Börsipäev 1. oktoober

Kommentaari jätmiseks loo konto või logi sisse

-

Head oktoobrikuu algust kõigile! Eilsega sai läbi 2009. aasta 3. kvartal ning nüüd on jäänud esimeste majandustulemuste ootamiseni veel loetud päevad. Aktsiaturgudel oli 3. kvartal sarnaselt 2. kvartalile väga võimas - S&P500 indeksi liikumist jälgiv börsilkaubeldava fondi SPY tootlus koos dividendidega oli 15.4%. 2. kvartalis oli see 16.3% ja 1. kvartalis -11.3%. Viimase 14 aasta kvartaalne tootluste graafik on olnud selline:

Täna on tulemas hulgaliselt majandusraporteid. Tund aega enne USA turu avanemist teatatakse eraisikute augustikuu sissetulekute muutus (ootus +0.1%), kulutuste muutus (ootus +1.1%), esmaste töötu abiraha taotlejate arv (annualiseeritud ootus 535 000) ja kestvad töötu abiraha taotluste arv (ootus 6.17 miljonit). Pool tundi pärast turgude avanemist ehk Eesti aja järgi kell 17.00 teatatakse augustikuu ehitustegevuse kulutuste muutus (ootus -0.1%), septembrikuu ISM indeks (ootus 54.0 punkti) ning augustikuu pending home sales (ootus +1.0%).

-

saksa (retail sales) ja jaapani (capital investment) kehvemad tulemused kukutasid varahommikul jārsult EUR/USD-i ca 70 punkti, ka Nikkei -1,5 %. Turul tundub olevat suur nōudlus USD jārele, tōenāoliselt oodata mōningast selloffi aktiaturgudel. aga avaldatavad tulemused vōivad selle pea peale keerata...

-

Täna võib AA päev olla. Kes teab.

-

? AA

-

AA nagu Alcoa, on üks päris suur alumiiniumitootja, kaupleb börsil.

-

:)

arvasin midgi muud... tänud -

kas mingu uudis aa kohta

-

Riias on Ventspils nafta tõusnud +15% Mis küll võis seda põhjustada?

Võibolla USA, kus tõusis vist +20% American Oil & Gas Inc. (AEZ)? -

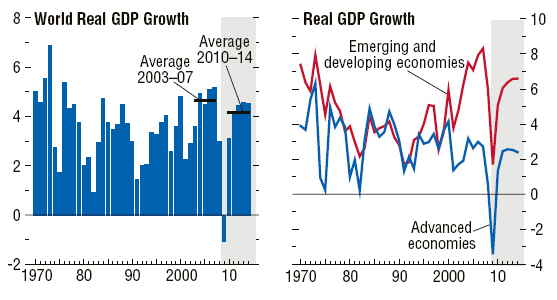

Nii nagu Handelsblatt eile spekuleeris, on IMF-i arvates maailmamajanduse tervis paranemas ning järgmise aasta kasvuprognoos pole enam 2.5%, vaid 3.1%. Kui arenenud riikidel jääb tõus suhteliselt loiuks ( 1.3%) siis arenevate majanduste reaalne SKT kasv peaks 2010 aastal ületama 5%. Võidukaarikut veavad Hiina (+9%), india (+6.4%) ning mitmed muud Aasia regiooni riigid. 226 lk pikkust raportit on võimalik lugeda siit

-

fun, tähtis ei ole ju, kas on AA päev või mitte. Seda saame teada. Tähtis, et on selle päev, kes ekraani taga jõllitab. :)

-

Oh my... Merrill Lynch tõstab täna kõrgemate marginaalide ootuses oma Apple'ile (AAPL) tehtavaid aktsiapõhiseid kasumiprognoose ning hinnasihti - soovitab aktsiat osta ning liigutab hinnasihi $185 pealt $220 peale. Merrill tõstab äsja lõppenud 2009. fiskaalaasta 4. kvartali EPSi ootuse $1.33 pealt $1.47 peale (mis on oluliselt üle turu konsensusootuse $1.38).

Apple peaks oma tulemused teatama ca 3 nädala pärast.

- 30. september 2009.PNG)

Apple'il on erinevate analüüsimajade poolt kokku antud 35 ostusoovitust, 1 hoiu- ja 2 müügisoovitust. Müüa soovitavad üksnes väiksed analüüsimajad Gabelli & Co ning MF Global Securities, kes on väljas $86lise hinnasihiga.

-

Suurbritannia septembrikuu PMI 49.5 punkti vs oodatud 50.2 punkti. Euroopa turud ja USA futuurid näevad selle peale müügisurvet.

-

Kes teab öelda kui mitu korda kujuneb Iraagi sõda arvatust kallimaks? Vastus 50x. Siin on üks tore lehekülg, mis paneb miljonid, miljardid ja triljonid perspektiivi.

-

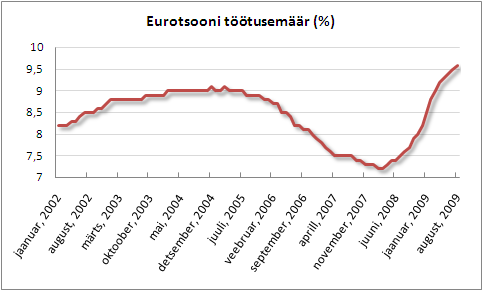

Töötusemäär kerkis eurolalal augustis 0.1 prosendipunkti võrra taas kõrgemale võrreldes juuliga, ulatudes nüüdseks 9.6%-ni ning ühtides Bloombergi küsitletud analüütikute prognoosiga. Ent nagu mitmed Euroopa Keskpanga liikmed on oma kõnedes viimasel ajal toonitanud, jätkab töötus kasvamist veel järgmisel aastalgi ning võib hakata rõhuma regiooni majanduse taastumist. Lähtudes IMF-i tänasest raportist, siis eurotsoon seisab 2010. aastal silmitsi 11.7%-lise tööpuudusega.

-

0,1 protsendipunkti võrra nagu 0,001%?

Või siis ikka 1 protsendipunkti võrra?

Muide - minule isiklikult ei ole need protsendipunktid üldse mokkamööda. Miks me ei võiks rääkida lihtsas keeles ja lihtsalt protsentidest? -

Hmm - nagu ikka, kõigepealt lõuga ja siis uuri.

Natuke uurimistööd ja asi selgem.

"mõiste "protsendipunkt" on võetud kasutusele selleks, et eristada protsenti/mõõtühikut/ protsendist/suhtarvust.

Kui ühel pangal on intressimäär 4%, siis sellest ühe protsendi võrra suurem intress on 4,04%. 5% intress on 4% intressist suurem ühe protsendipunki võrra."

Vabandan oma ebakompetentsuse pärast ja minu poolest võib minu eksitava posti ära kustutada. Olen lihtsalt juhtunud nägema palju postitusi kus protsendipunkti all mõistetakse 0,01% ja hämmastusega nentinud, et mis mood see siis nüüd on -

Meili peale tuli küsimus Suurbritannia naela tänase tugevuse kohta, kui samal ajal tuli PMI oodatust väiksem. Vastus siis selline, et lõuna ajal oodatust nõrgem UK PMI küll korraks naela USA dollari vastu nõrgestas, kuid kuna IMF tõstis Suurbritannia majanduskasvu väljavaateid 2010. aastaks +0.2% pealt +0.9% peale, siis viimase positiivne mõju oli PMI negatiivsest mõjust suurem ja pidev ostuhuvi naelas ongi päeva edenesed viinud selle plussi.

-

enn.e,

ma jätaks su postitused alles, ehk aitab see teistelgi erinevust selgemaks teha -

Eile õhtul hype'is Cramer NVDA-t, see pani järelturul kõvasti üles ja sulgus $15.28. Ütles, et "Investors looking to profit from the growing trend of netbook computing need to check out Nvidia (NVDA), said Cramer. He said these ultra small, ultra cheap computers represent a huge secular growth trend for the company."

Kutsun Jim Crameri duellile! 10 000 krooni võitjale + alatine respekt. Ühesõnaga, short NVDA $14.96-14.90 (avg 14.93). See positsioon ilmselt suureneb mingil hetkel. -

August Personal Income +0.2% vs +0.1% consensus, prior revised to +0.2% from 0.0%

August Personal Spending +1.3% vs +1.1% consensus, prior revised to +0.3% from +0.2%

August PCE Core M/M +0.1% vs +0.1% consensus, prior +0.1%

August PCE Deflator Y/Y -0.5% vs -0.6% consensus, prior -0.8%

Initial Claims 551K vs 535K consensus, prior revised to 534K from 530K; Continuing Claims falls to 6.09 mln from 6.16 mln -

USA eelturg on hetkel ca 0.5% miinuspoolel.

Euroopa turud:

Saksamaa DAX -0.10%

Prantsusmaa CAC 40 -0.43%

Inglismaa FTSE 100 -0.36%

Hispaania IBEX 35 -0.56%

Rootsi OMX 30 -0.78%

Venemaa MICEX +1.47%

Poola WIG +1.33%Aasia turud:

Jaapani Nikkei 225 -1.53%

Hong Kongi Hang Seng N/A (börs suletud)

Hiina Shanghai A (kodumaine) N/A (börs suletud)

Hiina Shanghai B (välismaine) N/A (börs suletud)

Lõuna-Korea Kosdaq -0.67%

Tai Set 50 +1.57%

India Sensex 30 +0.05% -

Warning Signs at the Start of the Quarter

By Rev Shark

RealMoney.com Contributor

10/1/2009 8:35 AM EDT

When life is too easy for us, we must beware or we may not be ready to meet the blows which sooner or later come to everyone, rich or poor.

-- Eleanor Roosevelt

The last day of the third quarter was one of the most chaotic we have seen in a while. The bears, who are convinced about the deteriorating fundamentals of the economy, battled with the dip-buying bulls, who have made a mint buying every pullback in this market. Yesterday the bears grabbed the advantage out of the gate on some poor economic news, but the dip-buying bulls showed once again that they will not be denied. We ended the day slightly in the red, but it was an impressive recovery for the bulls yet again.

As we kick off the fourth quarter of this crazy year, the big question is "Now what?" The pattern of the indices for quite a while now has been very sharp recoveries after a few days of weakness that looked like they may be indications of a market top. So far we have had very few signs that the inclination toward buying pullbacks is going to slow.

What has been driving this market for so long is that so many market participants have never been able to embrace the strength. Many were burned in the big meltdown last year and early this year, and they never believed that the market was going to recover from that nightmare by moving straight up for many months without a pause. Many thought it was just a bear-market bounce that would abruptly come to an end, but it is still going and there is a huge amount of anxiety among the underinvested folks on the sidelines who never embraced it.

These underinvested, reluctant bulls have continued to frustrate the fundamental bears, who are absolutely convinced that the market has moved far beyond what the fundamentals support. They are convinced that it is only a matter of time before all their concerns will begin to matter and the market will undergo a correction.

The problem of course is timing, and the bulls just won't give up despite all sorts of reasons, both technical and fundamental, for them to relent. We have had a few negative developments lately, but they've been mild and there isn't anything to indicate that a major trend change is about to take place.

After three days of pulling back last week that took us to key technical support of 1140 or so on the S&P 500, we bounced strongly but on low volume on Monday. Typically during this market run the bulls would just keep on going, but on Tuesday we were unable to follow through, although the selling was mild. That brought us to yesterday and the big battle, with the end result of a slight win for the bears.

So the question now is whether this ferocious and persistent buying of pullbacks will continue and keep this market going. That is the key attribute to this market, and when the dip-buying falters, the market will be in danger of seeing the trend turn down.

The recent action does raise some warning flags and we want to be more defensive, but it isn't enough to send us into to bear mode, especially because the first few days of a new month tend to have a positive bias.

The market is seeing increasing volatility; that is a sign of indecision and sometimes indicates that a change in market trend is coming. We don't want to jump the gun, but the bears are gaining more of an edge and we need to be ready to protect ourselves.

Indices are indicated to open slightly weak. Goldman Sachs downgraded Microsoft (MSFT) and we are probably going to hear about Ken Lewis so much that we will be tempted to start watching Brady Bunch reruns on Nickelodeon.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: XRTX +9.8%, STZ +9.6%, TER +8.1%, LWSN +7.9%... Other news: CPRX +22.6% (continues clinical development of CPP-109 for the treatment of cocaine and methamphetamine addiction; also upgraded to Neutral at Merriman), OPTT +20.1% (light volume; announces that it has achieved a significant milestone for its autonomous PowerBuoy product with the award of a new $2.4 mln contract), CHTP +17.9% (announced that continued analysis from first of two pivotal Phase III trials on Droxidopa confirm statistically significant benefits), PRST +13.7% (International Trade Commission finds VIM product infringes valid Presstek patents and violates Federal law), BCRX +10.2% (responds to Request for Proposal from U.S. Govt; initiates Phase 3 studies for patients hospitalized with influenza), SEAC +8.7% (still checking), SORL +8.3% (receives $744k tax refund), HALO +8.3% (presents phase 2 results for regular Insulin-PH20 confirming faster insulin absorption and superior glucose control), VICL +5.9% (announces the U.S. Navy has awarded a contract for $1.25 million to support large-scale cGMP vaccine manufacturing), APT +3.6% (still checking), DFT +2.4% (Cramer makes positive comments on MadMoney), BAC +1.0% (confirms that Ken Lewis announces his retirement)... Analyst comments: MLNX +1.8% (upgraded to Overweight from Neutral at JP Morgan), AA +1.4% (upgraded to Buy from Hold at Deutsche Bank), BIG +1.2% (upgraded to Overweight from Neutral at JP Morgan).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: AEHR -7.6% (light volume), GA -3.4%... Select metals/mining names trading lower with strength in the dollar: BHP -2.7%, BBL -2.2%, NG -2.0%, GOLD -1.6%, RTP -1.2%, MT -1.2%... Select financial names showing weakness: RBS -2.9%, LYG -2.9%, DB -2.0%, BCS -1.7%, FITB -1.6%, ING -1.4%, HIG -1.4%... Select European drug names trading lower: NVS -1.4%, AZN -1.1%... Select casino related names seeing early weakness: LVS -1.7%, WYNN -1.7%, MGM -1.6%... Other news: ABAT -7.8% (announces $19 mln registered direct offering), PAG -7.6% (terminates discussions with General Motors to acquire Saturn), ASTI -6.6% (announces public offering of 4 mln common shares and commitment from Norsk Hydro to purchase ~$5 mln of common stock), UAUA -5.6% (announces plans to offer 19 mln shares of common stock, and $175 mln in convertible senior notes due 2029), ETP -3.4% (filed for a 6 mln share common unit offering), HLCS -2.8% (filed for a ~6.63 mln share common stock offering by selling shareholders), CMCSA -2.7% (Comcast denies report on a deal to buy NBC Universal - NY Times ), SKS -1.8% (announces pricing of public offering of common stock of $6.70 per share), CLP -1.3% (announces pricing of 10,530,000 of its common shares at a public offering price of $9.50 per share)... Analyst comments: RVSN -21.0% (downgraded to Sell from Buy at Cantor Fitzgerald citing CSCO acquisition of competitor; downgraded to Underperform from Sector Perform at RBC Capital), PCS -3.3% (downgraded to Neutral at JPMorgan), AKAM -2.9% (downgraded to Sell at Merriman), FCS -2.2% (downgraded to Underweight at JPMorgan), A -1.9% (downgraded to Market Weight from Overweight at Thomas Weisel), PMCS -1.7% (cut to Neutral from Buy by Goldman- DJ), LEAP -1.5% (downgraded to Neutral at JPMorgan), NVDA -1.2% (downgraded to Underweight at JPMorgan), MAN -1.0% (downgraded to Hold from Buy at Citigroup), MSFT -1.0% (cut to Buy from Conviction Buy by Goldman Sachs - DJ). -

Nvidias siis JPMorgani downgrade + funi sisemine hääl Crameri vastu. hetkel paistab, et cramer kaotab. hea call, fun.

-

Väljas NVDA. Lõpuks siis oli avg $14.90 ja 6200 aktsiat. Shordi katsin 14.67-14.71 (avg. 14.68) ära. +1331 taala net. Kogus jäi 30c liikumise püüdmiseks liiga väikeseks, aga ei tekkinud kuskil hinna juures sobivat tunnet, et suurelt teha.

-

-

Pildi peal on jah huvitav võrdlus, aga isiklikult toetan seisukohta, et neid kahte riiki ja majandusmudelit on võimatu võrrelda. Lisaks ei kannata võrrelda jaapanlase ja ameeriklase käitumist, tarbimishajrumusi, huumorit:)

-

September ISM Manufacturing 52.6 vs 54.0 consensus, August 52.9

August Construction Spending M/M +0.8% vs -0.1% consensus, prior revised to -1.1% from -0.2%

August Pending Home Sales M/M +6.4% vs +1.0% consensus -

Keegi võiks siin mõnda teistsugust strateegiat ka tutvustada ja paar treidi välja visata. Äkki mõni põnev sümpaatiamäng vmt? Muidu jääb mulje, et kauplemine ongi nii ühekülgne, kuigi tegelikult ju pole.

-

ma kui algaja karu pakun FAZ

-

Küsimus TA gurudele - kas viimase kuue kuu tõusutrendijoone tänane murdumine võiks dip-buyerite soovi iga hinna eest aktsiaturge osta, nüüd mõneks ajaks maha rahustada?

-

short GBP/USD 1000K, entry @ 1,6005, target: 1,5900.

sygav sisemine veendumus, et tānane Dow kehv algus on mārgilise tāhendusega. -

FAZ positsioon kinni, päevasisene +5% mulle piisav

-

Kui Goldman Sachs oli juba niigi võrreldes konsensusootusega (ca -180 000) homse tööjõuraporti numbri osas negatiivsem, siis pärast tänast ISM indeksi olulist ootustele allajäämist on GS oma tööjõuraporti numbri ootuse langetanud nüüd -200 000 pealt jupp maad madalamale -250 000 peale.

-

General Motors says Sept sales down 45% from year earlier - Reuters

-

CIT Group planning for a debtor-in-possession loan of $5 bln to $7 bln, if it has to file for pre-packaged bankruptcy, sources say - Reuters

-

Richmond Fed's Lacker says Fed may need to raise interest rates before employment shows signs of recovery

-

VIX täna üle +10%. Welcome back dear friend.