Börsipäev 29. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

Eilne FOMC kohtumine ei toonud muutust senisesse monetaarpoliitika seisukohtadesse ega ka indikatsiooni, et lähiajal kavatsetakse turgudelt likviidsust kokku korjama hakata. Küll aga oli komitee võrreldes varasemaga veidi optimistlikum kasvuväljavaate suhtes, tõstes marginaalselt oma arvamust nii tarbimise, tööjõuturu kui ka kinnisvara osas. Ainsana jäi hääletamisel taaskord eriarvamusele Thomas Hoenig, kelle arvates võib keskpanga lubadus hoida intressimäärasid pikemat aega erakordselt madalal tasemel tulevikus uute makromajanduslike probleemideni ning limiteerib komitee paindlikkust intressimäärade tõstmise alustamisel. SP500 tegi pärast FEDi sõnumit kerge hüppe ülespoole, kuid andis osa sellest päeva lõpuks siiski ära, sulgudes 0.65% kõrgemal.

-

Lisaks Euroopa arengutele täna sentimenti mõjutamas ka USA esmaste ning kestva töötuabiraha taotlejate arvu avaldamine kell 15.30. Eelmisel nädalal näitas initial claims taaskord vähenemist pärast kehenädalast kasvu, taandudes 480 000 pealt 456 000 peale, mis osutus konsensuse 450K ootusest siiski suuremaks. Möödunud nädala numbriteks ootab konsensus seekord marginaalset langust 445 000 peale ja kestvate abiraha taotluste puhul alanemist 4.646 miljonilt 4.625 miljonile.

-

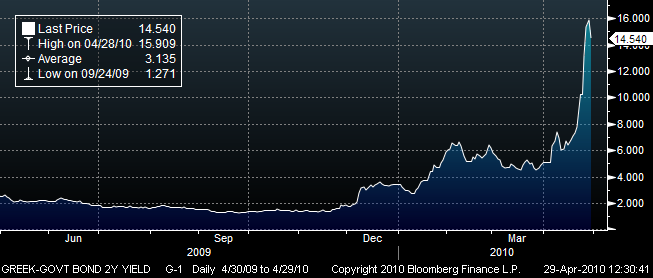

Lisaks sellele, et S&P eile Hispaaniat dowgrade's, hirmutas reitinguagentuur Kreeka võlakirja omanikke, öeldest et viimased saavad oma investeeringutest hinnanguliselt tagasi 30-50% ehk päris selgelt viitamas defaultile. Kaheaastase võlakirja yield olevat hetkeks käinud isegi 26% peal, ent on nüüdseks teinud tagasikäigu 14.5% peale tänu uudistele, et IMF ja EL plaanivad Kreekale kolme aasta peale anda 100-120 miljardit eurot ning antud pakett välistab ühe klausli all ka võlakohustuste restruktureerimise või edasilükkamise.

Kreeka 2a võlakirja yield

-

Kreeka probleemide tõttu on vähem tähelepanu saanud 1Q10 tulemused. Siin üks DB graafik, mis näitab, et S&P500 indeksisse kuuluvate ettevõtete eelmise kvartal tulemused on taas oodatust kõvasti paremad olnud - finantssektori eestvedamisel on EPS siiani koguni 20 protsenti oodatust parem:

-

Deutsche Bank tõstis heade tulemuste peale sellel nädalal S&P500 indeksi aastalõpu sihi 1375 punkti peale, mis peaks olema suuremate analüüsimajade poolt kõrgeim tase (vt teiste analüüsimajade targeteid siit):

Raising S&P 500 EPS estimates & year-end index targets: $84.6($80.8) and 1375 (1325) in 2010; and $95($93) and 1550 (1525) in 2011.

-

LHV Pro idee IMAXi (IMAX) tulemused olid oodatust küll paremad, kuid paljud lootsid ilmselt natuke suuremat üllatust. Tuleviku suhtes on ettevõte jätkuvalt optimistlik:

"While we are pleased to have generated record quarterly financial results, we believe the longer term benefits of titles such as Avatar and Alice in Wonderland to our business transcend a single quarter. Such benefits are perhaps best evidenced by the number of theatre deals we are doing, which will fuel additional growth for the Company over the long-term, and an increased level of tentpole movies being committed to the IMAX theatre network... We believe we have a very strong film slate for 2010, and with yesterday's film deal inked with Warner Bros. and new theatre announcements, we are beginning to paint a picture of 2011 and beyond. We are particularly pleased with the many theatre signings overseas, where our brand is gaining traction and where we see much of our future growth residing, providing a complement to our brand's strong foothold in North America."

Vaatame tulemusi lähemalt ja pikema kommentaari Pro alla paneme homme või järgmise nädala alguses.

-

Baidu (BIDU) saab pärast eile õhtul raporteeritud tulemusi ja spliti teatamist juba neljakohalisi hinnasihte:

Baidu.com tgt raised to $1000 from $728 at Susquehanna

-

Võtsin eile ühe Bidu Puti :)

-

Tööjõuturu numbrid ootustesse. Kuni 500 000ni tuli initial claims hoogsalt allapoole, ent nüüd on juba mitmendat kuud stabiilselt 450K juures püsinud.

Initial Claims 448K vs 445K consensus, prior revised to 459K from 456K

Continuing Claims falls to 4.645 mln from 4.663 mln

-

Gapping down

In reaction to disappointing earnings/guidance: OPWV -19.1%, GMCR -10.8%, AKNS -8.2%, TIS -7.9% (light volume), CVD -7.4%, EK -6.6%, POWI -6.6%, FIRE -6.5%, FICO -6.1% (light volume), DVR -3.7% (light volume), POT -3.7%, LSI -3.6%, RYL -3.3%, ALL -2.9%, CERN -2.8%, TWC -2.6%, ESRX -2.6%, AEA -2.2%, SKX -2.0%, CL -1.9%, VRSN -1.8%, SRDX -1.7%, PG -1.6%, GLBC -1.6% (light volume), SNY -1.5%, XLNX -1.4%, COLB -1.1% (announces commencement of $150 mln public offering of common stock), V -0.9%.M&A news: HPQ -0.5% (HP to acquire Palm for $1.2 bln, $5.70 per share).

Other news: WHI -10.0% (still checking), SNV -8.2% (prices 255.0 mln common shares at $2.75/share), ETFC -6.0% (announces secondary offering of 170 mln shares of common stock), DT -5.6% and DO -1.6% (trading ex dividend), CAGC -1.9% (announces public offering of 1,243,000 shares of common stock).

Analyst comments: VNDA -6.3% (downgraded to Reduce from Buy at Madison Williams), AKS -1.0% (downgraded to Neutral from Overweight at JP Morgan).

Gapping up

In reaction to strong earnings/guidance: IRBT +22.9%, GMET +16.3% (light volume), BIDU +15.1%, NENG +13.8% (also filed for a $40 mln mixed shelf offering), SFI +10.4%, ILMN +10.3%, AKAM +9.9%, AXTI +8.8%, MOT +8.4%, TLCR +8.0% (light volume), GTI +7.7%, DRAD +7.1%, CSCX +7.1% (also comments on FDA AED recall communication), FSLR +6.9% (also upgraded to Outperform at Robert W. Baird, upgraded to Buy from Hold at Deutsche Bank), TSRA +6.8%, OMX +6.2% (light volume), OSK +6.1%, BEC +4.2%, CELG +4.0%, ORLY +3.4%, FTNT +3.2%, HOT +3.1%, OFIX +3.0% (light volume), ITRI +2.7%, HRS +2.4%, CLF +1.8%, COP +1.6%, BEAT +1.4%.M&A news: ATSI +52.9% (ATS Medical to be acquired for $4.00 per share by Medtronic), PALM +26.6% (HP to acquire Palm for $1.2 bln, $5.70 per share; upgraded to Hold from Sell at Kaufman, upgraded to Hold at Morgan Joseph ).

Select financial related names showing strength: AIB +5.0%, IRE +4.6%, NBG +3.0%, AIG +2.5%, STD +2.2%, C +1.8%, BAC +1.4%, GS +1.3%, .

Select solar names higher, boosted by FSLR results: SOLF +4.0%, CSIQ +3.6%, LDK +3.3%, STP +2.8%, JASO +2.8%, ESLR +2.6%, TSL +2.6%, YGE +1.9%, SPWRA +1.8%,.

Select oil/gas related names showing strength: REP +3.8%, TOT +2.2%, RIG +1.4%, STO +1.4%, E +1.2%, SLB +1.2%, PBR +1.0%.

Other news: UWBK +8.8% (files civil complaint against Countrywide Financial Corporation), NVAX +5.8% (Novavax's Seasonal Influenza VLP Vaccine Candidate Shows Positive Results in a Phase II Clinical Trial in Older Adults), UL +3.6% and UN +3.0% (still checking for anything specific), TEF +2.7% (still checking), ABB +1.8% (still checking), JBHT +0.9% (announced that the Board of Directors has authorized the repurchase of up to $500 million of its common stock), .

Analyst comments: SUSQ +1.7% (upgraded to Neutral from Underweight at JP Morgan), ABX +1.1% (upgraded to Buy from Hold at Jefferies),

-

Rev Shark: The Pattern Holds ... For Now

04/29/2010 7:38 AMA foolish consistency is the hobgoblin of little minds, adored by little statesmen and philosophers and divines. With consistency a great soul has simply nothing to do.

-- Ralph Waldo EmersonWhat has been so remarkable about this market for so long is how quickly and easily we recover from every little selling squall. If the market pattern of the past year continues, the indices should go straight up from here and make new highs. The worries we had on Tuesday about European sovereign debt and the Goldman (GS - commentary - Trade Now) fraud charges will be completely forgotten and once again the underinvested bulls will be kicking themselves for not buying aggressively on the pullback.

My theme for quite a while has been that we should assume that the market's pattern of action will continue until we have some clear indication that things have changed. But when a pattern has been as persistent as the quick bounces to new highs, many of us can't help but guess when things will change. It is just common sense that the market pattern will change at some point, but it has been extremely frustrating for those who keep on trying.

What keeps fooling the market skeptics lately is that the bounces after a pullback usually start off slowly. That raises some doubts about the possibility of another "V"-shaped recovery, but then we steadily gain strength and before you know it the shorts are being squeezed again and the underinvested bulls are scrambling to add long exposure.

The pattern has been so consistent for so long that that you almost have to believe that it is going to fail. Normally when a pattern is obvious to everyone, it eventually fails to work as market players move faster and faster to stay a step ahead of each other. They will keep on anticipating a bounce at an early stage until we progress to the point of never pulling back in the first place.

Market players will almost always stick to a pattern until it stops working, and that is what causes the most pain when the character of the market shifts. The folks who count on the prevailing pattern suddenly find themselves poorly positioned when it doesn't occur. As they try to reposition, they feel the other side of the trade, making the move against them even more severe.

I'm absolutely positive that will occur in this market at some point, but I have no idea when that might be. There is no reason to believe that the pattern of sharp bounces back to new highs is going to fail this time. While we are still quite technically extended, the psychology of this market just hasn't shifted much. In fact, earnings are helping to maintain the complacent bullishness that has been in place for so long.

Fears about Greece have cooled a bit, which has Europe in the green and the dollar pulling back. Baidu (BIDU - commentary - Trade Now) earnings and the Palm (PALM - commentary - Trade Now) buyout have some of the momentum money excited, but there were a few soft earnings reports as well. The bulls are in control and we'll see if they can keep the pattern going for what seems to be the 100th time.

No positions.

-

USA futuurid indikeerimas hetkel avanemist 0.3 kuni 0.6 protsendi võrra kõrgemal

Euroopa turud:

Saksamaa DAX +0.52%

Pantsusmaa CAC 40 +0.87%

Suurbritannia FTSE100 +0.70%

Hispaania IBEX 35 +2.29%

Rootsi OMX 30 +1.60%

Venemaa MICEX +1.41%

Poola WIG +1.17%Aasia turud:

Jaapani Nikkei 225 suletud

Hong Kongi Hang Seng -0.81%

Hiina Shanghai A (kodumaine) -1.09%

Hiina Shanghai B (välismaine) -2.44%

Lõuna-Korea Kosdaq +0.26%

Tai Set 50 +0.51%

India Sensex 30 +0.71% -

RBC Capital Mkts notes according to filings, Palm received a 'high level of interest from other serious buyers', however, firm doesn't anticipate a higher bid given: a) superior fit; b) approval by both co boards and Palm mgmt; and c) the highly publicized auction process. PALM tgt to $5.70 from $11.00.

RBC ei oota PALM kõrgemat pakkumist ja suure tõenäosusega $5.70 ka hinnaks jääb. -

Hea näide võimsast kannapöördest. Kui aasta tagasi ei tahtnud keegi spekulatiivsetest võlakirjadest midagi kuulda, siis nüüd:

The riskiest class of corporate bond has inched close to par for the first time since 2007. The high-yield bond market now trades at 99.48 cents on the dollar, according to a Bank of America-Merrill Lynch index, its highest price since the financial crisis hit in 2008 (loe pikemalt siit).

-

U2 frontman Bono is poised to lose out from Hewlett Packard's acquisition of Palm for $1.2bn

Bono’s private equity venture, Elevation Partners, owns an approximate 30pc stake in Palm, having invested $460m in the struggling handset maker in 2007 and 2008. The H-P deal values Palm’s equity at $961m – the rest of the deal price is debt – meaning Elevation’s stake will be worth roughly $320m. -

DNDN sai kuulujärgi Provengele heakskiidu, kauplemine peatatud

-

Dendreon to resume trading at 15:30 ET

-

Today after the close, of the many companies scheduled to report, some of the bigger names include: CSTR, DRIV, EXPE, KLAC, MFE, WFR, SWIR, and WYNN. Tomorrow before the open look for the following companies to report: ACOR, AXL, AIV, AVP, B, CX, CSUN, DISCA, ENDP, DHI, MNKD, and NDAQ.

-

Huvitav, miks BP ca 9% alla tuli?

-

jyrkans, Mehhiko lahes läks põhja BP naftaplatvorm. Kuna tegu väga sügava kohaga, siis on ettevõttel suuri raskusi puurauk sulgeda ja reostus peatada. Ettevõtte enda hinnangul läheb see maksma iga päevaga vähemalt kuus miljonit dollarit, kuid kulud suurenevad pidevalt.

-

Tänan, Mikk

ai ,kurja. Kuulsin alles täna seda uudist ja asi tundub väga tõsine.

Paari nädala pärast lähen sinna kanti, eks võin kohapealt reportaaži teha.

Nüüd ei teagi, mida aktsiatega teha.

Kuna olen turul ostukohti ootamas, siis võib siin selline hetk just tekkida.

Võiks ju uurida, kui suur osa see nende rahavoost on. -

Seni pole teada kui palju kõik kokku maksma võib minna. BP ise on hinnanud, et kulud võivad ulatuda sadadesse miljonitesse dollaritese. President Obama ütles eile Valges Majas, et BP vastutab täielikult reostuse likvideerimiseks kantavate kulude eest ning samal ajal kasutab riik kõiki võimalike vahendeid reostuse kontrollialla saamiseks.

Reostuse ulatust võiks võrrelda 1989 aastal Alaska rannikut reostanud Exxon Valdez´e õnnetusega, mille tagajärjel tuli Exxon Mobilil kanda kulusid 4.3 miljardi dollari ulatuses.

Ridamisi alagtatakse ka kohtuasju nii BP kui ka teiste seotud ettevõtete vastu nn Transocean, Cameron Intl ja Haliburton.