquire Imclone For $60/Share)... Select metals/mining stocks trading higher with strength in commodities and dollar weakness: LMC +3.1%, BHP +2.3%, AU +2.0%, RTP +1.9%, BBL +1.7%, GFI +1.5%... Select solar stocks showing strength boosted by FSLR results: SOLF +6.8% (signs 30MW sales contract with Martifer Solar), SOLR +5.2% (still checking), CSUN +4.7%, YGE +4.7%, SOL +4.3%, JASO +3.9%, CSIQ +3.6%, ESLR +3.5%, SPWR +2.6%, STP +2.4% (the co and PV Crystalox Solar PLC, a specialist multicrystalline solar wafer manufacturer, announce they have signed an initial five-year silicon wafer supply agreement)... Other news: CADX +52.6% (announces FDA concurrence with clinical development plan for Acetavance), GVHR +7.2% (to engage in strategic discussions), AMLN +5.5% (still checking), QGEN +5.1% (still checking), MTL +5.0% (Russia widens coal probe to Evraz, Raspadskaya - WSJ), AMD +4.7% (still checking), PCLN +2.5% (will replace KEM in the S&P MidCap 400), RIMM +1.9% and RHT +1.0% (Cramer makes positive comments on MadMoney)... Analyst comments: SGP +6.0% (upgraded to Buy at Merrill), GTE +2.6% (upgraded to Overweight at Weisel), DELL +2.1% (upgraded to Outperform from Neutral at Cowen).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: BARE -22.0% (also downgraded to Neutral at Piper), AKAM -20.6% (also downgraded to Market Perform at FBR), HOLX -17.9% (also downgraded to Hold at Jefferies), NHWK -17.0%, SSYS -14.4%, ARCI -13.5% (light volume), BT -10.8%, CNX -10.7% (light volume), THQI -9.7% (also downgraded to Hold at Lazard, downgraded to Hold from Buy at Sterne Agee and downgraded to Perform at Oppenheimer), NEWP -9.0% (also downgraded to Hold at Brean Murray), GGP -8.4% (also downgraded to Sell at Citigroup), OII -8.3%, HRS -7.1%, LVS -5.9%, PH -5.1%, MA -5.1%, FLDR -4.9%, HMN -4.6%, DIS -3.7%, TSS -3.5% (also downgraded to Equal Weight at First Analysis), SNY -2.9%, RDS.A -2.4%, XOM -2.1%, MO -2.1%, AVB -2.0% (also downgraded to Underperform from Neutral at Merrill), V -1.8% (also upgraded to Buy from Add at Calyon), UNM -1.4%, SFI -1.1%... Select mortgage/financials pulling back: MBI -4.9%, FNM -4.8%, LEH -4.6%, FRE -4.0%, MER -3.8%, WB -3.4%, BAC -3.2%, WM -3.0%, C -2.3%, WFC -1.9%, GS -1.9%, MS -1.8%, JPM -1.6%... Other news: UN -9.0% (falls in Europe on lower 2Q volumes - DJ), GM -6.1% (still checking), TM -2.9% (Toyota Motor group cos Denso, Aisin Seiki and Toyota Industries were trounced after cutting their outlooks, casting a cloud over the mkt), CHKE -2.2% (cuts quarterly dividend to $0.50 a share from $0.75; ends strategic alternative process), ASML -1.5% (still checking)... Analyst comments: LYG -4.4% (downgraded to Hold at Deutsche Bank), KEY -2.2% (downgraded to Neutral at Baird), AVP -1.4% (downgraded to Hold at Deutsche Bank), GRMN -1.3% (downgraded to Hold at Wedbush), EXR -1.1% (downgraded to Hold at Deutsche Bank). -

France Telecom CFO says no desire to look again at TeliaSonera - DJ

-

Euroopa ja Aasia põhiindeksid:

Saksamaa DAX -0.36%

Prantsusmaa -0.60%

Inglismaa FTSE 100 -0.73%

Hispaania IBEX 35 -0.16%

Venemaa MICEX -0.67%

Poola WIG -1.41%

Aasia turud:

Jaapani Nikkei 225 +0.07%

Hong Kongi Hang Seng +0.18%

Hiina Shanghai A (kodumaine) -2.25%

Hiina Shanghai B (välismaine) -1.09%

Lõuna-Korea Kosdaq +0.17%

Tai Set 50 +1.31%

India Sensex +0.48%

-

Selgelt on näha, mis juhtub aktsiaga, kui ootused on liiga kõrged. 2009. aasta kasumiprognoosi tõsteti 10% võrra, kuid GMCR on 9% miinuses. Sellist reaksiooni olemegi oodanud, kuigi mitte ilmtingimata tänaste tulemuste peale.

-

short the f...cking AKS

-

lugu on 2 päeva vana ja tegi oma moovi ära

-

62.41 short

-

pool läks 62 juures kinni ..ülejäänud hoian.

-

out 62 juurest äkki jääbki üles

-

Pole paha abesiki. Vähemasti kui aktsia ei liikunud ideele järgi, siis said õigel ajal eest ära. Ilus.

-

WaMu lendas üle 20% uudise peale: An activist British hedge fund has taken a 6 percent stake in Washington Mutual Inc as the largest U.S. savings and loan tries to rebound from billions of dollars of mortgage-related losses. Toscafund Asset Management revealed the 105.5 million share passive stake in a Thursday filing with the U.S. Securities and Exchange Commission. The London-based fund also reported a 5.1 percent passive stake, or 33.5 million shares, in Sovereign Bancorp Inc , the second-largest U.S. thrift, a separate filing shows.

-

Proovisin WM 5.77 shortida, aga no luck :( Päris üllatav eksole, et kui keegi müüb aktsiaid, siis keegi teine ostab neid jällegi samal ajal. On see väärt sellist tõusu? Helgemadki pead kui see Toscafund on lutti saanud, nende ost küll fundamentaalset muutust ei too.

-

Tõusu põhjus jääb natuke arusaamatuks küll.

Shortimisega võib probleeme olla, vähemalt meil ei ole praegu shorditav. -

Kui maakler oleks aktsiaid laenanud, siis nüüd @5.42 kataks ära

-

Short squeeze saab valus olema, juuli short interest üle 19%.

-

Paistab, et eufooria hakkab siiski üle minema ja finantssektor vajumas tagasi tavapärasesse punasesse. Kes WM põrkest kasu tahavad lõigata siis võib kaaluda aug 6 call shorti (katmise peale tuleks siiski mõtelda) Impl vol on ahvatlev.

-

LHV Pro all läks lühikeseks müümise ideena äsja üles Kellogg (K). Põhjuseid leiab juba Pro alt ja ühtteist kommenteerisin ka eilses börsipäeva foorumis.

-

kas mingi ajaline horisont on ka või mitte?

-

Tegu on siis nii-öelda 'investment shordiga'. Ettevõtte eest välja käia tulev hind on meie silmis paisunud lihtsalt liiga suureks ning suure tõenäosusega on turg seda aja jooksul ümber hindamas. Aga ajahorisondiks hetkeseisu põhjal maksimum ca paar kvartalit.

-

tänud

-

greenspan ja tema kommentaarid...suutsid ralli rikkuda...

-

Greenspan ei olnud just kõige optimistlikum FNM ja FRE osas... Tagasihoidlikult öeldes.

-

nii, asi läheb huvitavaks: LHV Pro oponeerib Tark Investor'le

vastavalt K lühike ja K pikk

sihid 45 ja 59 -

Speedy, seda on ka varem juhtunud - 2007 kirjutati LHV Pro all, et Motorola on üks hea ettevõte ning parem investeering kui Nokia. Meie tees oli, et Nokia on hea rahapaigutus ning Motorolast tasub eemale hoida, kuna ettevõte executioniga raskustes (marginaalid nõrgemad) ning kaotamas turuosa.

Meie Nokia idee läks +46% kasumiga lukku

LHV Pro Motorola idee praegu -52% -

Nüüd siis vastupidi näited LHV-lt? Või ei ole te komprat kogunud?

-

Aga Kelloggi puhul on ka ajahorisondid erinevad, meil investeerimisidee ja paar aastat, LHV puhul "maksimaalselt paar kvartalit". Tuleb tunnistada, et mul pole väga tugevat veendumust, mis Kelloggiga lähikuudel juhtuda võiks, aga LHV-l tundub, et siis on. Kuid peamine tees ei saa olla "tarbija hakkab vaatama mitte-bränditud toodete poole", sest see protsess ei muutu nii lühiajaliselt oluliselt.

-

Gentlemen, place Your bets!

-

kas see K siht 59 investeerimisideena ja paari aasta jooksul (tootlus ca 14 %) veits närune ei tundu? Ka tähtajalise hoiusega saaks selle ajaga ju rohkem ja ilma mingi riskita...