Börsipäev 31. august

Kommentaari jätmiseks loo konto või logi sisse

-

Head viimast suvepäeva kõigile! USA turgudel täna olulisi majandussündmusi tulemas ei ole - kell 16.45 tuleb üksnes Chicago PMI augustikuu kohta, kus oodatakse võrreldes juulikuu 43.4-punktilise näiduga olulist paranemist 47.2 punkti peale.

Kuigi mulle on siin foorumis juba korduvalt öeldud, et Hiina turgude langust ei tohiks üle tähtsustada, toon selle põikpäiselt jätkuvalt välja. Shanghai A indeks on hetkel -5.5% ning 2% jagu on languses ka Hang Seng. Shanghai A on augustikuu alguse tipust praeguseks kukkunud üle 800 punkti ehk 22%. -

Kui Jaapani aktsiaturg avanes senise opositsioonipartei DPJ valimisvõidu peale ca 0.7% ülevalpool ja käis ka ära 2.2%lises plussis, siis nüüdseks ollakse Aasia turgude suurte langustega koos samuti miinuses. Viimane suurem ralli, mida maailma üllatusliku poliitilise valimisvõidu peale aktsiaturgudel mäletab, on maikuu India valimised, mille peale sealsed aktsiaturud tõusid päevaga üle 15%.

-

India statistikaamet registreeris riigi teise kvartali majanduskasvuks 6.1% , mis oli mõnevõrra kiirem võrreldes esimeses kvartalis saavutatud 5.8%-ga. Keskpank ennustab selle aasta majanduskasvuks 6%, kuid juunis alanud ja neli kuud kestev mussoon on jätnud põllumaad tänavu tavalisest kuivemaks, mis võib negatiivselt mõjutada majanduskasvu ja põhjustada kallimate toiduainete näol inflatsiooni kiirenemist. Pikemalt võib lugeda Bloombergi artiklist.

-

Jefferies soovitas eelmine nädal UNG asemel osta Londoni börsil registreeritud NGAS´si. Kas see oleks "Safe Haven" regulatsioonide eest peitu pugemiseks?

http://www.etfsecurities.com/csl/classic/etfs_natural_gas.asp#key

http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aqrCHNw79gZA -

Tõsi, NGAS.Li ees peaks välja käima madalamat preemiat kui UNG eest, kuid toonitan veelkord, et mõlemad nimetatud instrumendid sobivad üksnes lühemaajaliseks kauplemiseks ning mitte pikaajaliseks hoidmiseks, kuna futuuride tõusvad hinnad koos kaugemate kuupäevadega muudavad nende indeksite pikaajalised tootlused väga negatiivseks. Ning lühemaajalise liikumise peale panustamiseks kõlbab hoolimata preemiast täna veel ka USA börsidel kauplev instrument.

-

Goldman Sachs on tõstnud Hiina tänavuse majanduskasvu prognoosi varasemalt 8.3%-lt 9.4%-le ning 2010. aasta kasvuootust 10.9%-lt 11.9%-le, olles veendunud, et Hiina aktsiaturg jääb oma kasvupotentsiaali tõttu globaalses pildis üheks kirkaimaks. GS usub, et turu hirm valitsuse lähiaja kavatsusest väljuda majandust stimuleerivatest programmidest on ennatlik ega juhtu enne kui kasv on saanud kindlama pinnase või ilmnema hakkab inflatsioonirisk. CSI 300 indeksi 2010 sihiks seab GS 4300 (+52% preaegusest tasemest) ning Hiina H aktsiate liikumist järgiva Hang Seng China Enterprises Index sihiks 16 800 (+50% praegusest tasemest). Viimase aja korrektsioon pakub analüüsimaja sõnul atraktiivset võimalust positsioone suurendada.

-

Kas UNG-le vastav short ka olemas on?

-

Mina ei ole sellisest inverse instrumendist teadlik.

-

Joel aga mis sinu arust oleks UNG puhul see lühemaajaline periood kuude lõikes. LHV positsioon avatud UNG-s praeguseks ca. 3 kuud.

-

Euroala tarbijahinnaindeks langes augustis 0.2% YoY, mis natuke parem oodatud 0.3% langusest.

-

London täna ei kauple ?

-

Londoni börs on täna pühade tõttu suletud.

-

aga Google on küll maagaasi shortimise instrumendist kuulnud

Londonis USDis ETFS Short Natural Gas

Milanos EURis ETFS Short Natural Gas -

Saksamaa autotootjate seas tekitab müügisurvet reedene Roland Bergeri raport, mille järgi ei ole välistatud cash-for-clunkers programmi lõppemise tõttu Saksamaal autode müügi vähenemine rohkem kui 20%:

In the study, published Friday, Roland Berger said car sales in Germany may fall more than 20% next year, and that as many as 90,000 jobs may be lost across the industry by the end of 2011. One in two car dealerships could be threatened with failure, and gross domestic product could take a hit, it said. (allikas: WSJ)

-

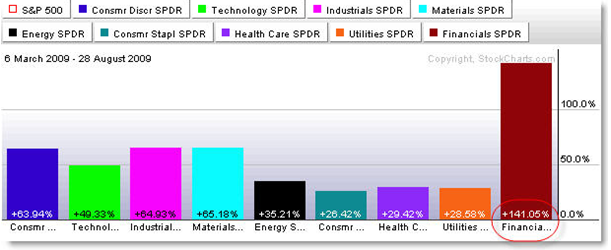

SPDRs ralli põhjadest (link graafikule siin):

XLF +140%. Kui puhkused lõppemas, tasub jälgida, kas turuosalised jätkavad offensive sektorite eelistamist!?

-

Mikku chartilt jäi puudu veel IYR (Real Estate) + 90 % ja XHB (Homebuilders) + 92 %.

-

Notable Calls on samuti puhkuselt tagasi & soovitab täna tähelepanu pöörata Goldman Sachsi GameStop'i soovitusele. LHV finantsportaalis on viimastel nädalatel kajastatud intervjuud blogipidajaga (loe siit) ja toodud näiteid blogi ideede põhjal kauplemisest (loe siit). Kel huvi tänase idee vastu, lugege blogi http://notablecalls.blogspot.com/

-

Stifel Nicolaus on täna väljas väga skeptilise kommentaariga Caterpillari (CAT) 2012. aasta prognoositava EPSi $8 kuni $10 saavutamise võimes.

Lühike kokkuvõte siia ka läbi Briefingu: Stifel Nicolaus sees CAT's mgmt's 2012 tgts as highly unrealistic (46.71)Stifel Nicolaus notes CAT sales and rev have moved closely with world real GDP since 1950. Using International Monetary Fund ests for GDP growth to 2012 firm calculates that CAT sales and revs would hypothetically be $48.6 bln in 2012, up 40% in three yrs from $34.6 bln in 2009E, yet far below the "approaching $60 bln base case" CAT mgmt presented at an analyst meeting August 4, 2009. Applying a CAT net income versus top-line regression since 1950 to those hypothetical sales projections equates to 2012 net income of $3.293 bln on 625 mln diluted shares, which would be 2012 EPS of $5.27 (6.8% net margin). That is far below the "$8 to $10 EPS by 2012" CAT mgmt "base case" scenario.

-

Endine Morgan Stanley Aasia aktsiate peastrateeg Andy Xie usub, et Hiina aktsiad on ainult üks suur Ponzi skeem ning et hoolimata 25%lisest aktsiaturu langusest tipust on kolmekordsel raamatupidamislikul väärtusel kauplevad aktsiad jätkuvalt väga kallid. Veel paar nädalat tagasi kauples ca 20% ettevõtteist üle 100 kordse kasumil.

Xie arvates oleks Shanghai Composite õiglane väärtus praeguse 2667 punkti asemel ca 1700 kuni 2000 punkti ehk 25% kuni 35% tänastelt tasemetelt veelgi madalamal.

Huvitav intervjuu, soovitan. Link siin.

-

Maailma börsidelt vaatavad vastu punased meeleolud ning teiste turgude languse taustal on ka USA futuurid avanemas miinuses. S&P500 futuurid indikeerivad päeva ca -0.7%list avanemist.

Euroopa turud:

Saksamaa DAX -0.81%

Prantsusmaa CAC 40 -0.65%

Inglismaa FTSE 100 N/A (börs suletud)

Hispaania IBEX 35 -0.29%

Rootsi OMX 30 -1.27%

Venemaa MICEX -1.79%

Poola WIG -0.62%Aasia turud:

Jaapani Nikkei 225 -0.40%

Hong Kongi Hang Seng -1.86%

Hiina Shanghai A (kodumaine) -6.75%

Hiina Shanghai B (välismaine) -6.16%

Lõuna-Korea Kosdaq -1.06%

Tai Set 50 -0.73%

India Sensex 30 -1.61% -

Sel Ponzi skeemi jutul võib tõsi taga olla. Nii Venemaa kui Hiina on ühise kommunistliku ajalooga, ja kommudega on kogu bisnes kahtlane.

-

Cracks in the Foundation?

By Rev Shark

RealMoney.com Contributor

8/31/2009 9:00 AM EDT

Caution is not cowardly. Carelessness is not courage.

-- Unknown

U.S. markets are set for a negative open following a 6.7% overnight decline of the Shanghai exchange. The Shanghai touched its lowest level in three months, and today's drop follows a 3% decline on Friday. Concerns of tighter monetary policy in China are driving the profit-taking, and the big drop is spooking our market, which is already lacking anything particularly positive.

Despite some good news lately from the likes of Intel (INTC) and Dell (DELL) and on the housing front, the major indices have been unable to make progress. The bullish view here is that this is just some healthy consolidation of an extended market that needs a rest. The bearish view is that the inability to rally further on good news is a sign that the market has priced in all the good news out there and is due for a more significant rest.

Last week's action had a bearish taint to it, but it wasn't quite bad enough to do any real technical damage. We simply stalled out, which may be the first step in a rollover or it may be just a pause that helps us consolidate and set up for further upside.

The bearish case here is pretty obvious. Many folks never believed the economic situation justified the strength we had off the March low. We are now in a seasonally weak time of the year and are unable to gain traction on good news.

The weakness in China is also significant because for much of the rally over the last few months, one of the bullish arguments was that strength in China and other overseas markets would be the real drivers that offset weakness in the U.S. Now that we are losing China, the U.S. will have to be the leader, and that is a very problematic contention for many.

I've been a bit slow in embracing the bearish view because the market has yet to do anything really negative. We just ran in place for a week, and that may prove to be a healthy thing, as has been the case a number of times since March. The fact that we haven't rallied on good news and that China is weak is definitely a warning. Also we have had a lot of "junk" running lately, and it isn't easy to find stocks that aren't in 3rd- or 4th-level bases.

These are good reasons to be negative, but we haven't yet seen real confirmation in the price action. This weak open will be a good test of the dip-buyers, who remain the key to this market. The bulls will have the edge until the dip-buyers weaken, but there is no mistaking the cracks in the action.

You never want to read too much into the open on Monday, so we'll see how things shape up -- still, increased defensiveness should be under consideration.

-----------------------------

Ülespoole avanevad:

M&A news: BJS +11.5% (Baker Hughes to acquire BJ Services in cash and stock or ~$17.94/share)... Other news: DCTH +31.6% (FDA grants Delcath orphan-drug designation for doxorubicin), POZN +13.3% (announces FDA acceptance of NDA For VIMOVO; $10 mln milestone earned), PACR +11.4% (enters into amended and restated credit agreement), MDCO +9.6% (announces new publication of data showing Angiomax reduces cardiac mortality and improves overall survival), SVA +7.9% (Sinovac Biotech's H1N1 Vaccine Passes Experts Evaluation Organized by SFDA), WIRE +5.3% (will replace Axsys Technologies in the S&P SmallCap 600), CBS +4.5% (CBS Corp reaches 65% sellout for Super Bowl - Media Week), ARG +4.1% (will replace Cooper Industries in the S&P 500), EXPO +3.1% (light volume; will replace Kirby in the S&P SmallCap 600), ATVI +2.7% (mentioned positively in Barron's), KEX +2.0% (light volume; will replace Airgas in the S&P MidCap 400), AZN +1.5% (announces that CRESTOR reduced risk of cardiovascular events in elderly patients in new analysis of Jupiter)... Analyst comments: KFN +7.7% (upgraded to Outperform from Mkt Perform at JMP Securities), GME +4.4% (raised to Conviction Buy from Buy by Goldman- DJ), CBI +1.9% (upgraded to Overweight from Neutral at JP Morgan).

Allapoole avanevad:

M&A news: BHI -3.2% (Baker Hughes to acquire BJ Services in cash and stock or ~$17.94/share), DIS -2.6% (Marvel Entertainment to be acquired by Disney for total of $30 per share in cash plus ~0.745 Disney share; transaction value is $50 per Marvel share)... Select financial names showing weakness: IRE -11.8% and AIB -8.4% (Ireland prepared to take majority stakes in banks - Sunday Business Post), AIG -9.2% (AIG weighing many options for ILFC: Sources - Reuters), FRE -7.1% and FNM -5.9% (Shares trade up on speculation; no underlying value remains - FBR Capital), BPOP -5.0%, GNW -3.9%, MBI -3.8%, C -3.4%, PMI -3.1%, HIG -3.0%, HBC -2.4%, MS -2.1% (downgraded to Neutral from Buy at BofA/Merrill), ING -1.7%, ABB -1.4%, JPM -1.4%, WFC -1.1%, GS -1.0%... Select oil/gas related names trading lower: ESV -3.0%, PBR -2.1%, SLB -1.9%, OXY -1.5%, COP -1.4%, XOM -1.1%... Select metals/mining names showing weakness: AU -3.2%, BHP -3.1%, GFI -2.7%, RTP -2.6%, ABX -2.4%, BBL -2.3%, VALE -2.3%, GG -2.2%, AUY -2.1%, MT -1.8%... Select China names trading lower following selloff in Shanghai: CHU -3.6%, SNP -2.9%, CHL -2.7%, BIDU -1.9%... Other news: KERX -16.5% (filed for a $40 mln common stock and warrants shelf offering), PNX -8.3% (Fitch downgraded the IFS ratings assigned to the life insurance subsidiaries of The Phoenix Companies), TSRA -6.2% (announced the Administrative Law Judge in the ITC issued an Initial Determination finding Tessera's asserted patents are valid, but not infringed by the respondents)... Analyst comments: SPF -5.6% (downgraded to Underperform from Market Perform at Raymond James), GENZ -3.7% (downgraded to Neutral at Baird), FICO -3.1% (ticking lower in early trade; hearing weakness attributed to downgrade before the open), AGO -2.5% (downgraded to Neutral from Buy at UBS). -

Kust saab vaadata turgude kogukäivet päeva lõikes?

-

Nasdaq ja NYSE üsna adekvaatse flash charti saab näiteks selliselt lehelt: http://www.sharkinvesting.com/volume.aspx