Börsipäev 14. september

Kommentaari jätmiseks loo konto või logi sisse

-

Suurem osa Aasia turgudest olid täna miinuses - languste rivi juhtis Jaapani Nikkei pisut üle 2%lise kukkumisega. USA futuurid on punases ca 0.8% jagu ja nafta languses 1.5%. USAs täna majandusraporteid välja tulemas ei ole.

-

Peaks tulema Obama kõne Lehmani aastapäevaga seoses (uued finantsturu regulatsioonid, valitsuse edasised sammud jne.).

-

Reede hilisõhtul teatas maagaasi liikumist jälgiv börsilkaubeldav fond UNG, et jätkab alates 28. septembrist juulist alates peatunud uute osakute väljalaskmist. Osakute väljalaskmise peatamise tulemusena on fond kaubelnud oma NAVi (UNG NAV reede õhtu seisuga $9.12) suhtes preemiaga, mis reede õhtu seisuga ulatus 16.1%ni. Uute osakute väljalaskmine peaks selle preemia nüüd ära kustutama. Kuigi osakute väljalaskmisega oodatakse septembri lõpuni, on ainuüksi väljalaskmise uudis tänasel börsipäeval toomas kaasa suure osa selle preemia kadumisest ning UNG hinnas korraliku languse.

-

Tavaliselt arvatakse, et vaid Aasia riigid on suutelised oma kaupa välisturgudel konkurentidest odavamate hinnatasemete juures pakkuma. Kuid nii üllatav kui see ka poleks, nuriseb hoopis Hiina selle üle, et USA nende turul osa oma tooteid alla turuhinna realiseerib ja ebaausat konkurentsi pakub. Pingestuvast kaubavahetuse suhtest kirjutab pikemalt Bloomberg

-

Morgan Stanley poolt kogutud andmete järgi on „credit crunch“ Euroopas viimastel kuudel suurenenud:

Net lending by banks went further into negative territory in July as companies paid back more loans than they took out new ones.

At the same time, there was a retreat in the recent record corporate bond issuance. Bond issuance in July declined for the first time since March, by €20bn month on month to €27bn, although bankers are convinced that it was only seasonal. (pikemalt FT''s)

-

Huvitav lugemine pealkirjaga: “Baling out the Titanic with a Thimble”. artiklis on point, et nõudlus majanduses koosneb SKP muutusest + võlakoormuse muutusest. Ameeriklaste võlakoormus oli 2007. aasta alguses 275% SKP'st (vs nt 175% enne Suurt depressiooni) & tarbijate soov vähendada suurt võlakoormust omab majandusele rohkem mõju kui valitsuse stiimulid. Teemakohane lugemine, kuna juulis langes USA consumer credit $21.6 mld dollari võrra (suuruselt teine protsendiline kukkumine pärast Teist maailmasõda).

-

Eurotsooni tööstustoodang langes juulis -0.3% MoM (15.6% YoY). Juuli number oli ootuspärane & IP kasv oleks olnud positiivne, kui juuni numbrit poleks korrigeeritud ülespoole.

Euroopa Komisjon ootab jätkuvalt sellel aastal 4% majanduslangust, kuid Q3 kasvuprognoos tõsteti +0.3%'le & Q4 +0.1%'le (kasvu asemel võib aasta teises pooles rohkem stabiliseerumisest rääkida). Prognoose saab täpsemalt vaadata siit.

-

Citigroup tõstab täna hommikul E*TRADE'i (ETFC) soovituse 'hoia' pealt 'osta' peale ja hinnasihi $1.50 pealt $2.30 peale, mis on turuhinnast pea 40% kõrgemal. Tänase soovituse tõstmise põhjused:

1) Even with conservative loss estimates, stock has good support

2) Provision trends are improving, not getting worse

3) Recent capital moves have allayed investor concerns

4) Shrinking the balance sheet/reducing risk

5) Growing core business

6) Possible events – take out play

Võimalike ETFCst huvitatutena märgitakse ära AMTD ja SCHW. Eelturul on aktsia igaljuhul juba ca 10% hüpanud.

-

USA alustab tänast päeva ca 0.5% kuni 0.8%lises miinuses. Peamise põhjusena toovad paljud välja USA poolt Hiina rehvidele kehtestatud 35%list tollimaksu, mis võib ekstreemse stsenaariumi korral aja jooksul viia kahe riigi vahelise kaubandussõjani, kuid kuna turud on lühiajaliselt üleostetud, siis võib pigem öelda, et lihtsalt otsitakse põhjust, et viimase aja tõusust natukene õhku välja lasta.

Euroopa turud:

Saksamaa DAX -0.99%

Prantsusmaa CAC 40 -1.01%

Inglismaa FTSE 100 -0.62%

Hispaania IBEX 35 -0.73%

Rootsi OMX 30 -1.36%

Venemaa MICEX -0.77%

Poola WIG -2.20%Aasia turud:

Jaapani Nikkei 225 -2.32%

Hong Kongi Hang Seng -1.08%

Hiina Shanghai A (kodumaine) +1.24%

Hiina Shanghai B (välismaine) +0.43%

Lõuna-Korea Kosdaq -0.26%

Tai Set 50 -2.21%

India Sensex 30 -0.31% -

Echoes of 1999

By Rev Shark

RealMoney.com Contributor

9/14/2009 8:32 AM EDT

The charm of history and its enigmatic lesson consist in the fact that, from age to age, nothing changes and yet everything is completely different.

-- Aldous Huxley

The market action last week had a similar feel to what we experienced in 1999. Prices went straight up and didn't pause for longer than a minute or two. While there were fundamental concerns, they didn't matter one bit to the market.

Back in 1999, the Fed was flooding the market with liquidity because of concerns over the Y2K problem. It seems a bit silly in retrospect that such worry over this issue turned out to be a complete nonevent, but back then the Fed was doing all it could to make sure there was plenty of cash in the system just in case. That money poured into stocks and resulted in a tremendous market bubble.

When we fast-forward 10 years, we see the Fed -- this time joined by Congress and the president -- throwing cash at the economy to help us through an extremely difficult period. The circumstances prompting the actions are quite a bit different and probably much more justified, but what isn't different is that all that cash out there is looking for a place to go. With interest rates close to nothing and real estate still struggling, the only real choice right now is the stock market.

Some folks will argue that the stock market isn't moving just because of liquidity but because fundamental conditions really are improving and that market players recognize that fact. Of course, it helps quite a bit that there is all that cash sloshing around.

We really don't need to determine if this strong market is fundamentally driven or liquidity-driven; we just need to appreciate that things are being driven up and that the trend is extremely strong. Back in 1999, many folks warned us that the move was unsustainable. They eventually were proved correct, but many were so early in their bearishness that they missed out on tremendous profits.

Like in 1999-2000, it is extremely easy to make bearish fundamental arguments about this market, but trying to guess when those things might matter is impossible. Given the amount of liquidity that has been pumped into the market, there is plenty of fuel for more upside regardless of what you may think of the fundamentals of the economy. It is very easy to overthink what is going on out there.

Back in 1999-2000, we were all a bit more naïve, and that might have made it easier to simply defer to the tremendously strong price action. In this environment, the negatives are much more obvious and conditions much more volatile. That makes it much harder to simply embrace the market and just ride it endlessly as it goes higher.

At some point, the negatives will matter again -- just like they did in 1999-2000 -- and there is likely to be a very nasty correction, but it is impossible to time when that might happen. All we can do is to watch the trend and stay vigilant. When conditions change it will happen quickly and we will need to act fast to protect our capital, but that isn't happening yet. The biggest danger remains being overly anticipatory of a correction.

We have a little negative action this morning on concern over the possibility of a trade war with China. So far it is a relatively minor issue involving tires, but the market is worried it could expand. In addition, we just need a little excuse for some profit-taking after going straight up all last week. China is as good an excuse as any.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: THC +7.2%... M&A news: S +26.0% (T-Mobile owner eyes multi-billion dollar bid for Sprint - UK Telegraph)... Select flu/biotech related names ticking higher: BCRX +4.0%, VICL +1.6%... Other news: SLXP +46.1% (announces statistically significant results for primary and key secondary analyses of rifaxamin), BRNC +19.4% (still checking), CVC +11.7% (mentioned positively in Barron's), ARIA +9.5% (announces result of first interim analysis of Phase 3 succeed trial of oral ridaforolimus in metastatic sarcomas; DMC recommends that trial continue with full patient enrollment and completion), VM +8.9% (still checking), XOMA +8.1% (announces plan to fully repay Goldman Sachs loan), HSTX +7.9% and CRNT +5.9% (Cramer positive comments on MadMoney), NLC +4.6% (mentioned positively in Barron's), THRX +4.4% (Theravance and Astellas announce FDA approval of VIBATIV for treatment for complicated skin and skin structure infections)... Analyst comments: ETFC +7.2% (upgraded to Buy at Citigroup), CMZ +7.2% (upgraded to Sector Perform from Underperform at CIBC Wrld Mkts), MOT +2.0% (upgraded to Buy at UBS).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: PSEC -2.6%, SSL -2.5% (light volume)... Select financial related names showing weakness: ING -4.2%, AEG -3.6%, MBI -3.6%, SLM -3.3%, DB -2.8% (downgraded to Reduce at Nomura), FITB -2.4%, RBS -2.2%, HIG -2.2%, AIG -1.8%, LYG -1.7% (downgraded to Neutral at Nomura), AZ -1.6%, BCS -1.6% (downgraded to Neutral at Nomura), BAC -1.6%, C -1.3%... Select metals/mining stocks trading lower: GFI -2.9%, GOLD -2.7%, AUY -2.6%, KGC -2.5%, AEM -2.3%, BBL -2.1%, VALE -1.9%, BHP -1.9%, GG -1.8%, ABX -1.5%, MT -1.3%... Select oil/gas related names seeing early weakness: BP -2.1%, PBR -1.7%, TOT -1.5%, RDS.A -1.4%, SLB -1.4%... Other news: ALXA -31.0% (announces preliminary results from its AZ-104 Phase 2b trial in patients with migraine headache; study did not meet its primary endpoint), DPTR -7.3% (pulling back from last week's surge higher), CWTR -7.0% (Dennis Pence has assumed the duties of President and Chief Executive Officer, effective immediately, replacing Daniel Griesemer), REGN -5.2% (Phase 3 trial of aflibercept in metastatic pancreatic cancer discontinued; Three Phase 3 studies continue)... Analyst comments: CAB -4.4% (downgraded to Underweight at JPMorgan), CDE -3.5% (downgraded to Underperform from Sector Perform at RBC Capital Mkts), FSLR -3.5% (downgraded to Sell at Soleil), MOS -3.2% (downgraded to Hold at Citigroup), AA -2.6% (initiated with Underweight at HSBC), GFIG -2.5% (downgraded to Neutral from Buy at Pali), CNSL -2.5% (downgraded to Hold at Soleil), POT -2.4% (downgraded to Hold at Citigroup), SPWRA -1.9% (downgraded to Outperform from Strong Buy at Raymond James). -

Joel mis selle ETFC.ga momendil toimub ?

-

matu111, mida täpselt mõtled? Ma näen volatiilset liikumist, kus Citi upgrade'i peale läksid lühikesed turu alguses oma positsioone katma (ca 30% floatist on short) ning mida paljud pikad on omakorda kasutanud müümisvõimaluse.

-

ug-le lükkas ETFC väikese filingu peale.

-

DNDN +8%... ülevõtujutud (taas) liikvel.

-

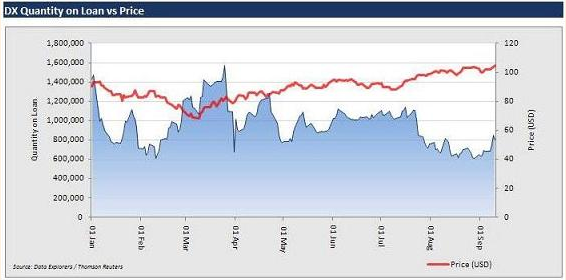

Data Explorersi graafik, mis näitab SPY välja laenatud osakute kogust on tõusnud 24% 7. septembrist:

S&P500 on sellel aastal tõusnud 12% ja kuna valuatsioon tõusuks ruumi ei jäta (praegu keskendudakse niigi üha rohkem 2011. aastale), siis siit oodatakse juba tõsisemalt mõningast kasumite lukustamist. Täna on turg igal juhul langusest välja roninud, kuid kahtlen, et siit palju enam jõudu ülespoole liikumiseks.

-

To: Joel

Kust selle DNDN ülevõtujutu koht rohkem infi saaks? -

Merriman: it wasn't me.

-

Neid ülevõtujutte olen kuulnud ma alates esimesest päevast, mil Provenge näitas statistiliselt olulisi efektiivsuse näite. Nii et mine võta siis kinni...

-

Bank of America: U.S judge rejects settlement with SEC, orders trial according to NY court document - Reuters (16.68 -0.30)

Judge says proposed settlement is neither fair, reasonable or adequate. -

Sector ETF strength & weakness @ midday

Leading Sector ETFs:

Coal- KOL +2%, Nat gas- UNG +1.5%, iShares REITS/real estate- ICF +1%, IYR +1%, US airlines- FAA +1%, SPDRS utilities- XLU +1%, Dry-bulk shippers- SEA +.5%, Biotech- IBB +.5%, BBH +.5%, SPDRS retailers- XRT +.5%Lagging Sector ETFs:

Solar power- TAN -1.5%, KWT -.5%, Base metals- DBB -1.5%, Ag/chem- MOO -1.5%, Livestock commods- COW -1.5%, Commods- DBC -1%, GSG -1%, RBOB gas futures- UGA -1%, Crude/WTI oil- USO -.5%, OIL -1%, Comm banks- KBE -1%, Gold miners- GDX -.5%, SPDRS homebulders- XHB -1% -

tunne siuke, et homme on massive rally over the world.

but im retard. -

ostaks tiba C-d ..vaataks mõne päeva jooksul mis juhtub.

-

C viimasel ajal üsna raske olnud ja pole turu eufooriaga kaasa läinud. Kas enne näeme enne $4 või $5 taset?

-

ja siit tuleb ralli!

-

njah ei taha siga rallida veel.