Börsipäev 22. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Head kalendritalve algust kõigile! Kui S&P500 indeksil jäi eile kõrgeim tipp alates 2008. aasta oktoobrist napilt veel tegemata, siis Nasdaq100 spurtis veenvalt uutele tippudele alates 2008. aasta septembrist.

Tund aega enne USA turgude avanemist teatatakse USA 3. kvartali SKP kasvu muutus - sedapuhku siis kolmas prognoosi korrigeerimine (ootuseks +2.8%). Kell 17.00 teatatakse USA novembrikuu olemasolevate elumajade müüginumbrid - ootuseks 6.25 miljonit, mis tähistaks võrreldes oktoobris nähtud 6.1 miljonilise näiduga ca 2.5%list kasvamist.

Eelturul on S&P500 indeksi futuurid ca 0.3% plussis, Nasdaq100 futuurid ca +0.4% ning nafta ca +0.4%. -

Moody'st Kreeka valitsuse lubadused võlakoorumust vähendada ei veena:

Moody’s Investors Service has today downgraded Greece’s government bond ratings to A2 from A1. Today’s rating action concludes the review for possible downgrade initiated by Moody’s on 29 October 2009. The outlook is negative.

Lühiajalisi likviidsusriske siiski ei kardeta:

“Moody’s believes that Greece is extremely unlikely to face short-term liquidity/refinancing problems unless the European Central Bank decides to take the unusual step of making the sovereign debt of a member state ineligible as collateral for bank repurchase operations — a risk that we consider very remote,”

-

Kreeka 10a võlakirjade tulusus liikus downgrade'i peale päevasiseselt üle 6% (esimest korda alates märtsis), mis nüüd on juba ca 280 baaspunkti kõrgem Saksa 10a võlakirja tulusust.

-

Briti kinnisvaraehitajate perspektiive näeb paremas valguses ka Goldman, kes tõstab Barratt ja Taylor Wimpey aktsia valuatsiooni tõttu osta peale ja säilitab Berkeley Groupi puhul osta reitingu. Eelmisel nädalal kommenteeris Citi samasuguse soovitusega Baratt Developmentsi, Taylor Wimpey'd ja Redrow'd. Viimase puhul on analüüsimajad siiski erimeelel, kuna Goldmani arvates tuleks aktsiat müüa. Marketwatchi vahendusel:

After underperforming the FTSE 100 by 24% over three months, and trading below 1.0x book, we believe the valuation of the U.K. housebuilders is now more reasonable, although returns may remain depressed for at least two years," it said. Long-term affordability and limited mortgage availability will weigh on U.K. house prices through 2010, the broker said.

-

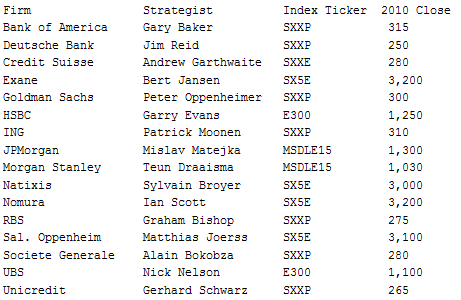

Bloombergi kokkuvõtte järgi näevad strateegid Euroopa aktsiaturge järgmisel aastal kõrgemal. Erandiks on Morgan Stanley T. Draaisma, kelle sõnul peaks 2010. aastal algav "tightening phase" turud allapoole tooma (Draaisma on hiljutise Thomson Extel uuringu järgi Euroopa investorite poolt enim hinnatud strateeg. Draaisma nägemust Euroopa turgude kohta saab näha nt siit).

-

Sai ka soetatud pikema perspektiiviga Bank of America aktsiat. Loodan, et oli hea otsus

-

Bank of America tundub ka Äripäeva lemmikaktsia olevat.

-

USA 3. kvartali SKP qoq annualiseeritud kasvuks kolmanda hinnangu järgi siis 2.2% vs oodatud 2.8% (teine hinnang oli 2.8% ja esimene hinnang 3.5%).

Ehk siis Q3 09 kasv:

3.5%->2.8%->2.2% -

Euroopa turud:

Saksamaa DAX +0,23%

Prantsusmaa CAC 40 +0,51%

Inglismaa FTSE 100 +0,80%

Hispaania IBEX 35 +0,37%

Rootsi OMX 30 +0,81%

Venemaa MICEX -0,78%

Poola WIG +0,37%Aasia turud:

Jaapani Nikkei 225 +1,91%

Hongkongi Hang Seng +0,69%

Hiina Shanghai A (kodumaine) -2,32%

Hiina Shanghai B (välismaine) -1,53%

Lõuna-Korea Kosdaq -1,02%

Tai Set 50 +1,54%

India Sensex 30 +0,55% -

Upbeat Action at the End of a Bizarre Year

By Rev Shark

RealMoney.com Contributor

12/22/2009 8:07 AM EST

What you need to know about the past is that no matter what has happened, it has all worked together to bring you to this very moment. And this is the moment you can choose to make everything new. Right now.

-- Unknown

It is very difficult to offer any great insights about this market right now. Volume is slowing and we are drifting around with a positive bias as market players look to close the books on a very challenging year.

This slow but generally positive trading is exactly what you'd normally expect around the holidays, but this market has been far from normal all year, so it's difficult to be too sanguine. As Jim Cramer comments this morning, this rally has been very easy to miss. We have progressed in a very unusual fashion since the March low. We didn't have the typical sort of advance where we would run a little and then consolidate and then pull back a little and then run some more. We consistently went straight up without seeing any easy entry points.

If you doubted the bullish story at all, you found yourself watching the market run away without you, and this has been a very hard market to trust. All year long it has been extremely difficult to reconcile an upbeat Wall Street with a struggling Main Street.

In retrospect it is easy to see that the market was driven by a flood of liquidity, a weak dollar and interest rates so low that there was no good alternative to invest in but equities. These forces drove the market, so it was a mistake to even try to reconcile the mood of Main Street with the euphoric action of Wall Street.

What I find most striking about the market this year is how often I hear from traders who were struggling with it. Given how much we are up, it is surprising that there is so little celebration about the great year, but over and over I hear how the trading action was atypical and how strategies like momentum and CANSLIM did not work very well.

It has been an unusual year, but we can't spend too much time dwelling on it. We need to focus on the future and how the market will act going forward. Unfortunately, some of the peculiar action is likely to persist because of the massive stimulation and debt that has been racked up. We will need to unwind that at some point, and when we do it will make navigating the market quite tricky.

For now, during the holidays, the market is likely to be rather benign, and we shouldn't try to read much into the action. It bothers me a bit that market players seem so complacent, but the action has been positive and there isn't any good reason to fight it right now.

We have a positive open on the way this morning. The news wires are fairly quiet, but overseas markets were perky and the mood is positive once again. Goldman has raised its target on Google (GOOG) to $670 from $635, and the big-cap technology names look ready to lead for the second day in a row.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: AMKR +9.4%, JBL +7.6%, PRGS +5.3%, NAV +3.3% (light volume)... Select oil/gas related names showing strength: TOT +2.3%, RDS.A +2.1%... Select European drug names trading higher: AZN +1.6%, SNY +1.5%, GSK +1.4%... Select solar names ticking higher in early trade: CSIQ +2.4%, STP +1.5%, JASO +1.1%, ENER +1.1%... Other news: AVII +12.8% (reports systemic treatment with AVI-4658 demonstrates RNA exon skipping and dystrophin protein expression), ATHX +12.5% (continued momentum from yesterday's 100%+surge higher; upgraded to Buy at WBB Securities), VICL +7.2% (announces the issuance of U.S. Patent No. 7,628,993 covering DNA vaccines for herpes simplex virus type 2), ARNA +7.0% (submitted a New Drug Application to the FDA for lorcaserin), CLRT +6.9% (Clarient acquires Genomics in all stock merger valued at up to $17.6 mln), CBAK +4.6% (announces its Tianjin Facility has begun to execute a contract with Jilin Hi-tech Electric Vehicle), YRCW +4.5% (gets approvals for debt-for-equity offers), CYBX +4.1% (still checking), PDLI +2.9% (announces new licensing agreement with Eli Lilly), RTP +1.9% (checking for anything specific), NBG +1.8% (Moody's cuts Greece ratings; the one-notch downgrade was less than many investors had expected), AMGN +1.9% (still checking), UN +1.7% (Unilever NV close to announcing it is replacing WPP for its crucial mainland China account - UK Mail Online), RRC +1.2% (Cramer makes positive comments on MadMoney)... Analyst comments: REXX +4.7% (target raised to $16 at KeyBanc Capital Mkts following recent property transaction in the Marcellus shale), AMTD +2.4% (upgraded to Outperform at Keefe Bruyette).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: CMC -6.6%, TWI -2.7%... Select fertilizer names showing weakness: POT -1.9%, IPI -1.7%, MOS -1.6%... Select European financials pulling back: AIB -9.2%, ING -3.3%, RBS -2.3%, BCS -1.3%... Other news: FIG -4.1% (Fortress Investment sues law firm over loss - WSJ.com), TTWO -3.5% (confirms sale of Jack of All Games Unit to SNX; lowers Q1 and Y10 revenue guidance), HOLX -1.2% (announces decision in patent infringement suit against SenoRx brought by Hologic, Cytyc, and Hologic L.P.; jury has returned a verdict in favor of SenoRx)... Analyst comments: MNKD -8.4% (Concerns surround AFRESA PDUFA date - Oppenheimer), GIGM -2.5% (downgraded to Hold at ThinkEquity and downgraded to Hold at Roth), IMAX -1.5% (downgraded to Hold from Buy at Morgan Joseph). -

November Existing Home Sales mln 6.54 mln vs 6.25 mln; M/M change +7.4%

-

Ja Ford teeb uusi tippe.

-

Senate votes on health bill, debt ceiling set for Dec 24 - DJ