Börsipäev 3. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Globaalselt on taas häid uudiseid tulemas. Austraalia majandus tõusis esimeses kvartalis 0.4%, ehkki analüütikud olid prognoosinud langust. Hiina ja Indiaga kuulutakse nende väheste majanduste hulka, mis esimeses kvartalis suutsid kasvu näidata. Aktsiad lõpetasid plussis ning Austraalia dollar tõusis kaheksa kuu kõrgeiamale tasemele.

-

Austraalia ASX 200 indeksi liikumine viimasel aastal:

USA börsil on võimalik lisaks paljudele teiste riikide ETFidele kaubelda ka Austraalia omaga, mille sümbol on EWA.

-

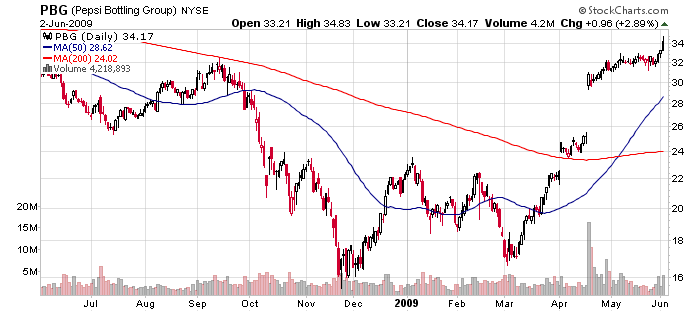

Pepsi Bottling Group (PBG) tõstis eile enne turu avanemist oma Q2 ja FY09 kasumiprognoose. Tegemist on juba teise kasumiootuse tõstmisega viimase kuue nädala jooksul:

Co issues in-line guidance for Q2 (Jun), sees EPS of $0.70-0.74 vs. $0.70, a $0.05 increase from previous range. First Call consensus. Co issues upside guidance for FY09 (Dec), sees EPS of $2.30-2.34 vs. $2.25 consensus, up $0.10 from previous range. PBG also its full-year operating free cash flow guidance by $25 mln to $525 mln. Among the key drivers of the revised outlook are: improved carbonated soft drink performance in the U.S.; decreased volatility in foreign currencies; and continued commodity cost deflation.

Siiski ei tasu põhjust selliseks optimismiks kaugelt otsida. Tõenäoliselt on antud sammu motiiviks survestada Pepsico (PEP) juhtkonda kõrgema ülevõtupakkumise tegemiseks. Pärast prognooside kergitamist avaldas UBS note’i, milles näevad ühinemises tekkivad sünergiad rohkem kui $400 mln ulatuses ja uut pakkumist suurusjärgus $39:

UBS raises their tgt for PBG to $39 from $33 as the firm ests that total cost savings fom the merger with PEP will exceed $400 mln, which will ultimately lead to PEP paying roughly $39 for PBG shares based on these cost savings ests and the topline opportunity the deal provides. Additionally, the firm believes that PBG's strong 1Q results and '09 outlook further increases the likelihood that PEP will need to raise their offer price for PBG from $29.50. The firm believes this increase in price justified as the deal costs savings are likely multiples above PEP's $200 mln estimate, the current takeout bid assigns no premium to historical trading, and the firm's estimates that the deal is accretive well above the current offer.

Sarnase arvamusega oli Citigroup väljas juba 7. mail, kui nimetati Pepsico esialgset $29.5 suurust ülevõtupakkumist äärmiselt madalaks. Citi analüütikute stsenaariumi kohaselt teeb 90%-lise tõenäosusega Pepsico kõrgema pakkumise ja 10%-lise tõenäosusega loobub. Hinnasihtideks on erinevate stsenaariumite puhul vastavalt $38 ja $33 ehk tõenäosustega läbi kaaludes saadi hinnasihiks $37.5.

Pärast eilset kasumiprognooside tõstmist Citi oma eelpool kirjeldatud arutluskäiku ei muuda, kuid nende kommentaaris on siiski välja toodud veel üks huvitav nüanss. Nimelt teates eile Pepsico, et nende investorsuhete juht Mike Nathenson viiakse oma praeguselt kohalt üle PBG ülevõtupakkumisega tegelevasse meeskonda. See samm lubab oletada, et Pepsico’l on plaanis lähiajal tulla välja kõrgema pakkumisega, sest vastasel korral ei loobuks Nathenson oma praegusest positsioonist.

On Pepsi (PEP.N; US$53.13; 1L): For investors who still question PEP's commitment to do the deal at a higher price, we note PEP's announcement this morning that the head of Inv. Relations, Mike Nathenson, is transitioning from IR "to play a key role in partnering with [CFO Richard Goodman] and [PepsiCo's] senior management team in the proposed acquisition of our two anchor bottlers,PBG and PAS."

We strongly believe Mike Nathenson would not be leaving PepsiCo IR for a role in a deal that PepsiCo was not committed to closing.

-

Kiire ülevaade täna USA börsidel toimuvast:

- Kell 15:15 avaldab ADP Employment Change raporti. Aprillis kasvas töötus 491,000 võrra ning konsensus prognoosib, et maikuus kasvas ADP töötus 525,000 inimese võrra. Analüütikud hindavad raporti mõju turgudele suureks.

- Kell 17:00 avaldatab The Commence Department tööstustellimuste raporti. Ökonomistid prognoosivad, et aprillikuus kasvasid tellimused 0.9% (märtis langesid tellimused 0.9%). Mõju turgudele on väike.

- Kell 17:00 teatatakse ISM Services indeksi näidust. Konsensus prognoosib näiduks 45.0 punkti. Mõju turgudele võiks hinnata keskmiseks.

- Kell 17:30 avaldab Department of Energy Crude Inventories ehk toornafta varusid kajastava raporti. Mõju aktsiaturgudele hinnatakse suureks.

-

...ja kell 17:00 annab pressikonverentsi Föderaalreservi esimees Ben Bernanke.

-

CSFB:

Global Equity Strategy A. Garthwaite

Downgrade Equity to Market Weight from Overweight 44 20 7883 6477

• We leave our year-end target unchanged at 920 on the S&P 500 but take our equity weightings down to benchmark from

overweight (at the time of writing the S&P 500 is close to our overshoot range of 950-1,000). Our reasons for downgrading

are:

• The recent rise in bond yields has undermined the valuation of equities. The equity risk premium (using trend reported EPS of

US$61 on the S&P 500) is now 4.7%. While this is 'cheap' versus the long-run average ERP of 3.6%, we continue to find that

the 'warranted' ERP is determined by the credit spreads and ISM. Even assuming that the ISM picks up to 52 (consistent with

nearly 2.2% GDP growth), the 'warranted' ERP would be 5.3%. On trend earnings, the S&P 500, at 15.5x, is trading in line

with its long-run average, as is market cap to GDP and Tobin's Q. Although earnings momentum looks set to turn positive for

the first time since Sept 2007, we already price markets off trend earnings.

• Implied corporate default rates: (for high yield) are now close to fair value at 40% for the next five years (and compares with a

peak default rate of 36% in 2003). CDX-high yield and S&P 500 generally move together.

• Some of the tactical indicators are now becoming more worrisome: net corporate equity issuance has surged to 2% of market

cap-an all-time high; equity sentiment and equity risk appetite are now back to neutral levels (with regional equity risk appetite

now in 'euphoria' zone); insider buying is abnormally low; and market breadth is deteriorating (a warning signal).

• We struggle to buy high beta: US cyclicals trade on a 2009E P/E of c19x, even if we assume average margins. Bear market

rallies can be 50% (1929 and Japan), but this rally has already been 47% globally and 40% in the US.

• We remain concerned about the economic backdrop. We suspect that the inventory build will be completed by mid-Q3 and

expect lead indicators to peak then. US core retail sales (ex food, gasoline and energy) are already up 6.7% quarterly

annualised (from -13% six months ago). The best lead indicators of US activity are consistent with US GDP growth of only

1.3%. ISM tends to double-dip five to eight months into a conventional upturn. We still fear there is US$7tr of excess leverage

in the G4 countries and that the monetary and fiscal stimulus seen only offsets 60% of this. Added to this, we believe that US

trend GDP is lower (2.25-2.5%) and the scope for policy error is large. The recent rise in bond yields is worrisome-on our

analysis, each 1% on ten-year yields takes 0.5% off GDP growth (and requires a 10% fall in house prices to leave affordability

unchanged). We believe we are in an upward sloping W-shaped recovery.

• Conclusion: We believe the downside and upside risks to equities are now quite symmetrical and believe strongly that the

lows have been seen. The upside risk to equities is further aggressive QE. We believe we are in a range trading market like

the 1970s.

• Bonds …value appearing: We believe the Fed will be more willing to risk a dollar crisis than a funding crisis. We believe

inflation, particularly in Continental Europe, will surprise on the downside. -

ADP Employment Change mai number tuli 532 000 vs ootus 520 000 - 525 000 (erinevad konsensused) ja aprilli 491 000 revideeriti 545 000 peale ... turg reageerib tõusuga

-

No ikka ju. Rohkem töötuid --> vähem töötajaid --> ettevõtted peavad töötajatele vähem palka maksma --> kõrgemad marginaalid --> kõrgem kasum. Kõige parem oleks nii, kui kõik töötuks jääksid.

-

USA börsid on täna avanemas miinuspoolele. S&P500 -0.90%, Nasdaq -0.7% ning nafta -1.1% @ $67.8.

Saksamaa DAX -0.79%

Prantsusmaa CAC 40 -1.25%

Inglismaa FTSE 100 -2.02%

Hispaania IBEX 35 -1.16%

Venemaa MICEX -3.87%

Poola WIG +0.30%

Aasia turud:

Jaapani Nikkei 225 +0.38%

Hong Kongi Hang Seng +1.02%

Hiina Shanghai A (kodumaine) +2.00%

Hiina Shanghai B (välismaine) +1.26%

Lõuna-Korea Kosdaq +0.48%

Tai Set 50 +1.54%

India Sensex 30 -0.03%

-

Take Whatever the Market Is Giving You

By Rev Shark

RealMoney.com Contributor

6/3/2009 8:29 AM EDT

The superior person can hold two contradictory thoughts simultaneously and still continue to function. You need a long-term vision combined with short-term focus.

-- Brian Tracy

I keep reading stories about how wonderful things are going for the economy -- home and car sales increasing, consumer sentiment jumping, inflation well under control and green shoots of recovery everywhere. Given how the stock market has been acting, a lot of folks are embracing these optimistic views.

The debate between those (like Jim Cramer) who think things really are rapidly improving and aren't fully reflected in the market. and those (like Doug Kass) who think the market has gotten ahead of itself is going to be the primary theme we read about for quite some time. No matter what side of the argument you agree with, the key thing is that you not let economic arguments blind you to the way that stocks are actually performing.

I have great concerns about the eventual repercussions of all the government involvement in the economy. Handing out money is something the government does well, but paying the bill down the road is going to be the big challenge. Although there are already growing fears of inflation and concerns about government intrusion into private business, the market isn't reflecting those worries at all. In fact, the market seems to be indicating that things are going to work out very well.

The easy thing to do is to be dogmatic and adopt either the extremely rosy view or the extremely pessimistic view. Most everyone has a strong opinion and is leaning one way or the other.

The most practical approach for investors is let the market be your guide to the economy. Right now the market is acting like the economy is going to be just fine. While we are a bit toppy in the short term, nothing in the technical action indicates anything other than blue skies and apple pies ahead of us. We have strong speculative action, a growing list of stocks hitting new highs, rising commodity prices and stocks making parabolic moves. You might not believe what this is indicating about the economy, but trying to fight it isn't going to make you much money in the near term.

At some point the indices are going to struggle and even lose some underlying support. At that point we can start worrying more about the validity of the views of the economic pessimists. I believe the market won't make it through the summer unscathed by a pretty severe pullback, but that is not today's business. Today's business is navigating a market that is still acting quite well.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: APSG +11.8%, TSRA +11.7% (also enters into technology license agreement with Motorola), BOBE +9.3%, FE +6.0%, JOYG +1.0%... M&A news: DDUP +3.1% (NetApp raises DDUP acquisition offer to $30/share in cash and stock)... Other news: TIVO +46.1% (confirms Court rejected EchoStar's "attempted workaround claim" regarding the TiVo patent), PPHM +25.0% (highlights "promising early data" from its three Phase II bavituximab cancer trials), SAY +17.8% (SEBI OKs Tech Mahindra open offer - WSJ), SGY +11.9% (announces deepwater discovery on Pyrenees Prospect), CTIC +11.6% (announces that patients with cancer of the lower esophagus had evidence of a high pathological complete response rate when given OPAXIO), IPAS +11.4% (to return up to $40 mln of capital to stockholders), PMI +6.6% (The PMI Group ratings raised by Standard & Poor's), CHLN +6.1% (still checking), HEB +4.4% (continued momentum from yesterday's 25%+surge higher)... Analyst comments: AAI +7.0% (upgraded to Buy from Underperform at BofA/Merrill), PLT +3.5% (upgraded to Overweight from Neutral at JP Morgan), EBAY +1.3% (upgraded to Buy at Collins Stewart).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: VLO -11.8% (also announces 40 mln common share offering; downgraded to Underperform from Mkt Perform at BMO Capital), AET -7.0% (downgraded to Underperform at Credit Suisse and downgraded to Market Perform from Outperform at Wachovia), PAY -6.7%, BCSI -3.3%... Select financial related names trading lower: RBS -5.9%, BCS -5.6%, HBC -4.2%, UBS -3.8%, LYG -3.8%, MET -1.7%, C -1.6%... Select metals/mining names showing weakness: AAUK -4.0%, GFI -4.0%, BBL -3.4%, MT -3.4%, RTP -2.6%, GOLD -2.1%, GG -1.9%, KGC -1.9% (downgraded to Neutral from Overweight at JP Morgan), BHP -1.7%, AUY -1.5%... Select managed healthcare names trading lower in sympathy with AET guidance: CI -4.1%, WLP -4.0%, HUM -4.0%, UNH -3.9%, CAH -1.5% (downgraded to Neutral at Baird)... Select refiners and oil/gas related names showing weakness partially attributed to VLO guidance: HOC -7.2%, TSO -5.1%, SUN -3.3%, REP -2.9%, RDS.A -2.9%, WNR -2.7%, CHK -2.5%, TOT -1.9%, MRO -1.5%, E -1.5%, BP -1.4%, CVX -1.1%... Other news: FFBC -10.2% (trading ex-dividend), STLD -8.0% (announces proposed offerings of 27 mln shares common stock and $150 mln aggregate amount of convertible senior notes), NGG -6.7% (trading ex-dividend), JBLU -6.6% (announces proposed offerings of 20 mln shares of common stock and $150 mln of convertible debentures), DISH -6.3% (confirms court's decision finding co in contempt), ACGY -6.2% (still checking), PRU -4.1% (prices 32,051,283 common share offering at $39/share), HBAN -3.6% (announces a $300 mln common equity public offering and suspension of current discretionary equity issuance program), LAZ -3.3% (Certain Lazard Ltd shareholders sell common four mln shares of stock in a secondary offering), BKD -1.8% (prices 13,953,489 follow-on common share offering at $10.75/share)... Analyst comments: AMSC -4.1% (downgraded to Underweight at Morgan Stanley), CUB -3.1% (downgraded to Hold at BB&T), NG -2.1% (downgraded to Underperform at RBC Capital), VMW -1.9% (initiated with a Sell at Ladenburg), BRCD -1.6% (Goldman Sachs removes from Americas Conviction Buy list; maintains Buy - Reuters). -

Volckeri pessimistlikud kommentaarid USA majanduse kohta tulid juba eile õhtul, kuid video väärib vaatamist kahtlemata ka praegu. Link siin.

-

Palm (PALM) kaupleb täna rohkem kui 6% võrra miinuses. Ühest küljest on tegu igati loomuliku korrektsiooniga, sest aktsia on leidnud väga tugevat ostuhuvi enne Pre lansseerimist 6. juunil, tõustes viimase nelja kauplemispäevaga $2.5 võrra. Samas võib Palm'i aktsiat mõjutada ka tänases Business Week'is ilmunud äärmiselt negatiivne artikkel, mille kohaselt on Pre tõenäoliselt läbikukkumine. BW kirjatükk on nii tugeva sõnastusega, et Eric Savitz nimetab oma blogis seda hatchet job'iks...