Börsipäev 10. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

USA turud sulgusid eile tänu lõputunni ostuhuvile ca 0.5% kõrgemal, kuid sellest jäi väheseks, et Aasiat täies ulatuses plussi lükata. Liikumine on seal täna hommikul olnud erisuunaline: Jaapan -1.4%, Hongkong -0.65%, Hiina +0.45%.

Euroopas leiab täna aset kahe keskpanga kohtumine, ent suurt muutust seni tehtud avaldustesse ei oodata ei Inglise ega ka Šveitsi keskpanga puhul. USA-s avaldatakse kell 15.30 esmaste töötuabiraha taotlejate arv, mille suurusjärguks ootab konsensus 455 000 (eelneval nädalalal 457 000) ning paralleelselt teatatakse ka oktoobrikuu kaubandusbilanss.

-

Hispaania eelarve defitsiidiks prognoosib S&P reitinguagentuurg 11.5% 2009. aastaks, 11% 2010. aastaks ja loodetavasti kahaneb see 3% juurde 2012. aastaks. Riigi võlakoormus on kiiresti kasvamas ning kulutusi ei olda koomale tõmbamas. Kiiresti kasvav riigi võlakoorem oli peamine põhjus, miks S&P andis Hispaania AA+ reitingule negatiivse väljavaate. Üks intervjuulink ka siia.

-

Obama peab Nobeli rahupreemia kõnet, mida saab otseülekandes jälgida CNNi pealt. Väga hea jutuga mehega on tegu vaieldamatult.

-

Initial Claims 474K vs 455K consensus, prior 457K

Continuing Claims falls to 5.157 mln from 5.460 mln -

October Trade Balance -$32.9 bln vs -$36.8 bln consensus, prior revised to -$35.7 bln from -$36.5 bln

-

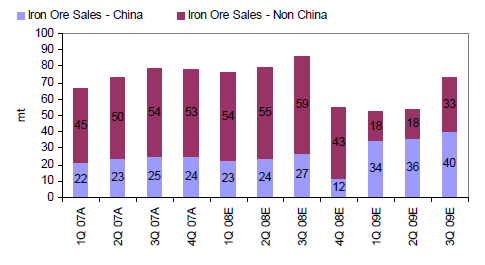

JPM on tõstnud Brasiilia kaevandustööstuse Vale'i (VALE) soovituse "overweight" peale (hinnasiht tõsteti 24.50 pealt 35.50 peale). Aktsia kaupleb eelturul 1.7% plusspoolel 28.5 dollari juures. Vale on Hiina hype, kus rauamaagi nõudus on ülikiirelt tõusnud (tänu fiskaalstiimulitele):

-

USA aktsiaturud alustavad päeva plusspoolelt. S&P500 indeksi futuurid hetkel ca +0.6% ja Nasdaq100 omad +0.3%.

Euroopa turud:

Saksamaa DAX +1,21%

Prantsusmaa CAC 40 +0,89%

Inglismaa FTSE 100 +0,66%

Hispaania IBEX 35 +0,13%

Rootsi OMX 30 +0,43%

Venemaa MICEX +0,30%

Poola WIG +0,11%Aasia turud:

Jaapani Nikkei 225 -1,42%

Hongkongi Hang Seng -0,19%

Hiina Shanghai A (kodumaine) +0,46%

Hiina Shanghai B (välismaine) +0,12%

Lõuna-Korea Kosdaq +0,55%

Tai Set 50 N/A (börs suletud)

India Sensex 30 +0,37% -

Looking for Direction

By Rev Shark

RealMoney.com Contributor

12/10/2009 8:47 AM EST

Patience is waiting. Not passively waiting. That is laziness. But to keep going when the going is hard and slow -- that is patience.

-- Unknown

With the help of Apple (AAPL) the buyers came alive in the final 90 minutes of trading on Wednesday and put some green on the screen. Despite this positive action, this is a market that is still looking for direction.

Over the last three weeks we have been in the tightest trading range all year. The technical patterns aren't bad, but they're not compelling either. It is a very neutral situation. We have had a number of distribution days lately, but the major indices are still holding near their highs and we are bouncing around rather randomly on news. The bulls are all ready for an end-of-the-year Santa Claus rally, while the bears are looking for money managers to lock in gains and move to the sidelines early.

Trading-range markets often make for very good trading, but this one hasn't been so easy. The problem is that there is little quality leadership and there are few good themes. We also have had gaps to start the day and then quiet trading intraday, which means if you aren't in overnight you don't get a chance to get in.

Gold, oil and commodities were doing very well on the weak dollar, but the dollar is now showing some signs of strength this week and there is concern that some of the big money may start to unwind the dollar carry trade, which has been driving the commodity and energy sectors.

The dollar sank again into the close last night, which helped to trigger our late rally, but the dollar is looking better, and it may not be the same positive factor going forward. Ideally, I'd like to see less focus on and correlation with the dollar and some new leadership groups emerge. Rotation into technology, retail, biotechnology is what we need at this point. The late jump in AAPL on Wednesday gives some weight to the rotation idea; we'll see if that plays out further.

The big picture right now is very mixed. Neither the bulls nor bears have been able to gain much traction lately, and we are still waiting to see if new themes or trends emerge as the dollar gains strength. The pockets of momentum that I am always looking for are very narrow, with a few plays in China and a smattering of small technology and chip stocks, but there is nothing particularly hot.

The good news it that this sort of action usually is a good setup for some better trading down the road. Eventually we'll break out of the range and we'll see some new trends in play. I'm leaning toward the idea that big-cap technology like AAPL, Amazon (AMZN) , Priceline (PCLN) , Baidu (BIDU) , Google (GOOG) , Research In Motion (RIMM) and others may take the lead and drag some other smaller technology names along for the ride. That is the thesis; we just have to wait to see if it develops.

I'm going to be agnostic as to market direction at this point and will continue to look for indications of new emerging trends and themes. If we can catch them early, it will make for some good trading to end the year.

We have AAPL continuing its run this morning and gold weaker. Stay alert.

-----------------------------

Ülespoole avanevad:

European banks trading higher after Eurogroup head said Greece 'will avoid bankruptcy': RBS +5.0%, ING +4.8%, CS +2.1%, BCS +1.8%... Other news: AKNS +20.0% (Andalay AC solar panels now available at Lowe's Home Improvement Stores, ONTY +4.7% (announces that Merck KGaA of Darmstadt, Germany, has initiated a Phase 3 trial of Stimuvax in Asian patients with advanced non-small cell lung cancer), ME +4.6% (APC announced a discovery at the Lucius exploration well - ME is a co-owner of the discovery), PXP +3.0% (APC announced a discovery at the Lucius exploration well - PXP is a co-owner of the discovery), NBG +3.0% (Greece 'will avoid bankruptcy,' Eurogroup head says - AFP), NLST +2.8%, WU +2.8% (announces dividend increase to $0.06 from $0.04 and new $1 bln share repurchase authorization), C +2.6% (Treasury official says Citigroup negotiations are a moving target, but headed in a good direction - CNBC), GFI +2.5% (still checking), AAPL +0.9% (China Unicom says sold 100,000 Apple iPhones in China since launch - DJ)... Analyst commentary: HNSN +7.8% (upgraded to Buy at Brean Murray; tgt $4.50), OXM +7.1% (upgraded to Buy at Suntrust), VECO +2.7% (initiated with a Buy at UBS), MEE +2.5% (upgraded to Overweight from Neutral at JP Morgan).

Allapoole avanevad:

On disappointing earnings/guidance: STLD -4.5%, KONG -3.1% (announces impact due to new telecommunications operator measures; sees Q4 revenue of $34-$35 mln vs $36.66 mln consensus), CIEN -2.5%... Other news: SIGA -10.4% (announces sale of 2.7 mln shares at $7.35), IT -8.3% (filed for a common stock shelf offering for an indeterminate amount), Analyst commentary: GEF -9.1% (downgraded to Underperform at Barrington Research), SUSS -5.2% (downgraded at BofA/Merrill). -

Dick's Sporting Goods (DKS) on BofA Merrill Lynchi käest saanud ostusoovituse (varasem soovitus "neutraalne"). Hinnasiht tõsteti $23 dollari juurest $28 dollarile. Pärast aktsia korralikku kukkumist tundub väga hea call & DKS kaupleb eelturul $22.7 dollari juures (+6%). Notable Callsi sõnul on hind all 22.5-i screaming buy.

-

UNG liikuma saanud kergelt ja põhjus ehk siit

http://finance.yahoo.com/news/Natural-gas-stocks-decline-apf-3845704411.html?x=0&.v=2 -

Arvestades praegust tuisust ja väga külma talveilma USA põhja- ja kirdeosariikides, näeme ka järgmisel nädalal kindlasti päris korralikku varude vähenemist.

New Yorkis täna öösel -7 kraadi, homme -6 ja ülehomme -6 kraadi Celsiuse järgi; Chicagos hetkel -14.5 kraadi, täna öösel -13, homme -8, ülehomme -6 kraadi jne. Tuulekülm muudab reaalselt tunnetavad kraadid veelgi oluliselt külmemaks ning külma käest pääsemiseks on vaja tube kütta... ja korralikult. -

Visa (V): Hearing removed from Buy list at Deutsche Bank

MasterCard (MA): Hearing removed from Buy list at Deutsche Bank

Mõlemad vajunud päeva põhjadesse. -

Moody's downgrades three Dubai-based banks:

Emirates NBD, Mashreqbank PSC and Dubai Islamic Bank PJSC -

American Axle announces pricing of $425 mln in senior secured notes

Co announces its wholly owned subsidiary, American Axle & Manufacturing, has priced its previously announced offering of $425 mln in aggregate principal amount of 9.25% senior secured notes due 2017 at an issue price of 98.715% in an offering exempt from the registration requirements of the Securities Act of 1933.

Paistab, et GM rahasüstist hakkab juba puudu tulema. -

GS teatas, et maksab boonused 100% välja, kuid väljamaksed toimuvad GS aktsiates ning piiranguks 5 aastane müügikeeld.

-

Tänasest on NYSE-l kaubeldav uus CIT aktsia ning hetkel indikeerimas hinda $28.10. Hetkel jääb kergelt arusaamatuks, kas ka CITGQ aktsionärid midagi saavad. Suure tõenäosusega siiski jäävad neile tühjad pihud.

http://www.nytimes.com/2009/12/10/business/10cit.html -

MF's Lipsky says global economic recovery tentative in some places, new shocks still possible - Reuters

-

$13 bln 30-year Bond Auction: Yield 4.520% (expected 4.483%); Bid/Cover x2.45 (2009 avg 2.41x, prior 2.26x); Indirect Bidders 40.2% (2009 avg 42.8%, prior 44.0%)

-

Fed's Duke says lenders have tightened terms so much that lack of credit availability a partial impediment to homeownership - Reuters

-

November Treasury Budget -$120.3 bln vs -$131.6 bln consensus

-

America Is Massively Slowing Its Debt Binge

http://www.businessinsider.com/actually-america-slowing-its-debt-binge-2009-12

Ses suhtes täitsa õige, et majandussurutise ajal, kui ärid ja eraisikud ei laena, riik laenab ja stimuleerib majandust. Järgmine tark samm oleks headel aegadel võlg tagasi maksta... aga selles ma natuke kahtlen.