Börsipäev 7. mai

Kommentaari jätmiseks loo konto või logi sisse

-

Täna on oodata Euroopa Keskpanga intressiotsust, valdavalt prognoositakse 0.25% suurust kärbet, mis jätaks intressid 1% peale. Samas oodatakse vihjeid ka QE suhtes.

-

Maailma ühe parima aktsendiga onu Trishee olla teatanud otsustusõigusega ECB kõvematele kärbestele, et nad võiks edaspidi meedia kuuldes mitte suud lahti teha. Noh ikka selleks, et meedias ECB "behind the curve" poliitikat oleks vähem põhjust kottida ning sisevastuolud välja ei paistaks. Selline Brezhnevi-aja maik on asjal man' küll :-)

-

Teisalt on nad "behind the curve" suhtes ise teistsugusel arvamusel, sest Trichet on üsna otsesõnu välja öelnud, et ilmselt jääb tänane viimaseks kärpeks.

-

Tänaste kvartalitulemuste avaldajate hulka kuuluvad teiste seas General Motors (GM), Cryptologic (CRYP), DIRECTV (DTV), Hansen Natural (HANS), Nvidia (NVDA) ja VeriSign (VRSN). Ühtlasi avaldavad enne turu avanemist tulemused veel Imax Corporation (IMAX) ning Pro varasemad ideed Lamar Advertising (LAMR) ja Sotheby's (BID).

-

Vitali (VTAL) eile õhtul avaldatud tulemused olid oodatult tagasihoidlikud. Tulude osas jäädi analüütikute prognoosidele alla, kuid kulude kokkuhoiu tõttu teeniti EPSi -$0.02 turu oodatud -$0.04 vastu. Haiglad on kulutuste tegemisel ettevaatlikud ning müügitsükkel on pikenenud. Positiivse poole pealt on Vitalil jätkuvalt globaalselt parim toode ning arvestades seda, et ettevõttel on bilansis vaba raha ca $10 aktsia kohta, kaupleb aktsia täpselt rahal (eilne sulgemishind $10). Seis ei ole kindlasti nii halb, pigem on aktsia fondide vaateväljast kõrvale jäänud. Toode on hea ja tulevikuperspektiiv tugev - selle tõestuseks ostetakse ka aktsiaid tagasi.

Kuna juhtkond peab tulemustejärgse konverentsikõne alles täna õhtul, siis pikem kommentaar Pro alla tuleb hiljem.

-

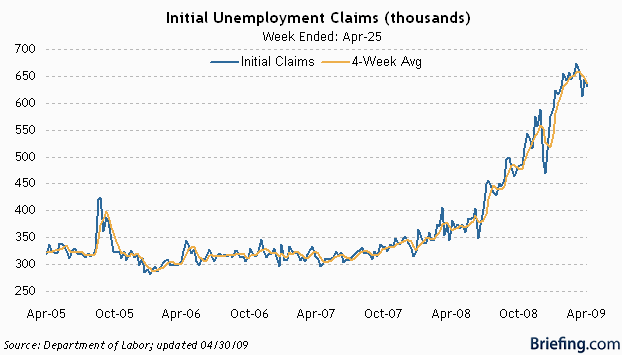

Tund aega enne turu avanemist tuleb esmaste töötu abiraha taotlejate number. Viimastel nädalatel on numbrid hakanud allapoole tulema ning optimisminoot põues põksuva südamega aktsiaturge jälgivad investorid vastupidist stsenaariumit täna kindlasti näha ei tahaks. Seekord ametlikuks ootuseks 635 000 (eelmine nädal oli 631 000), mitteametlikult oodatakse tõenäoliselt paremaid numbreid, Briefing on ise väljas näiteks 620 000lise numbriga.

-

Eelturul ei julge veel keegi buldooseri ette astuda ning väikeste sammude kuid suure järjekindlusega liigutakse üha kõrgemale. S&P500 +0.7% @ 924 punkti. Huvitav, kui paljud toolita jäävad, kui muusika korraks seisma pannakse?

-

"Buy in May and stay in" hoopis tükkis ? See muusika ei tahagi justkui lõppeda.

-

vahetult enne keskpanga kohtumist on JPMorgan ja Merrill Lynch tõsmas oma nägemust eurotsooni kasvu osas, prognoosides pööret paremuse suunas juba 2009. aasta keskel, muutes veelgi küsitavamaks, kas EKP kavatseb täna radikaalsemaid meetmeid käiku lükata.

Merrill: While we slashed our call for 1Q GDP from -1.7% to -2.0% qoq, we have raised our call for 3Q from -0.2% to +0.1% qoq. In other words, the recession may be even a little deeper than we thought upon publishing our last recovery checklist on 31 March, but it may also be a little shorter.

JPM: Now we expect a much more moderate contraction in the current quarter, followed by stagnation in the third quarter and a return to positive growth in the final quarter.

-

Inglismaa keskpank jättis intressimäärad 0.5% peale. Varade ostuprogrammi suurendati 50 miljardi naela võrra 125 miljardi peale.

-

Bank of England on küll Suur-Britannia e. Ühendkuningriigi keskpank, aga tühja sest, analoogselt võib öelda Harjumaa keskpank ja küll lugejad, kui nad just lauslollid pole, aru saavad, et tegemist on Eesti Pangaga.

-

Madis & Joel, mis on teie arvates peamised põhjused, miks Vital Images (VTAL) kaupleb bilansi sularaha hinnaga (võlg=0)? Nad ju omavad super toodet ja müüvad seda kuidagimoodi ka praegusel raskel ajal. Kas neto-rahavoog on +/-?

-

wifebeater, ma kirjutame ka, et intressimäärade otsusi teeb FED, mitte FOMC. Pigem küsimus selles, kuidas lugeja aru saab, üle ei maksa pingutada.

-

wifebeater... kui pindu tahad lõhki hakata ajama, siis ikka "Suurbritannia", mitte ebakorrektne Suur-Britannia.

-

Ouna Ants, Vitali juhtkond loodab EBITDAt aasta lõpuni positiivsena hoida, esimesel kvartalil seda suudeti. Intresse kandvaid kohustusi põhimõtteliselt pole (EV -$1.5). Üks põhjus aktsia allamüügil on kindlasti olnud fondide väike huvi - market cap vaid $145M. Teisalt pole selge, millal haiglad kulutusi taas tõstma hakkavad - DRA on tugevat mõju avaldanud. Samas on toode tõesti hea, saanud üle maailma ainult positiivset vastukaja. On oht, et kui praegu eriti müüa ei suudeta, tuleb peale mõni konkurent uue tootega, samas neid eriti ei paista (alternatiivsete toodete kvaliteet on valgusaasta kaugusel) ning ega Vitalgi arendusel maga.

-

Mul on lihcalt šotlastega kokkupuuteid olnud, sellest too pindude lõhkumine. Nad suhtuvad Inglismaasse ~ samuti, kui nõuka ajal eestlased suhtusid sellesse, kui meie elukoha kohta Venemaa öeldi - vanemad inimesed ehk mäletavad veel.

-

ECB -0.25%.

-

Goldman Sachs tõstab American Expressi (AXP) soovituse 'müü' pealt 'neutraalsele'.

-

Imax beats by $0.02, beats on revs.

Reports Q1 (Mar) loss of $0.06 per share, $0.02 better than the First Call consensus of ($0.08); revenues rose 43.4% year/year to $33.7 mln vs the $30.6 mln consensus.

Pikem kommentaar tuleb Pro alla.

-

GS downgreidis samas STI, mõlemad stockid ikka umbes samapalju üleval

-

Deflation? Paljude toiduainete varud (nt teravili) on maailmas tegelikult väga tagasihoidlikud ning häired tootmises võivad kaasa tuua väga suuri hinnaliikumisi. India saagi ikaldumine tõotab kaasa tuua suhkru uued hinnarekordid.

-

Euroopa Keskpanga intressimäära otsuse järgset pressikonverentsi saab kuulata siit.

-

Analüütikud jätkavad ettevõtete kiitmist - Briefing: Intel added to Focus List at Credit Suisse. Credit Suisse adds INTC to their U.S Focus List based on a recovery in corporate spending in 2H 2009 and/or 2010; and the stock tends to follow the directional move of gross profit margins which are poised to increase from the mid 40s in 1H 2009 to the high 40s in 2H09, driven by higher utilization rates and lower 32nm costs.

-

Initial claims 601K vs oodatud 635K.

-

Saksamaa DAX +1.40%

Prantsusmaa CAC 40 +1.80%

Inglismaa FTSE 100 +2.56%

Hispaania IBEX 35 +2.04%

Venemaa MICEX +5.14%

Poola WIG +1.35%

Aasia turud:

Jaapani Nikkei 225 +4.55%

Hong Kongi Hang Seng +2.28%

Hiina Shanghai A (kodumaine) +0.19%

Hiina Shanghai B (välismaine) -0.11%

Lõuna-Korea Kosdaq +0.77%

Tai Set 50 +0.81%

India Sensex 30 +1.37%

-

Momentum's Tightrope

By Rev Shark

RealMoney.com Contributor

5/7/2009 8:42 AM EDT

The reason people find it so hard to be happy is that they always see the past better than it was, the present worse than it is, and the future less resolved than it will be.

-- Marcel Pagnol

The strong rally in banks continues this morning as we await the actual stress test results. I'm not sure there are any surprises yet to come, but the market is quite pleased with the results that have been leaked so far.

As it stands now, according to The Wall Street Journal, JPMorgan (JPM) , Goldman Sachs (GS) , MetLife (MET) , American Express (AXP) , Bank of New York (BK) and Capital One (COF) , won't be required to raise new capital, while Bank of America (BAC) , Wells Fargo (WFC) , GMAC, Citigroup (C) , Regions Financial (RF) and State Street (STT) will need to raise funds. We still don't know what the results are for six more banks, but the market reaction even to BAC, which must raise the most money, has been very positive.

The market has been quite frenzied over this bank news, and the question for us is whether we have now overshot and should get ready for some profit-taking or whether the increased clarity about the health of banks going to keep this momentum going. The atmosphere right now seems to be that the problems are addressed and we are on the road to recovery.

It is difficult not to feel a bit contrarian, like Doug Kass, about such exuberance, but the power of momentum has been clearly illustrated over the past couple of weeks. It just doesn't end suddenly -- there are too many folks who have been left out who want in and are provide underlying support. Institution fund managers tend to buy pullbacks rather than chase strength, and they are keeping the market from having any major dips.

Aside from the banks, we saw some extremely strong momentum in the energy and commodity sectors yesterday. The logic is that the economy is improving and therefore demand for oil, coal, steel and such will grow. With the way banks have been running and the overall increased in confidence, it is not surprising to see that theme develop.

Lately some very big moves have occurred in select small-caps. Momentum traders have been willing to chase some moves, and it has been paying off. We saw some profit-taking in some names yesterday but traders aren't backing off much. They have had a taste of some positive action and they are hungry for more.

So we continue to walk the tightrope of big momentum. We obviously are a bit frothy, especially given how the banks are jumping this morning, but the strong momentum and fear of being left out are causing tremendous frustration for those who are anxious for a pullback.

My approach here is to give this momentum great respect and play to the upside but to consistently take gains and look for some opportunities to put on hedges when we show some signs of cooling off.

We have a big open this morning, but it sure isn't easy to chase. I suspect we'll see some selling on the open but I wouldn't count on the bulls backing off too much for too long. They have the advantage and they are pressing hard.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance/same store sales: VICL +38.6% (Vical and U.S. Navy to expedite development of H1N1 pandemic influenza vaccine), KNDL +16.7%, PLCE +14.9%, SXCI +12.2%, LOCM +12.2%, AMPL +12.0%, BONT +10.1%, ANF +9.6%, UL +9.1%, ONNN +9.0%, UN +8.0%, SIG +7.4%, BJ +6.7%, TGT +5.5%, GM +5.4%, FLY +4.8%, GPS +4.5%, CENT +4.1%, PRU +4.0%, JCP +3.9%, TS +3.8%, WMT +3.6%, BKE +3.1%, GG +3.0%, LINE +2.6%, TI +2.4%, SUN +1.9%, COST +1.9%, CLRT +1.8% (light volume), , MSSR +1.2%... M&A news: NSHA +122.6% (to be acquired by Cenveo; the total consideration is valued at $6.88 per Nashua share)... Select financials showing strength: FITB +23.7% (upgraded to Neutral from Sell at Goldman- Reuters and upgraded to Outperform at Keefe Bruyette), GNW +18.1%, COF +17.0% (upgraded to Buy from Neutral at Goldman- Reuters), BAC +15.5% (upgraded to Overweight at Morgan Stanley), AIG +14.1%, SNV +13.3%, LNC +12.4%, DFS +12.3%, SNV +11.9%, RF +10.1%, IRE +10.1%, HIG +8.9%, C +8.8%, STT +8.3%, ZION +6.8%, BK +6.7% (added to Conviction Buy list at Goldman- Reuters), WFC +5.7%, HBC +4.5%, MS +4.3%, CIT +4.2%, JPM +4.1%, AXP +3.4% (upgraded to Neutral from Sell at Goldman- Reuters), HBAN +2.9% (Cramer makes positive comments on MadMoney), GS +1.4%... Select metals/mining names trading higher: RTP +3.2% (upgraded to Overweight at Barclays), MT +2.8%, BHP +2.6%, AAUK +2.3%, BBL +1.3%... Other news: VNDA +778.7% (confirms FDA approves Vanda Pharmaceuticals' Fanapt for the treatment of schizophrenia; also upgraded to Buy at Natixis Bleichroeder), BLDP +14.4% (announces sale of fuel cell distributed power generation solution to FirstEnergy), CDNS +13.6% (Cramer makes positive comments on MadMoney), DDR +6.7% (announces new secured debt financings for $125 mln, Otto transaction scheduled to Close May 11), IPXL +6.1% (receives final FDA approval for generic depakote extended-release 250mg tablets), TS +3.8% (still checking), HGSI +3.3% (Human Genome Sciences and Novozymes announce amendment to albumin fusion license agreement), CVX +1.6% (confirms discovery offshore Republic of the Congo)... Analyst comments: ACAS +6.1% (upgraded to Market Perform at Keefe Bruyette), TER +6.1% (added to Conviction Buy list at Goldman- Reuters), ERIC +2.3% (upgraded to Buy at BofA/Merrill).

Allapoole avanevad:

In reaction to disappointing earnings/guidance/same store sales: FOE -29.8%, DGIT -19.8%, EZCH -18.7%, HT -16.4%, BEE -16.1%, TBSI -14.8%, FTK -14.7%, CECO -14.5%, OCNW -13.7% (light volume), HOTT -13.5% (also removed from Top Picks List at Friedman Billings), MIC -12.2%, BBBB -10.4% (also downgraded to Outperform from Strong Buy at Raymond James and downgraded to Buy from Strong Buy at Davenport), IO -9.5%, ANSS -8.4%, NICE -7.9%, WEL -6.9%, SATC -6.0%, USU -5.1%, SYMC -4.8% (also downgraded by multiple analysts), SMSI -4.4% (also downgraded to Neutral at UBS), BCS -4.2%, EXPD -3.9%, MELI -3.7%, EGLE -2.4%, TSO -1.8% (also downgraded to Underperform at BofA/Merrill), DIOD -1.5%, DTV -1.4%... Other news: LYG -13.2% (continues to fund itself well, CFO says; co still expects pretax loss for year - DJ), LCC -7.8% (concurrent offerings of 15.2 mln shares of common stock and $75 mln in convertible notes for total gross proceeds of $150 mln), DSX -4.7% (announces pricing of 6 mln shares of common stock offering at a price of $16.85), SWHC -3.7% (announces it has priced its offering of 5.5 mln common shares at $6.25/share), SPG -3.4% (announces it intends to conduct, subject to market and other conditions, an offering of 14,000,000 shares of common stock). -

Tulemuste tabel nüüdseks eelturul numbrid teatanud ettevõtetega uuendatud. Link tabelile on siin.

-

Otsustasime enne stress-testi tulemusi sulgeda TBT. Lähemalt saab lugeda Pro alt, aga tänastelt tasemetelt ei tundunud riski-tulu suhe lühiajaliselt enam kõige parem.

-

USAl muutub enda defitsiiti finantseerimine odava rahaga üha keerulisemaks ning aja jooksul mõjub see majanduse taastumise kontekstis pidurina.

30-yr goes off at a higher yield 4.288% against expected 4.190% -

Olgu siis öeldud, et stress-testi tulemused tehakse teatavaks meie aja järgi südaöösel, seega turgude reaktsioon jääb homsesse. Kuulaks huviga veel viimaseid vandenõu- ja muidu teooriaid.

Igal juhul on selline tunne nagu mõnel investeerimishuvilisel Fedi intressimäärade otsust oodates - põnevus on suur, aga midagi teha ei oska. :) Aga ega polegi osata... -

Peale nii pikka jahumist ei ole sellest no-stress-testist küll midagi huvitavat oodata.

My best guess: yawn.

Tuleb igav vaikne suunata loksumine homme. -

Oodata on ikka huvitav, tulemused ise on igavad. :)

Mul kipub arvamus pigem Kassi poole, kes viitas finantssektori liiga tugevale rallile ning on mõnda nime pigem shortimas. -

Stresstest oli midagi sellist nädal aega sampus tort ja küünlad(kõik tõusis ja mitte väheisegi prügi rallis). Kas pohmell või juuakse homme edasi? Pakun et reaalsus on ikka pohmell ja tugev miinuspäev homme. Eriti närvi ajab see et avalikustatakse keskööl jne aga nädal aega graafikud ja infokilde lekib või lekitatakse.

-

My guess - sell the news... nagu juba ütlesin. Ja soovitaks mu hommikust lõbusat videot vaadata - juba praegu kipuvad mõned turul 'toolita' jääma. Traditsioonilist päevalõpu tugevust pole tulnud.

-

Sell the news tundub liiga läbinähtav..

-

Tulemuste tabel õhtuste teatajate ja seniste aktsia reageeringutega uuendatud. Võrreldes kahe varasema nädalaga on koos kiiresti tõusnud aktsiaturuga kerkinud ka ootused ning aktsia reageeringute tulpa jõuab üha rohkem punast värvi.

-

Briefing:

Ten of 19 banks in stress tests must raise net new capital of $74.6 bln, u.s. regulators say - Reuters$455 BLN OF LOSSES FROM ACCRUAL LOAN PORTFOLIOS, MAINLY HOME MORTGAGE, CONSUMER LOANS. BANKS FACE 2-YEAR CUMULATIVE LOSSES OF 9.1 PCT OF TOTAL LOANS UNDER WORST SCENARIO.

Federal Reserve, OCC, and FDIC release results of the Supervisory Capital Assessment Program The results of a comprehensive, forward-looking assessment of the financial conditions of the nation's 19 largest bank holding companies (BHCs) by the federal bank supervisory agencies were released on Thursday. The exercise--conducted by the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation--was conducted so that supervisors could determine the capital buffers sufficient for the 19 BHCs to withstand losses and sustain lending--even if the economic downturn is more severe than is currently anticipated. In a detailed summary of the results of the Supervisory Capital Assessment Program (SCAP), the supervisors identified the potential losses, resources available to absorb losses, and resulting capital buffer needed for the 19 participating BHCs. The SCAP is a complement to the Treasury's Capital Assistance Program (CAP), which makes capital available to financial institutions as a bridge to private capital in the future. Together, these programs play a critical role in ensuring that the U.S. banking sector will be in a position of strength.

REGULATORS SEE TRADING, SECURITIES LOSSES AT $135 BLN IN 2009-2010 - ReutersBANKS NEEDED TO ADD $185 BLN TO CAPITAL BUFFERS AT END 2008 TO REACH TARGET. SOME BANKS SOLD ASSETS, RESTRUCTURED CAPITAL SINCE END '08, RAISING TIER 1 COMMON CAPITAL. TEN OF 19 FIRMS TOO STRONGLY TILTED TOWARD CAPITAL OTHER THAN COMMON EQUITY

17:01 Ten of 19 banks in stress tests must raise net new capital of $74.6 bln, u.s. regulators say - Reuters$455 BLN OF LOSSES FROM ACCRUAL LOAN PORTFOLIOS, MAINLY HOME MORTGAGE, CONSUMER LOANS. BANKS FACE 2-YEAR CUMULATIVE LOSSES OF 9.1 PCT OF TOTAL LOANS UNDER WORST SCENARIO -

Link Föderaalreservi tervikdokumendile on siin.

-

Lisakapitali vajadused suuruses $74.6 miljardit jagunevad siis niimoodi:

Bank of America $33.9 mld

Wells Fargo $13.7 mld

GMAC $11.5 mld

Citigroup $5.5 mld

Regions $2.5 mld

Suntrust $2.2 mld

KeyCorp $1.8 mld

Morgan Stanley $1.8 mld

Fifth Third $1.1 mld

PNC $0.6 mld

AmEx $0.0 mld

BB&T $0.0 mld

BNYM $0.0 mld

Capital One $0.0 mld

Goldman Sachs $0.0 mld

JPMC $0.0 mld

MetLife $0.0 mld

State Street $0.0 mld

USB $0.0 mld -

Wells Fargo plaanib juba $6 miljardilist aktsiate lisaemissiooni, Morgan Stanley müüb aktsiaid $2 miljardi eest ja võlga $3 miljardi eest.