Börsipäev 27. mai

Kommentaari jätmiseks loo konto või logi sisse

-

Eilne päevalõpp vajus USA börsidel ära ning järelturul tundus juba, et karud on taas käppa turule peale saamas, kuid praegune eelturg näitab vastupidist. S&P500 indeksi futuur on juba +1.5% ehk tagasi eilse keskpäeva tasemete juures.

Eesti aja järgi kell 15.30 on täna oodata USA 1. kvartali revideeritud SKP näitajat, kust oodatakse 3.3%list kasvunäitajat varasema 3.2% asemel. Esmaste töötuabiraha taotlejate arv peaks olema ca 455 000 (eelmine kuu oli see üllatavalt kõrge 471 000) ning kestvate töötuabiraha taotlejate arv ca 4.6 mln. -

Eile õhtul teatas U.S. Treasury Department, et on müünud ligi viiendiku neile kuuluvatest Citigroup-i aktsiatest keskmise hinnaga $4.13. Seega peaks ligikaudu 6.2 miljardit aktsiat veel müügijärjekorda ootama. Järgmised 1.5 miljardit aktsiat loodetakse müüa 30. juuniks.

-

Kuidas võiks selline uudis C aktsia hinda mõjutada, eeldusel, et müümist ootav pakk hinda aktsia hinda ei mõjuta? See on hea, et riik positsiooni vähendab kuna riigi kontroll panga üle väheneb, või kuidas? Või riik lahkub uppuvalt laevalt?

-

Riik ei ole huvitatud Citigroupi (C) juhtimisest, mistõttu on pikemas perspektiivis hea, kui ta sellest väljub ja need aktsiad pikaajaliste strateegiliste investorite portfellidesse jõuavad. Kui ka ülejäänud aktsiatele leitaks ostjad ilma hinda allapoole surumata, oleks see C investoritele väga hea uudis, kuna sellega võetaks ära praegu pidevalt Citi peakohal rippuv 'kirves'.

-

Hea uudis ka maksumaksjale, sest need Citi aktsiad ostis riik 3.25 dollariga.

-

seniks - kuniks hind alla selle taseme ei lange

-

Barton Biggs ühineb nendega, kes ootavad lähiajal aktsiaturgudelt korralikku hüpet ülespoole. Link Bloombergi loole.

Biggs: “The market is very, very oversold, and I think we’re going to have a big pop to the upside some time in the next couple of days,” said Biggs. “I wouldn’t be surprised to see us go to a new recovery high, just to make everybody squirm.”

-

Joel,mis kell see GIGM pressikas algab?

-

Eesti aja järgi 14.30 - panen lingi ka.

-

Bill Ackman Has Loaded Up On Citi Shares

http://www.businessinsider.com/bill-ackman-citi-shares-2010-5 -

Euroopas on täna korralik rallipäev ning Euroopa indeksid ca 2% plussis. USA indeksite futuurid on varahommikust saati olnud tõusus ning praeguseks hetkeks kogunenud juba +2.4% tõusu, mis on tõstnud futuurid tagasi eilsete päeva tippude juurde. Ka nafta on ca 2% plussis ja jõudnud $73ni barrelist.

-

Märgilise tähendusega sündmus Apple'i fännidele. Eilse USA sulgemise seisuga on tegu suurima tehnoloogiaettevõttega:

When the New York markets closed on Wednesday, Apple was worth $222bn – short only of ExxonMobil. Microsoft was valued at $219bn.

Apple’s most recent full-year revenue was $36.5bn, close to double the level of three years before but shy of Microsoft’s $58bn. But Apple’s profit margins are wider. Its net income has nearly trebled in three years to $5.7bn, while Microsoft’s profit has only inched forward. (link)

-

Briefing.comis avaldatud analüüsimajade hinnasihtide kergitused:

- Stericycle (SRCL 56.44) upgraded to Hold from Sell at Wunderlich; raises tgt to $50 from $42. Firm continues to believe that sustainable organic growth in the domestic market will slow and regress toward the industry's expected long-term average growth of 5.0%. They believe the alliance with Republic Services may limit further pressure if a strong number-two player emerges in the regulated medical waste market

- BP (BP 42.41) upgraded to Outperform from Perform at Oppenheimer; $55 tgt. Firm believes upside potential is significantly greater than any further downside risk from the oil spill. Firm thinks the current price reflects a worst-case scenario of at least $20 bln in potential financial damages and penalties, which, even if they materialize, are likely to be spread over several years, and, therefore, would not constrain the co financially.

- TAL International Group (TAL 21.86) upgraded to Outperform from Neutral at Baird; maintains $29 tgt. Firm bases upgrade on containerized leasing trends that are very strong and should be sustained into 2011. Additionally, TAL's earnings tailwind should continue as it deploys a record amount of capital in 2010 and benefits from rising lease rates throughout the year.

- Microsoft (MSFT 25.01) upgraded to Outperform from Market Perform at FBR Capital; raises tgt to $32 from $31. Firm notes MSFT is in the midst of a massive product cycle across many of its divisions. Most importantly, they believe the corporate PC refersh cycle is in the early stages and should provide a boost to the co's flagship desktop offerings (Windows 7 and Office 2010). Furthermore, the risk/reward profile is attractive given the underperformance of the shares.

- Hess (HES 51.62) upgraded to Hold from Sell at The Benchmark Company, as they believe the modest premium to their downward revised normalized net asset value estimate appropriately reflects the value of several exploratory interests not currently included in their NAV estimate.

- BRE Properties (BRE 39.31) upgraded to Buy from Hold at The Benchmark Company; $47 tgt. Firm notes shares are trading at a 16% NAV discount, the widest disparity relative to the group in recent memory

- Tenaris (TS 35.67) and Seadrill (SDRL 21.94) upgraded to Buy from Neutral at UBS

- Sterling Bancorp (STL 9.23) upgraded to Buy from Neutral at Janney Montgomery Scott; maintains $11 tgt.

- Cemex (CX 10.52) upgraded to Buy from Sell at Citigroup

- Acergy (ACGY 14.59) upgraded to Buy from Neutral at UBS

-

Ja USA turud alustavad päeva võimsa 2.3%lise plussiga.

Euroopa turud:

Saksamaa DAX +2.11%

Pantsusmaa CAC 40 +1.95%

Suurbritannia FTSE100 +1.77%

Hispaania IBEX 35 +1.67%

Rootsi OMX 30 +1.22%

Venemaa MICEX +1.49%

Poola WIG +0.76%Aasia turud:

Jaapani Nikkei 225 +1.23%

Hong Kongi Hang Seng +1.22%

Hiina Shanghai A (kodumaine) +1.14%

Hiina Shanghai B (välismaine) +2.17%

Lõuna-Korea Kosdaq +2.23%

Tai Set 50 +1.17%

India Sensex 30 +1.70% -

Give the Bulls Room

By Rev Shark

RealMoney.com Contributor

5/27/2010 8:41 AM EDT

Be not disturbed at being misunderstood; be disturbed rather at not being understanding.

-- Chinese proverb

A denial by China that it is selling eurozone sovereign debt has the market bouncing strongly this morning. The mood was looking pretty grim last night as bounce follow-through had failed and we closed at the lows of the day. The sudden reversal this morning has caught a lot of folks leaning the wrong way and we probably have a little short squeeze adding to the upside pressure.

It was rumors that China was selling European debt yesterday afternoon that helped to turn the market down; the reversal this morning takes us back up to almost exactly where we were when the news first hit. Once again the focus will shift to the key areas of overhead resistance which are 1090 and 1100 on the S&P 500. 1090 is the high we hit last Friday and yesterday, and 1100 is the 200-day simple moving average and the intraday low of May 18.

So far this market has been struggling with key areas of overhead resistance, which is exactly what technicians expect. Up until this month, overhead resistance has had little impact on the trading. Once we started to bounce, we'd just keep on gaining. The technical action has been quite different during this correction, which is nice to see -- it gives us some higher-percentage setups to consider.

The challenge of the market right now is trying to balance defensiveness, since we are obviously are in a downtrend, with some opportunistic short-term trading, as the odds of oversold bounces, short squeezes and spikes are quite high. The technical overhead levels give us some guidance in considering how far we might bounce.

Frankly I was surprised we didn't bounce better yesterday, but the market is obviously skittish and the China news caused U.S. shareholders to move to the sidelines in case overseas markets reacted to that news. It sure makes for tricky navigation of this market.

The start this morning is looking very similar to what we had yesterday, so it will be a good test to see if the bulls can build further momentum. It is the end of the month, which also probably helps us to the upside, but I suspect there may be a little nervousness about holding positions over the long weekend.

The bottom line is that this is very tricky trading. We are in trading range between 1100 and 1040 of the S&P 500, and this time, overhead resistance is proving to be a much bigger hurdle than it has been in the past. Give the bulls some room, but look for formidable resistance to develop as we near 1100.

The bounce this morning has trapped some bears, but the bulls need to show us that they can build on their advantage. Lately they have not been able to do that.

-----------------------------------

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: FSII +25.5%, NTAP +7.2%, PAY +5.3%, JAS +4.7%, TIF +3.8% (light volume), CDXS +2.8%, COST +2.5%, NDN +1.6%, DBRN +1.4%, RUE +1.3%.

Select financial related names showing strength: PUK +7.8%, ING +6.5%, AEG +6.0%, RBS +5.4%, PMI +5.4%, NBG +4.6%, BBVA +4.6%, UBS +4.5%, BPOP +4.4%, HIG +4.0%, DB +3.8%, C +3.6%, HBC +3.6%, RDN +3.5%, STD +3.2%, CS +3.2%, BAC +2.8%, GS +1.9%.

Select metals/mining stocks trading higher: BBL +7.0%, MT +6.6%, RTP +6.2%, BHP +6.1%, NG +4.0% (files its first sustainability report), VALE +3.1%, AA +2.4%, .

Select oil/gas related names showing strength: TOT +5.0%, BP +4.8% (discloses "top kill" operations continued overnight and are ongoing; co says no significant events to report at this time; also upgraded to Outperform from Perform at Oppenheimer), REP +4.4%, E +4.1%, STO +3.8%, WLT +3.7%, HAL +3.3%, RDS.A +2.7%, .

Other news: IGC +22.8% (announces $35 million iron ore supply contract with Chinese Mining & Smelting Group), OXGN +13.9% (Data published on OXi4503 that demonstrate potent activity against acute myeloid leukemia), ALXA +6.0% (Staccato Loxapine (AZ-004) reduced signs and symptoms of agitation as early as ten minutes after dosing in patients with schizophrenia or bipolar disorder), DAI +5.1% (still checking), HITK +3.0% (will replace Tractor Supply in the S&P SmallCap 600), QGEN +2.5% and RHHBY +1.8% (reaches settlement over distribution agreement for TheraScreen Companion Diagnostics), AN +1.8% (AutoNation authorizes additional $250 mln for share repurchases), VOD +1.7% (Cramer makes positive comments on MadMoney), PFE +1.6% (announces EMPHASIS-HF trial to halt recruitment due to significant benefit observed in patients treated with Inspra), .

Analyst comments: BCON +11.1% (initiated with a Buy at Ardour Capital), NBS +6.9% (light volume; initiated with a Buy at Maxim), TS +5.8% (light volume; upgraded to Buy from Neutral at UBS), CX +4.6% (upgraded to Buy from Sell at Citigroup), MSFT +3.2% (upgraded to Outperform from Market Perform at FBR Capital), BRCD +2.7% (initiated with a Buy at Citigroup), SBUX +2.4% (initiated with an Outperform at Credit Suisse).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: JMBA -7.2%, MON -4.3%, CSTR -1.3% (updates guidance to include impact from sale of E-Payment Services Business to InComm for $40 mln).

Other news: ZIOP -8.6% (announced that it is offering to sell shares of its common stock in an underwritten public offering ), RMBS -2.8% (ITC extends target date of final determination in Rambus matter regarding NVIDIA products), MCO -3.7% and MHP -3.5% (CNBC reported that fund manager Einhorn said to short the rating agencies). -

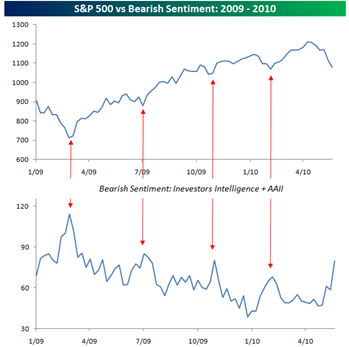

Maikuu eelviimasel kauplemispäeval on näha korralikku tõusu(käive küll üsna tagasihoidlik). Bespoke on hästi näidanud, kuidas Investors Inteligence'i ja American Association of Individual Investorsi küsitluse järgi kiiresti kasvav karune sentiment on viimasel ajal olnud hea ostukoht. Selle järgi on ka praegu hea setup korralikuks põrkeks.

-

Ja S&P500 futuur jõudnud 1100 punkti alla. Eileõhtune müük oli ikkagi lõks karudele. Ja korralik lõks.

-

Kui nüüd alumist graafikut tehnilise poole pealt vaadata, siis kõrgem põhi ja kõrgem tipp. Kõik eelnev ei loe enam. Trend on muutunud. :)

-

Eks täna oli ka kuu viimane kauplemis päev!

-

st homme ikka :))

-

Sassis? Esmasp. on 31 -ne kuupäev?Või on Edisoni mingi tähtpäeva puhul hõõglampidel vaba päev?

-

Seda ma vaatan jah, et ka Mikk ei taha esmaspäeva maikuusse lugeda. Mõtlesin, et äkki mingi püha.

-

31. mail peetakse USAs mälestuspäeva ehk Memorial Day'd ning turud on siis tõesti kinni.

-

Euroopa ju ikka lahti?

-

Euroopa ikka lahti jah.