Börsipäev 7. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

Täna on üks väheseid päevi, mil USA turud saavad kaubelda ilma, et makromajandusraportite avaldamised kaarte segaksid. USA indeksite futuurid hetkel väikeses, ca 0.3%lises miinuses.

-

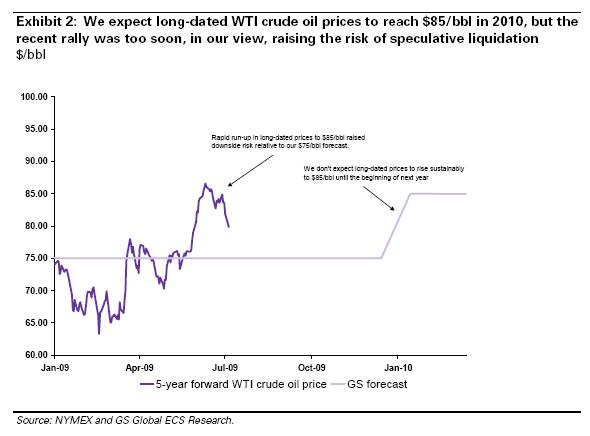

Merrill Lynch kergitas täna naftahinna prognoosi: "Merrill Lynch increased its view in 2009 and 2010 oil prices, citing a weaker dollar, a significant improvement in global liquidity conditiosn and a slightly tighter-than-expected global oil market balance. It expects WTI crude to average $58.50 a barrel in 2009, up from $52, and WTI to average $75 a barrel in 2010, up from $62. Oil prices may reach $82 by the fourth quarter of 2010 due to limited growth in non-OPEC supply, shrinking of OPEC spare capacity, a robust emerging market demand outlook and more dollars in circulation."

-

Euroopa turgudel levib uudis, et Hispaania telekom Telefonica SA (+0.07%) allkirjastas Palmiga (PALM) lepingu, mille kohaselt saab telekomist uue nutitelefoni Palm Pre ainumüüja Euroopas. Algul paisatakse Pre turule Hispaanias, siis Suurbritannias, Iirimaal ning viimaks ka Saksamaal.

-

Mismõttes viimaks? Euroopa ei ole ju ainult ES, UK, IE & DE!

-

"Viimaks" alla mõtlesin seda, et neljast ülalpool nimetatud riigist läheb Pre müüki viimasena just Saksamaal (vähemalt nii väidavad analüütikud). Teiste Euroopa riikide kohta infot pole!

-

Peale viimaste päevade kukkumist kaupleb Vital Images (VTAL) taas rahal. Bilansis on aktsia kohta raha ligi $10, aktsia eilne sulgemishind oli $10.25. Ehkki tulemused pole halvemaks läinud, ei piisa sellest investorites huvi tekitamiseks. Oodatakse kvartalinumbrite paranemist, mida aga haiglate kulude kokkuhoiu programmi taustal on keeruline loota. Kui varem oli meie teesiks lihtsalt hea positsioneerimine uue tõusutsükli lävel, siis praegu usun üha enam, et ettevõte on mingil hetkel võimeline kõvasti üllatama. Kui aktsia kaupleb cashil, on ootused äärmiselt madalal. Samas on tähelepanuta jäänud viimased lepingud edasimüüjatega ning Vitali aeglane, kuid kindel globaalne laienemine. Aktsias tasub siiski edasi istuda, sest haiglate kulude taastudes tõuseb aktsia väga kiiresti. Tänase aktsia hinna eest saab osta raha, tõusupotentsiaal antakse tasuta kaasa.

Vital on täna ka ühe soovituse tõstmise saanud:

Thomas Weisel upgrades Vital Images (VTAL 10.25) to Overweight from Market Weight and raises their tgt to $14 from $12, as they believe the new ViTAL enterprise product offers significant functionality improvements and is also offered in a more cost-effective package. They now believe this product could be a new catalyst for the company. As hospital purchasing trends eventually improve, VTAL could significantly benefit. Also, valuation levels are very attractive given the co's $10 in cash per share.

-

Briefing vahendab Fox Businessit, kes väidab, et Obama, ei ole välistanud vajadusel veel ühe majanduse abipaketi vastuvõtmise. Olukorras, kus riigi eelarve puudujääk on ca 15% SKPst, makes me say hmm..., aga eks Obama tea isegi, et (dollari) situatsioon on delikaatne ning seetõttu sõnastus ka suhteliselt konservatiivne.

Obama says second stimulus package a possibility, according to Fox Business. President Barack Obama said in an interview that a second stimulus package is a possibility, Fox Business Network reported. Asked about the possibility of a second stimulus in an interview in Moscow, Obama said he would take nothing off the table. However, Obama said stimulus spending is currently happening about as fast as possible, and he hoped that it would create more job growth later this year.

-

Euroopa turud:

Saksamaa DAX +0.34%

Prantsusmaa CAC 40 +0.28%

Inglismaa FTSE 100 +0.74%

Hispaania IBEX 35 +0.72%

Venemaa MICEX +2.07%

Poola WIG +0.62%Aasia turud:

Jaapani Nikkei 225 -0.34%

Hong Kongi Hang Seng -0.65%

Hiina Shanghai A (kodumaine) -1.13%

Hiina Shanghai B (välismaine) -1.05%

Lõuna-Korea Kosdaq +0.66%

Tai Set 50 N/A (börs suletud)

India Sensex 30 +0.90% -

At an Impasse

By Rev Shark

RealMoney.com Contributor

7/7/2009 8:13 AM EDT

There is nothing harder than the softness of indifference.

-- Juan Montalvo

A very mixed day on Monday has left the market in a confused state. While the Dow Jones Industrial Average and S&P 500 closed in positive territory, breadth was solidly negative and small-caps, energy and commodities saw some heavy selling pressure. The major indices did hold some key support areas at important moving averages and may have a bit more bounce in them, but we are seeing the first real correction in this market since the March lows.

Weak oil was the big drag on the market yesterday. Interestingly, the folks who always talk about strong oil being bullish because it indicates economic strength start to talk about how weak oil is bullish because it puts money in the hands of consumers. I'm not sure oil moves are particularly indicative of anything other than the current state of trading emotions. Folks in the oil industry tell me that the price movements don't seem to have any relationship to real supply and demand. Oil just makes for good trading, and it doesn't take much of a catalyst to send it one way or the other.

The most notable development in the market recently is that the pockets of momentum have pretty much dried up. We aren't seeing any great sector strength for the hot-money traders. There is some life in defensive groups like food and consumer staples, which have been led by stocks like General Mills (GIS) , Colgate (CL) , Kellogg (K) and Kraft (KFT) . Tobacco stocks, which also tend to attract buyers in difficult markets, are also active; names in that group include Lorillard (LO) , Altria (MO) , Philip Morris International (PM) and British American Tobacco (BTI) .

One of the more potentially promising leadership groups for the broad market is semiconductors. They have been showing some relative strength lately, and an upgrade of Intel (INTC) and a few others in the group today by Bank of America/Merrill may attract some attention. We will have to monitor that group to see if it can attract some positive sympathy.

Overall, the market is mostly mixed and not offering any great opportunities for aggressive trading or momentum investors. The opportunities are mostly for quick trades. I suspect that the bears are lurking about and patiently waiting for the chance to reload some shorts. They will give the bulls an opportunity to build a bit on yesterday's bounce off support, but the nature of this market lately has been that neither bulls nor bears have been able to gain a lot of traction.

The bulls were in control as the second quarter came to an end, but they were unable to push through key upside resistance around 930 on the S&P 500. The bears had a good day prior to the Fourth of July holiday, but the market found support almost exactly at the 200-day simple moving average of 886 and bounced nicely.

There is no really strong momentum either way, and we're not seeing much sector action either. That leaves us with a fairly short list of trading opportunities for now ... but earnings season is fast approaching and things are sure to heat up a bit. The only question will be in which direction.

We have a mildly positive start shaping up. Oil, gold and commodities are bouncing back a bit from yesterday's drubbing, and the wires are relatively quiet.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: ISCA +10.7% (light volume)... Select metals/mining names trading higher: MT +3.1%, IVN +3.1%, HMY +2.9%, SLW +2.5%, BBL +2.5%, AU +2.5%, BHP +1.6%, GFI +1.3%... Select European financial names showing strength: IRE +6.0%, AIB +5.4%, DB +3.0%, ING +2.5%... Other news: MMR +5.2% (announces positive drilling results at Blueberry Hill exploratory well), MYL +2.9% (receives FDA approval for generic version of prostate cancer treatment Casodex), SYT +2.8% (still checking for anything specific)... Analyst comments: LSI +8.1%, MRVL +5.3%, STLD +4.1%, APC +3.1%, INTC +2.7% and STO +1.6% (all upgraded to Buy at BofA/Merrill); KEY +2.8% (upgraded to Outperform at Keefe Bruyette), MCO +2.1% (light volume; upgraded to Overweight from Neutral at Piper Jaffray), HES +1.8% (upgraded to Overweight from Equal Weight at Barclays), KSS +1.7% (ticking higher; hearing upgraded to Buy fat tier 1 firm), MMM +1.3% (light volume; upgraded to Buy at Jefferies).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: HNSN -34.5% (also downgraded to Hold from Buy at Lazard Capital and downgraded to Hold at Brean Murray)... Other news: DFS -7.2% (files mixed securities shelf offering and announces $500 mln public offering of common stock), WY -2.5% (declares quarterly dividend of $0.05; down from $0.25 previously; also says guidance for the recently completed quarter remains unchanged), VOD -2.3% (Telefonica wins exclusive Palm Pre deals, which beat off interest in the Pre from European rivals such as Vodafone - Financial Times)... Analyst comments: VIVO -4.3% (light volume; initiated with a Average and $21 tgt at Caris), AMSG -2.9% (downgraded to Neutral at Baird), ASTE -1.2% (downgraded to Market Perform from Outperform at Barrington), CEPH -0.8% (downgraded to Hold at Argus). -

Cramer on täna avaldatud Saksamaa viimase kahe aasta suurimat tööstustellimuste numbrit positiivselt kommenteerimas:

I have seen the future, and it is German manufacturing orders! We are always looking for totems when we are teetering on the second dip, and a number that came out today from Germany showing a 4.4% increase in May manufacturing orders -- the best in two years -- ignited the European markets and should do the same for ours. -

Barclays arvab USA energiaettevõtetest igatahes nii:

"Barclays raises oil price assumptions for '09 and '10 to $57 and $75 per barrel; raises ests on integrated names accordingly; lowers ests on refinersBarclays notes they are raising their oil price assumptions for '09 and '10 to $57 and $75 per barrel, from $50 and $70 per barrel reflecting the current stronger than expected oil price environment. As a result of these changes, they are raising their Integrated Oil EPS forecasts by an average of 66% for '09 and 13% for '10. They are lowering their refiner earnings forecasts by an average of 45% for '09 and 19% for '10. They are raising their COP '09 EPS est to $3.75 from $3.15 (consensus $3.37) and their tgt to $59 from $61, they are raising their XOM '09 EPS est to $4.05 from $3.50 (consensus $4.32) and raising their tgt to $91 from $87 and they are raising their CVX '09 EPS est to $4.75 from $3.65 (consensus $4.57), lowering their tgt to $96 from $99. They are raising their MRO '09 EPS est to $3.25 from $2.30 (consensus $2.38) and raising their tgt to $73 from $72."

-

63-le dollarile kukkunud nafta Goldmani analüütikuid veel muretsema ei pane (kes oskavad muide päevapealt musta kulla hinnatõusu ette näha).....

......lugedes taandumist tooraineturul vaid korrektsiooniks, mille katalüsaatoriks oli oodatust nõrgem tööjõuturu raport. Seevastu muu makromajandusliku info osas on uudiseid olnud igasugust laadi ning pigem pööratakse tähelepanu positiivsetele sõnumitele tööstussektorist .

-

Mäletatavasti tõi PVM Oil Associates'i derivatiivide maakler eelmisel nädalal autoriseerimata toornafta positsioonidega kaasa musta kulla kaheksa kuu uue hinnarekordi, millest Dresdner Kleinwort järeldab järgmist:

It clearly underlines in our view that short-term events on the oil market have little to do with supply and demand. We expect the price correction to continue in the direction of $60 a barrel in the next few days. Even reports on further attacks on oil infrastructure in Nigeria have had little effect, an indication that the mood is changing on the oil market.

-

no täna on vist küll tagumine päev UNG`s pikaks minna

-

Päevasiseselt on UNG miinusest igaljuhul välja roninud ja plusspoolele jõudnud - hea märk.

-

-

UNG kauplemine peatatud?

-

takeover

-

UNGst pikemalt: Co discloses that on July 6, 2009, it announced in a current report on Form 8-K that only 32,100,000 of its units registered with the Securities and Exchange Commission (the "SEC") were available for purchase by UNG's Authorized Purchasers. As stated in its current prospectus, UNG creates and redeems units in blocks of 100,000 units called "Creation Baskets" and "Redemption Baskets," respectively. Only Authorized Purchasers may purchase or redeem Creation Baskets or Redemption Baskets. As of July 7, 2009, UNG issued all of the remaining outstanding units to its Authorized Purchasers. As a result of these issuances, UNG will temporarily suspend the issuance of additional Creation Baskets until the SEC declares effective the registration statement on Form S-3 (333-159772) which was initially filed on June 5, 2009 and registers an additional 1,000,000,000 units. This registration statement is currently subject to review and comment by the SEC, the Financial Regulatory Industry Association ("FINRA") and the National Futures Association ("NFA"). The suspension of the issuance of Creation Baskets has no effect on the ability of Authorized Purchasers to redeem baskets of units. (currently halted)

-

mida see tähendab?

-

Põnev case. Saan aru nii, et SEC on lubanud väljastada teatud hulga aktsiaid, mis on tänaseks limiidini jõudnud. Nõudlus UNG järgi on aga suurem ning seepärast küsitakse luba 1 miljardi uue aktsia väljastamiseks. Olemasolevate futuuride hulgaga ei suudetaks gaasi hinnaga täielikult korreleeruda.

-

kui nõudlus on nii suur, siis miks hind on nii madal

-

Kauplemine UNG-ga jätkub

-

Ok, õigem oleks öelda nii, et fondi mahtu ei saaks rohkem kasvatada (nõudlus fondi järgi, mis ei pruugi tähendada kohest hinna kasvu, sest vastaspool kasutab gaasi hinnaliikumiste peegeldamiseks futuure. Vastaspool ei ole teine investor.), sest SEC ei ole lubanud suuremat futuuride hulka.

-

UNG halt on üpriski kentsakas juhtum. Kuigi ETFidega kauplemise peatamine on harv juhus, on see siiski võimalik. UNG puhul on põhjuseks just kauplemismahtude ülikiire tõus, millega ei ole börsilkaubeldava fondi haldur suutnud piisavalt kiiresti arvestada... või siis pole SEC omalt poolt üles näidanud kiiret tegutsemisvõimet(-tahet). Kauplemismahtude tõus on allolevalt graafikult selgelt näha:

-

Kas uudis on siis:

* posit

* negat

* non event

? -

Põhimõtteliselt non-event.

Laiemas plaanis toob ETF'ide puudustele suuremat tähelepanu.