Börsipäev 16. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Täna ei ole USA aktsiaturud huvitavad üksnes tehnilise poole pealt, kuna makrouudised võivad nii tõusu kui ka languse nurjata.

14:45 - ICSC-Goldman Store Sales

15:30 - Housing Starts. Konsensus prognoosib, et maikuus laoti vundament 485,000-le ehitisele USAs. Aprillis tehti algust 458,000 ehitusobjektiga. Raporti mõju on turgudele suur.

15:30 - Bulding Permits. Konsensuse hinnangul väljastati maikuus 508,000 ehitusluba. Aprillis väljastati 498,000 ehitusluba. Mõju on turgudele samuti suur.

15:30 - Producer Price Index. Konsensus prognooosib maikuu tootjahinnaindeksi 0.6%-list kasvu. Aprillis kasvas indeks 0.3%. Ka selle raporti mõju on turgudele suur.

15:30 - Core PPI. Maikuu "core" ehk siis PPI v.a. toit ja energia. Maikuu "core" PPI kasvuks prognoosib konsensus 0.1%. Aprillis kasvas "core" PPI 0.1%. Mõju on turgudele samuti suur.

15:55 - Redbook

16:15 - Industrial Production ehk maikuu tööstustoodang. Konsensus prognoosib, et maikuus langes tööstustoodang 1.0%. Aprillis vähenes toodang aga 0.5%. Mõju turgude suur.

16:15 - Capacity Utilization ehk tootmisvõimekuse rakendatus. Konsensus prognoosib, et maikuus oli tulemus 68.4%. Aprillis oli tootmisvõimekus rakendatud aga 69.1% ulatuses. Mõju turgudele suur.

20:00 - 4-nädalase võlakirja oksjon

-

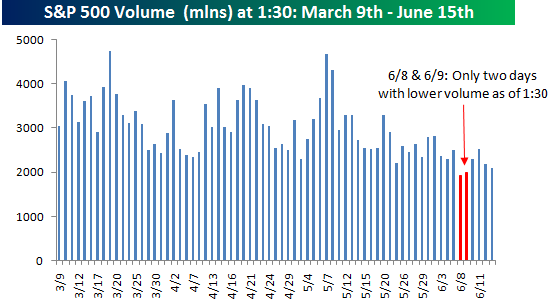

Oodatust kehvem makro ning nafta ja metallide odavnemine on muutnud investoreid ettevaatlikumaks võimalike green shootide jätkusuutlikkuses, mistõttu sulgus SP500 indeks eile -2.4% madalamal ja täna võetid Aasia turgudel sellest šnitti (Nikkei 225 sulgus -2.86% punases, hoolimata sellest, et Jaapani keskpank oma majanduslikku hinnangut tõstis). Kuid, nagu allolevalt Bespoke'i graafikult võib näha, on müügisurvet siiski tekitamaks tavapärasest õhukesemad käibed.

Halvad uudised aktsiaturgudel ja majanduses mõjuvad positiivselt jälle võlakirjadele. USA valitsuse võlakirjade hinnad tõusid iele neljandat päeva järjest - pikim tõususeeria viimase viie kuu jooksul. 10-aastase võlakirja tulususe langus aitab tuua madalamale ka hüpoteeklaenude intresse, mille kiire tõus viimastel kuudel võis üsna paljudele laenusoovijatele valmistada ebameeldiva üllatuse.

USA valitsuse 10a võlakirja tulusus

Euroopa turud on avanud esmaspäevaste sulgumistasemete juurest ning ning nagu Kristjan tõi välja, aitavad makroandmed paika panna, kas riskikartlikkus jätakb turgude juhtimist. Enne USA makrot võiks Euroopas täna teatud tähelepanu pälvida ZEW majanduskonjuktuuri indikaator, mis avaldakse kell 12.00.

-

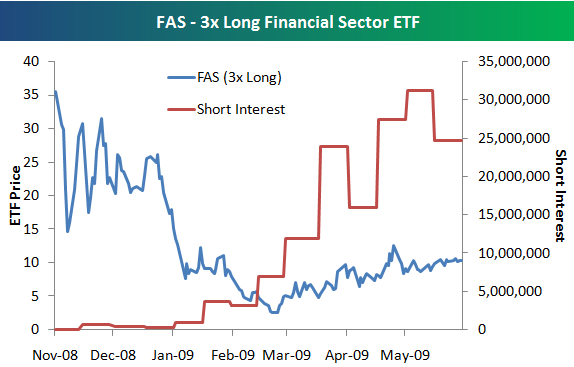

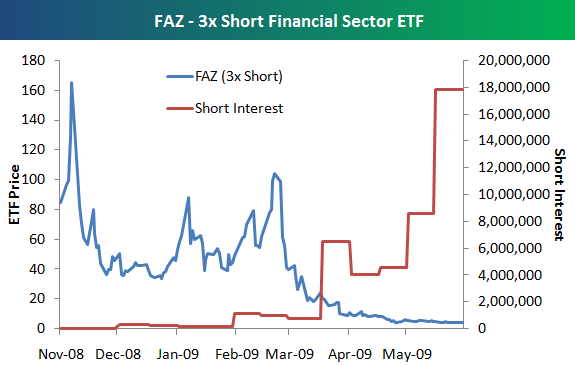

Börsipäeva foorumites ning Madise kirjutatud artiklis on võimendusega ETF-de kurioossus korduvalt teemaks tulnud.Veelkord meeldetuletuseks, miks sellised tooteid ei sobi pikaajalisele investorile. Kui kolmekordse võimendusega ETF-de järgitav finantssektori indeks ise on alates novembri keskpaigast 7% tõusnud siis 3X finants long (FAS) on sama perioodi jooksul näitamas -71%-list kaotust ja 3X finants short (FAZ) -95% kaotust. Graafikutelt on ühtlasi näha, et üha rohkem investoreid üritavad raha teenida lühikeseks müügiga. Üks üsna hea inglise keelne webinari seletab lahti põhjalikumalt, milline võimendusega börsil kaubeldavate fondide tegelik lugu.

Allikas: Bespoke

-

Ühel heal päeval tuleb see heavy short interest kõigile osalejatele üllatusena valusalt kätte. just a reminder.

-

Vaataks ka tehniliselt, mis viimased päevad kaasa on toonud.

Alloleval graafik on ajaperioodiga YTD ning indeksiks on SPX ehk S&P 500.

-

Mis arvad rehatrader- kas siit lühikeseks või pikaks :)

-

ZEW indikaator, mis peegeldab järgmise 6 kuu oodatava Saksamaa majandusarengu suhtes pessimistlikult ja optimistlikult meelestatud analüütikute suhet, kerkis juunis 44.8-ni versus oodatud 35 punkti. Konsesus ootas üsna marginaalset paranemist.

-

Mul on FAZ positsioon soetatud. Mängin alati 38,2 ja 61,8 tasemetel põrkele. ESM9 38,2 tase on 958 ja sealt ka allapoole pöörati. Nüüd võiks ES-futuur üritada murda tagasi koridori, ebaõnnestuda ja siis vabalt allapoole tulla. See oleks nagu õpikus :)

-

Veel üks võimalus....

-

USA eramuturult oodatust veidi paremad näitajad.

May Housing Starts 532K vs 485K consensus; prior revised to 454K from 458K

May Building Permits 518K vs 508K consensus

USA börsiindeksid on hommikust saati näidanud vaikset kosumist ning preaguseks hetkeks kauplevad futuurid 0.4-0.5% kõrgemal

-

Keep Your Focus Tight

By Rev Shark

RealMoney.com Contributor

6/16/2009 8:17 AM EDT

It is wise to keep in mind that neither success nor failure is ever final.

-- Roger Babson

Every since the market started to bounce back in early March, the question has been, "How much higher can we go?" The answer has been, "Much higher than just about anyone suspected." We have continued to chug along steadily, and every pullback along the way has been a good buying opportunity. The only problem has been that every pullback has been so short and shallow that the dip-buyers have to move so fast that they end up just chasing the market higher.

Yesterday we experienced another one of these pullbacks within the uptrend. Trading was downright dismal, with lousy breadth and nowhere to hide. Most of the momentum plays dried up. Small-cap stocks had no clear pockets of hot action and the stronger dollar put pressure on energy, metals and commodity stocks.

Overall it was pretty unsurprising day of correction. The most notable thing about it was that the bulls were unable to manage their typical late-day buying spike, which had been routine since this rally began. It was also a bit troubling that even with the rather substantial point loss, the mood seemed rather sanguine. This was not a panicky selloff with folks rushing to escape out of fear they would be caught in the next major leg down.

And that brings us to the question of whether this is just a continuation of the recent pattern of short and shallow pullbacks or whether we're finally seeing a more profound change in market character. So far the technical picture of the market doesn't suggest anything too worrisome at this point. We gave back most of the gains for the month but we are at the bottom of the recent trading range and have plenty of support from the action in May.

The biggest negative for the market lately is that it hasn't had a lot of upside traction. There has been some very strong trading in various small-cap sectors like China and biotechnology, but the major indices have been unable to hold breakouts and are churning as they look for some new catalysts.

The indices have done nothing wrong and still appear to be technically healthy, but they just don't have much juice. What is going to be the key to the market is the flow of "hot money" from one sector to another. Lately we have consistently seen traders aggressively jump on new themes. They want to buy and are happy to join others when they see strength. It has worked, and that success helps to shore up confidence for the broader market.

The biggest danger for this market is that momentum buyers will lose confidence. We have already seen some of the bigger-cap technology names like Google (GOOG) , Apple (AAPL) , Shanda Interactive (SNDA) and others pull back, but traders are still out there looking for action and appear ready and anxious to jump back in when things perk up.

So we have major indices that don't have a lot of life but haven't done anything wrong, and an undercurrent of momentum trading that paused yesterday but hasn't shown any signs of collapsing yet. That means we need to focus on what sectors are working and on our stock-picking because the bigger picture is a bit muddled.

We have a little bounce setting up to start the day. The dollar is back down and that is boosting oil and commodities. Otherwise there isn't much news out there.

----------------------------------------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: LZB +34.6%, TEL +10.9% (also upgraded to Hold at Collins Stewart), FDS +3.1% (light volume), CASY +1.8%... Select financial names ticking higher: RBS +4.2%, LYG +4.0%, BCS +3.5%, HBAN +2.9%, AIB +4.7%, DB +1.9%, CS +1.9%, ABB +1.6%, STD +1.4%, HBC +1.1%... Select European drug names showing strength: SNY +2.8%, GSK +2.6%, SHPGY +1.5%, NVS +1.3%, AZN +1.2%... Select oil/gas names trading higher: WFT +3.9%, STO +3.3%, PBR +2.0%, TOT +1.8%, ... Select metals/mining names showing strength: HL +3.8%, MT +2.7%, SLW +2.7%, ABX +2.4%, AUY +2.2%, GG +1.8%, AEM +1.6%, BHP +1.4%, AAUK +1.2%... Other news: EMKR +21.1% (awarded solar panel manufacturing contract for NASA's Global Precipitation Measurement Mission), ALVR +15.6% (trading higher with Bloomberg reporting that the co won $100 mln contract), AIM +10.6% (continued momentum from yesterday's 70%+ jump), SATC +8.7% (selected for "largest solar energy rooftop installation" in the Southeast United States), JAZZ +7.5% (continued momentum from yesterday's 60%+surge higher), CDII +7.1% (receives several basic materials sales contracts valued at $30.5 mln), SOAP +7.0% (announces approval of plan of liquidation and dissolution by Board of Directors and wind down of operations; ests stockholders to receive $4-4.50/share ), SAY +4.7% (still checking for anything specific), BT +4.1% (traded higher overseas following analyst upgrade yesterday afternoon), WEN +3.1% (signs major development agreement for the Middle East and North Africa), CRM +1.2% (Cramer makes positive comments on MadMoney), CELG +1.1% (announces positive top line data from randomized controlled phase II study of apremilast in psoriatic arthritis; also initiated with a Buy at Morgan Joseph)... Analyst comments: SMOD +10.0% (upgraded to Buy at Needham), FRPT +5.2% (upgraded to Buy at Collins Stewart), SINA +3.6% (seeing early strength; hearing added to Buy List at tier 1 firm), BRCD +1.6% (initiated with a Buy at Canaccord).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: APWR -10.3% , CPST -7.0% , SFD -3.4% (light volume), BBY -3.3%... Other news: BMR -17.8% (declared Q2 common stock dividend of $0.11/share, down from prior dividend of $0.335/share), GENZ -10.8% (temporarily interrupts production at Allston plant), HAR -7.8% (files for mixed securities offering and announces common stock offering of 9 mln shares), NBG -7.7% (to propose 1.25 bln euro rights issue - Reuters.com), BRKR -7.4% (files for 35 mln share common stock offering), INSM -7.0% (CEO resigns due to health concerns ), MMR -6.9% (commences a public offering of ~11 mln shares of common stock ), AINV -5.8% (trading ex dividend), PCAR -5.0% (comments on recent trends; sees Q2 industry truck production in North America and Europe 5-10% lower than Q1), BMRN -4.7% (down in sympathy with GENZ), CHU -4.5% (still checking), PCX -4.1% (announces it plans to offer approx 12.0 mln shares of its common stock in a registered public offering), GWR -4.1% (announces intent to discontinue operations of Huron Central Railway; expects to record Q2 charges of $0.15/share and announces public offering of 4 mln shares of its Class A common stocK), SPPI -4.1% (to raise $10 million from institutional investors at $5.83 per share), YGE -2.4% (announced that it has signed an off-grid PV system sales agreement with the Shanxi subsidiary of China Mobile)... Analyst comments: T -1.1% (downgraded to Equal Weight at Barclays). -

May Core PPI M/M -0.1% vs +0.1% consensus, prior +0.1%

May PPI M/M +0.2% vs +0.6% consensus, prior +0.3%

May Core PPI Y/Y +3.0% vs +3.2% consensus, prior +3.4%

May PPI Y/Y -5.0% vs -4.4% consensus, prior -3.7% -

Store Sales - W/W change previous 0.2% actual -0.6%

Store Sales - Y/Y previous -0.8% actual -1.5% -

Redbook - Store Sales Y/Y change previous -4.4%, actual -4.8%

-

USA eelturgudel oli seis järgmine: SPY +0.31%, QQQQ +0.45% ja IWM +0.80%.

Mujal maailmas olid liikumised järgmised:

Saksamaa DAX +0.70%

Prantsusmaa CAC 40 +0.76%

Inglismaa FTSE 100 +0.92%

Hispaania IBEX 35 +0.55%

Venemaa MICEX +2.63%

Poola WIG -0.07%

Aasia turud:

Jaapani Nikkei 225 -2.86%

Hong Kongi Hang Seng -1.80%

Hiina Shanghai A (kodumaine) -0.49%

Hiina Shanghai B (välismaine) +0.12%

Lõuna-Korea Kosdaq +0.25%

Tai Set 50 -2.66%

India Sensex 30 +0.55%

-

May Industrial Production -1.1% vs -1.0% consensus, prior revised to -0.7% from -0.5%;

Capacity Utilization 68.3% vs 68.4% consensus, prior 69.0% -

Fed's Warsh says US jobless rate to stay high for longer than usual

Fed's Warsh says global econ may be "mired" in weak growth for many years

Fed's Warsh offers downbeat outlook for US, global -

no tänase päeva kohta võib siis öelda ... somebody call 911...

-

Kevin M. Warsh, 38

"Harvard Law graduate, is not an economist by training."

"economic adviser in the George W. Bush White House."

"He’s married to Jane Lauder, his Stanford classmate and the daughter of Ronald Lauder, the cosmetics billionaire, Republican donor and former ambassador to Austria."